For the Akzo Nobel group, the divestment is part of a broader strategic portfolio review aimed at focusing efforts on leading positions in key global coatings markets. The deal, which is awaiting regulatory approvals and a mandatory open offer for the remaining 25% held by the public, is expected to close by the end of 2025.

This has breathed fresh life into Akzo, which had corrected by more than 25% from its peak in October 2024. The counter rallied by more than 7% on Friday following the announcement.

But how will this play out for JSW?

Small fish set to make it into the big league

Akzo Nobel India is a subsidiary of a Dutch-based multinational company that has been operating in India for more than seven decades. Its Dulux is a household brand in the country.

In contrast, the unlisted JSW Paints, backed by the $23 billion cement-to-steel conglomerate JSW Group, joined the paints sector in 2019. It had been piling on losses until FY24. Even in FY24, when it reported ₹2,000 crore in revenues, 60% of that had come from the JSW Group itself.

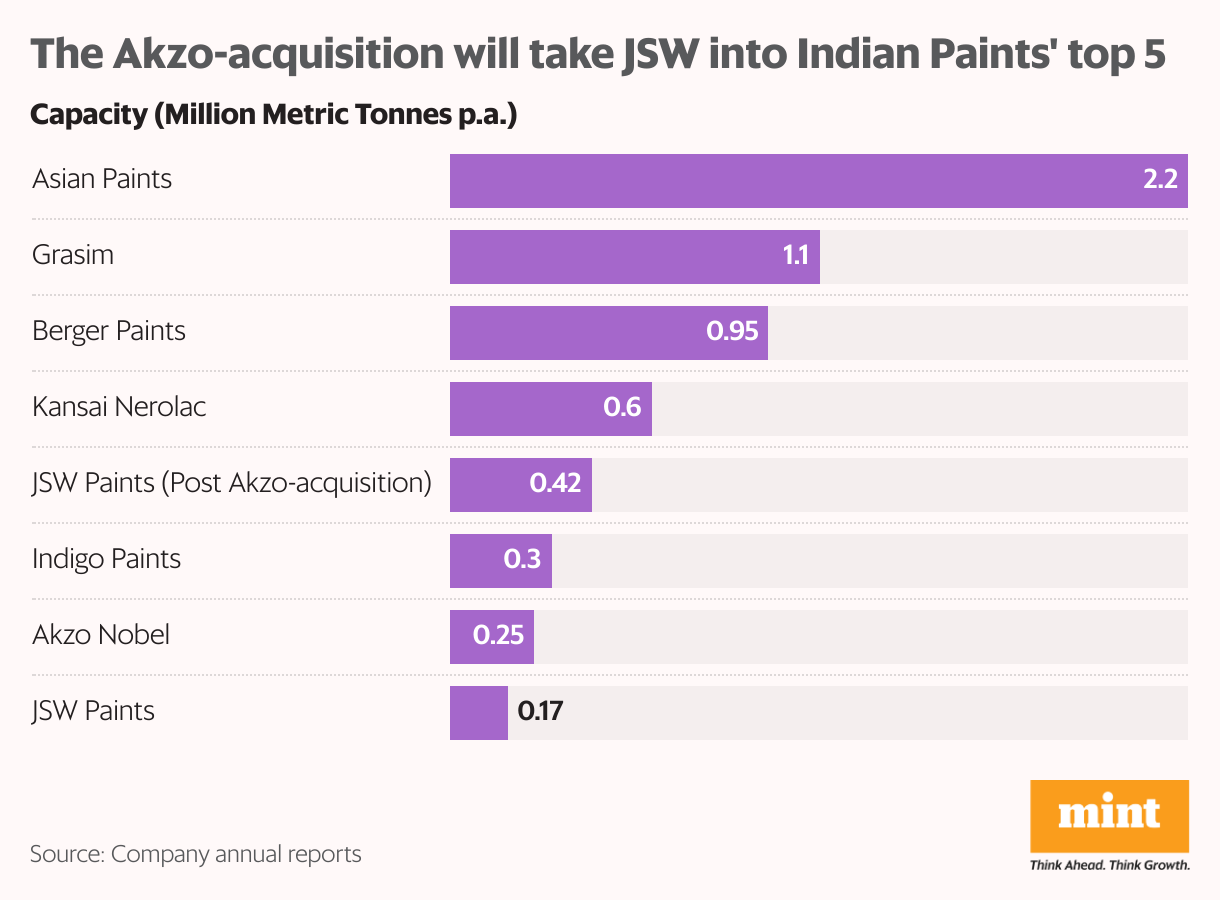

When it comes to production capacity, Akzo is bigger than JSW. With the acquisition of Akzo’s 0.25 MMTPA capacity, JSW is set to climb into the big league as one of the top five paint players in India.

JSW to become a serious paints player

So far, JSW has largely remained a captive paint manufacturer for the JSW Group. Even after five years of operation in the industry, around ₹1,200 crore of its ₹2,000 crore revenues clocked in FY24 was driven by industrial paints supplied to JSW group companies.

