Their secret? Scale, operating leverage, and business models built for massive volumes. Here, single-digit margins aren’t a weakness—they’re a different, equally powerful path to profitability.

This research unpacks three such companies—Dixon Technologies, Avenue Supermarts, and Blue Star—to understand how they consistently turn slim spreads into strong earnings.

Dixon Technologies: Scale over spread

Dixon Technologies has long been a pioneer in India’s electronics manufacturing services (EMS), earning its place as the “brand behind brands.” It assembles everything from TVs and washing machines to smartphones and wearables for global players.

The company’s latest numbers once again highlight the paradox of scale over margins. As a contract manufacturer, Dixon works on razor-thin spreads, but its high-volume, capital-efficient model keeps profits on a steady climb.

Dixon’s revenue nearly doubled to ₹12,836 crore in the first quarter of FY26 from ₹6,580 crore in the same period last year. This growth was driven by strong momentum in its mobile and other EMS divisions, whose revenue rose 125% to ₹11,663 crore. This segment generated a margin of 3.4%, while the consumer electronics and lighting products operated at about 6%.

Home appliances stood out with a higher margin of 11.5%, although its revenue contribution was modest at ₹313 crore, which is not yet enough to move the needle. However, it holds the potential to lift overall margins as the share of home appliances grows.

Ebitda rose 89% year-on-year to ₹484 crore, while profit after tax (PAT) doubled to ₹280 crore from ₹140 crore. At first glance, the numbers look extraordinary, but Dixon’s margins stand razor-thin. Ebitda margin was 3.8%, broadly flat compared to 3.9% a year ago, while PAT margin improved just a shade to 2.2% from 2.1%.

Manufacturing costs account for over 92.5% of Dixon’s revenue, leaving little room for fat margins. Yet, its diversified portfolio across mobiles, TVs, appliances, and lighting allows profits to scale rapidly. High returns back this up—return on equity (RoE) at 49% and return on capital employed (RoCE) at 34%. With working capital at minus four days, Dixon gets paid faster than it spends, ensuring strong cash flows.

The company aims to produce between 42 and 43 million smartphones. The acquisition of a 51% stake in Vivo’s manufacturing unit is expected to boost sales by about 20 million units starting FY27. Dixon also expects to generate ₹7,000 crore in export revenue, up from ₹1,600 crore last year.

Dixon expects significant growth across its non-mobile segments, which are anticipated to help improve blended margin. To this end, it sees a multi-year growth opportunity in the telecom segment. Apart from this, it is increasing the capacity of refrigerators from 1.2 million units to 2 million units, and is also expanding the capacity of other home appliance products.

Avenue Supermarts: Turning inventory into profits

Avenue Supermarts (DMart) has built its empire on a simple philosophy: sell at the lowest price and let volumes do the heavy lifting. Operating on wafer-thin margins, the chain has turned scale and cost discipline into its strongest weapons, making it India’s most successful value retailer.

