Priced at ₹315-332 per share, the ₹2,079.37-crore IPO comprises a fresh issue of ₹1,500 crore and an offer for sale worth ₹579.37 crore by the promoters.

At the upper end of the price band, Vikram’s market capitalisation is estimated at ₹12,009 crore. Interestingly, the IPO price is 14% below Vikram’s most recent unlisted market price of ₹385 and nearly 30% off its peak level of ₹475, highlighting the risky nature of the unlisted market.

What makes Vikram Solar’s IPO particularly noteworthy is where the proceeds are headed. A majority of the fresh capital ( ₹1,364.9 crore) will go towards funding expansion plans, and the rest for general corporate purposes.This growth ambition, backed by a multifold increase in capacity, makes Vikram Solar’s IPO worth a closer look.

What makes Vikram Solar a heavyweight in solar manufacturing?

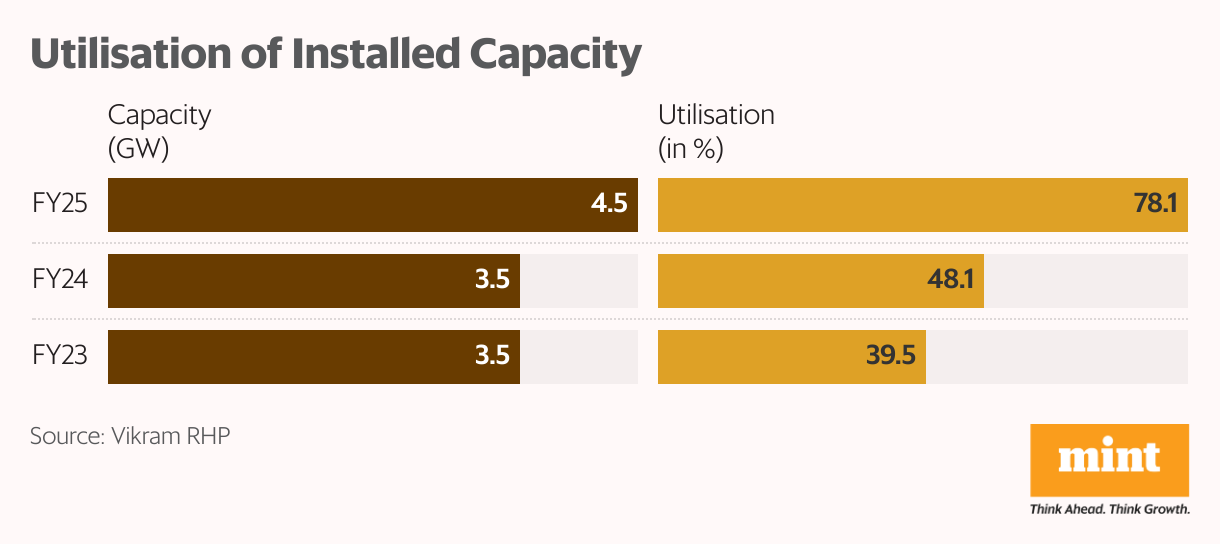

With an installed manufacturing capacity of 4.5 gigawatts (GW) across its plants in Kolkata and Chennai, Vikram focuses primarily on producing solar PV modules. These accounted for 98.2% of revenue in 2024-25, up from 97.3% in FY24 and 46.8% in FY23. While this helps the company capitalise on rising demand, it also exposes the business to cyclical risks if demand slows.

But what sets Vikram apart is its strong regulatory and brand credibility. A key competitive advantage is its listing under the ministry of new and renewable energy’s approved list of modules and manufacturers (ALMM). This is crucial because only manufacturers and models approved under ALMM can supply to government projects.

What sets Vikram apart in a crowded solar manufacturing market?

As of 30 June, Vikram had 2.85 GW of ALMM-listed capacity, which is among the highest for an Indian module maker. This enables access to large-scale domestic projects.

In May, Vikram was awarded the EUPD Top Brand PV seal, a global recognition of brand strength and product quality. That month, Vikram also became the first company in its sector at the group level to receive the EcoVadis platinum medal, placing it among the top 1% of global organisations evaluated on energy and water efficiency.

Vikram has also consistently featured in BloombergNEF’s Tier-I list since 2014, signalling bankability and execution strength. The latest inclusion was in April-June 2024.

Will Vikram Solar’s bold capex bet reshape its growth path?

