But when a microcap starts showing steady, sustainable growth, something interesting happens. The volatility gradually settles, confidence builds, and the market begins to rerate the stock.

Over the past year, smallcaps have fallen sharply. Microcaps even more so. Prices have come down across the board, in many cases faster than the underlying businesses.

Corrections like these create fertile ground for investors who are willing to dig deeper to find companies that may be mispriced despite clear growth visibility.

In this editorial, we look at three micro-cap stocks with strong growth plans.

These businesses aren’t just promising scale but actively investing to achieve it.

Ddev Plastiks

First on the list is Ddev Plastiks, India’s largest listed manufacturer of polymer compounds, producing the essential raw materials that manufacturers turn into high-voltage power cables, footwear, packaging, and automotive parts.

Their core business revolves around creating a variety of specialized compounds, including PVC, XLPE, and Halogen-Free Flame Retardant materials, which are the lifeblood of the wire and cable industry. This generates about 81% of the revenue.

It has five factories split between India’s east and west coasts, to efficiently manage logistics for both domestic and foreign clients in over 50 countries.

The company achieved a 5% compounded annual growth rate (CAGR) in revenue growth over three years, along with a net profit CAGR of 50%.

The last three-year average return on equity (RoE) was 27%.

Looking ahead, the management is guiding for an aggressive target of ₹5,000 crore in revenue by FY30, a CAGR of 12-15%. For FY26, the guidance is for revenues between ₹2,850 crore and ₹2,950 crore and a volume target of 210,000 to 220,000 tonnes.

The leadership is confident in maintaining earnings before interest, taxes, depreciation, and amortization (Ebitda) margins in the 10-12% range.

A major pivot is their entry into the battery energy storage systems (BESS) sector, where the plan is to invest ₹150–200 crore to build a 5 GWh assembly plant.

This venture is expected to start contributing revenue from the second half of FY27, with the first gigawatt projected to generate ₹800-900 crore annually once fully operational.

The company is also seeing a revival in export demand, particularly from the US markets, following trade tariff resolutions, which should further bolster volumes.

TCI Express

Next on our list is TCI Express, a specialised B2B logistics provider moving high-value, time-sensitive cargo across India using a strictly asset-light model.

Instead of owning a massive fleet, the company controls the critical intelligence and network infrastructure, including over 970 company-owned branches and 28 sorting centres, while outsourcing the trucking.

This structure allows for a low-cost base and high capital efficiency.

Talking about its recent financial performance, the company has delivered a top-line growth of 4% CAGR over a three-year period and a net profit CAGR of -12%.

The last three-year average RoE has been 18%.

Looking ahead, management is targeting volume growth of 15% in FY27, driving revenue growth of 17-18%. This targets a recovery in FY26, with an anticipated 10% top-line growth and an 8% increase in volumes.

The guidance for FY27 is for profit after tax growth above 20%, a move heavily dependent on regaining operating leverage as the company scales.

For this to happen, operational efficiency needs to improve, specifically, truck utilization getting back to 85-86%. The management estimates this will expand margins by at least 1.5% and help restore Ebitda margins to 15%+.

The company is also implementing price hikes of around 2%.

Capital allocation remains disciplined but is aggressive on infrastructure. The company has revised a five-year capex plan to ₹400 crore, with the remaining ₹150 crore allocated through FY27. This is to automate sorting centres and add 60-80 new branches in this financial year alone.

The long-term strategy is to diversify the revenue, with a goal of generating 20-22% of the income from newer, faster-growing verticals such as rail, air, and C2C express in the next three years.

