The rally follows a 90-day pause on reciprocal tariffs by the US and the conclusion of the India-UK Free Trade Agreement, both of which are expected to boost export competitiveness for the textile manufacturer.

The Indian government’s recent decision to restrict the entry of ready-made garments from Bangladesh to just two ports—Kolkata and Nhava Sheva—is also likely to bode well for the company as this could improve its pricing power.

For Gokaldas Exports, which derives over 75% of its revenue from the US, these developments come at a crucial time. The easing of trade barriers and favourable policy signals could help the company deepen its global presence and attract more Western buyers seeking alternatives to China.

Yet, underneath the optimism lie financial cracks.

Despite robust revenue growth, Gokaldas Exports has been grappling with sliding margins and a rising debt burden. Moreover, its promoters hold just 9.38% of the company and nearly all of it is pledged.

Profit Pulse takes a look into what’s driving Gokaldas Exports’s recent rally, the risks lurking beneath the surface, and whether the current momentum is sustainable.

India-UK FTA opens new doors

While the 90-day pause on the US’s reciprocal tariffs and import restrictions on Bangladeshi garments offer near-term relief and protection, Gokaldas Exports stands to gain the most from the India-UK free trade agreement. The two countries finalised their FTA on 6 May, bringing to an end nearly three years of negotiations.

According to the agreement, the 8-12% UK import duty on textiles and garments will be eliminated, making Indian exports more competitive as compared with those from countries such as Bangladesh and Vietnam.

This development is expected to double the UK’s contribution to Gokaldas Exports’s revenue. Currently, the company earns about ₹250 crore annually from the UK—accounting for about 5% of its total revenue.

Additionally, Gokaldas Exports is eyeing a $1 billion incremental export opportunity in the UK market, driven by a 12% cost advantage over Chinese suppliers.

Bangladesh previously enjoyed a competitive edge through duty-free access. However, with India now securing similar benefits under the India-UK FTA, a shift in sourcing towards Indian exporters is likely.

Gokaldas Exports expects the real impact of the trade agreement to be felt from the second half of 2025-26 (October 2025-March 2026), once ratification and customs implementation are complete.

Also read | Trent’s 1,000% rally takes a breather. Can a Sensex rejig revive its fortunes?

The $1 billion revenue target

Credit rating agency Icra expects India’s textile export volumes to the UK to double in 5-6 years following the implementation of the revised tariffs. It also expects the India-UK FTA to drive the addition of incremental capacities across the industry.

For Gokaldas Exports, Icra’s outlook reinforces the case for scaling up operations to meet future demand. The company is targeting $1 billion ( ₹8,500 crore) in revenue over the next few years, up 120% from its FY25 revenue of ₹3,864 crore.

To enhance its competitiveness, the company is positioning itself through new factory builds and recent acquisitions to ride the expected export surge.

Gokaldas Exports has already commissioned phase I of a new sewing factory in Bhopal, Madhya Pradesh, where it plans to add 1,100 machines. The first phase of this facility is already operating at near full capacity. Phase II is expected to be completed by the end of June.

In Karnataka, Gokaldas Exports is constructing another facility where it will add about 750 machines.

Additionally, a new leased unit in Ranchi is expected to house 200 machines operating in two shifts, effectively functioning as a 400-machine unit dedicated to knits.

With these expansions alone, Gokaldas Exports is expected to generate ₹355-365 crore in incremental income annually.

The company is also expanding capacity at Atraco, one of its acquired entities, where 500 machines are being added. This expansion could contribute an additional ₹125-130 crore in revenue. All these new units are scheduled to commence operations at various points through FY26.

These initiatives are part of a broader growth strategy. Gokaldas Exports’s management has made it clear that capacity addition will remain a focus over the next two years and beyond.

Also read | Can this under-the-radar company cash in on the $150 bn weight-loss drug boom?

On the mergers and acquisitions front, Gokaldas Exports recently acquired UAE-based Atraco and Indian knitwear manufacturer Matrix Clothing Pvt. Ltd for a combined ₹930 crore to expand its product offerings.

