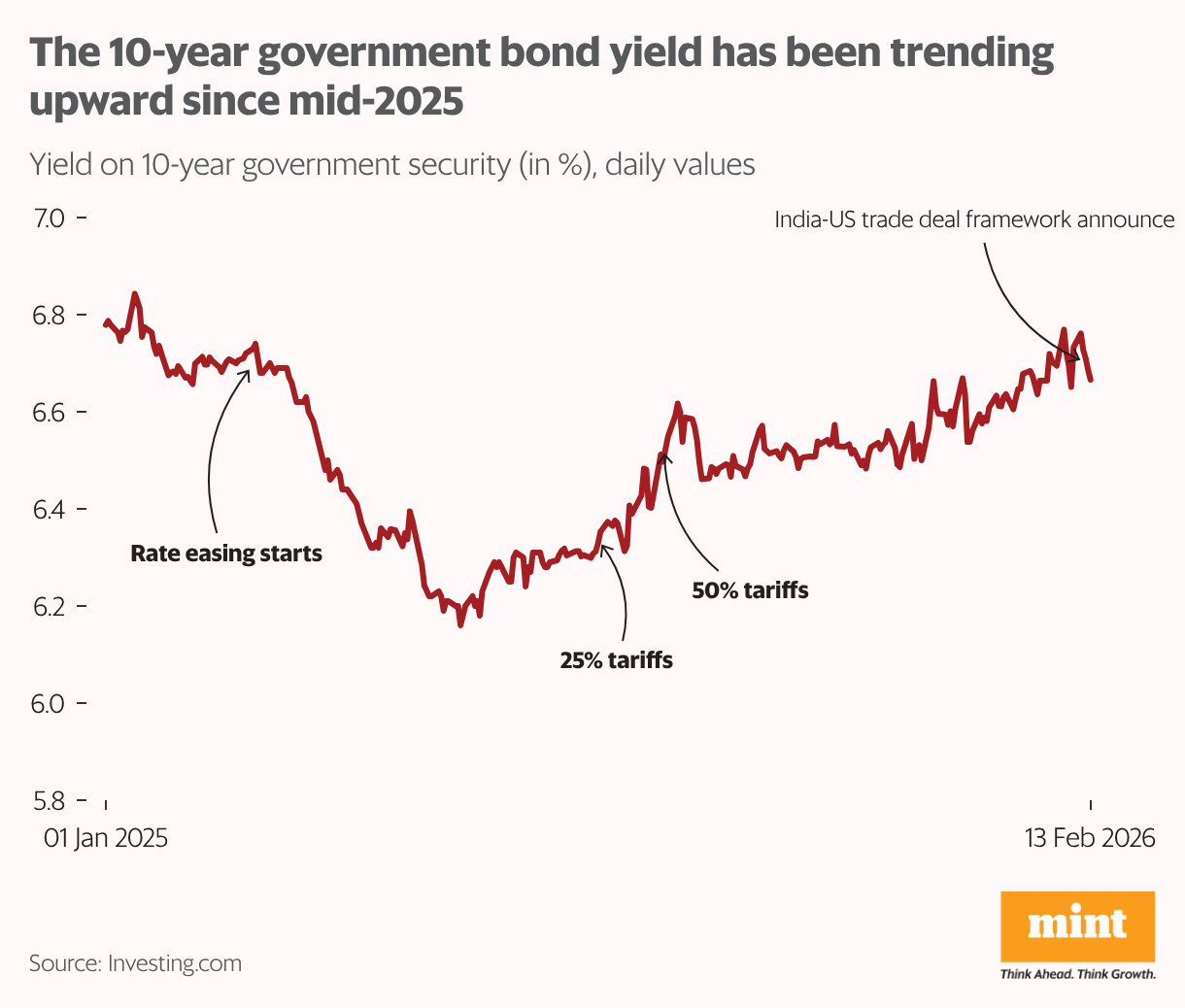

It is even more unusual that the 10-year G-sec yield has barely moved over the past year, despite a 1.25% cut in the policy repo rate. In previous rate-easing cycles, the 10-year benchmark yield tended to fall significantly, especially towards the end of the cycle. But this time, G-sec yields are stubbornly high.