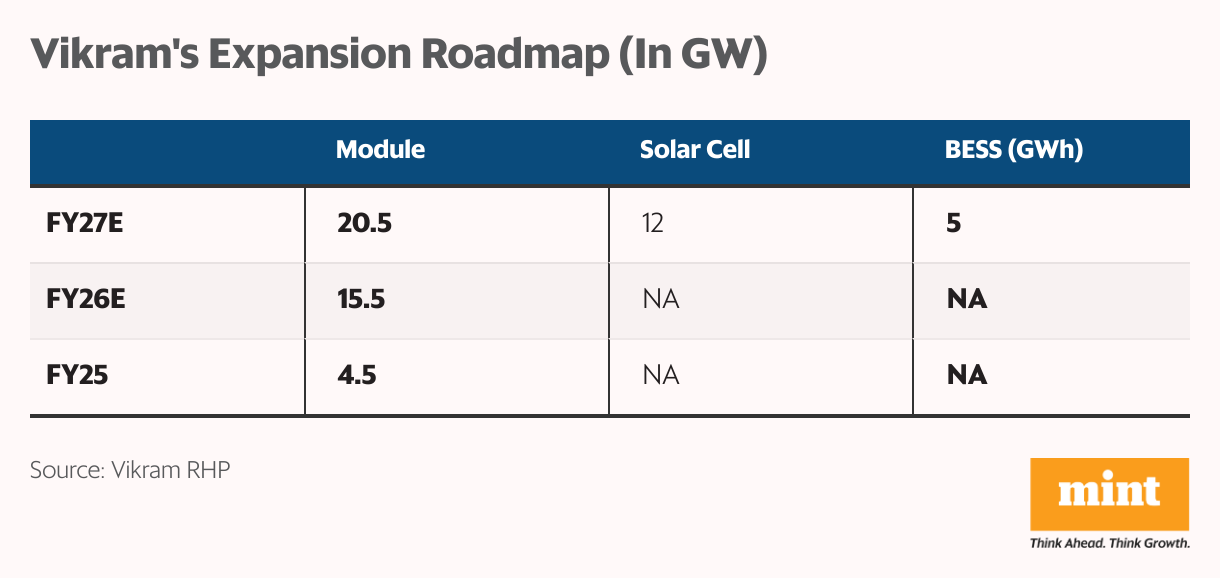

Vikram’s IPO stands out because of its ambitious expansion plans.The company aims to increase its installed PV module manufacturing capacity by more than fourfold—from 4.5 GW currently to up to 15.50 GW in FY26 and 20.5 GW in FY27.

Vikram is also setting up two solar cell units with a capacity of 12 GW, which are expected to start commercial operations by FY27. This backward integration will help Vikram reduce dependence on imported solar cells, meet domestic content requirements, gain cost and quality advantages, and shield margins from input price fluctuations.

