Of course, some companies are likely to beat the trend. But it will be important to separate the wheat from the chaff. Not all revenue growth or profit expansion should be considered cues to buy. Some businesses could appear promising on the outside, but a deeper look would raise eyebrows. Specifically, investors could keep an eye out for growth in operating revenues and profits, while growth driven by one-off or exceptional items should deserve a relook.

In this article, we shall look at three such businesses, where other income has painted a picture that’s prettier than real.

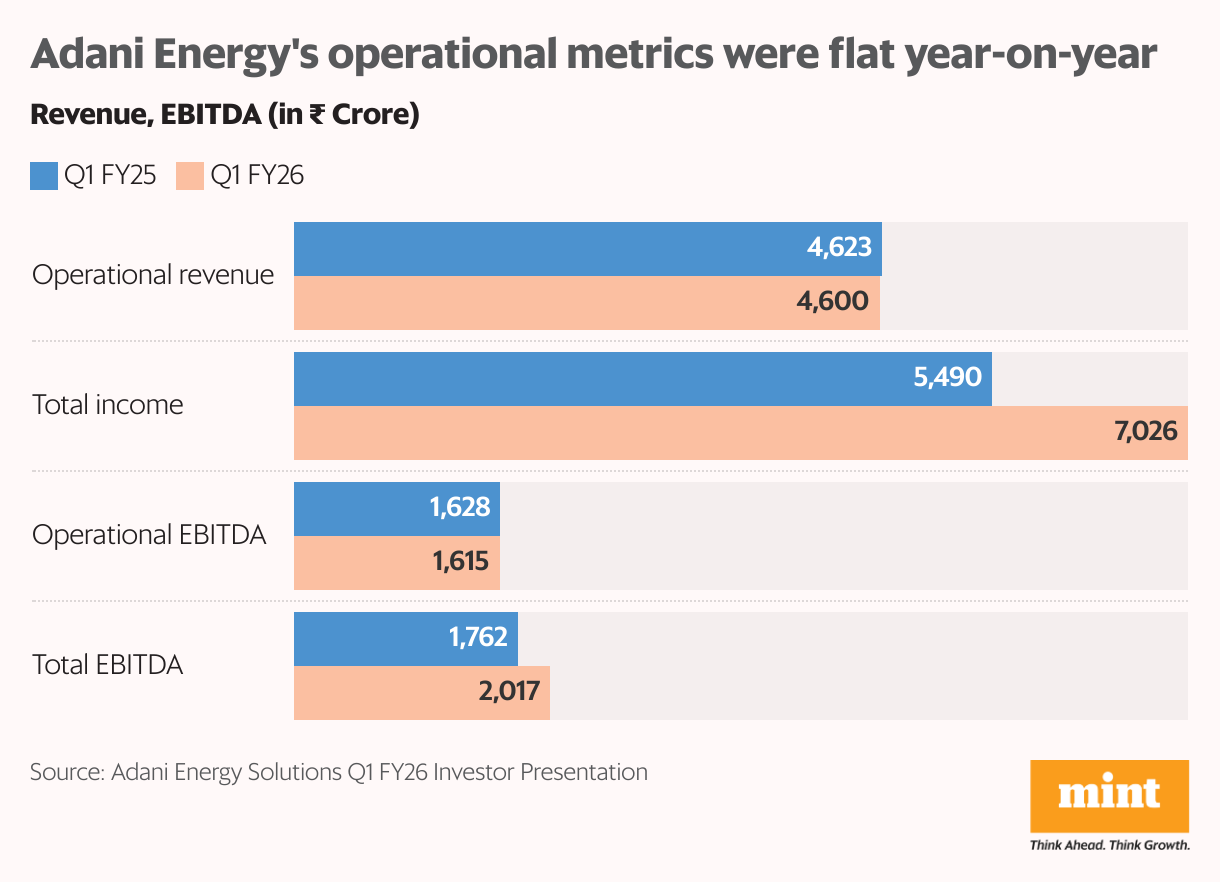

Adani Energy Solutions’ devil in the details

Adani Energy Solutions has been in the news recently for a turnaround in its profitability. The transmission and distribution company went from reporting a loss of ₹1,191 crore in Q1FY25 to a profit of ₹539 crore in Q1FY26. But the loss reported in the base quarter was due to a one-off line item: The company’s Dahanu power plant was carved out during the quarter, and that had resulted in an exceptional loss amounting to ₹1,500 crore.