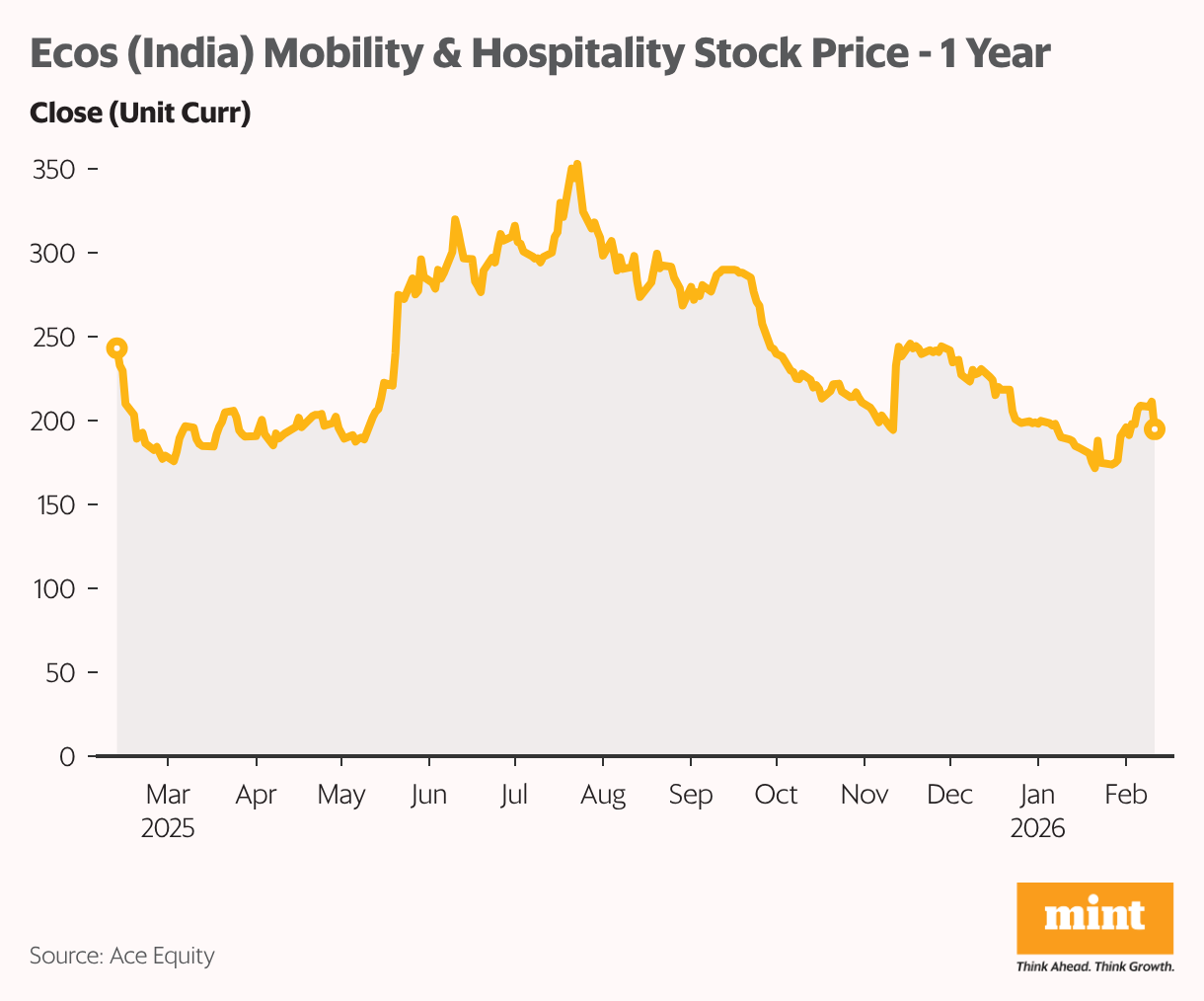

Ecos (India) Mobility & Hospitality

Ecos (India) Mobility & Hospitality is a provider of corporate managed mobility solutions, offering comprehensive B2B transportation services.

It operates through two segments: Employee Transportation Services (ETS) and Chauffeured Car Rentals (CCR).

Operating an asset-light model, the company manages a fleet of over 19,000 economy to luxury vehicles, which are primarily vendor-sourced, to serve a clientele comprising Fortune 500 companies, BSE 500 enterprises, and Global Capability Centres.

It has a pan-India presence spanning more than 130 cities and a global presence in over 30 countries.

Coming to its recent financial performance, the company has delivered a top-line growth of 63% CAGR over three years and a net profit CAGR of 87%.

The last three-year average RoE has been 35%

.

Looking ahead, management is guiding for a long-term topline growth of 15-20%. In the first nine months of FY26 alone, the company clocked nearly 26% growth.

The company is aggressively chasing market share in a fragmented industry.

Ebitda margins came in around 11.3% in the December quarter, down from historical highs. But the management has maintained its steady-state guidance of 13-15% and 8.5-10% net margins over the medium to long term.

The current dip in margins is largely due to ramp-up costs. The company onboarded 39 new enterprise clients in the last quarter. The management expects margins to stabilise and improve as operating leverage kicks in over the next few quarters.

Large corporate contracts are sticky and profitable eventually, but they are expensive to start because the company has to deploy resources before the billing kicks in.

On the tech front, the company is moving beyond being a service provider to being a platform. Over 21% of the Chauffeured Car Rental (CCR) bookings are now powered by their own digital tools like CabDrive Pro.

It has launched a direct web booking portal to capture premium B2C and SME demand, widening the net beyond just big contracts.

Conclusion

In microcaps, growth attracts many investors, but growth alone doesn’t make money.

Profitable growth does. Cash-generating growth does. Sustainable growth backed by a strong balance sheet, disciplined capital allocation, and effective management does.

A company can grow revenue by 30% and still destroy shareholder value (investor’s money) if working capital keeps on ballooning and capital allocation is poor.

That’s why it’s always crucial to thoroughly research financials and corporate governance before investing. You must be sure of the quality of growth.

So if you’re tracking these businesses, don’t just focus on top-line growth. Watch how efficiently these companies are able to turn ambitions into profits and profits into cash.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com