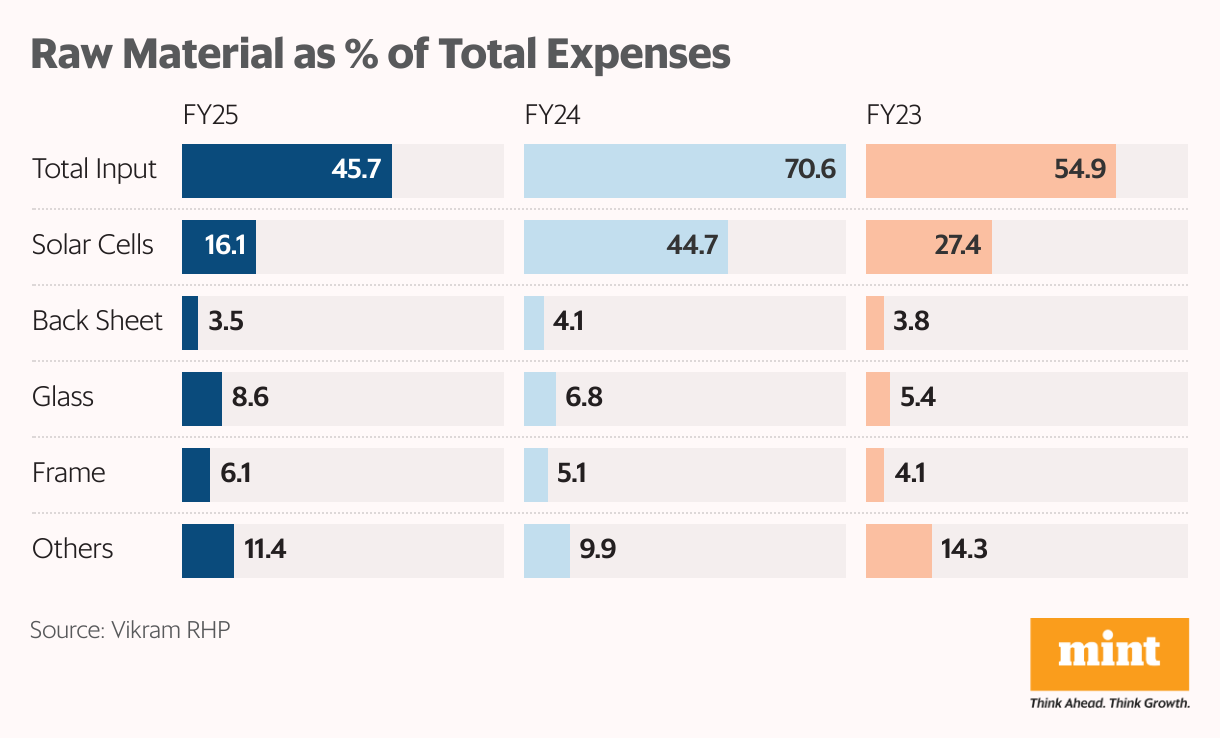

This is especially true since solar cells are Vikram’s primary expense driver, with prices being relatively volatile. They accounted for 27.4% of total expenses in FY23 and increased to 44.7% the following year before dropping to 16.1% in FY25. Global pricing, trade policy, duties, competition, and the demand-supply scenario for solar cells fuel this volatility.

Can in-house manufacturing reduce Vikram’s import reliance?

