But Polycab’s first-quarter earnings present a more nuanced picture. Rather than showing signs of defensive positioning ahead of competitive threats, the company’s strong performance suggests the situation may be more complex than the paint industry analogy implies.

When conglomerates circle

The market disruption fears began in February 2025 when UltraTech Cement unveiled plans for a ₹1,800 crore investment over two years to establish a significant presence in electrical cables. The Adani Group followed in March with its own entry announcement. Polycab’s stock fell over 6% the day after Adani’s revelation, as investors anticipated a repeat of the paint industry carnage.

The paint industry precedent loomed large. Birla Opus had systematically leveraged UltraTech’s extensive cement dealer network to capture market share, sending Asian Paints’ margins down 480 basis points as market share fell from 59% to 52% in just 12 months.

The disruption succeeded because it exploited structural vulnerabilities. The industry’s four-player oligopoly—Asian Paints, Berger Paints, Kansai Nerolac, and AkzoNobel—has nearly 70% dealer overlap with cement distribution, making rapid market penetration possible. Birla Opus could immediately access established relationships and compete on price.

Cables ain’t paints

The cable industry presents fundamentally different challenges that make the paint disruption playbook less applicable. Timeline reality alone suggests a multi-year horizon: Three to five years to build manufacturing plants, five to eight years for brand credibility establishment, plus stringent regulatory approvals for electrical products.

More critically, the cable industry operates across 400+ fragmented players, requiring specialized distribution networks and technical expertise that cement sector relationships might struggle to provide. Electrical contractors and distributors need comprehensive product education, technical support, and application guidance—services that go far beyond competitive pricing strategies.

The technical complexity of electrical cables, combined with safety regulations and certification requirements, creates natural barriers to entry absent in the relatively straightforward paint industry. Cable specifications must meet precise electrical standards, fire safety requirements, and durability benchmarks requiring years of manufacturing expertise.

Polycab’s Q1 defiance

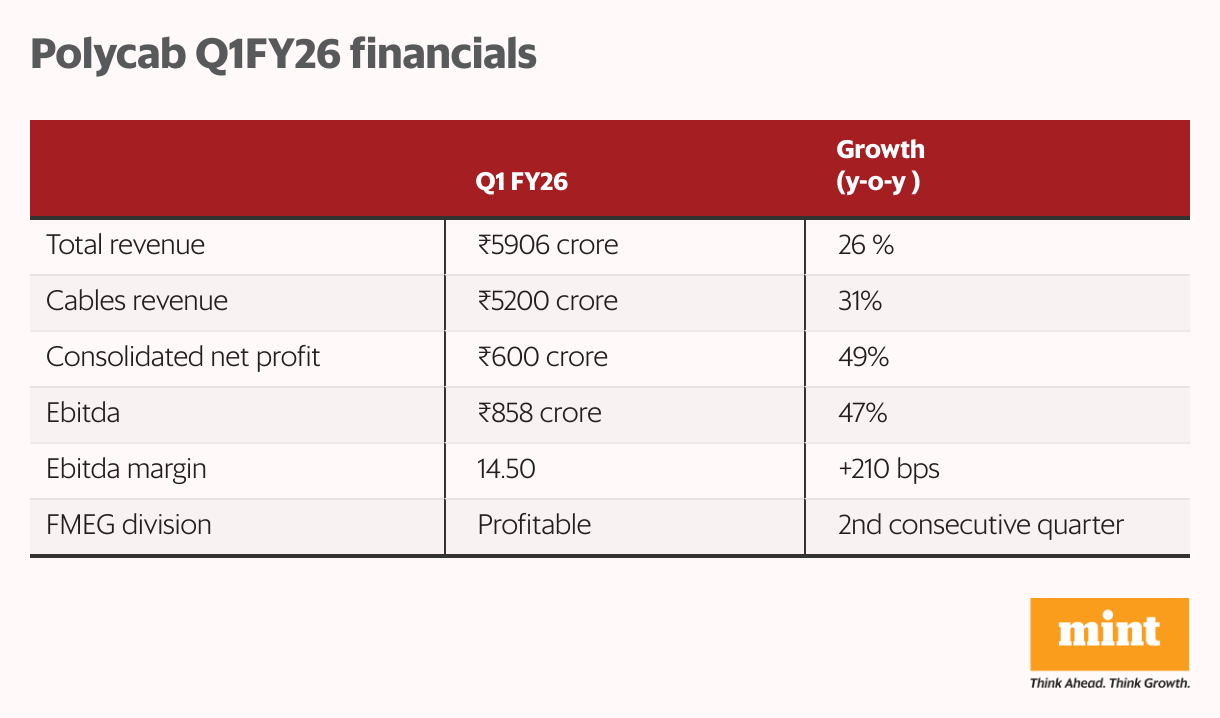

Polycab’s first-quarter results showed solid numbers. These suggest that near-term competitive impact may be limited, at least until the capacities of Adani and UltraTech go live and create actual competitive headwinds.

