Every once in a while, a well-established but currently struggling corporate giant is deemed too big to fail. But history shows there is no such thing. Several companies that had entrenched themselves deeply in their industries and had deep pockets and larger-than-life reputations are nowhere to be found now.

This Profit Pulse article zooms in on three business giants that have devolved into near-oblivion, and the cautionary tales they offer for investors.

Dewan Housing Finance Corporation Ltd: A house of cards

DHFL’s former chairman and promoter Kapil Wadhawan was recently declared bankrupt after he failed to honour personal guarantees for loans taken for the housing finance company. Wadhawan and his brother Dheeraj Wadhawan, ex-director of DHFL, are also barred from the securities markets for five years and have been fined more than ₹100 crore in penalty, along with others. What went wrong?

DHFL used to be India’s third-largest housing finance company. With a loan book of ₹1 trillion, it was a force to reckon with. But when Infrastructure Leasing and Financial Services Ltd (IL&FS) collapsed in 2018, lending to non-banks dried out. DHFL was no exception.

Of course, what was going on at DHFL was more sinister than the industry-wide stress.

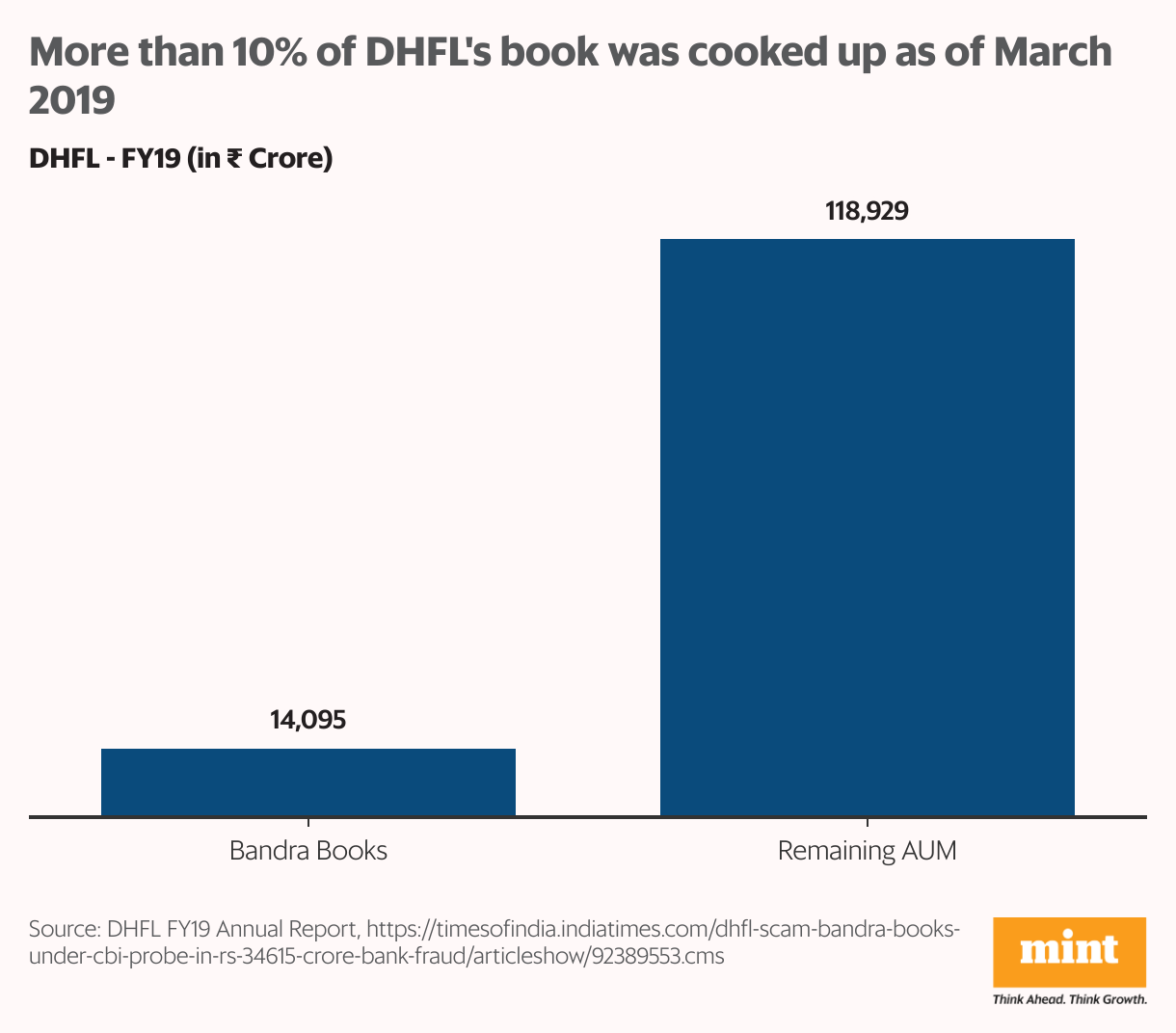

As banks and regulators became more vigilant, DHFL’s legacy turned out to be a pack of cards. A fake branch in Bandra housed ₹14,000 crore of its book as of March 2019, a lot of it cooked up. Affordable housing loans disbursed through this branch had been rerouted to more than 80 shell companies linked to the Wadhawans. Subsidies were claimed under the government’s affordable-housing scheme, Pradhan Mantri Awas Yojana, and repayments were recorded where there were none.

