Built at India’s price point and refined through scale, the company now plans to replicate this template in higher-priced international markets. But as it doubles down on its ambition, the scale that powered its domestic rise could turn into a liability overseas, if execution risk, staffing fragility, and competitive intensity spike, experts warned.

Nonetheless, the company is set to tap the public markets on Wednesday to fund its next leg of expansion. The ₹871-crore initial public offering (IPO) comprises a ₹353.4-crore fresh issue and an offer for sale of ₹517.6 crore. Vuppala, who holds about 11% stake, will not sell any shares.

At the upper price band of ₹460 apiece, the company is seeking a valuation of ₹4,615 crore. At a post-issue price-to-equity (P/E) ratio of 69x, the offer prices NephroPlus at a modest discount to the sector’s average of 75x, according to the company’s red herring prospectus (RHP).

This suggests that while the market is pricing in its scale advantage and growth opportunities, it is also adjusting for the structurally thinner margins of a pure-play dialysis model, said analysts.

Going ahead, NephroPlus’s capital-intensive model and high operating costs could constrain profitability, noted Kunvarji Wealth Solutions. Adding to the concerns is its premium valuation, as Swastika Securities highlighted: based on the latest financials, the issue appears aggressively valued and is best suited for long-term investors with a higher risk appetite.

Overseas capacity boost

Despite these concerns, NephroPlus is doubling down on capacity expansion. The IPO proceeds will fund the opening of 169 clinics by 2027-28—17 of which are slated for the current fiscal—helping it deepen its presence across India while expanding abroad.

As of 30 September 2025, it operated 519 clinics across four countries, including 468 centres in 288 cities in India and 51 overseas, including roughly 30 in the Philippines, after bouts of inorganic expansion, 16 public-private partnership (PPP) clinics in Uzbekistan, and a few in Nepal, with a Saudi Arabia joint venture expected to begin operation soon.

As India’s dominant organized dialysis provider, commanding over half the segment’s revenue, NephroPlus is increasingly leaning on its overseas business to boost profitability. International operations accounted for 32% of its 2024-25 operating revenue, which rose to 40% in the first half of 2025-26.

This could inch up to 41-43%, Vuppala told Mint. But he expects India to remain the anchor market, supported by chronic disease prevalence, Ayushman Bharat coverage, growing insurance penetration, and rising middle-class incomes.

The economics help explain this pivot. India’s average revenue per treatment (ARPT) is about $22. In contrast, the Philippines generates around $110 per session, Vuppala said. Uzbekistan’s PPP model yields $48-72.5, while Saudi Arabia reimburses close to $300 per treatment, according to its RHP.

Each market offers a different uplift. In the Philippines, prices rose 45% in October after nearly a decade of no revision. Uzbekistan’s PPP award lowered the state’s dialysis outlay from $60 to $48 per treatment while boosting patient volumes. Launches planned in Saudi Arabia and Kazakhstan aim to extend the same playbook: export a low-cost Indian operating engine into underpenetrated markets with far higher reimbursement ceilings.

This overseas push helps shore up margins in a business defined by low treatment rates and PPP-heavy contracts in India—the biggest structural drag on the company’s long-term profitability, said Vinit Bolinjkar, head of research at trading platform Ventura.

