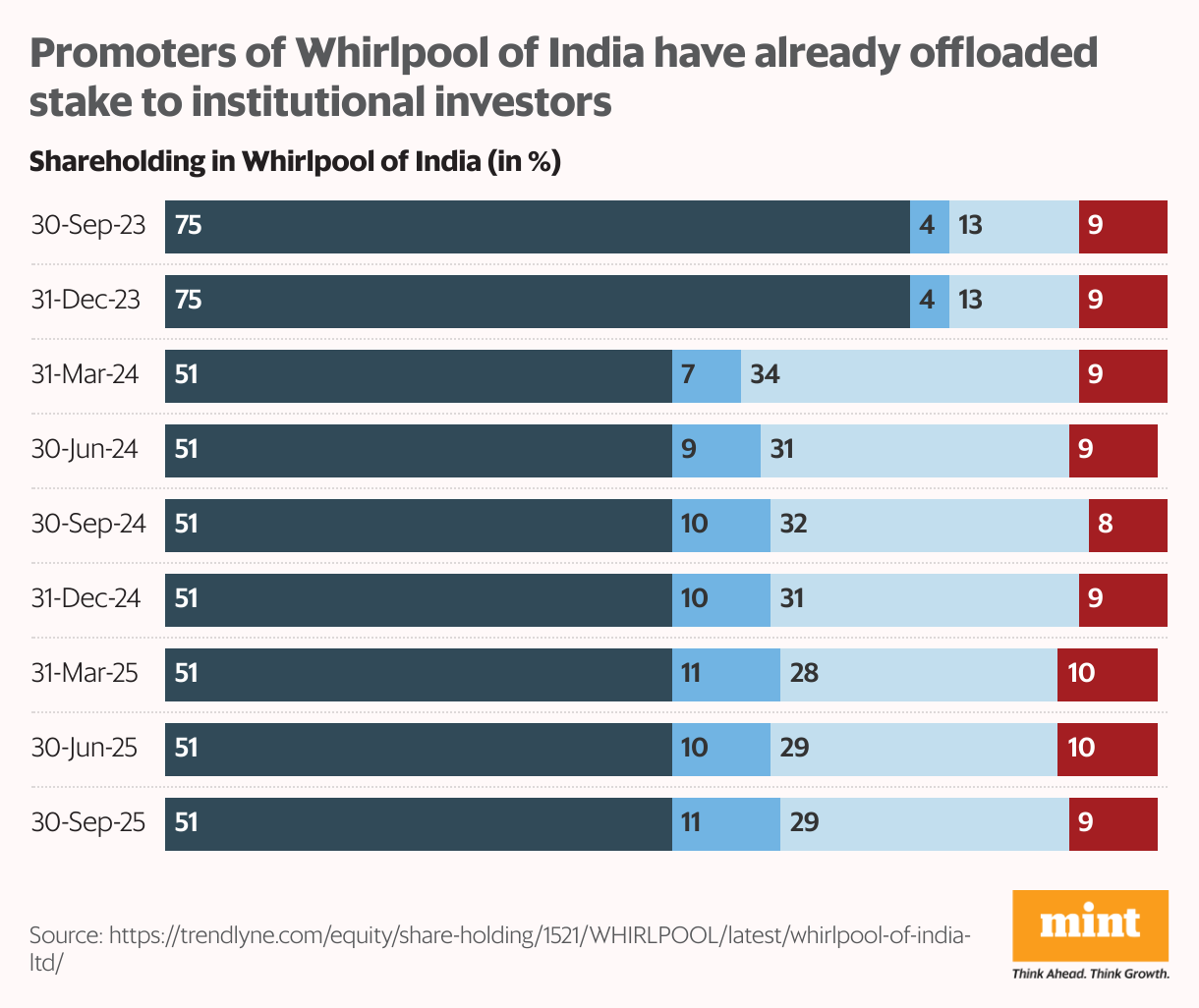

Last week, Whirlpool Corp., the promoter of Whirlpool of India, sold 11.2% stake in the Indian entity. This was the first step towards bringing down the promoter’s stake in the home-appliance maker from 51% to 20% by mid-2026.

The parent is offloading equity to pare down $1.85 billion of debt due in 2025 while restructuring globally. It has already spun off its European business into a new entity, sold operations in the Middle East and Africa, and now looks to raise about ₹9,000 crore through the India stake sale.

The Whirlpool India stock has corrected more than 35% since January 2025, when the parent company’s stake-sale plans first made news, and made investors drop the stock like a hot potato. On Thursday, when the promoter’s shareholding dropped to sub-40%, the stock tanked more than 11%.