With no such exceptional item dragging down profits this quarter, the company appears to have turned around. Sequential numbers reveal a 30% degrowth in the bottom line. Moreover, even the relatively modest 28% year-on-year growth reported in the top line is not without caveats.

The company clocked ₹7,026 crore in revenues during the quarter, a jump of ₹1,536 crore over the same quarter a year ago. But this is largely due to an acceleration in SCA (Service Concession Arrangement) income from ₹572 crore to ₹1,924 crore during the period.

SCA is essentially capital expenditure incurred by the company towards under-construction assets under the BOOT (build-own-operate-transfer) framework in its transmission and smart-metering businesses. In accordance with Ind AS 115, such assets are recognized as contracted or financial assets rather than featuring under gross block or PPE (property, plant, and equipment) in the balance sheet.

Accordingly, the capex incurred on such projects flows into the top line as ‘Revenue under SCA’, and also into the expenses as ‘construction expenses related to SCA’. Result? The top line shows growth, but profits don’t. Also, ‘total’ financial metrics appear inflated compared to operational metrics.

The Eternal PAT mirage

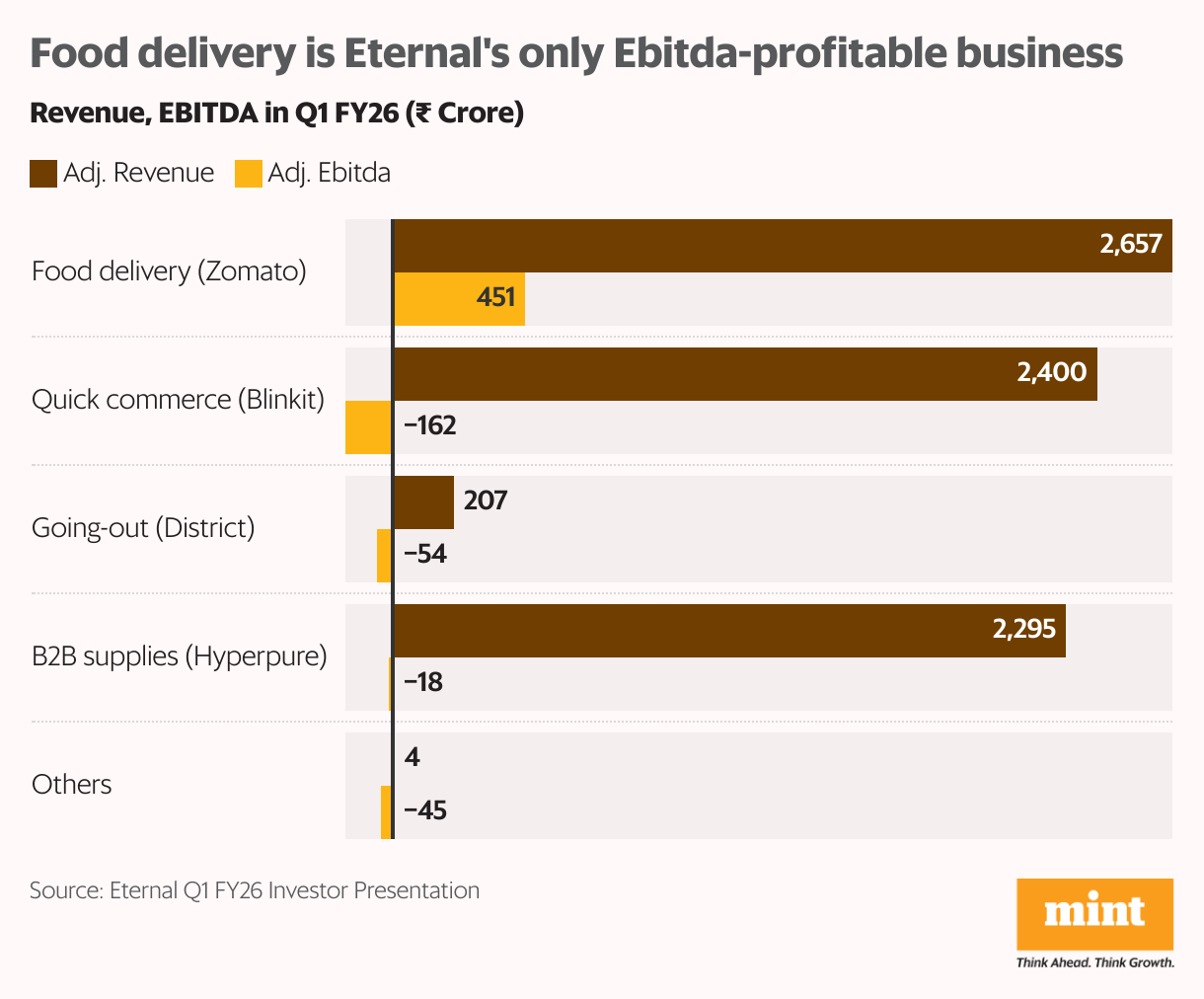

There is no doubt that Eternal Ltd (formerly Zomato Ltd) is at the forefront of India’s food and quick-commerce space. The company started in food delivery with Zomato and has been growing the business profitably for several quarters now. Blinkit has been thriving despite the recent rush of large players into India’s fast-growing quick-commerce industry. Its net order value (NOV) finally surpassed that of Zomato in Q1FY26. There’s still some way to go before the business turns Ebitda-profitable, but the losses have been shrinking. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

Eternal’s buisness-to-business (B2B) vertical, Hyperpure, has grown to about the same size as Zomato and Blinkit. The company has also been making large strides in the going-out business with District. It is currently a fifth of the size of Eternal’s food delivery/quick-commerce businesses, and is not profitable yet. But the management expects to scale it to $3 billion in annual NOV with $150 million Ebitda over the next five years.