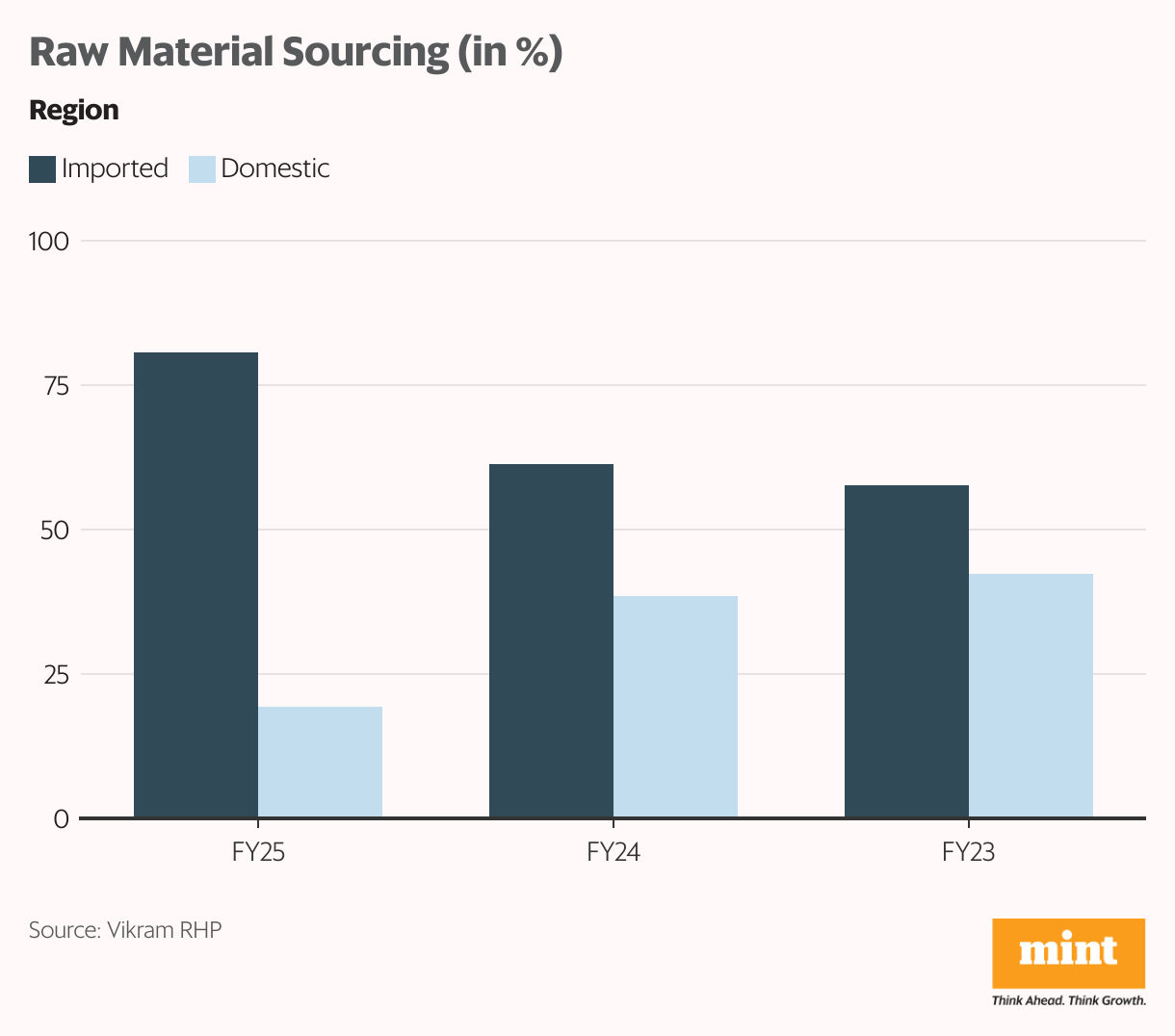

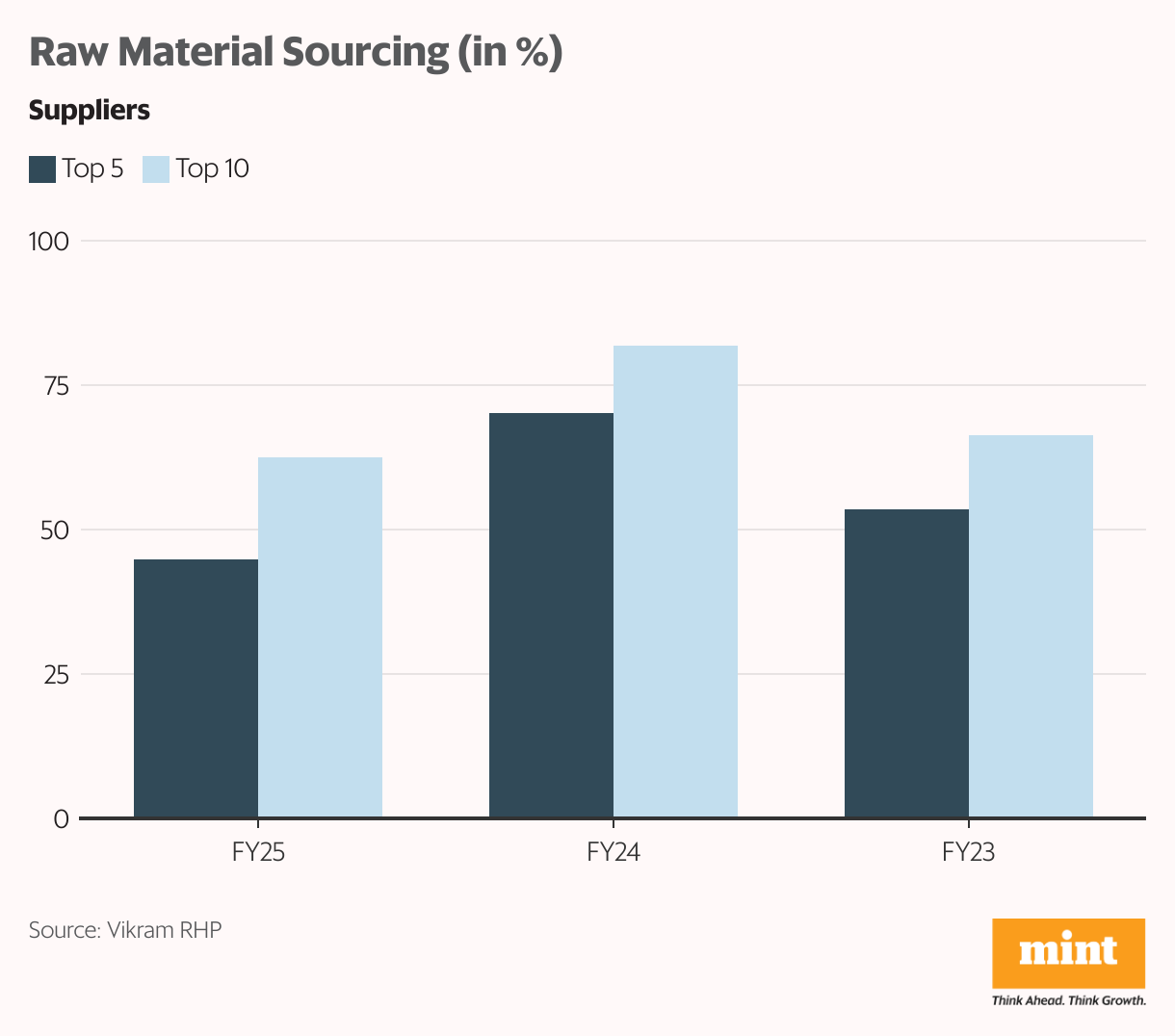

Yes, but not fully. In FY25, Vikram imported 80.7% of raw material from China and other East and Southeast Asian countries, up from 61.4% in FY24 . The supply-chain dependence is skewed with the top five suppliers accounting for 44.9% of Vikram’s raw material costs, and the top 10 for 62.6%. All these are international suppliers.

