Recent moves by the government are accelerating this shift. It recently invited global carmakers to manufacture EVs locally in exchange for lower import duties.

Meanwhile, early investments in lithium refining are starting to materialise as players such as Lohum and Vardhaan Lithium lay the groundwork for India’s battery material supply chain.

This is opening up new opportunities, not just for automakers but also r chemical, electronics, and auto component companies enabling the transition.

For investors willing to look beyond the obvious names, this segment offers a quiet yet potentially rewarding way to ride India’s EV push.

#1 Minda Corporation

Minda Corporation is a leading auto component supplier offering system solutions across vehicle access, clusters, wiring harnesses, sensors and EV electronics. It caters to two-wheelers, passenger vehicles and commercial vehicles, with a growing emphasis on electric mobility.

FY25 was its best year yet. Revenue rose 9% to ₹5,100 crore and profit after tax (PAT) rose 12%. Margins improved as well, with Ebitda margin expanding to 11.4%. The company posted its highest-ever quarterly revenue of ₹1,321 crore in Q4. Net profit, however, declined sequentially owing to higher finance and depreciation costs resulting from the Flash Electronics acquisition.

The company acquired a 49% stake in Flash in January 2025, adding scale in EV and powertrain electronics. Flash clocked ₹1540 crore of revenue in FY25 revenue, with a 14.5% Ebitda margin and 23% of its sales from EVs. Its global footprint offers export upside, and synergies in sourcing, R&D, and cross-selling are expected to accelerate profits by FY27.

Minda’s growth is backed by order wins. It secured over ₹8,000 crore in lifetime orders in FY25, with a quarter linked to EVs. The company is also expanding capacity through two greenfield plants. Capex will remain at ₹250-350 crore a year, with order execution set to ramp up in FY26. Net debt jumped to ₹1,200 crore, but promoter warrants worth ₹420 crore are expected to ease leverage.

#2 Lumax Auto Technologies

Lumax Auto Technologies is an auto parts maker with offerings across plastic modules, gear shifters, lighting, telematics and electronics. It operates independently and through joint ventures with global players such as Jopp, Ituran and Alps Alpine.

In FY25, revenue rose 5% to ₹2000 crore, though PAT declined 21%. Margins came under pressure owing to mix shift and higher fixed costs linked to capacity expansion and R&D.

The company commissioned two new plants, one in Pune for gear shifters and another in Chennai for telematics and electronics, both of which are now ramping up.

The company’s joint venture with Ituran clocked ₹200 crore in revenue with a 12.5% margin. Its electronic telematics business is already profitable and serves more than 1.1 million vehicles in India.

Meanwhile, the Alps JV is expected to break even in FY26. Combined, the electronics business (including JVs) contributes over 25% of consolidated revenue.

Order inflow in FY25 stood at ₹1000 crore, of which nearly half came from EV programmes. Capex of ₹400 crore capex is planned over FY26-27. Management is targeting ₹3000 crore in consolidated revenue over the next three years.

#3 Hero MotoCorp

Hero MotoCorp is India’s largest two-wheeler company by volume, with a strong market position. Its products spans motorcycles, scooters, and electric vehicles. Its recent focus has shifted toward premiumisation, global markets, and EV adoption.

In FY25 revenue rose 7% to ₹37,000 crore, driven by 5.7% volume growth. PAT rose 28%. Operating margin expanded to 11.5% on better product mix and cost control. In Q4FY25 revenue was flat, but net profit rose 18% year-on-year.

Sales of premium motorcycles (150 cc and above) crossed 100,000 units in a quarter for the first time in Q4, led by new launches like Mavrick 440. The company is also ramping up exports, with volumes growing 20% year-on-year in Q4, though they still account for less than 4% of total sales.

In EVs, Hero is expanding its Vida brand and charging ecosystem. It also holds a 35% stake in Ather Energy. EV sales touched 10,000 units in Q4FY25 and new models are slated for launch in FY26. The upcoming EV plant in Andhra Pradesh will support the scale-up.

The company ended FY25 with ₹5300 crore net cash and announced a ₹1,000 crore buyback. Capex guidance stands at ₹1,000 crore for FY26, focussed on premium bikes, EVs, and global growth.