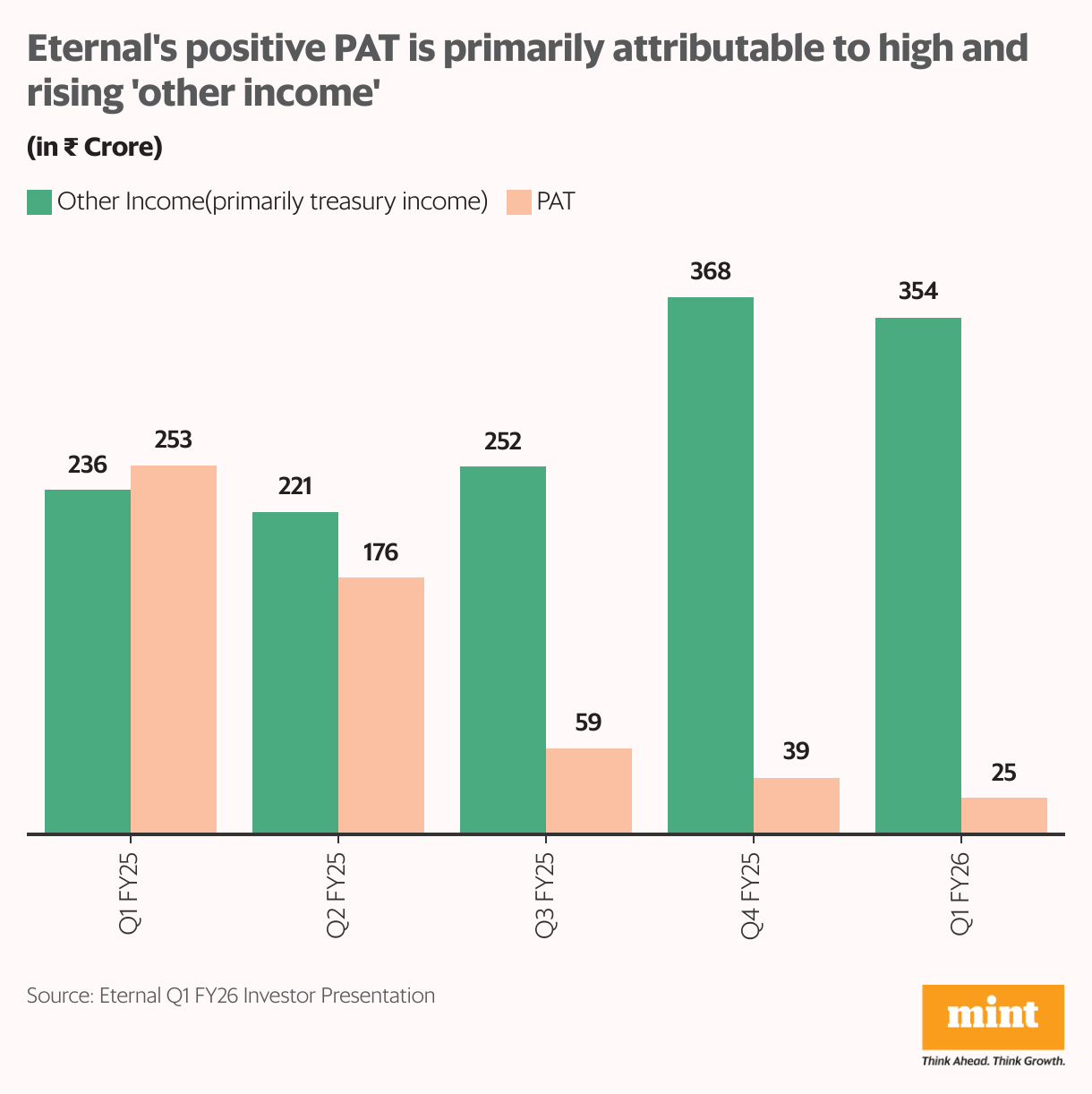

Other businesses Eternal has invested in recently include Bistro, Nugget, and Greening India. They added about ₹45 crore in Ebitda losses during Q1. In fact, all of Eternal’s businesses except food delivery are Ebitda-negative. But quarter after quarter, the company has managed to clock positive profit after tax (PAT). How?

The answer should make investors take a pause. Eternal has been posting ₹200-400 crore as ‘other income’ every quarter. A closer look indicates that this is treasury income, which the company earns on funds parked in investment instruments. Its cash balance has expanded from ₹12,500 crore in Q1FY25 to almost ₹19,000 crore in the latest reported quarter. With that, its ‘other income’ has increased as well, thus helping the company report positive PAT.

In other words, Eternal is profitable primarily due to money earned on money raised. While the company is Ebitda-profitable, bottom-line profitability (excluding treasury income) has proved more elusive. Of course, in anticipation of eventual profitability, its stock has grown fivefold in less than three years.

L&T’s low interest boost

Larsen & Toubro is the flagbearer of India’s infrastructure growth story. As the government amped up its capex spending to capitalize on its multiplier effect on gross domestic product (GDP) growth, L&T’s order book expanded in tandem. The company has also bagged international orders, which constitute more than half of its order book.