In that context, in-house solar cell manufacturing could reduce Vikram’s exposure to the global supply chain. Phase I of the project (3.0 GW each for solar cells and modules) will be partially funded by the IPO proceeds ( ₹769.7 crore). The balance ₹595 will fund the phase II expansion of module capacity from 3.0 GW to 6.0 GW.

The two phases are expected to be commercialised by March 2026 and September 2026, respectively, which will help boost Vikram’s top and bottom lines.

Importantly, this expansion qualifies for the government’s production-linked incentive (PLI) scheme, which will offer an estimated incentive of ₹528.5 crore over five years. The Tamil Nadu government will also offer an incentive of ₹900 crore, which Vikram plans to use to prepay its loan.

Will Vikram’s battery venture unlock the next growth frontier?

Vikram is entering the fast-growing battery energy storage system (BESS) market to capitalise on increasing demand. This aligns with the government’s ambitious target of achieving 236 gigawatt-hour (GWh) of BESS capacity by 2031-32, up from just 505 MWh currently.

To capitalise on this, Vikram is setting up a BESS project with an initial capacity of 1.0 GWh, with plans to expand it to 5 GWh by FY27.

This positions Vikram as a one-stop solar solutions provider, from module to cell to storage. If executed well, the company can unlock new revenue streams and support long-term profitability.

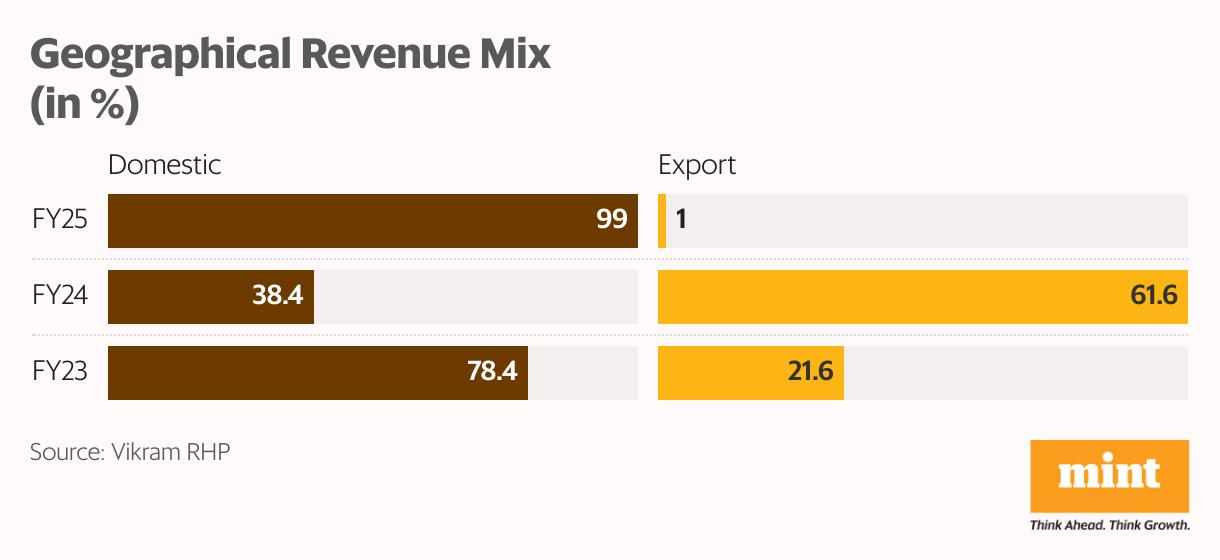

How a sharp fall in exports was offset by surging domestic orders

Vikram has a global presence through offices in the US and China and has supplied photovoltaic modules to 39 countries. However, the company’s export revenue declined sharply to 1% in FY25 from 61.6% in FY24. This is because 96.6% of its exports went to the US, and the company scaled back due to regulatory uncertainty.

But Vikram is setting up a 3.0 GW module manufacturing facility in the US by FY27 to localise the supply chain.

Vikram compensated for this loss of revenue from the domestic market, which now accounts for 99% of its total revenue, up from 38.4% in FY24 and 78.4% in FY23. The revenue is diversified across states, with customers from Gujarat (36.6%), Rajasthan (12.2%), and New Delhi (10.8%) contributing the most.