These acquisitions provide access to high-value knitwear, new customer bases, and low-cost production locations. The integration of these entities is progressing. The management has indicated that bringing both these entities up to the company’s standards will be a priority.

Gokaldas is also evaluating a strategic merger of BRFL Textiles Pvt. Ltd (BTPL), its recently acquired fabric unit. The company has so far invested ₹175 crore in the company via optionally convertible debentures to support BTPL’s capital expenditure, performance upgrades, and working capital needs.

Capacity utilization at BTPL has improved meaningfully, from near-zero orders to 40-45%, accompanied by better production quality and reduced reprocess rates.

Margins under pressure

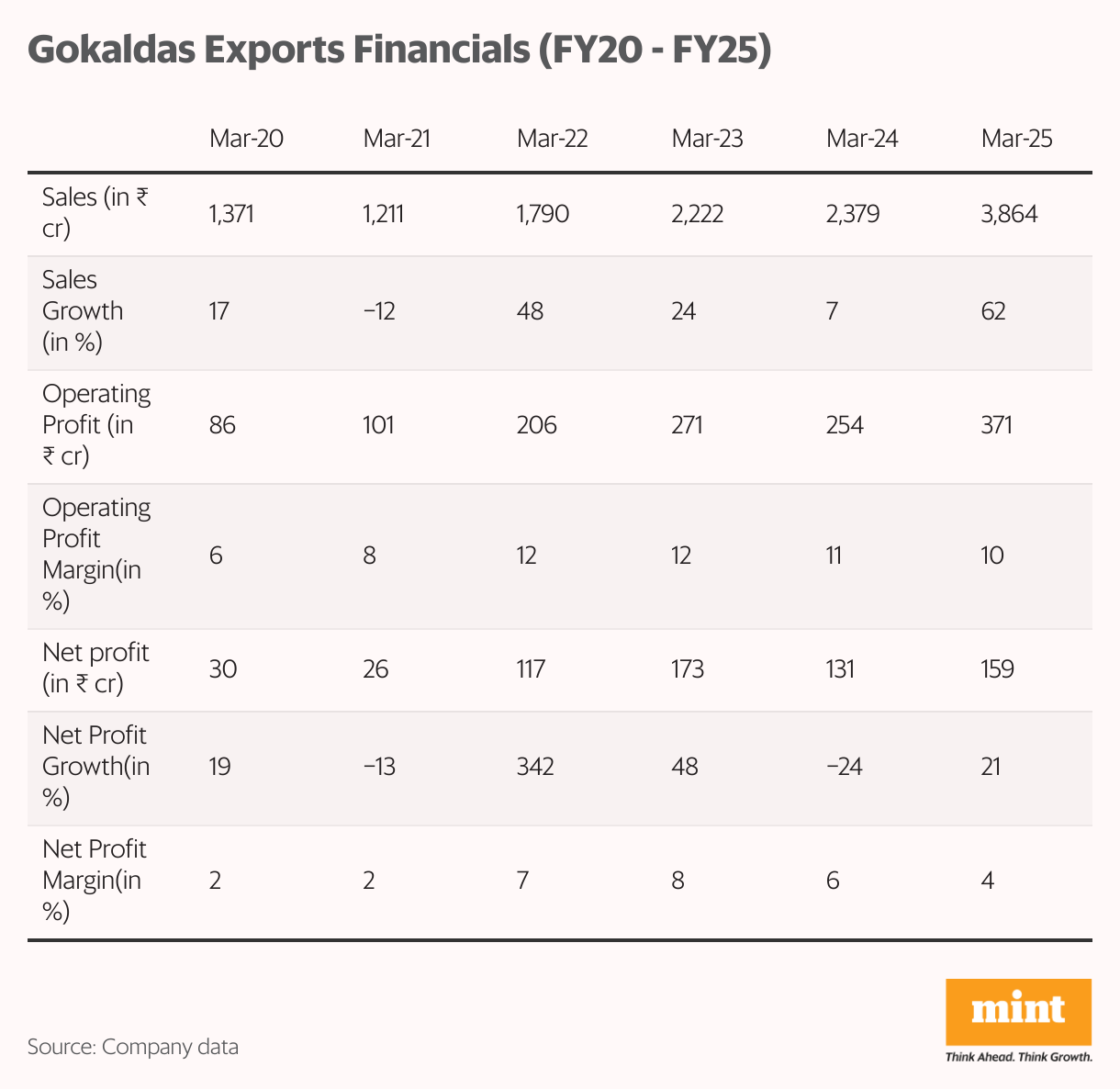

Gokaldas Exports has delivered strong topline growth over the past three years, with sales nearly doubling from ₹1,790 crore in FY22 to ₹3,864 crore in FY25.

