But with high leverage, thin margins, and rich valuations, the offer comes with its share of risks.

Read this | Why is walking on eggshells beyond Gurugram, its home turf

Deleveraging through IPO

Kalpataru Ltd, the developer behind the upcoming offering, is currently 100% promoter-owned. Post-IPO, the promoters will dilute 18.6% of their stake, bringing their holding down to 81.4%.

Of the ₹1,590 crore raised, ₹1,193 crore is earmarked for debt repayment across Kalpataru and its subsidiaries, while ₹397 crore will be allocated for general corporate purposes. At the upper end of the price band, Kalpataru’s market capitalization will stand at ₹8,524 crore.

The issue coincides with ongoing deleveraging efforts. The company previously converted ₹1,440 crore of compulsorily convertible debentures into equity. The IPO proceeds, alongside robust pre-sales, are intended to reduce leverage further and unlock capital for development.

Strong brand in a concentrated market

Kalpataru belongs to the diversified Kalpataru Group, which has interests spanning power transmission, oil & gas, railways, and other sectors.

In real estate, it brings over 55 years of experience, with a dominant presence in the Mumbai Metropolitan Region (MMR)—India’s most valuable property market.

The company also operates in Pune, Hyderabad, Bengaluru, Indore, and Jodhpur, but Mumbai remains its core market. As of December 2024, Kalpataru ranked fifth in Greater Mumbai and seventh in Thane by units supplied. While it covers all income segments, nearly 40% of residential sales come from ultra-luxury, followed by high-end (37%), luxury (19%), and mid-end (4%).

Execution pipeline, asset-light strategy

Over the years, Kalpataru has delivered 120 projects covering 25.9 million sq. ft. and holds a development pipeline of 49 million sq. ft. across ongoing, upcoming, and planned projects.

Approximately 95% of this pipeline is residential, with nearly 70% concentrated in the MMR. New launches are scheduled through FY25 to FY27. The company also holds 1,886 acres in land reserves across key cities, offering room for future expansion.

To optimize capital deployment, Kalpataru has been increasingly adopting an asset-light model via joint ventures, joint development agreements, and redevelopment projects. It currently operates 13 such projects, with a combined developable area of 12.4 million sq. ft. This model is expected to remain a major growth lever.

Geographical and funding constraints

However, Kalpataru’s tight geographical concentration remains a vulnerability. Around 95% of its active and planned projects are in MMR and Pune, exposing it to region-specific risks.

Read this | Why Macrotech is upbeat about its prospects even as India’s realty market braces for a slowdown

Some peers, including Oberoi Realty and Sunteck, face similar concentrations but have begun expanding into tier 1 and tier 2 cities—something Kalpataru may eventually need to pursue more aggressively.

Funding remains another challenge.

Development relies heavily on project completions and borrowings, limiting flexibility to acquire or launch new projects independently. As of April 2025, total borrowings stood at ₹10,186 crore, translating to a debt-to-equity ratio of 4.1x. This will likely drop to 2.2x after IPO-related debt repayments, but will still remain elevated compared to peers like Sunteck (0.8x), Sobha (1.2x), and Prestige (0.6x).