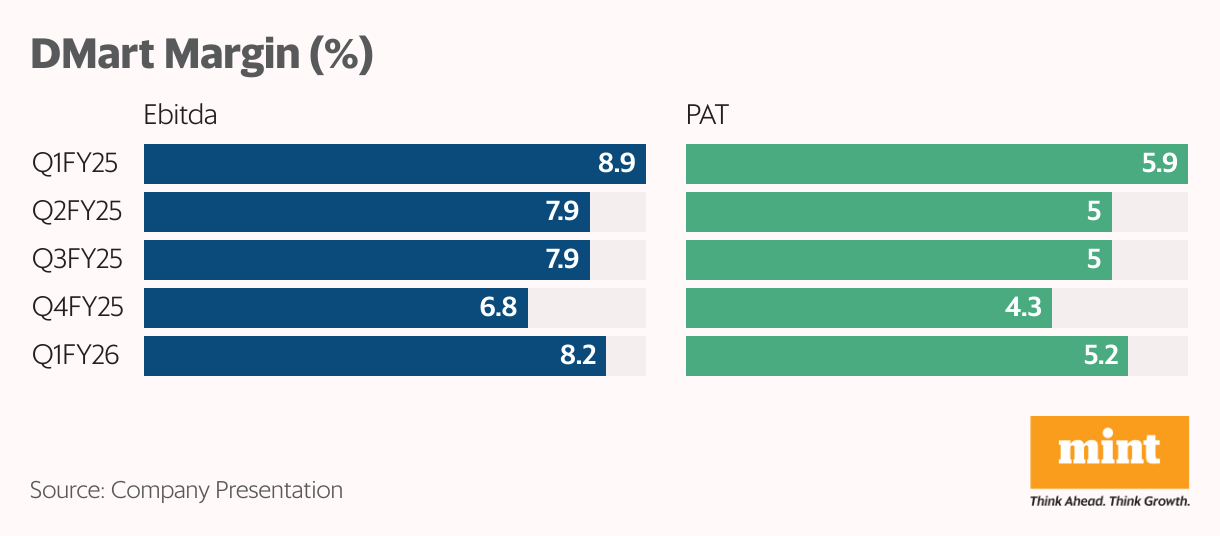

In the June 2025 quarter (Q1FY26), DMart reported consolidated revenue of ₹15,932 crore, up from ₹13,712 crore in the same period last year. Ebitda stood at ₹1,313 crore, growing 7.5% year-on-year, while PAT rose by just 3% to ₹830 crore. Shoppers’ shift towards quick commerce has been weighing on its business lately.

Thin spreads remain the hallmark of DMart’s model. Ebitda margin stood at 8.2% versus 8.9% a year ago, while PAT margin moderated to 5.2% from 5.9%. Foods, which account for 56% of revenue, naturally run at low margins. By contrast, non-food FMCG and general merchandise (44% of revenue) offer higher profitability.

DMart’s value proposition lies not in extracting fat margins but in turning inventory rapidly and maintaining tight control over costs. In FY25, DMart sold its inventory in just 31 days, but paid suppliers after only 7 days, demonstrating the rapid inventory turnover. DMart’s efficiency is reflected in its return ratios. RoCE and RoE stood at 18% and 14%, respectively.

Looking ahead, management is highly optimistic about the offline sector and believes India offers immense opportunities for value retail across all segments. The company plans to double its investment in store expansion by adding 10-20% of its base stores annually. These stores are expected to be concentrated in Uttar Pradesh and Odisha.

DMart also aims to create a unique and hard-to-imitate online model that delivers value with convenience. It plans to accelerate the opening of fulfilment centers near delivery markets and deliver all orders within six hours (currently, 65% of orders are delivered within 12 hours).

BlueStar: Cooling India with steady returns

Blue Star benefits from being a diversified cooling solutions player. Unlike consumer-durables peers tied to seasonal AC sales, it operates across B2C and B2B segments.

BlueStar revenue in Q1FY26 rose 4% to ₹2,982 crore, due to uneven growth across segments. The B2B-focused (electro-mechanical projects and commercial air conditioning systems) business grew 36% to ₹1,412 crore, driven by demand from factories and data centres. In contrast, the unitary products business (room ACs and refrigeration) de-grew 13% to ₹1,499 crore, hit by an early monsoon that dampened cooling demand.

At a consolidated level, Ebitda dropped to ₹200 crore from ₹238 crore last year, with margins narrowing to 6.7% from 8.3%. PAT slipped 28% to ₹121 crore. The weaker summer muted operating leverage benefits, particularly in the AC segment. Still, RoE and RoCE remain robust at 21% and 36%.

Looking ahead, management expects demand to rebound during the festive season, which will offset some of the summer weakness. The recent reduction in GST on ACs from 28% to 18% is also expected to boost AC sales. It expects unitary cooling products to grow at 10-15% by the end of FY2026, driven by pent-up demand. Margins are also likely to remain in 7-8% range.

On the B2B side, order inflows remain strong in data centres, healthcare, and manufacturing, positioning the company well for 15% growth. However, exports, which account for 2% of total revenue (1% from the US), may be affected due to geopolitical factors. To offset this, the company is expanding in Europe, Africa, and the Middle East.

Bottomline

The journeys of Dixon Technologies, Avenue Supermart, and Blue Star show that profitability is not always about commanding high margins. Each operates in industries where spreads are inherently limited, yet scale, efficiency, and disciplined execution have allowed them to generate healthy earnings and strong returns.

Dixon leverages high-volume contract manufacturing, DMart thrives on rapid inventory turns in value retail, and Blue Star balances cyclical consumer demand with steady project-driven revenues.

For investors, the lesson is clear: single-digit margins do not always equate to weak businesses. What matters is how effectively revenues are converted into absolute profits and shareholder returns.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.