However, the company has struggled with slipping operating margins and rising leverage, raising questions about the sustainability of its expansion strategy.

Gokaldas Exports’s operating margins have barely improved, rising from 8.4% in FY21 to 9.6% in FY25, due to cost pressures, additional costs for starting new units, and one-off expenses related to the two acquisitions. Net profit margins have fluctuated between 2% and 7%, not offering any stability.

Meanwhile, peers like Page Industries Ltd and KPR Mill Ltd have consistently reported operating margins in the 18-21% range, reflecting stronger pricing power, integrated operations, and better cost controls.

Gokaldas Exports’s return ratios also reflect the pressure on profitability. The company’s return on equity (ROE) stands at just 9.4%, significantly below its peers. Page Industries’s RoE stands at 48.5% and Vedant Fashions Ltd’s at 23%.

Gokaldas Exports’s return on capital employed (RoCE) is similarly modest, at 11.8%, lower than Page Industries’s RoCE of 59.4% and Vedant Fashions’s 26.6%.

Adding to the concern is Gokaldas Exports’s rising debt burden. The company’s borrowings increased to ₹845 crore in FY25 from ₹154 crore in FY23, pushing its debt-equity ratio to 0.41x.

While this is still comfortable, interest costs have tripled over the last two years, putting pressure on the company’s bottom line.

While Gokaldas Exports aims to improve its margins in the long term, over the next few quarters it expects its margins to decline by 200 basis points, with a recovery likely from the third quarter of FY26 (October-December 2025), depending on clarity around tariff-related policies.

Also read | This luggage leader is staging a turnaround. But can it overcome its baggage?

Despite current uncertainties, Gokaldas Exports expects to clock 10-15% revenue growth over the next 2-3 years. For FY26, it is targeting consolidated revenue growth of 15%, supported by a healthy order book.

Volumes for the ongoing first quarter (April-June) are fully secured, although Q2 visibility is lower due to ongoing tariff uncertainties.

Gokaldas Exports has also earmarked ₹150 crore in capital expenditure for FY26, with ₹166 crore in cash and cash equivalents to support this.

Sharekhan has a ‘buy’ rating on Gokaldas Exports citing strong medium- to long-term prospects. While the brokerage acknowledges near-term headwinds, particularly from US tariff uncertainties that may dent demand and compress margins, Sharekhan remains optimistic about the company’s ability to navigate these challenges.