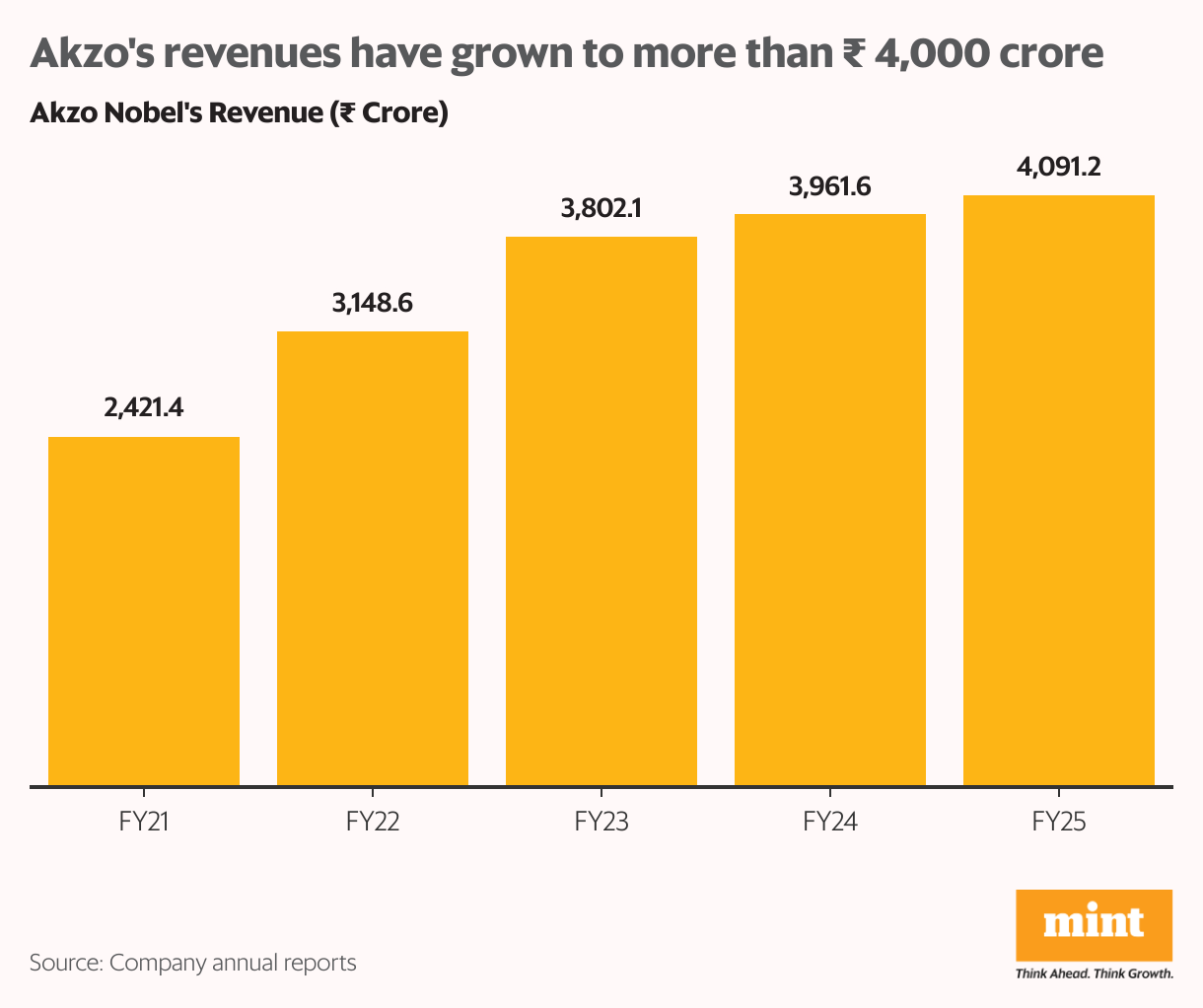

On the other hand, Akzo Nobel India has five manufacturing plants and two RD&I (research, development, and innovation) centres in the country. It reported more than ₹4,000 crore of revenues in FY25, recording a compound annual growth rate (CAGR) of 14% in sales between FY21 and FY25.

The acquisition is expected to triple JSW Paints’ business to ₹6,000 crore, and help the combined entity claim about 10% of the industry’s revenue market share.

Looking beyond scale

JSW has been able to manage only about ₹800 crore in annual revenues from clients outside the JSW Group, presumably in decorative paints. This is in contrast to the broader industry, which derives almost three-quarters of its revenues from decorative paints.

The acquisition of Akzo’s business, which is reported to have 45% exposure to decorative paints, can tilt the scale in favour of JSW Paints. The higher share of industrial paints versus the industry can lead to faster growth amid subdued demand for decorative paints. Take Akzo’s Q4 FY25 performance, for instance. It registered double-digit growth in its business-to-business vertical, but overall revenue growth was pulled down to 5% due to muted demand in mass and economy decorative paint categories amid rising competition.

While rural demand has picked up, urban demand is expected to eventually follow suit. This would give a leg up to decorative paints, thereby weighing on JSW’s prospects. But one can hope that by the time the demand environment looks up, with its newfound economies of scale, JSW Paints is able to double down on its focus on distribution, marketing and innovation to carve a niche for itself.

Distribution and innovation might

JSW is also acquiring a wider reach through the more than 22,000 distribution points of Akzo across the country. These include its experiential stores inaugurated recently in seven states. The acquisition of listed Akzo Nobel also leaves the door open for a reverse merger to take JSW Paints public without the hassle of an initial public offering.

While powder coatings and Akzo’s international research centre have been excluded from the deal, Akzo has committed to technologically partnering with JSW for India’s liquid coatings industry. Akzo’s innovation is apparent from its recent product launches, including the Wanda Easy RM Basecoat, a fast-drying ready-mixed basecoat for automotive and speciality coatings, and its climate-friendly Low-E (low cure) range of Interpon powder coatings.

