Foreign institutional investors (FIIs) turned net buyers in select mid and large-cap names even as domestic institutional investors (DIIs) and retail shareholders pared their exposure, according to Prime Database, a provider of data on the capital markets.

This divergence comes at a time when FIIs’ stake stands at 16.7%—the lowest in 13 years, while DII holdings have risen to 18.3%, the highest on record.

This shift partly reflects the opposing flow trends between domestic and foreign investors over the past year. FIIs became cautious amid global monetary tightening, higher US bond yields, and a stronger dollar, resulting in sustained outflows from emerging markets, including India.

In contrast, DIIs continue to receive steady inflows through mutual funds, allowing them to increase their equity exposure even as FIIs trimmed theirs.

But which are these three stocks that caught the attention of foreign investors even as others exited? Let’s take a closer look…

Shaily Engineering Plastics

Shaily Engineering, one of the largest exporters of plastic components in India, offers solutions in plastic products, spanning design, development, tooling, moulding, and assembly.

The company operates across three segments— healthcare, consumer, and industrial. The healthcare portfolio encompasses platform devices, drug delivery devices (such as pens & auto-injectors), and pharmaceutical packaging.

Shaily manages over 200 injection moulding machines ranging from 35 tons to 1,000 tons across its seven units (six for plastics and one for steel furniture) in Gujarat.

It stands out as one of the key beneficiaries of the surging demand for GLP-1 medications, as it supplies delivery devices and components used in these formulations. The healthcare segment is the primary growth engine and is expected to account for half of the company’s revenues within three years, up from 21% in FY25.

The management aims to grow the healthcare segment by 30-35% CAGR over the next three to five years. At a consolidated level, revenue is expected to grow by more than 25% per annum over the next few years. This growth is likely to be driven by GLP-1 pens, with commercial supplies scheduled to begin in FY26.

Shaily expects the bulk of revenues from these products to accrue in the second half of FY26. To meet the rising demand for GLP-1 or glucagon-like peptide-1, a hormone that regulates blood sugar and appetite, the company plans to expand capacity over the next 12–18 months, targeting production of 70–75 million pens by early FY27. Around 60% of this capacity is already booked through customer commitments, and it expects full utilisation by FY28.

Institutional investors have already noticed this. The proportion of FII holdings rose from 9.71% in June 2025 to 11.30% in September 2025. During the same period, DII holdings declined from 14.13% to 13.71%, while public holdings fell from 32.42% to 31.26%.

Financial performance has been improving sharply. Revenue rose 38% year-on-year to ₹247 crore in Q1 FY26, led by strong momentum in the healthcare segment, which surged 181% to ₹77 crore. Healthcare’s contribution to the revenue mix rose to 31%. With improved utilisation, margins also increased 840 basis points (bps) to 28.5%, leading to a 136% increase in net profit to ₹41 crore.