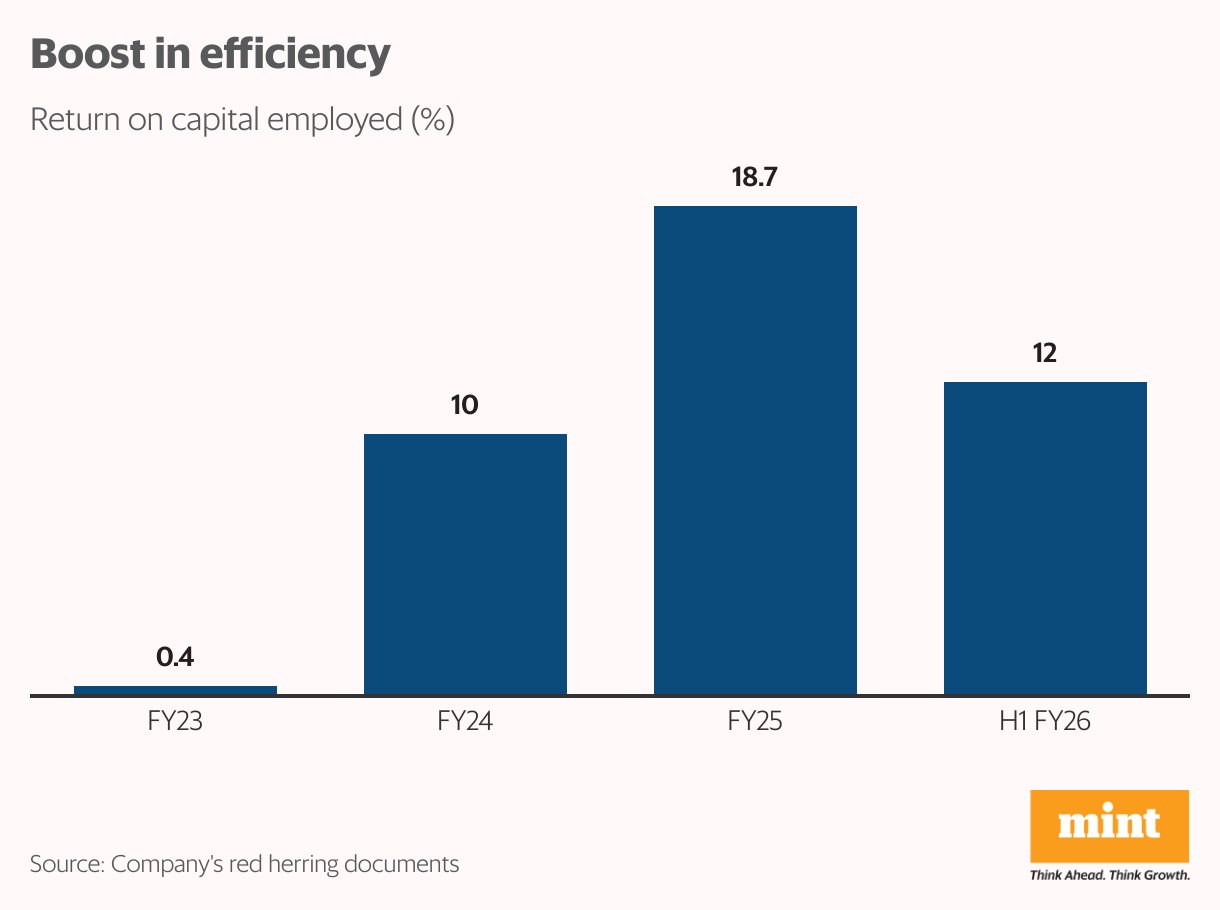

Yet, NephroPlus has wrung out every efficiency gain at home to sustain its margins, almost doubling its return on capital employed in 2024-25 from 10% a year ago. Still, the standout momentum came from abroad, noted Vuppala.

The company’s revenue rose 34% year-on-year to ₹756 crore in 2024-25, while profit almost doubled to ₹67 crore on the back of its Philippines rollout and Karnataka PPP wins, he added.

Double-edged sword

NephroPlus’ global play can be margin-accretive, Ventura’s Bolinjkar said, but only if it successfully handles the grind of expanding and integrating new markets. Investors should closely track overseas growth, Ebitda resilience, and collection levels in reimbursement-led geographies. Meanwhile, Uzbekistan’s PPP performance will be the real test of durability, he added. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

This implies that NephroPlus’ scale is a double-edged sword. Dialysis is a high-touch, daily-care service, and running more than 500 centres introduces operational fragility, noted experts.

Maintaining uniform quality across tier-II and tier-III locations demands consistent technician capability, reliable water and biomedical infrastructure, and tight oversight—factors, according to analysts, will become harder to control as the company adds nearly 170 clinics in the next four years.

Kunvarji Wealth Solutions flagged the business’ inherently high operating costs and dependence on trained healthcare professionals. Vuppala, too, acknowledged that nephrologists remain reluctant to relocate beyond metros, making clinical oversight harder as the network deepens. The chain instead relies on a rolling roster of nephrologists who cover centres beyond big cities on a visiting basis, he said.

Competitive pressure also weighs on pricing. SBI Securities and Swastika Securities noted that PPP tendering remains aggressive, while hospital contracts are frequently renegotiated, and these dynamics curb ARPT growth both at home and abroad. Working-capital strain adds another layer, with SBI highlighting delayed PPP payments and longer reimbursement cycles in international markets.

Investor sentiment mirrors this push-and-pull. NephroPlus’ grey market premium remains flat as of 9 December, a sign of subdued appetite for the IPO, which Ventura’s Bolinjkar pins on rich valuations and a shaky equity market backdrop.