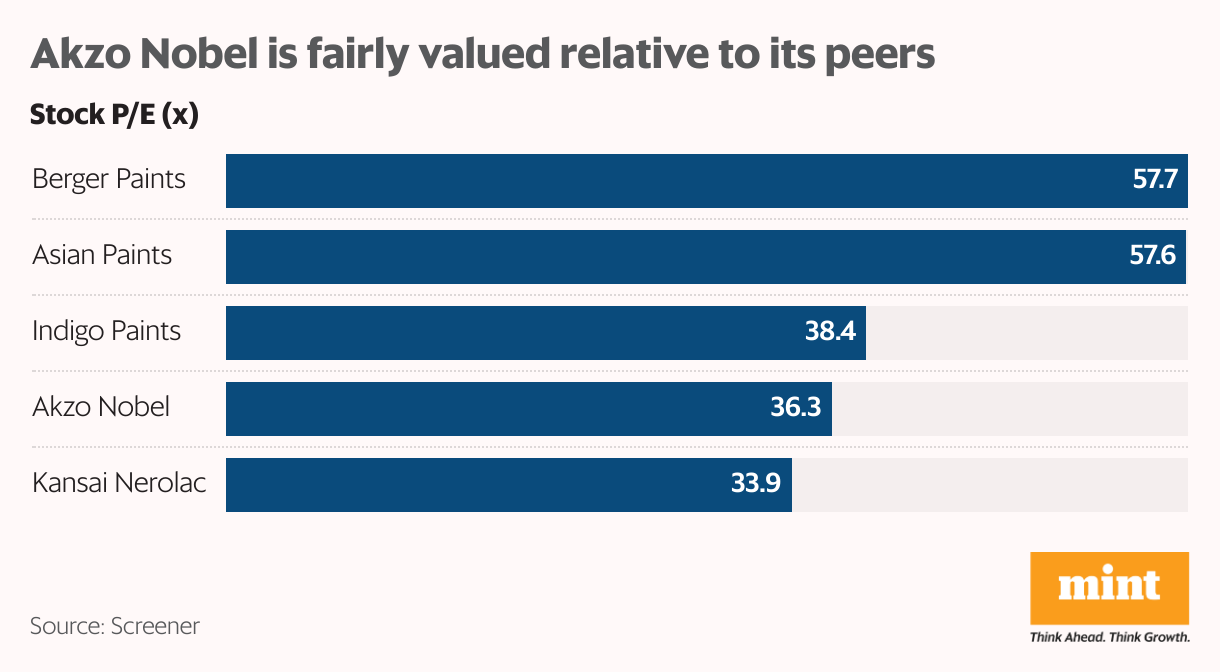

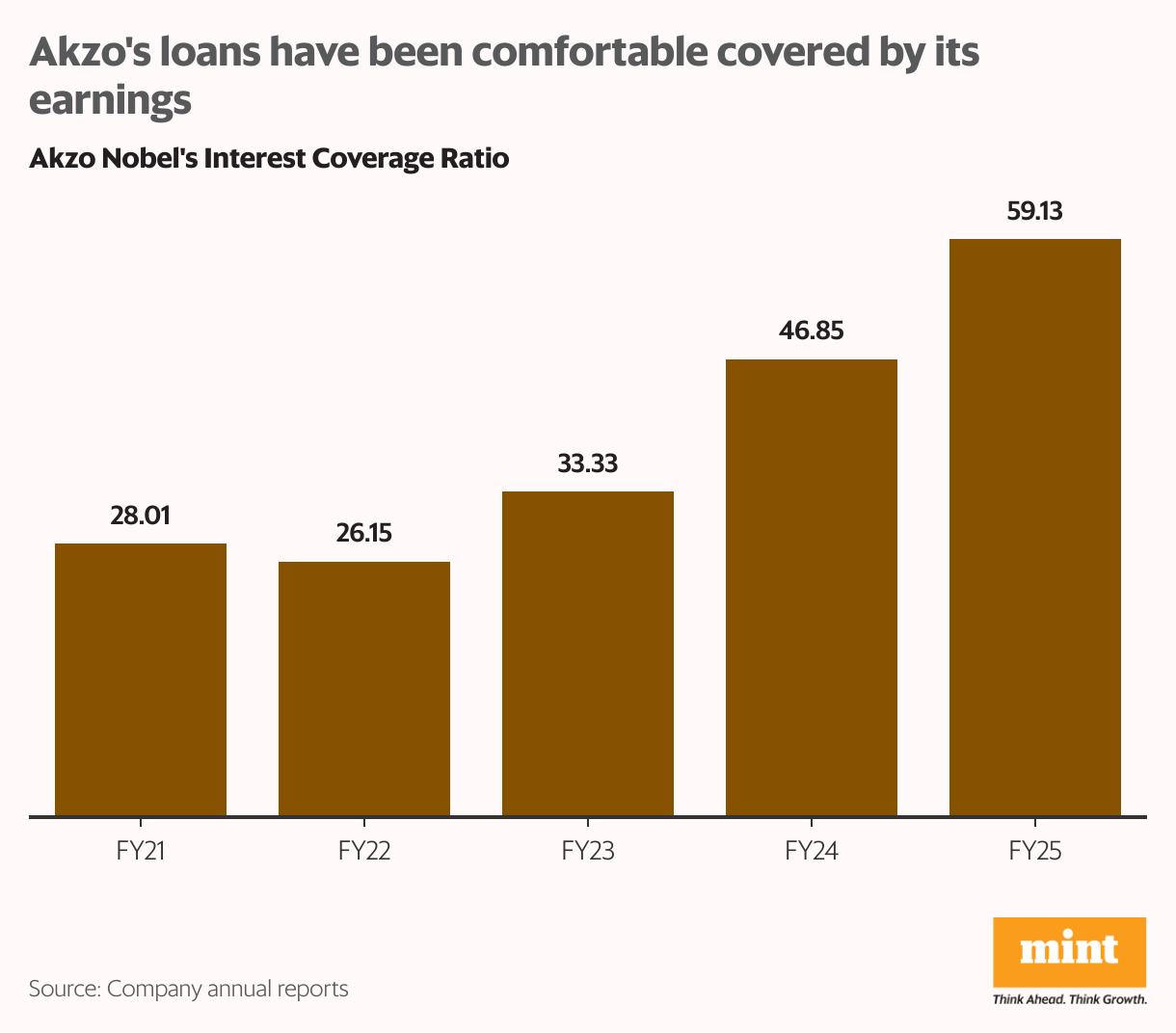

This is all at about a 15% discount to Akzo’s market price, which was, anyway, fairly valued relative to competitors. Furthermore, Akzo Nobel India has negligible long-term debt, and its working capital loans have been comfortably covered by its earnings. This is to say that, leaving aside the acquisition cost, Akzo’s business will not add significant debt to JSW.

The acquisition is likely to be funded with debt amounting to ₹4,000 crore. But this will show up on the books of the JSW Group.

Industry forces

India’s paints industry is valued at around ₹60,000-90,000 crore, depending on whether we look at it from the revenue or capacity lens. With rising disposable incomes, sustained revival in rural demand, an imminent recovery in urban demand, and premiumization, the market is expected to grow to ₹1,40,000 crore over the next five years. The government’s infrastructure push and initiatives on affordable housing can accelerate this.

But with the entry of new players in the industry, such as Pidilite and Grasim, and their aggressive pricing, marketing, and distribution strategies, incumbents have lost some market share, and their margins have come under pressure as well. Muted demand and rising prices of raw materials have made matters worse.

Large incumbents are allegedly using pressure tactics to prevent their dealer network from engaging with the new players. The Competition Commission of India has also been involved and is looking into allegations of unfair trade practices.

The consolidation with JSW’s acquisition of Akzo will heat up competition further. But from JSW’s point of view, it has strengthened its position in the jungle.

Problems that the acquisition won’t solve

Asian Paints leads the market by a huge margin with a claim on more than 50% of the market share. Berger Paints is a distant second with less than 20% share. Grasim and Kansai Nerolac rank next with 6-12% share each.

Post-acquisition, JSW Paints will gain a significant lead with around 10% share of the market. But with a bulk of the market still controlled by Asian Paints, the industry can be expected to continue struggling under competitive pressure despite any consolidation among the smaller players.

Of course, similar to what has been seen in the cement sector, more consolidation can be on the horizon for paints as well. Furthermore, aggressive investments planned by smaller incumbents can tilt the power balance away from Asian Paints.

Whether JSW Paints is able to keep up amid such aggressive organic and inorganic expansion will have to be seen. Meanwhile, how their nascent profitability evolves will be a key monitorable. If JSW has to carve its niche, it will need to focus on marketing, distribution, and innovation, and closely follow the inorganic expansion.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.