After a brief setback last year, shares of railway companies are back on investors’ radar owing to a combination of sustained order wins and positive market sentiment. RailTel Corp. of India Ltd, Rail Vikas Nigam Ltd, and RITES Ltd have seen their stock gain more than 20% over the past month.

Indian Railway Finance Corporation Ltd, which is the primary lending arm of Indian Railways, also has been riding this wave of optimism.

The IRFC stock is up 8.8% over the past five trading days on NSE, and up 4.29% over the past month, in part due to the government’s approval for the company to raise up to ₹10,000 crore via deep discount bonds.

However, despite the recent rally, shares of IRFC, once a once a market favourite thanks to its predictable earnings and quasi-sovereign backing, are down by more than 20% over the past year.

Stagnating revenues

Indian Railway Finance’s recent underperformance stems from a key issue—declining disbursements. As a result, its revenue growth dropped to 1.9% in 2024-25 from an average of 19% during FY21-FY24, and profit growth to 1.4% in FY25 from about 38% in FY21 and FY22.

IRFC’s assets under management, too, have remained stagnant despite the government allocating ₹2.5 trillion to the Indian Railways in its Union Budgets for FY25 and FY26.

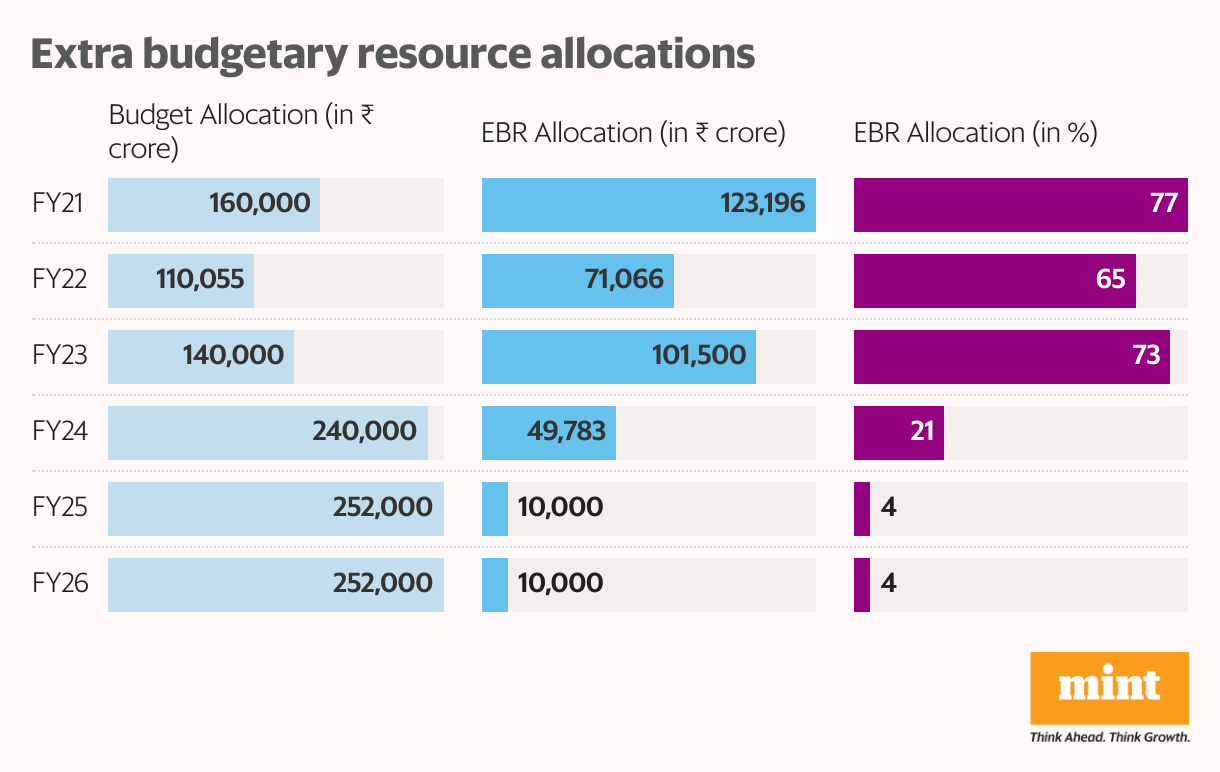

IRFC primarily raises funds and lends money exclusively to Indian Railways, earning interest income in return. However, Indian Railways does not solely rely on IRFC for funds. It receives funds directly from the government as well, known as budgetary resources. Funding from IRFC is known as an extra budgetary resource (EBR).

While the government’s budgetary support for Indian Railways has increased tremendously since FY22, extra budgetary resources have been scaled back, resulting in declining sales growth for IRFC.

There was no requirement for extra budgetary resources for Indian Railways in FY24 due to the high budgetary support. Even for FY25, the budget had no explicit EBR requirement from IRFC. For FY26, too, over 96% of Indian Railways’ ₹2.52 crore capital expenditure is being covered through gross budgetary support (GBS).