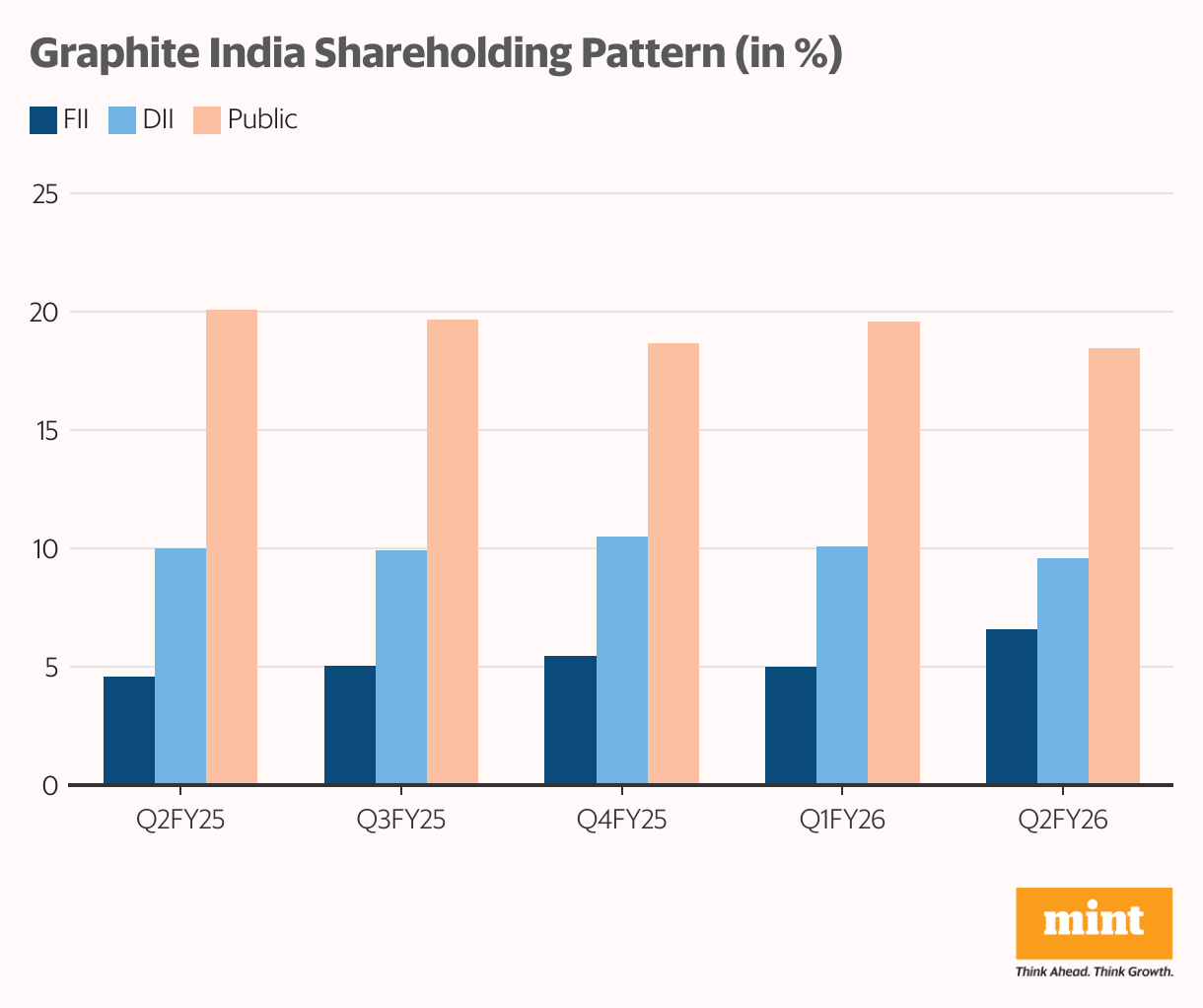

Graphite India

Graphite India is one of the world’s leading manufacturers of graphite and carbon-based products. The company’s core graphite electrode business remains its primary growth engine, contributing nearly 90% of total revenue. With an installed capacity of 98,000 tonnes per annum (TPA), it is India’s largest and among the top global producers of graphite electrodes.

Its manufacturing footprint spans three plants in Durgapur (West Bengal), Nashik (Maharashtra), and Nurnberg (Germany). In the first quarter of FY26, capacity utilisation stood at 82%, reflecting stable operating efficiency amid a challenging pricing environment. Graphite also serves the steel, glass-reinforced plastic (GRP) pipes and tanks, and captive power generation sectors.

Such leading companies often attract the attention of investors. The proportion of FII holdings rose from 4.99% in June 2025 to 6.6% in September 2025. During the same period, DII holdings declined from 10.09% to 9.58%, while public stake fell from 19.58% to 18.47%. FII confidence stems from graphite expansion into advanced materials.

It is well-positioned to benefit from the global transition towards sustainable steelmaking, driven by the growing adoption of electric arc-furnace technology. To capture this structural demand shift, Graphite is expanding its electrode capacity by 25,000 TPA with an investment of ₹6 billion.

The expansion will be rolled out in two phases: 13,000 TPA in the first phase and 12,000 TPA in the second, with commissioning expected within 12 and 36 months, respectively.

Beyond its traditional business, Graphite India is steadily diversifying into advanced materials. It has developed proprietary technology to produce large-area, high-quality, low-cost graphene sheets for scalable industrial applications. With a 31% stake in Godi India, it has also ventured into advanced battery chemistries for electric vehicles and energy storage systems.

Further, Graphite is developing carbon-carbon brake discs for fighter aircraft and carbon-silicon carbide components for defence applications. This positions the company to benefit from India’s rising defence and EV manufacturing ecosystem. However, financials remain tepid due to the cyclical nature of the sector.

In Q1 FY26, the company’s revenue declined 8.7% year-on-year to ₹665 crores, primarily due to weaker realisations in graphite electrodes. Operating margins contracted by 1,320 basis points to 29%, resulting in a 43.6% decline in PAT to ₹133 crore. Meanwhile, the company continues to maintain a strong balance sheet, providing ample flexibility to fund growth initiatives.