Revenue in the June quarter grew 26% year-on-year (y-o-y) to ₹5,900 crore, with the core cables business advancing 31%. Consolidated net profit reached ₹600 crore as Ebitda increased 47%, with Ebitda margins expanding 210 basis points to 14.5%. Ebitda is short for earnings before interest, taxes, depreciation, and amortization,

Cables revenue reached ₹5,200 crore, up 31% y-o-y, with domestic growth at 32%, indicating the company maintained strong momentum in its home market despite the competitive announcements. The fast-moving electrical goods (FMEG) division achieved its second consecutive profitable quarter, while solar products doubled to become Polycab’s largest category in that segment.

Integration creates defensive moats

Polycab’s resilience reflects structural advantages that Asian Paints never possessed. The company operates an integrated electrical ecosystem, systematically cross-selling switches, lighting fixtures, fans, and solar equipment alongside cables. This integration creates significant switching costs for customers and generates multiple revenue streams from single customer relationships.

The integration strategy accelerates at an opportune moment in India’s infrastructure development cycle. Polycab’s solar revenue doubled as India targets 500GW renewable capacity by 2030, positioning the company to benefit from the country’s green energy transition. Manufacturing synergies mean quality copper processing capabilities serve both cable and motor applications, while safety certifications and technical expertise transfer across multiple product lines.

The cable market’s projected growth at 8%-9% annually over the next few years fundamentally changes competitive dynamics. When markets are expanding rapidly, established leaders can grow alongside new entrants rather than engage in zero-sum battles for market share.

Real challenges ahead

While Polycab’s Q1 results are impressive post the announcements by these giant conglomerates, it’s crucial not to be swayed by just one quarter’s performance. The market will start re-calibrating valuations as the true impact of these changes becomes more visible in the coming quarters, as and when project updates arrive from UltraTech and Adani.

That Polycab faces genuine competitive threats cannot be emphasized enough. UltraTech brings substantial financial resources and established relationships throughout India’s construction industry that could prove valuable in cable distribution. The company’s experience in building and managing large-scale manufacturing operations provides operational advantages that shouldn’t be underestimated.

Pricing pressure will inevitably intensify as new capacity comes online over the next three to five years. Some margin compression seems inevitable as competitors establish manufacturing presence and begin competing for market share. The construction industry relationships that UltraTech brings could prove particularly valuable in large infrastructure projects where bulk purchasing decisions are made centrally.

The Adani Group’s entry adds another large dimension of competitive pressure, particularly given the conglomerate’s extensive presence in power generation, transmission, and infrastructure development. These existing relationships could provide natural entry points for cable sales, especially in utility-scale projects.

Structure over size

The paint industry taught investors to fear conglomerate entry into established markets, creating a template for disruption fears across multiple sectors. However, the cable industry may teach them that market structure, technical requirements, and defensive positioning matter more than balance sheet size alone.

The cable wars are just beginning, and the ultimate outcome will depend on execution rather than intentions. Polycab’s strong first-quarter performance suggests the company may be better positioned than feared, though sustained competitive pressure over multiple quarters will provide a clearer picture. In markets where technical expertise and integrated solutions matter, financial firepower alone may not guarantee rapid disruption success.

While conglomerate entry deserves serious attention, the specific characteristics of each industry determine whether disruption is inevitable or merely possible. At least for now, Polycab demonstrates that in cables, unlike paints, the incumbent’s defensive advantages may prove more durable than initially feared.

For more such analysis, read Profit Pulse.

Dev Chandrasekhar advises corporations and think tanks on big picture narratives relating to strategy, governance, markets, and policy.

Disclaimer: The author owns shares of Polycab India Ltd. He is not associated in any pecuniary or advisory capacity with Polycab, its owners, its employees, or its competitors. The article is a forward-looking interpretation of publicly available information on strategy and governance; it does not offer any investment advice related to any company. Any factual error, if pointed out, shall be corrected. No liability accepted.