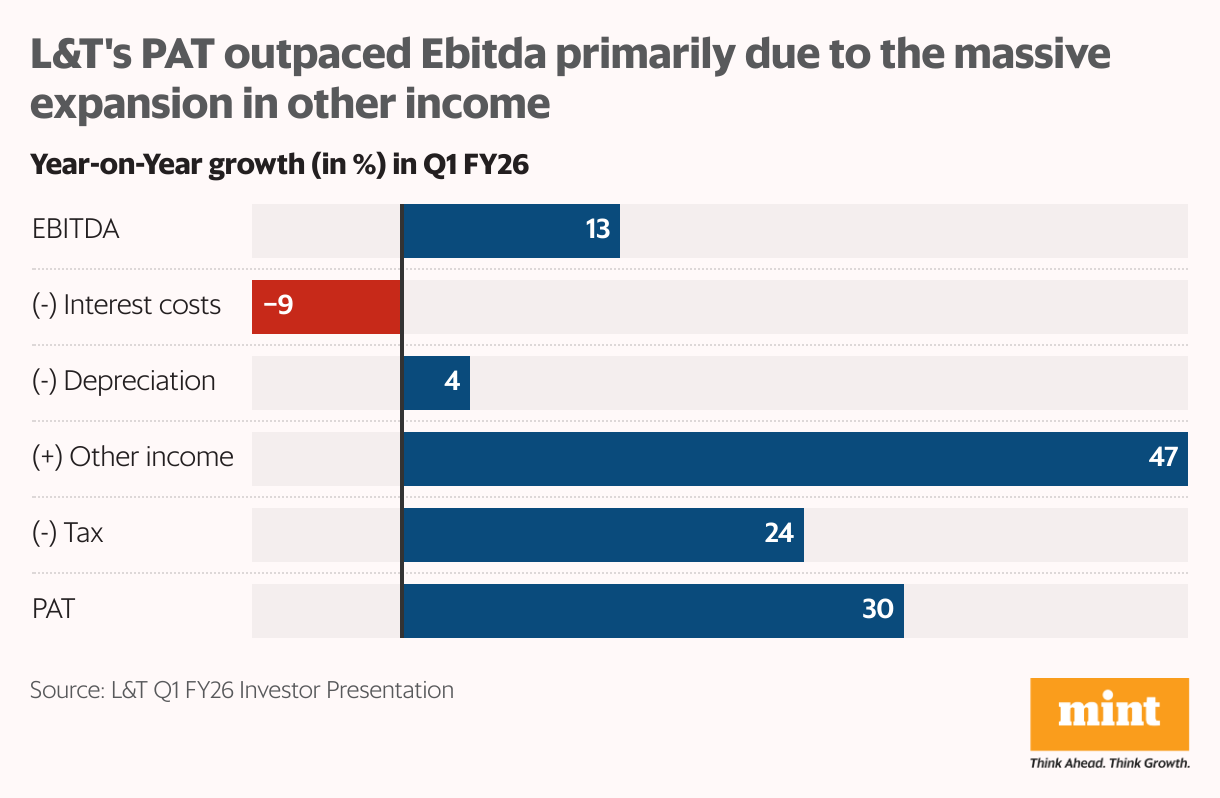

The momentum kept up in Q1FY26. L&T reported 33% year-on-year growth in its order inflows, which took its order book up by 25% to more than ₹6 trillion. Of course, execution has been slower with the top line registering a mellower 16% growth over the same quarter last year. Notwithstanding, the company reported a 30% on-year increase in PAT during the quarter.

If profitability had expanded on the back of higher operational efficiencies, that would have been good news. But for L&T, Ebitda margin witnessed a contraction during the period—from 10.2% to 9.9%. Ebitda grew by just 13%. Then how did PAT outpace Ebitda?

Interest costs compressed by 9% year-on-year due to lower interest rates and average borrowing levels, and that helped. But a bulk of the PAT growth came from other income. The company’s cash balance shrunk over the period, but its treasury yields improved. This resulted in treasury income of ₹13.6 crore during the quarter, a massive 47% increase over the base quarter. Half of L&T’s PAT expansion seen during the period came from other income.

Rounding it up

It is not wrong by any means to benefit from cash lying idle. But when treasury income becomes the difference between profit and loss for a company, as seen in the case of Eternal, investors should be wary of consuming headline numbers at face value. Of course, Eternal’s market dominance, high growth, and comfortable cash position could be worth betting on. But as things stand today, it would be a stretch to consider it profitable at the PAT level.

Similarly, with L&T, the massive order book and top-line growth at 16% promise potential. But drawing any inferences from the 30% PAT growth would be misleading. For others like Adani Energy, accounting standards could result in many layers obscuring the true picture.

For more such analysis, read Profit Pulse.

One-off items on the income statement are neither representative of the true state of the business nor repeatable. As cash dries up on the books, so would treasury income. Such income is also critically dependent on market conditions. Given their fickle nature, extrapolating them into the future could lead to subpar investing decisions.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author holds shares of some of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.