This has dampened investor sentiment on IRFC, raising questions about the company’s future trajectory.

Diversifying beyond Indian Railways

While Indian Railway Finance has traditionally focused on railway financing, the reduction in EBR support has prompted the company to explore other revenue sources.

Indian Railway Finance is actively exploring opportunities to diversify into sectors with forward and backward linkages to the railways, such as ports and logistics, as well as infrastructure projects.

It is also exploring opportunities to fund railways-related rolling stock and renewable energy requirements, container train operators, metro rail and rapid rail infrastructure projects, port rail connectivity projects, and public-private partnership projects sanctioned by Indian Railways.

As part of this shift, IRFC is targeting disbursements of around ₹30,000 crores in FY26.

Also read | Why Tata Teleservices is drawing institutional bets despite mounting losses

In just the past three months, the company has won three consecutive bids, securing around ₹14,000 crore in assets. These projects offer better margins—100 basis points as against 40 bps that the company used to get from Indian Railways. Its net interest margin is expected to improve from 1.4% to 2%.

Currently, non-railway assets account for less than 1% of IRFC’s book, but the company’s management anticipates a steep rise in the share of such assets, with each new loan enhancing IRFC’s net interest margin.

Indian Railway Finance has also announced a ₹3,200 crore loan to Patratu Vidyut Utpadan Nigam and a ₹7,500 crore rupee term loan to NTPC Renewable Energy Ltd.

Pivoting beyond, yet powered by the Railways

Despite IRFC’s strategic pivot to other sectors, the company’s role as the primary financing arm for Indian Railways ensures its relevance.

Even with no EBR allocation, the company is positioned to benefit directly from the increased budgetary allocations to Indian Railways.

In the Union Budget for 2025-26, the government announced ambitious plans to expand and modernize India’s railway infrastructure. This includes the rollout of 200 new Vande Bharat trains, 100 Amrit Bharat trains, and 50 Namo Bharat trains.

The government also announced a major push toward cargo transport, with a target to move 1.6 billion tonnes of freight by the end of the year, positioning India as the second-largest freight mover globally.

To support these plans, the government has outlined large-scale projects for laying new tracks, upgrading existing routes, and deploying modern trains.

IRFC is well positioned to benefit from projects across this value chain, reinforcing its critical role in India’s railway ecosystem, even as it expands into new sectors.

Also read | Info Edge: Can India’s job giant stay on top in 2025?

Strong fundamentals but not without risks

Despite IRFC’s disappointing sales and profit growth over the previous two years, its fundamentals stand strong.

The company’s sales and profit have grown at a compound annual growth rate of 15% over the previous five financial years on account of steady disbursements. It also has a strong operating margin of 99-100% and a net profit margin of 24%.

While IRFC’s fixed lending spread model limits profitability, its strategic relationship with the ministry of railways has helped maintain a low cost of borrowing. This along with minimal operating expenses and a tax-exempt status has supported the company’s profitability.

These margins have enabled IRFC to build a healthy cash reserve of Rs. 6,143 crore as of 31 March. It also has sanctioned credit lines of ₹7,417 crore, ensuring ample liquidity support.

Another standout metric is IRFC’s asset quality. Since the sole borrower for a majority of its portfolio is the ministry of railways, a sovereign entity, IRFC faces virtually no credit risk.

As a result, the company has consistently reported nil non-performing assets, or loans turned bad.

This unique borrower profile provides IRFC with unmatched stability and predictability of cash flows, which significantly enhances its risk-adjusted return profile.

Also read | Defence stocks are soaring again, but can fundamentals support the rally?

Going forward, the management expects the company’s financials to remain robust for about two years due to income from past investments. This is because the moratorium period on leases signed in previous years (2017-18 onwards) will end soon, and the Indian Railways will start making lease payments, providing a steady cash flow for IRFC.

The company plans to use this window to actively roll out its diversification strategy, positioning itself for sustainable growth beyond its current business model.

That said, rating agency ICRA expects IRFC’s portfolio diversification to increase the proportion of risk-weighted assets in the company’s portfolio. Moreover, if loan growth accelerates significantly relative to internal capital generation, IRFC may need to raise fresh capital to maintain a prudent capitalization profile.

Conclusion

Indian Railway Finance Corp.’s revenue and profit growth slowed significantly in the previous two financial years on account of declining EBR allocations for the Indian Railways. And with no targets for FY26 as well, the company’s traditional leasing model is under pressure.

However, IRFC is actively laying the groundwork to diversify its loan book and turn its financials around by venturing into projects with backward and forward linkages to Indian Railways.

While revenue growth may remain subdued in the near term, the company could be well-positioned for a new phase of growth if its diversification strategy bears fruit.

Nevertheless, for now, investors must weigh the comfort of strong fundamentals against the near-term earnings plateau.

Any re-rating in the stock will likely hinge on how quickly IRFC can translate its strategic pivot into financial growth.

Ayesha Shetty is a Sebi-registered research analyst and a certified financial risk manager.

Disclosure:The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.