Vikram Solar serves industry leaders, including Adani Renewables, NTPC, JSW Energy, Azure Power, Acme, and Sterling and Wilson. To strengthen its domestic presence, the company intends to leverage e-commerce by launching a proprietary platform and introducing new project categories such as inverters, cables, and solar kits.

Is Vikram over-reliant on a handful of clients?

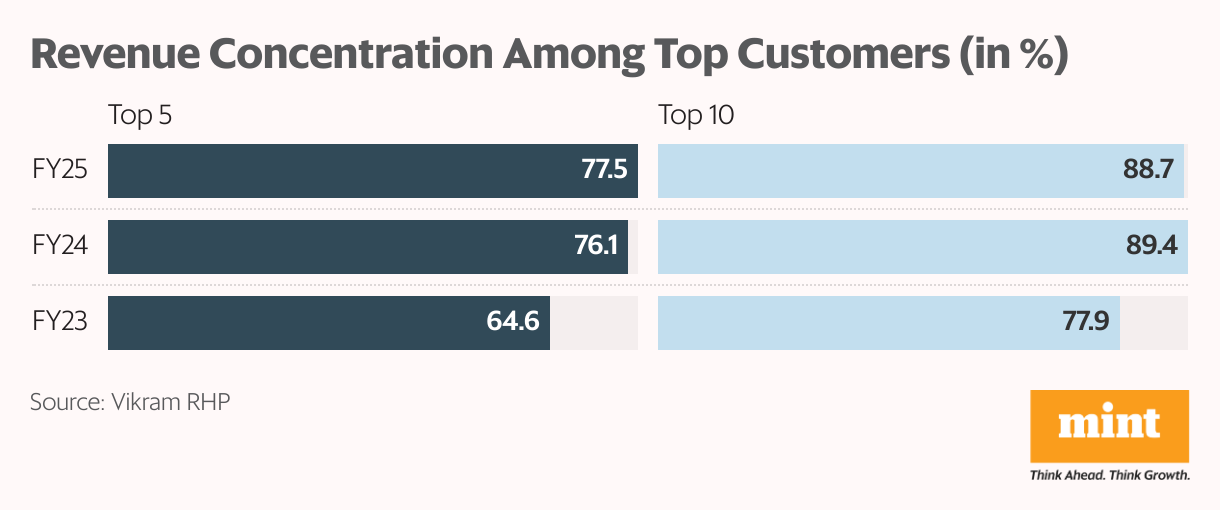

Yes. Vikram served 130 customers in FY25, up from 91 in FY24 and 115 in FY23. However, customer concentration risk remains high. Its top five customers contribute 77.5% of revenue, and the top 10 account for 88.7%. Thus, a churn at the top could materially impact the business.

Do Vikram’s financials back up its growth ambitions?