A mirage of financial health was maintained even as more than 10% of its book was just hot air. DHFL kept borrowing more until banks, its lenders, started asking questions. Seventeen banks alleged fraud amounting to ₹34,615 crore.

A federal investigation ensued, and the Reserve Bank of India took DHFL off the promoters’ hands. Nearly ₹30,000 crore in losses followed. As the DHFL stock corrected from ₹680 to less than ₹20 per share in just about a year, more than 95% of investor wealth was wiped out.

DHFL was eventually merged with Piramal Capital and Housing Finance Ltd in 2021, and now operates as an unlisted non-banking financial company.

Bhushan Power and Steel Ltd: Insolvency deja vu

Bhushan Power and Steel Ltd may be the only company to have been dragged to bankruptcy courts three times. BPSL itself was born out of the bankruptcy of Jawahar Metals in 1987. It grew into a formidable steel manufacturer but crumbled under ambitious expansion plans, piling debt, and alleged fraud, exacerbated by the crash in steel prices following the global financial crisis in 2007-09.

Bhushan Steel, an affiliated company, suffered a similar fate and was eventually acquired by Tata Steel Ltd.

BPSL knocked on the doors of India’s bankruptcy court in 2017 with ₹47,000 crore in dues to banks and ₹4,000 crore in alleged fraud. So dire was its problem that RBI ranked BPSL at the top of its ‘Dirty dozen’ list of defaulters, which accounted for a fourth of India’s bad loans at the time.