Rate cuts, yet high yields

The current easing cycle began in February 2025 with a 25 bps cut. Initially, government borrowing rates fell, shedding around 60 bps by May 2025. But after mid-2025, yields have been on an upward trend, even as the policy rate cuts continued until December 2025. Market experts have put forward various reasons for the upward pressure on G-sec rates, which can be broadly classified into factors that affect debt market operations, the fiscal outlook, and external factors.

In 2025, bond market liquidity was drained by foreign direct investment outflows, sell-offs by foreign portfolio investors, and RBI intervention to support the exchange rate. The Reserve Bank of India (RBI) responded by pumping in massive amounts of liquidity through open-market bond purchases and forex swaps.

RBI’s support kept the market functioning, but could not compensate for the growing mismatch between demand and supply of G-secs. On the demand side, large institutional buyers such as insurance companies and pension funds have cut back on G-secs; the former due to a moderation in premium growth and the latter because regulatory changes permitted greater investment in equity.

Oversupply of debt paper

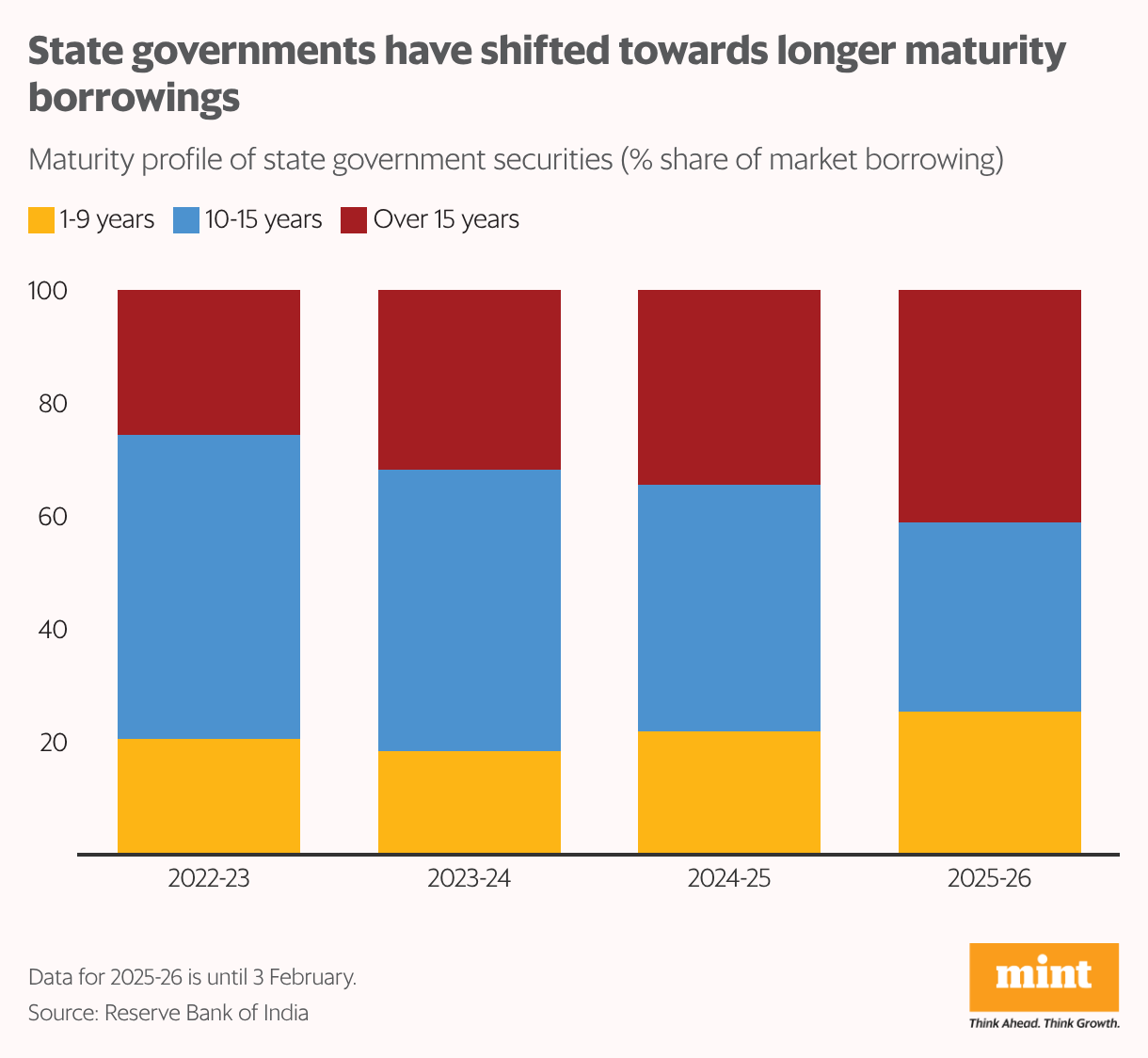

At the same time, there is an oversupply of government debt paper. The Centre is set to borrow ₹14.7 trillion through dated securities in 2025-26; and a whopping ₹17.2 trillion borrowing is budgeted for 2026-27. States are also flooding the market with debt: at ₹12.5 trillion, their 2025-26 gross borrowing through state government securities (SGS) is 16% higher than the previous year. But it’s not just the amount, markets are also spooked by the maturity profile of debt.