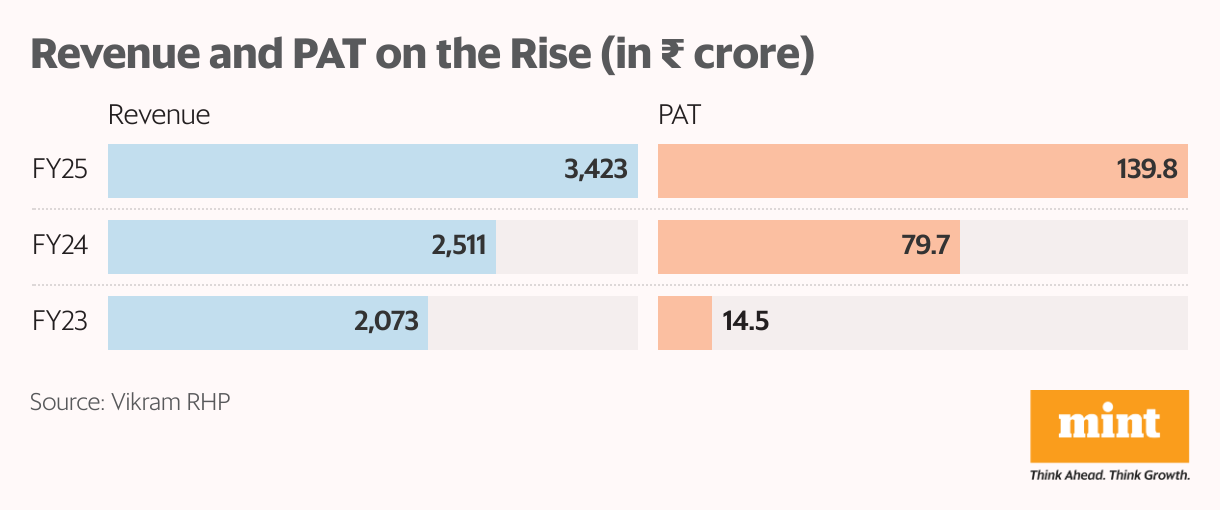

Vikram’s financial performance has picked up sharply. Revenue increased about 70%, from ₹2,073 crore in FY23 to ₹3,423 crores in FY25. The key driver was strong domestic demand for PV modules following ALMM enforcement and levy of basic customs duty. This is reflected in a healthy inventory turnover of 6.2 times, up from 4.4 in FY24 and 5.1 in FY23.

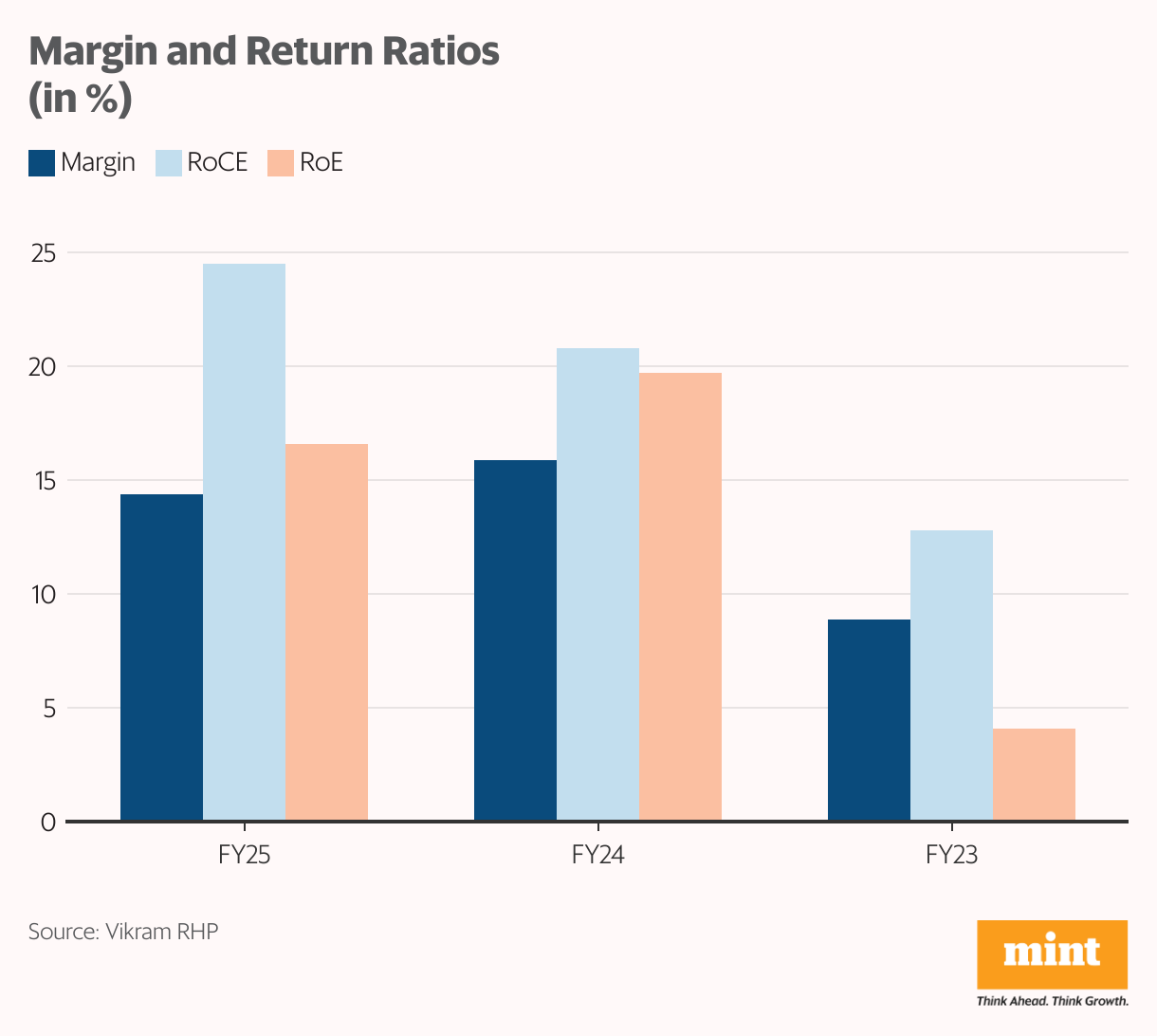

Operating leverage has played out as well, as capacity utilisation improved. Ebitda margin expanded from 8.9% to 14.4%, pushing profit after tax (PAT) up nearly tenfold to ₹139.8 crore in FY25 from ₹14.5 crore in FY23. However, the margin is lower than Waaree’s (21%), Premier’s (29%), and even smaller rival Websol’s (44.2%).