As promoters pare their stake further down to 20%, should investors brace for more pain? Let’s discuss.

Liquidity overhang

Promoter stake has already fallen from 75% to 51% in February 2024. The latest block was largely absorbed by institutions — typically a positive signal. But the flip side of the coin is that falling promoter-shareholding raises a few red flags.

First is the liquidity overhang – the promoter plans to halve their stake to 20% by mid-2026. This means that the supply of shares is going to increase further, leading to an overhang on the stock price. The degree of the overhang will depend on the price at which promoters sell their stake – lower the price, larger will be the overhang.

Strategic signal

If the offloaded stake is picked up by strategic investors rather than financial ones, it would strengthen Whirlpool India’s long-term direction. Investors can also take some comfort in the fact that Whirlpool Corp. will continue as the largest shareholder, and business continuity remains secured through a 30-year brand-license agreement and a separate technology-license pact between the two firms.

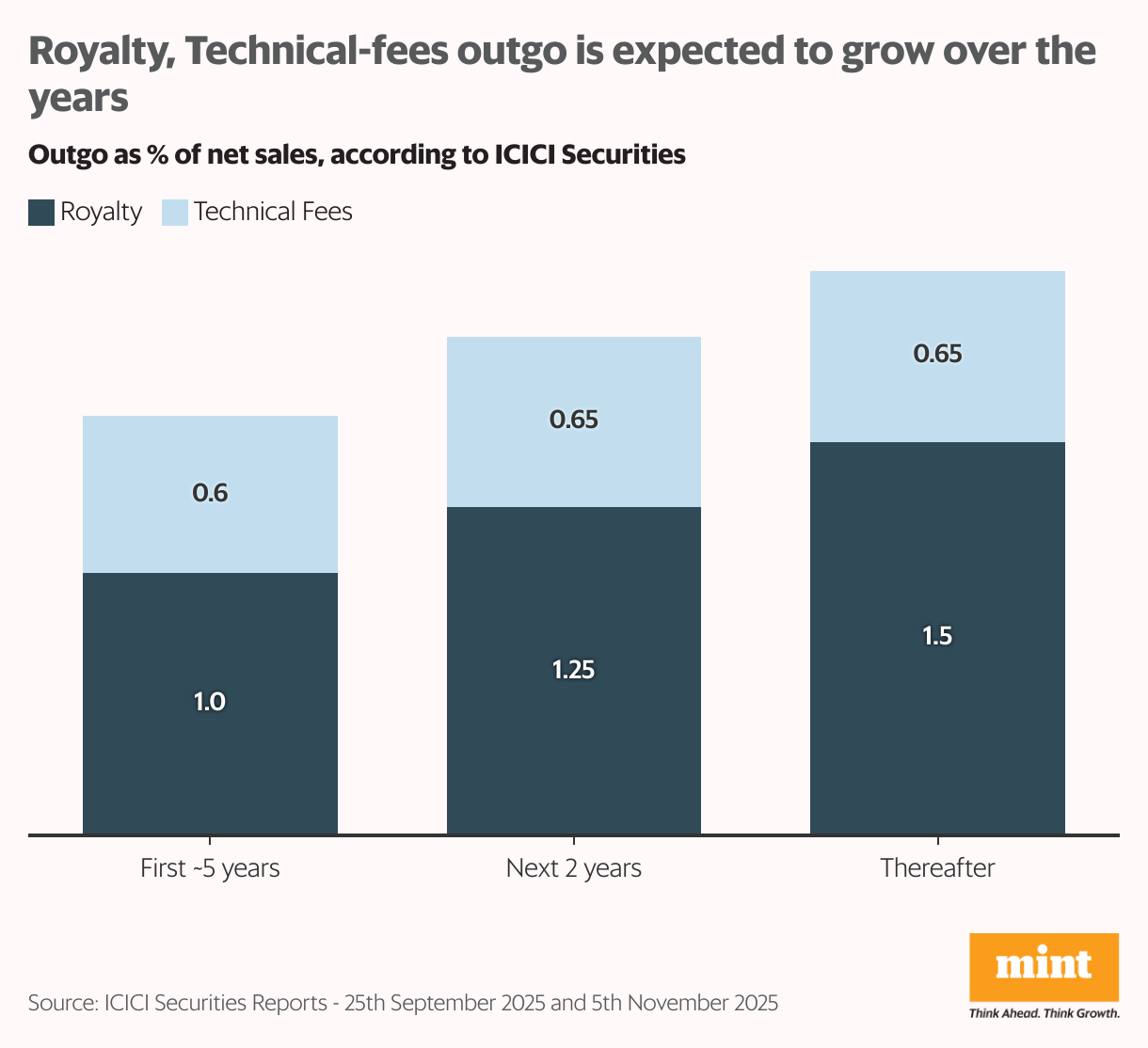

However, analysts are split on how these agreements will impact royalty payments. While Nuvama does not foresee an increase in royalty outgo, ICICI Securities estimates that royalty and technical fees could amount to 1.6% of net sales initially. For reference, royalty payments were maintained between 0.9–1.1% of net sales between FY15 and FY25.