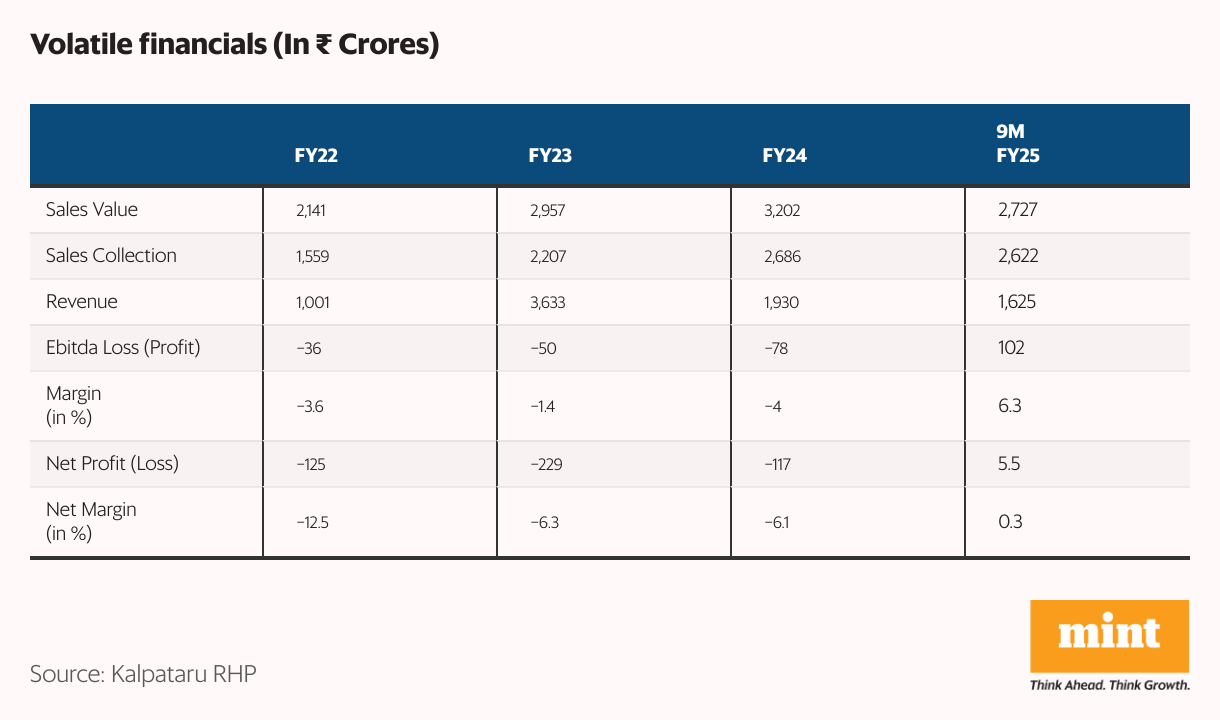

Sales improving, profits lagging

Kalpataru’s sales performance has been on an upswing, with revenue growing at a CAGR of 29% during FY22–FY25 to reach ₹2,166 crore (annualized). Yet profitability has remained underwhelming due to high finance costs and thinner margins, despite its premium positioning.

In FY25, net margin was just 0.3%—significantly below peers such as Kolte Patil (2.3%), Sobha (4%), Sunteck (6.2%), and Brigade (13.5%). That said, its premium focus delivers higher sales realizations per sq. ft. ( ₹13,304), ahead of rivals like Sobha and Brigade.

The company paid ₹104 crore in interest in FY25. With ₹1,193 crore debt likely to be cleared using IPO proceeds, interest costs should ease somewhat, creating headroom for improved profitability in FY26 if execution strengthens.

Premium market demand and redevelopment potential

Kalpataru’s IPO comes at an opportune moment: housing demand—particularly in the premium segment—is booming. The aging housing stock in Mumbai offers significant redevelopment potential. Kalpataru already has active projects in areas such as Bandra East and Juhu, with more in the planning stages.

Read this | Bumper launches in FY26, but a note of caution on home prices

While its current footprint remains focused on top-tier cities, expansion into emerging tier 2 locations—much like its peers—could offer diversification benefits and future growth.

Valuation leaves little room for error

Valuations, however, appear stretched.

According to Deven Choksey Research, the IPO is priced at 186x FY25 (annualized) EV/Ebitda—a steep premium to peers such as Kolte Patil (52x), Sunteck Realty (23x), Signature Global (28x), and Prestige (29x).

For more such analyses, read Profit Pulse.

Kalpataru offers scale, brand strength, and deep experience in Mumbai’s lucrative real estate market. But its elevated leverage and thin profitability remain key risks. The IPO offers exposure to India’s most resilient housing market—but at a price that leaves little margin for missteps.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.