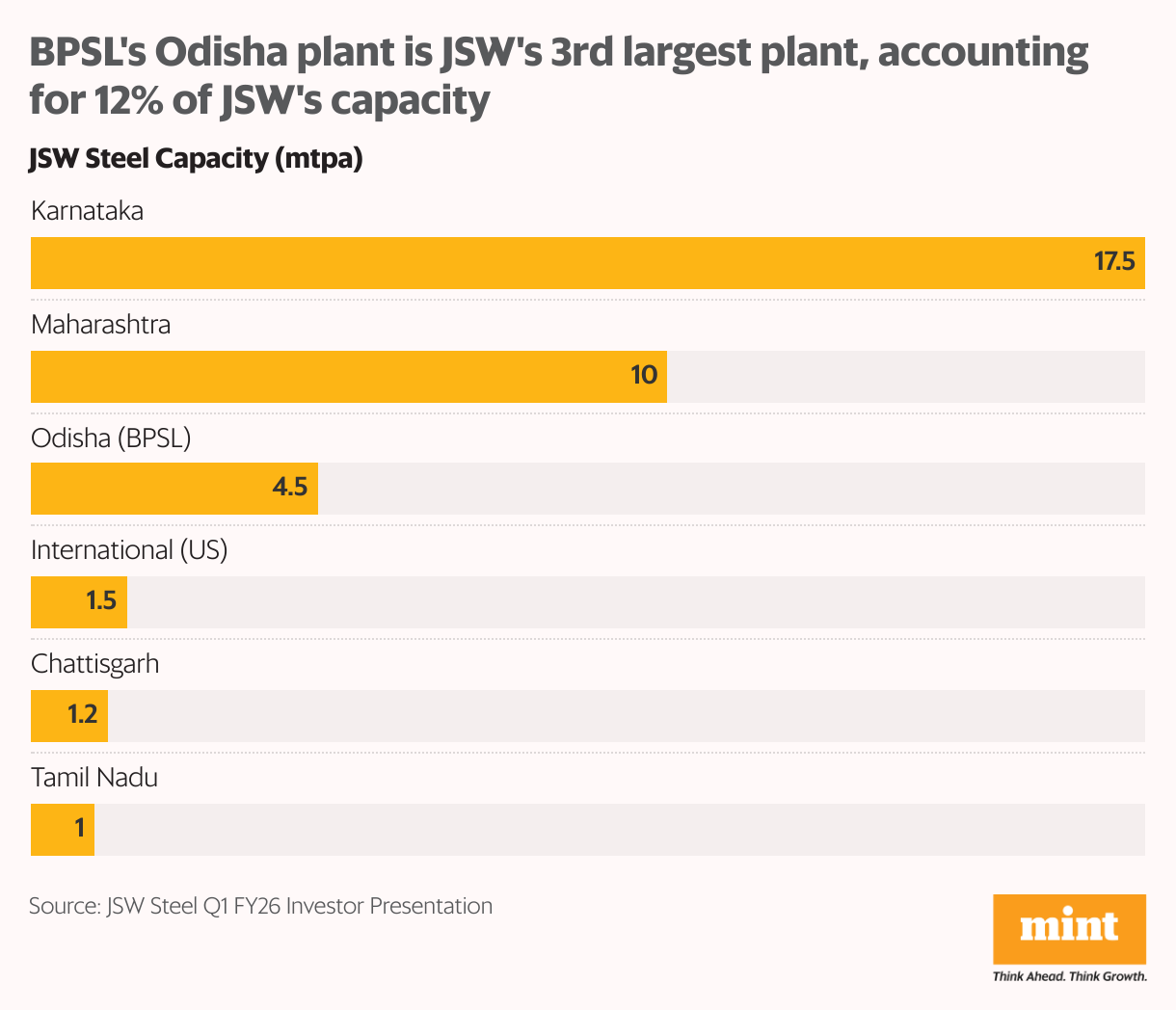

JSW Steel Ltd acquired BPSL for nearly ₹20,000 crore in 2021 and expanded its steelmaking capacity. BPSL now accounts for about 15% of JSW Steel’s total capacity and about 10% of its earnings before interest, taxes, depreciation and amortization. JSW Steel plans to expand BPSL’s capacity from 4.5 million tonnes per annum (mtpa) now to 5 mtpa by September 2027.

But an unexpected twist in the tale arrived a few months ago when the Supreme Court decided to annul the acquisition. Why? During the insolvency proceedings, the Enforcement Directorate had tried to attach BPSL’s assets amid allegations of money laundering against the promoters. Notwithstanding this, the National Company Law Tribunal (NCLT) had gone ahead with the proceedings.

The apex court cited this alleged overreach by NCLT and operational creditors being handed the shorter end of the stick to scrap the insolvency resolution and order BPSL’s liquidation. The Supreme Court recalled its order last month, allowing JSW Steel’s and BPSL’s financial creditors to breathe a sigh of relief.

Jet Airways: Nosedived after a miscalculated acquisition

Established as one of the first private airlines when India opened up its aviation sector in the 1990s, Jet Airways had a dream run for more than two decades. In a sector then dominated by the government, Jet Airways managed to carve a niche for itself by offering superior service and timeliness.