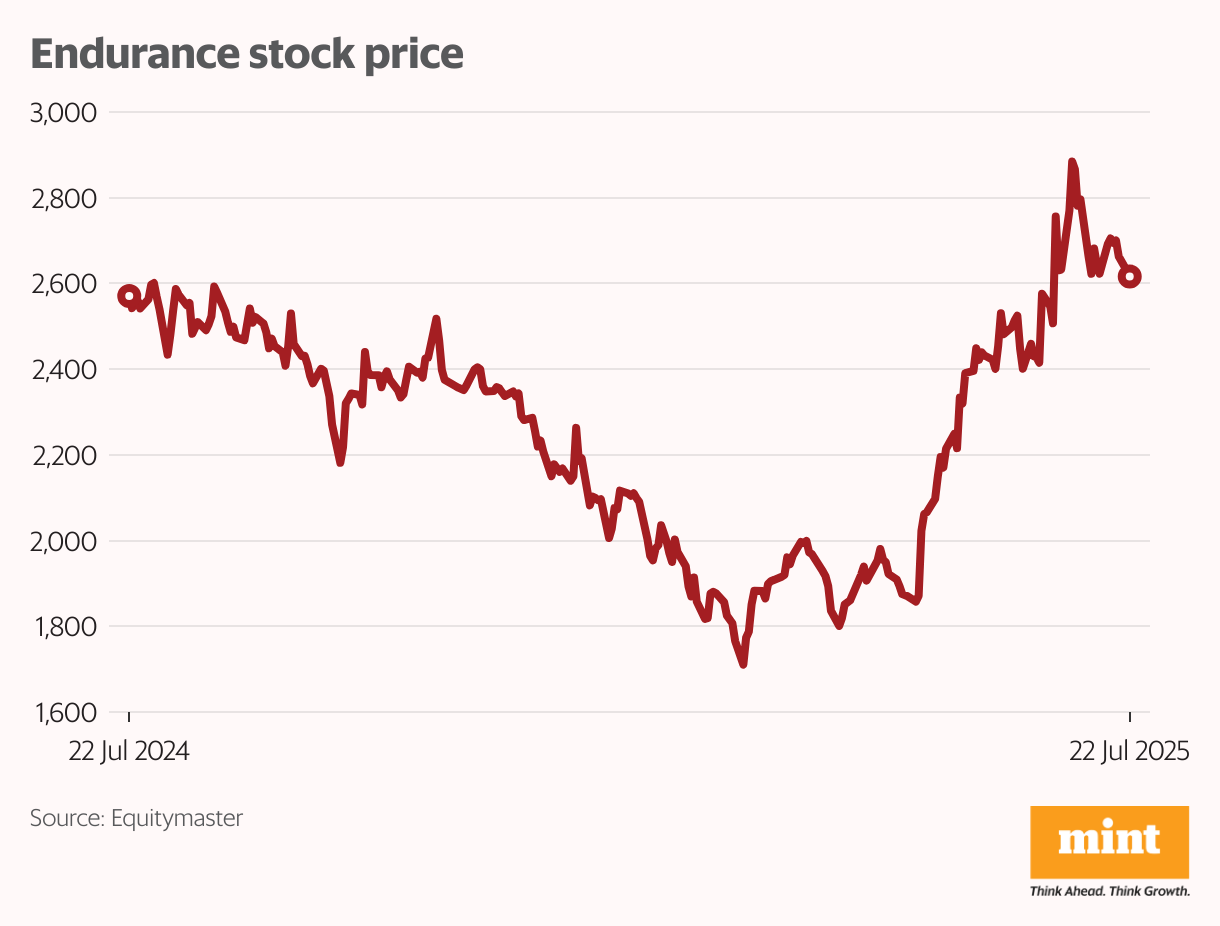

#4 Endurance Technologies

Endurance Technologies is a diversified auto component supplier with presence across suspension, braking systems, aluminium die casting and EV parts. It serves Indian two-wheeler and three-wheeler original equipment manufacturers. Through its European arm, it supplies powertrain components to global passenger vehicle makers.

In FY25 revenue rose 9% to ₹11,600 crore, with India contributing 78% and Europe 22%. PAT rose 12% to ₹800 crore. Margin was stable at 14.3%.

Cost control and rising contribution from premium products helped offset softness in Europe. In Q4FY25, revenue rose 8% and Ebitda climbed 11% year-on-year.

The company’s growth is being driven by robust order wins and a rising share of EV programmes. In India, Endurance secured ₹1,200 crore worth of new orders in FY25, of which 49% were linked to EVs.

Its Maxwell unit, which focuses on EV power electronics, contributed ₹70 crore in revenue during the year. In Europe, the company won €208 million worth of new business tied to EVs and hybrids, accounting for 84% of total new orders over the next five years.

Endurance is guiding for a capex of ₹500-600 crore in FY26, aimed at expanding capacity for EV systems and aluminium castings. It is also enhancing Maxwell’s platform to support higher-voltage applications.

#5 Himadri Speciality Chemical

Himadri Speciality Chemical is a carbon-based chemical manufacturer with a growing portfolio in advanced materials for lithium-ion batteries, speciality black and performance chemicals. It supplies to end-markets such as aluminium, rubber, textiles and increasingly, energy storage, and EVs.

In FY25 revenue declined 7% to ₹3,100 crore on the back of falling volumes and soft realisations. Gross margins improved, though, as raw material costs cooled, but the net profit dropped 23%.

What’s drawing investor interest, however, is the company’s aggressive pivot toward the energy transition. Himadri has committed ₹4,800 crore in capex over five years for advanced carbon materials used in lithium-ion batteries.

This includes an integrated anode plant with a capacity of 200,000 tonnes per annum (TPA) and a speciality carbon black plant with a capacity of 30,000 TPA. Construction for phase 1 has begun and trial production is expected to start by mid-FY26.

The company has already signed offtake agreements with leading global players and 60–70% of the project is expected to be export-linked. It holds net cash of over ₹1,000 crore, with an additional fundraise likely through debt and strategic investors. Management expects peak revenue potential of ₹8,000 crore from the battery material business by FY30.

Conclusion

The EV industry’s huge opportunity is impossible to ignore. As the planet embraces cleaner mobility, an increasing number of companies are establishing their presence in battery materials.

Some are adding capacity, while others are entering worldwide partnerships. Many are developing new chemistries that meet the requirements of lithium-ion batteries.

Though the story is exciting, investors need to proceed with caution. Business potential is only one aspect of the equation. You also need to consider valuations, profit margins, debt, R&D expenditure and return ratios before making an investment decision.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com