Eventually, ICICI Securities expects total outgo to rise to around 2.15% of net sales—significant for a business that posted just 3.5% Ebitda margins in Q2FY26. More worryingly, the agreements include minimum guaranteed payouts—“$6 million in the first 10 years, $9 million in the next 10, and $12 million thereafter”—which raises the risk of losses, especially if revenue performance falters.

Another concern is Whirlpool Corp.’s rationale for the stake sale. Given the recent slowdown in growth and shrinking profitability, the return on investment from the India business is now expected to be lower than its cost of debt. That’s the only reason it would make financial sense for the parent to use Indian proceeds to pay down leverage—and that doesn’t exactly boost investor confidence.

What do the financials say?

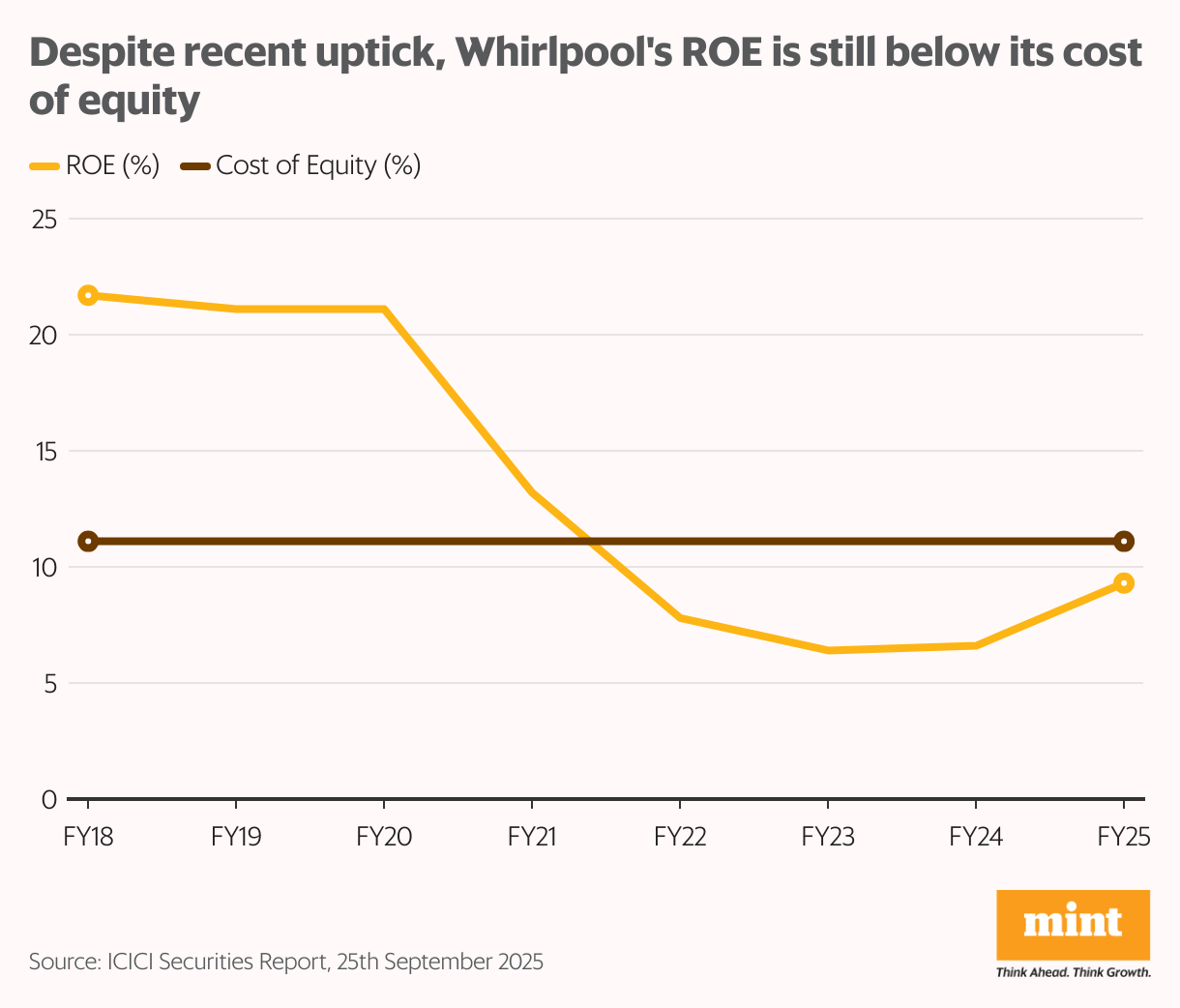

These fundamental and liquidity worries matter even more because Whirlpool India’s financial performance has weakened in recent years. The company has been squeezed by intense competition, leading to sharp erosion in growth and profitability. Since FY21, the company’s return on equity (ROE)—including cash—has fallen below its estimated cost of equity.