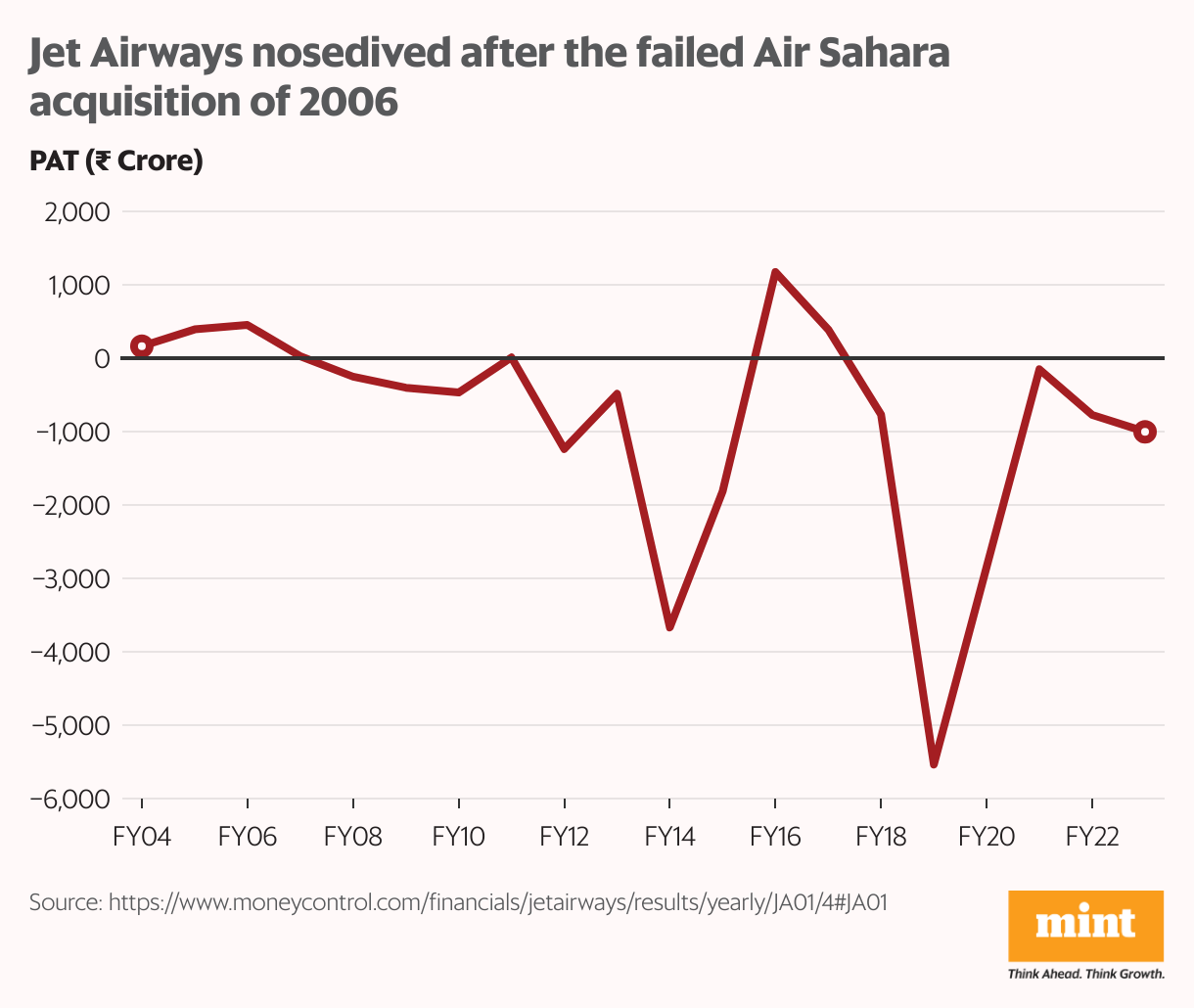

Things took a turn for the worse when the airline company overstretched its resources by acquiring Air Sahara in 2006. Jet Airways piled up ₹6,500 crore in losses and in 2015 wrote off its ₹1,800 crore investment in Air Sahara. There was more to come.

Jet Airways had partnered with the United Arab Emirates’ Etihad Airways and Air France, but the partnerships turned sour while losses and debt continued to pile up. Money-laundering allegations also surfaced. Jet Airways ended up accumulating more than ₹8,500 crore in debt to lenders, ₹16,500 crore to employees and operational creditors, and ₹3,500 crore to fliers.

Jet Airways eventually called it quits in 2019. Yet, retail investors kept accumulating stake in the company in anticipation of a successful insolvency resolution. But late last year, the Supreme Court ordered the liquidation of Jet Airways. Tens of thousands of jobs and crores of rupees in retail investor funds were lost in the ether.

How to avoid such falling giants?

India’s corporate history is littered with many such examples of falling giants—Videocon, Amtek Auto, Alok Industries, Essar Steel, Kingfisher, and GoAir, to name a few. But every such case of bankruptcy was preceded by several opportunities for investors to cut their losses and exit.

When a company’s losses mount and debt piles up, it is a telltale sign of stress. Heavy promoter pledge is another red flag—it pins a company’s fate on fickle stock prices.

Pending litigation, especially with concerns around money laundering, should also be taken seriously. Particularly when seen in conjunction with other qualitative concerns such as auditors’ opinions, complex related party transactions, and frequent churn in management, board, and auditors. These should make investors sit up and take notice.

Finally, when a business does not seem kosher, fear should not hold one back from booking losses. Similarly, greed should not push one to accumulate positions in stocks that appear to be a value pick.

Despite taking all these preventive measures, an investor may still end up with a few such stocks in their portfolio. That’s when portfolio diversification can come to the rescue.

Key Takeaways

- Rising losses and mounting debt are early warning signs of financial stress—do not ignore them.

- High promoter pledges can be a red flag, as they tie a company’s fate to volatile stock prices.

- Litigation, especially around fraud or money laundering, must be treated seriously.

- Auditor warnings, frequent churn in management/board, and related-party dealings can signal deeper problems.

- Don’t let fear stop you from cutting losses when fundamentals deteriorate.

- Avoid buying “value picks” in troubled companies driven by greed or speculation.

- Portfolio diversification is essential. Some failures are unavoidable despite due diligence.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.