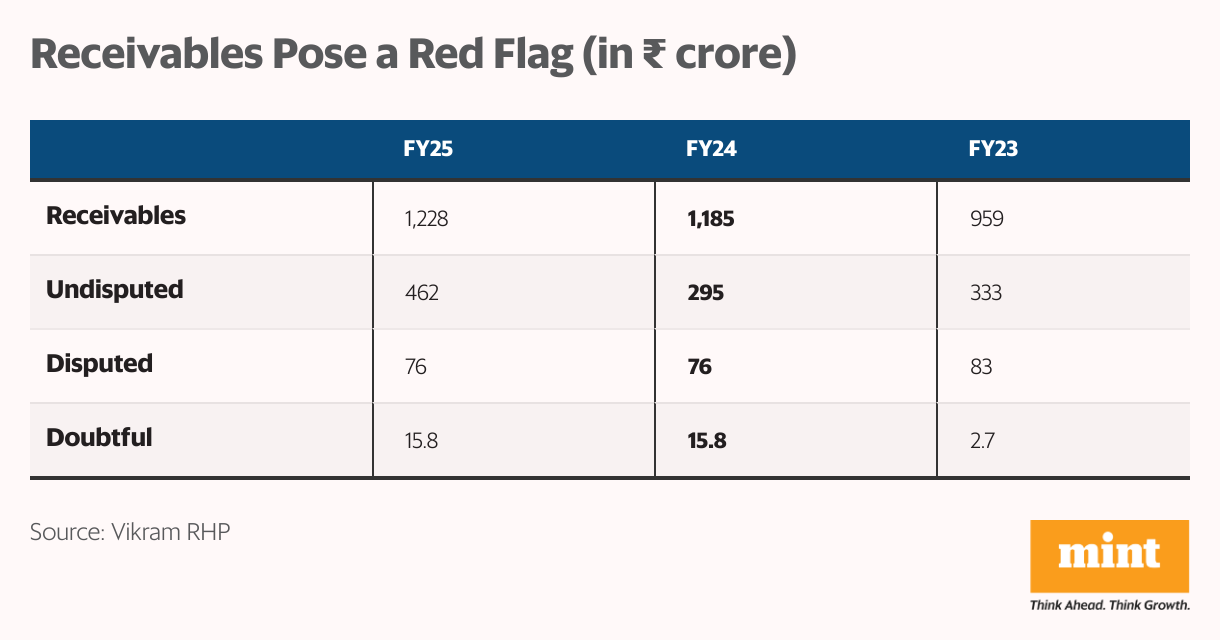

Vikram’s return ratios are also strong. Return on capital employed stands at 24.5% while return on equity is at 16.6%. Despite heavy capex, its debt-equity ratio has improved to 0.19 times from 1.8x in FY24 and 2.0x in FY23. But receivables account for 36% of revenue, which is a red flag.

Do Vikram’s receivables signal stress in working capital?

Vikram’s total receivables increased to ₹1,228 crore in FY25 from ₹1,185 crore the previous year and ₹959 crore in FY23. Of this, 37.6% is undisputed, 6.2% is disputed, and 1.3% is doubtful. This trend raises concerns, especially given instances when customers delayed payments.

Such delays could strain Vikram’s working capital and weigh on cash flows and overall financial health. That said, the company’s working capital was stable at ₹829 crore in FY25, down from ₹931 crore in FY24 and ₹886 crore in the year before.

Vikram’s order book more than doubled to 10 GW in FY25 from 4.3 GW in FY24, underscoring strong growth visibility.

Are the positives already priced in?

At the IPO price, Vikram is asking for a steep 86x price-to-earnings multiple, which is more than double that of Waaree’s (37x) and Premier’s (42x). This implies that growth prospects driven by capacity expansion are already factored into the IPO, leaving a limited margin of safety.

The company also has pending litigation worth ₹343 crore. Any adverse ruling could impact margins and profitability.

Other risks include a sharp fall in module prices due to potential dumping by China and oversupply, as module prices dropped 42% in FY25. There is also the risk of the Indian government removing the basic customs duty, which currently shields domestic players from cheaper imports.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.