To defend market share, Whirlpool has sharply increased spending. R&D costs more than doubled in FY25, and advertising spends jumped nearly 50%. The “feet on street” initiative to push expansion in tier-2 and tier-3 markets has also added to costs. While these efforts aim to revive growth and strengthen the brand, their payoff has been limited so far. Even with a slight uptick in ROE in FY25, it still lags the cost of equity.

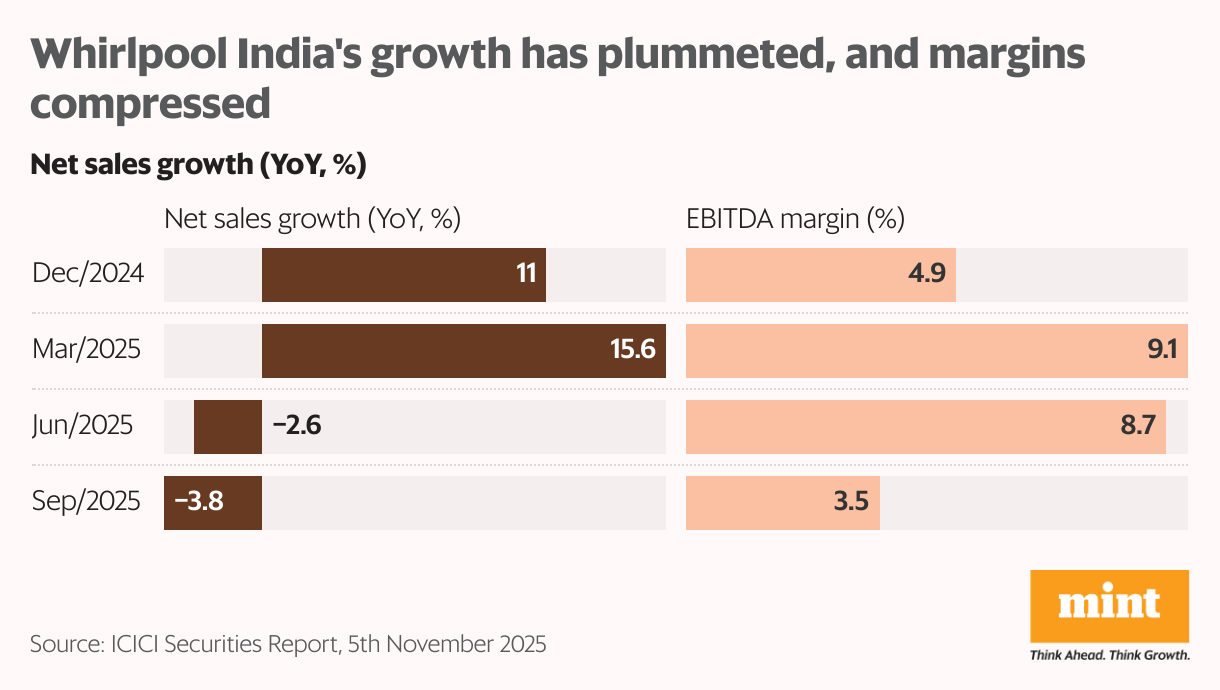

Making matters worse, seasonally soft demand for refrigerators and ACs, along with demand-deferral ahead of GST 2.0 have capped growth in recent quarters. Result? Growth has plummeted, and margins have compressed in H1FY26.

Silver linings

Despite these headwinds, there are positives keeping sentiment from completely unraveling. Whirlpool India gained market share in FY25 across refrigerators, washing machines, and ACs. Its subsidiary — Elica PB Whirlpool — continues to lead in cooking appliances.