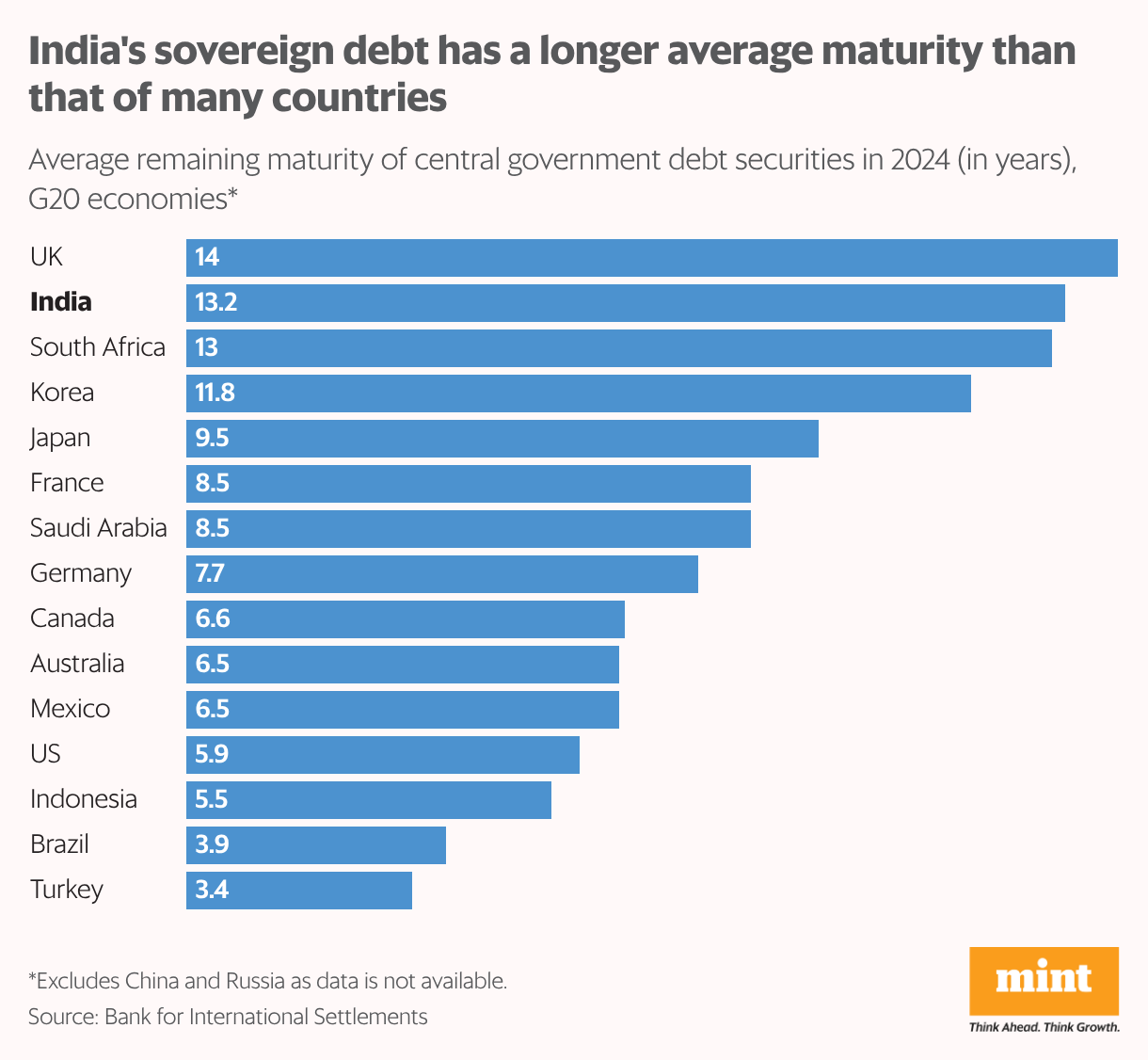

Both central and state governments have shifted towards longer maturity paper; this pushes up yields because investors demand a term premium for holding longer-dated bonds. In fact, Indian sovereign debt has one of the highest maturities among G20 economies.

The lengthening maturity of SGSs is a bigger concern because states have limited sources of tax revenue, which makes them more likely to reduce developmental spending to cover higher interest expenses.

Fiscal consolidation

Unease over debt has cast a shadow over the government’s remarkable fiscal consolidation. The Centre’s fiscal deficit was brought down below 4.5% of GDP by 2025-26 as promised. Normally, markets reward such fiscal discipline with lower yields. But this time, the focus has shifted to general government metrics rather than the headline deficit number.

The collective fiscal deficit of states is expected to be 3.3% of GDP in 2025-26, implying a general government deficit of 7.7% of GDP. The central government debt-to-GDP ratio for 2025-26 was 56.1%, but once we include state debt, the general government debt-to-GDP ratio rises to 85.3% of GDP. That is not as jaw-droppingly high as Japan (230%) or the US (124%). But markets worry more about the future direction of the debt-GDP ratio, rather than its current level.

That explains why yields on Japanese government bonds (JGBs) rose after Prime Minister Sanae Takaichi’s landslide victory this month: her promises to cut taxes and expand spending threaten to increase the already-high national debt.

For investors tracking government debt, there are three areas of concern about India’s fiscal outlook. One, recent cuts in GST and personal tax rates will certainly reduce tax revenue from these sources, but there is no guarantee that it will stimulate a consumption-led recovery. Two, several states have introduced freebies (farm loan waiver, free electricity, cash transfers to women, subsidized transport) without any plans to increase revenue; this is likely to worsen their future deficit.

Finally, the external environment poses downside risk to growth, and by extension, to debt capacity. The connection between growth and debt is straightforward: a country can run a primary deficit provided its nominal growth rate is higher than the interest rate on government debt. This was never a problem in past years, when the economy grew at double-digit nominal rates, and the average government borrowing rate rarely crossed 9%.

However, in 2025-26, nominal growth dipped to 8%, dangerously close to the 7.2-7.5% interest rate on G-secs. Nominal growth is expected to recover to 10% in 2026-27, but markets are wary. If the tariff situation worsens and puts India’s trade at a disadvantage, growth may fall by enough to threaten debt sustainability. In an uncertain world, that risk is enough to put a floor under government yields.

The author is an independent writer in economics and finance.