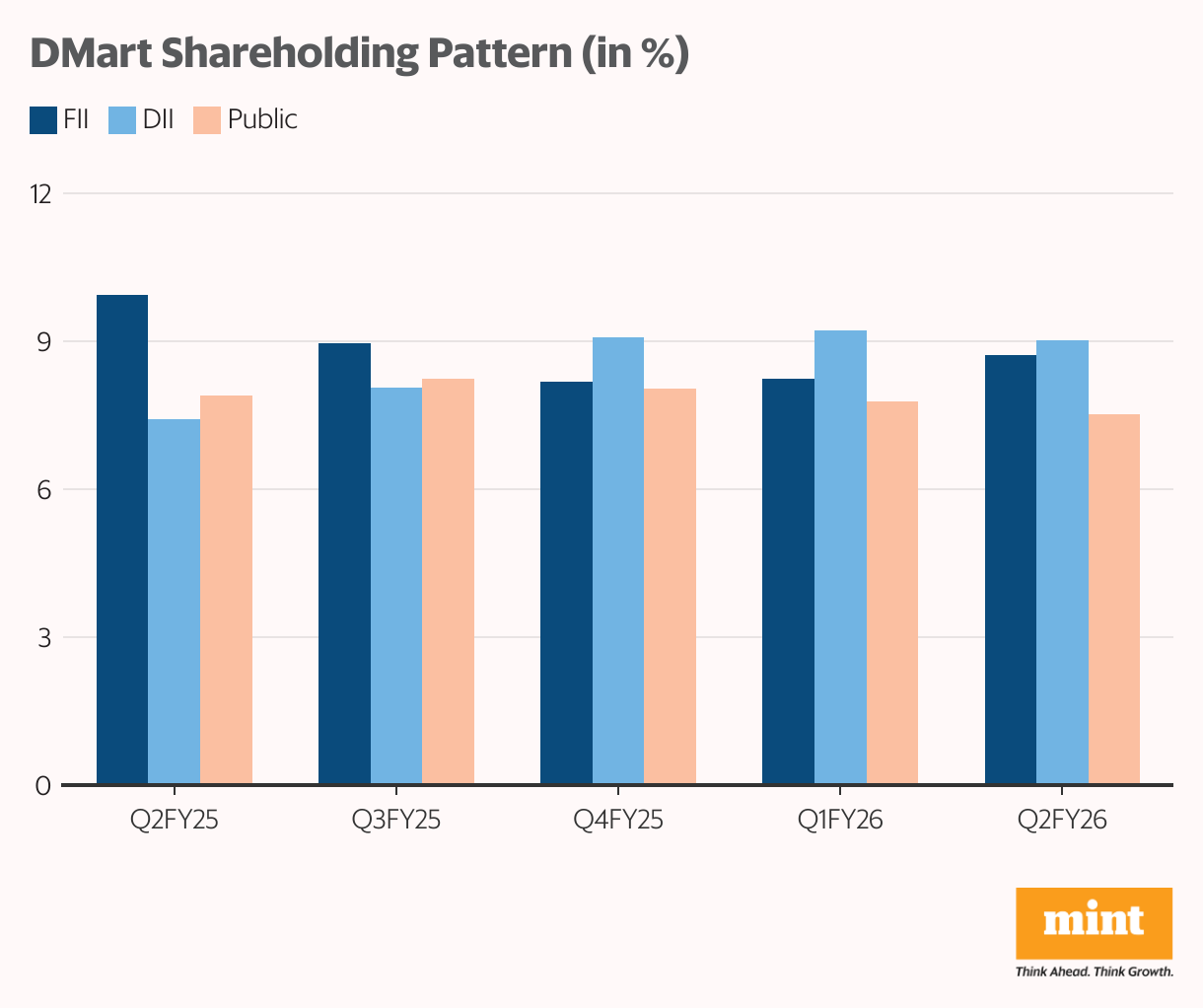

Avenue Supermarts

Avenue Supermarts (DMart) operates a business built around retail, focusing on three major product categories: food, non-food (FMCG), and general merchandise and apparel. DMart has always followed a simple philosophy: sell at the lowest price and let the volumes do the heavy lifting. Its expansion strategy remains cluster-based.

Its 432-store network is geographically concentrated in Western and Southern India. Maharashtra leads with 120 stores, followed by Gujarat (68 stores), Telangana (45 stores), Andhra Pradesh (42 stores), and Karnataka (41 stores). Its total retail business area at the end of Q2 FY26 was 17.9 million square feet.

In the revenue mix, food accounted for 57% of the total revenue share, followed by general merchandise and apparel (23.3%), and non-food items-FMCG (19.6%). The company’s revenue in H1 of FY26 increased by 15.8% year-on-year to ₹32,151 crore. However, the margin declined 50 bps to 7.9%. However, PAT rose by 3.5% to ₹1,576 crore.

DMart’s performance has remained subdued as consumer spending patterns continue to shift. The growing shift toward quick commerce platforms for daily essentials has impacted its footfall and same-store sales growth. Additionally, high competition and slower discretionary demand have limited its overall revenue momentum.

Meanwhile, DMart continues to trade at a high valuation. As a result, FIIs have increased their stake from 8.25% (June 2025) to 8.73% in the September 2025 quarter. At the same time, DIIs have reduced their holding marginally by 20 bps to 9.22%, and retail by 26 bps to 7.53%.

Looking ahead, management is highly optimistic about the offline sector and believes India offers immense opportunities for value retail across all segments. The company plans to double its investment in store expansion by adding 10-20% of its base stores annually. These stores are expected to be concentrated in Uttar Pradesh and Odisha.

DMart also aims to create a unique and hard-to-imitate online model that delivers value with convenience. It plans to accelerate the opening of fulfilment centres near delivery markets and deliver all orders within six hours (currently, 65% of orders are delivered within 12 hours).

Bottomline

The September quarter’s shareholding data shows FIIs selectively increasing their exposure in a few companies even as DIIs and retail investors booked profits.

Shaily Engineering Plastics, Graphite India, and Avenue Supermarts stood out in this trend, each driven by distinct business developments, including new product launches, capacity expansion, and sectoral positioning.

However, relying solely on this data is not indicative of their long-term investment stance, as quarterly shareholding changes may also reflect short-term portfolio adjustments or tactical positioning rather than structural conviction.

For more such analysis, read Profit Pulse

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.