New product launches such as auto-defrost single-door refrigerators, ACs with 6th Sense IntelliCool, and premium glass-door designs under the Kalakriti range have helped the brand remain competitive. The company will also benefit from the lower GST regime implemented from 22 September 2025.

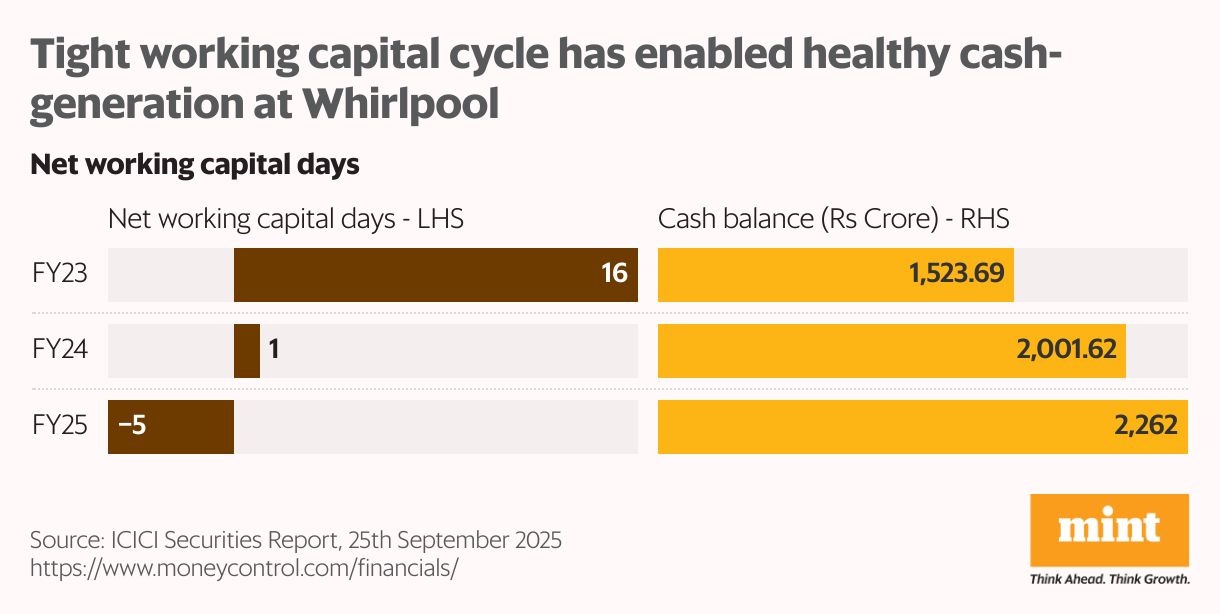

Meanwhile, its cash-generation has remained healthy, thanks to a tight working capital cycle. In fact, with increasing creditor-days, the company’s net working capital cycle had turned negative in FY25. This has helped keep its cash coffers full, which in turn, generated above-industry-average other-income in FY25.

Even as high other income has protected profits for the company recently, its cost-cutting initiatives under its Productivity for Growth (P4G) program, and a modified pricing strategy that focuses on premiumization, will hopefully support margins against competitive pressures. If the company manages to deliver on these hopes in Q3 and subsequent quarters, sentiment in the stock could recover.

Bottom line

Promoters selling down their stake in a business already wrestling with slow growth and margin pressure has amplified market concerns. The drag could worsen if the shares continue to go to purely financial investors and if the royalty-heavy licensing structure eats into already thin margins. Lower promoter skin-in-the-game also raises questions about confidence in future prospects.

But leaving aside the short-term liquidity-impact from supply overhang, the long-term impact of slashed promoter-stake is not necessarily negative as a rule.

For example, in the case of private banks in India, promoters’ shareholding has been reduced in response to industry-wide regulations. In fact, best governance practices call for capped promoter-stake to ensure diversified control and democratized decision-making.

Furthermore, in stocks with limited float (recent case in point: Groww), if lower promoter-shareholding results in higher free-float, it can aid in better price-discovery and lower volatility. Another possible benefit of a promoter slashing their stake is that it could help bring in strategic investors’ capital and expertise.

In the end, context is key. Against the context of healthy fundamentals, even if promoters sell stake to book profits, the impact on the stock is usually fleeting. Of course, this is subject to consistent strategic vision despite lower promoter-shareholding. On the other hand, when promoters reduce their shareholding in struggling businesses, it tends to reinforce negative sentiment.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.