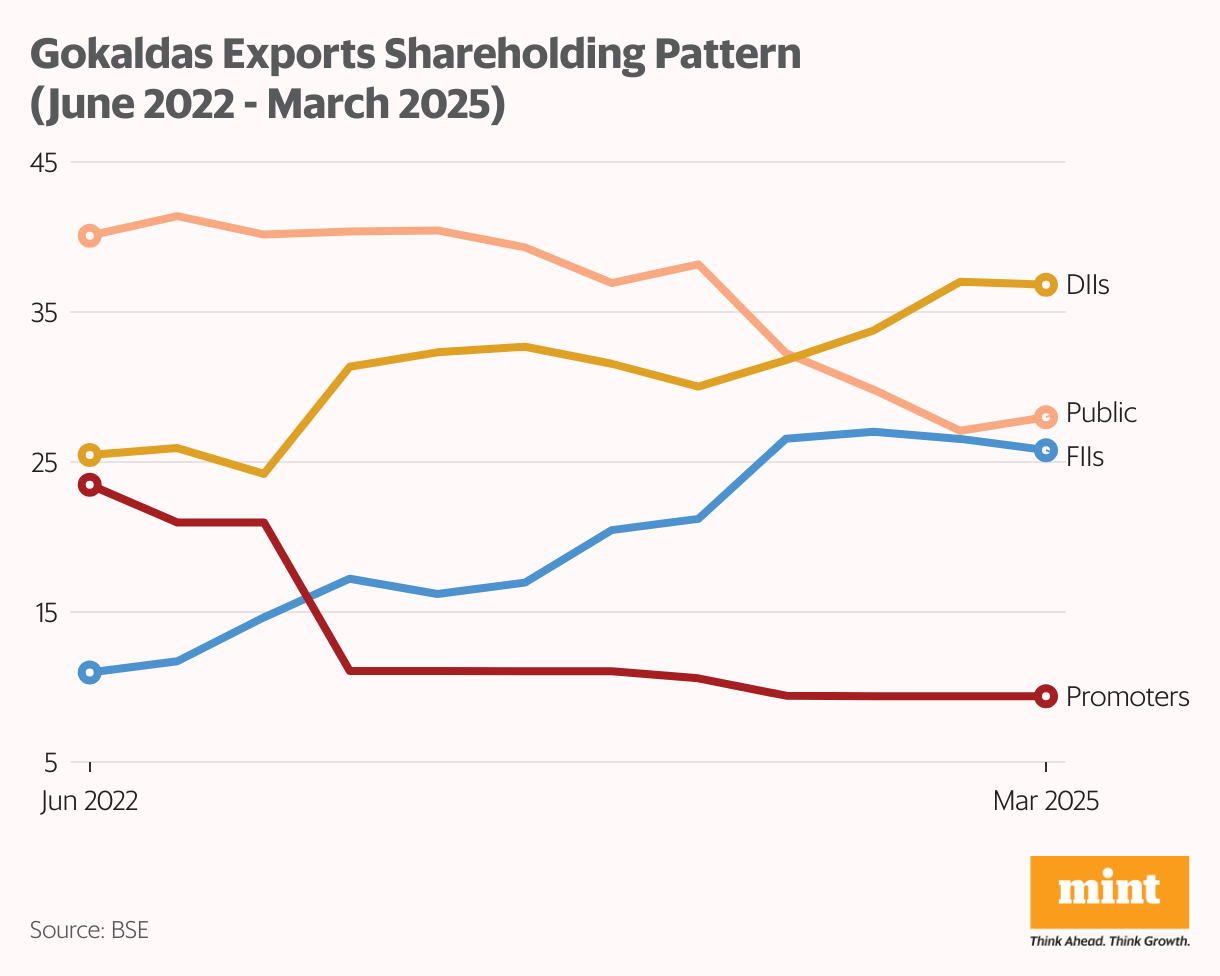

Promoter pledging clouds rally

Over the last couple of quarters, Gokaldas Exports has witnessed rising institutional interest on account of its growth prospects.

Domestic institutional investors (DIIs) have gradually increased their stake in Gokaldas Exports from 25.46% in June 2022 to 36.82% in March 2025, making them the largest shareholder group. Foreign institutional investors also have ramped up their stake in Gokaldas Exports aggressively, from 10.97% to 25.79% during the same period.

However, a key concern is that promoter ownership in Gokaldas Exports stands at just 9.38%, with 96.3% of promoter shares pledged as collateral, an unusually high level even in capital-intensive industries.

While pledging is not inherently negative, a level this high can expose shareholders to significant downside risk. If the company underperforms or the share price drops, lenders may invoke the pledge, triggering forced selling and sharp stock corrections.

A bumpy road

Gokaldas Exports is clearly benefiting from multiple macro trends that have bolstered investor sentiment. However, the road ahead is not without bumps. Margin pressure, rising debt, and an unusually high level of promoter pledging cast a shadow over the company’s growth narrative.

For investors, the stock offers high growth potential but also high risk. Keeping an eye on margin recovery, execution of new capacities, and promoter-level developments will be critical in assessing whether this momentum can turn into durable long-term performance.

Ayesha Shetty is a research analyst registered with the Securities and Exchange Board of India and a certified Financial Risk Manager.

Disclosure:The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.