Investors may be enticed by strong fundamentals or promising innovations, but certain companies face regulatory challenges that could dramatically disrupt valuations, progress, and public trust.

Some companies discussed below operate almost as duopoly businesses with high degree of visibility on revenue and profit.

But in India, companies operating in duopoly industries are also subject to a lot of government control and have a compliance burden to ensure they don’t misuse their dominance to harm consumers.

India’s regulatory landscape is complex – shaped not just by market dynamics but by broader national priorities such as consumer protection, digital sovereignty, fiscal transparency, and social impact.

As a result, sectors and companies that may once have flourished under lenient or ambiguous rules now find themselves exposed to sudden, sweeping regulatory interventions.

In recent years the Indian government and regulators such as Sebi, RBI and Trai have become far more proactive, sometimes even aggressive, in plugging legal loopholes, enforcing consumer protections, and asserting jurisdiction over grey areas.

While these steps are often well-intentioned, aimed at transparency, fairness and long-term stability, they can have immediate and significant consequences for publicly listed companies.

Understanding regulatory risk is no longer a matter of long-term legal forecasting – it’s a core part of due diligence for any serious investor in Indian equities.

In this article, we highlight five companies that are operating in highly regulated environments and thus carry significant risks.

#1 ITC

Established in 1910, ITC is India’s largest cigarette manufacturer and seller. The company operates in five business segments – FMCG, cigarettes, hotels, paper and packaging, and agriculture.

ITC is the leader in the organised domestic cigarette market with a share of over 80%. The cigarette business contributes to 40% of revenue but almost 81% of the earnings before interest and tax (Ebit).

In the FMCG business, which contributes 23% of revenue, the company owns more than 25 brands such as Sunfeast, Aashirvad, Bingo, Savlon, Fiama and Classmate.

The hotels business was established in 1975 and contributes 3% of revenue. ITC operates the second-largest hotel chain in India with 108 hotels across 70 locations.

The agriculture business contributes 23% of revenue. ITC is the second-largest exporter of agriculture products from India. It trades in food grains, marine products, processed fruits, and coffee.

It is also the leader in the value-added paperboards market, which contributes 11% of revenue.

As ITC derives majority of its revenue from the cigarette business, regulatory risks such as high taxes on cigarettes to discourage consumption, advertising and marketing restrictions, and ethical and ESG scrutiny may hamper company’s profitability.

ITC Ltd reported 10.9% growth in revenue from operations in FY25. However, Ebitda growth was flat as margins deteriorated from 37% to 34%. With prospects of a normal monsoon and green shoots visible in rural demand, management has guided for a revival of consumption in the coming quarters.

ITC stock is down 20% over the past year owing to subdued financial performance.

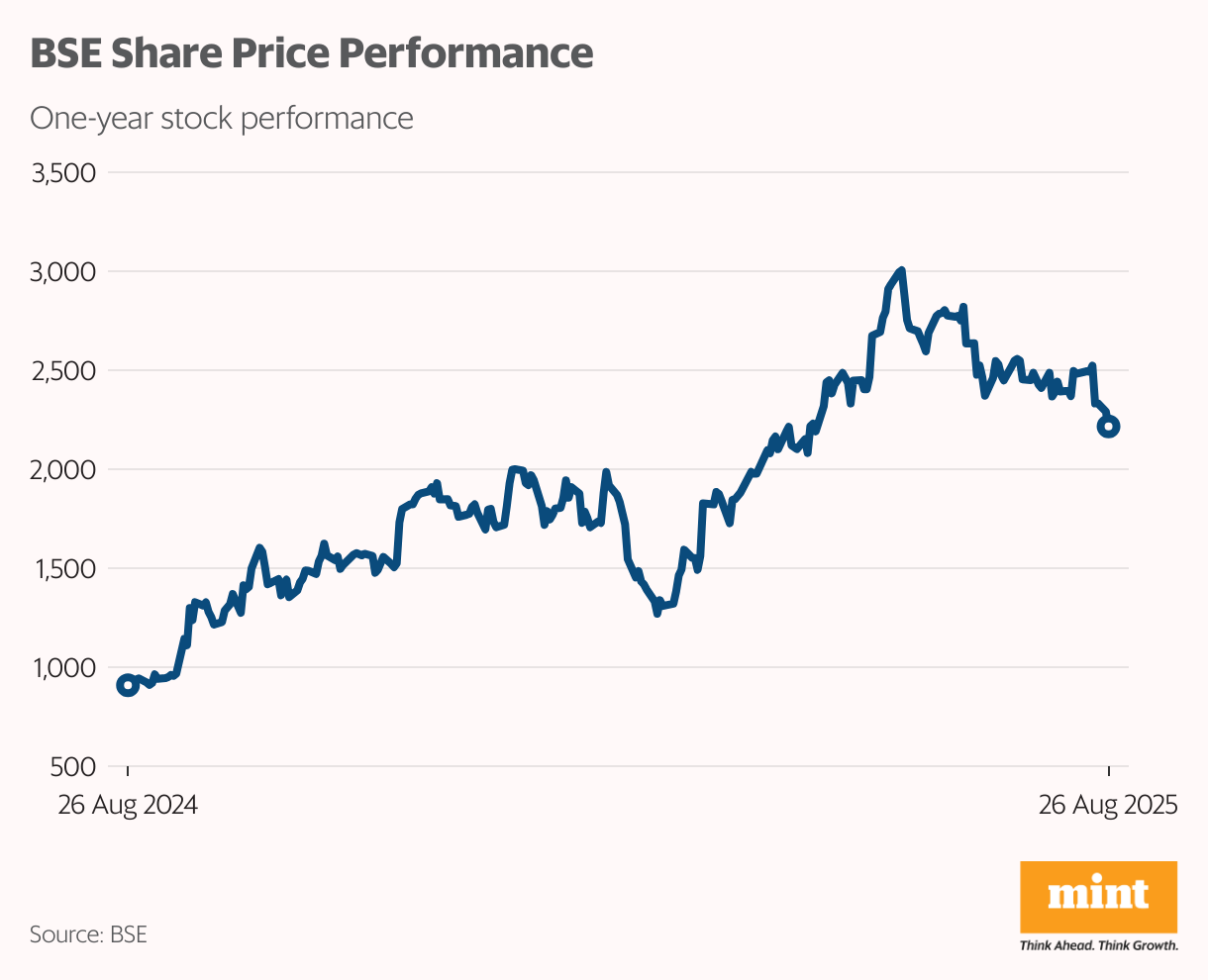

#2 BSE

BSE has long been one of India’s most prominent financial institutions, serving as a gateway for investors seeking to capitalise on the country’s robust economic growth.

For decades, BSE-listed companies have played a pivotal role in creating wealth for investors, with numerous success stories of individuals who turned modest investments into millions.

The company facilitates a market for trading in equity, currencies, debt instruments, derivatives, and mutual funds. It provides a platform for trading in equity, debt, equity derivatives, currency derivatives, commodity derivatives, SME, SME Startups, interest rate futures, and the e-agricultural spot market. It also offers listing services for equity, debt securities, mutual funds, and commercial papers.

The company’s market share across various segments is as follows: companies/securities listed: 73%, interest rate derivatives: 66%, debt/fixed income: 39%, currency derivatives: 28%, equity derivatives: 4%, equity cash 8% and commodity derivatives: 9%.

It derives 44% of revenue from securities services, 45% from corporate services, 6% from data dissemination fees, and 5% from other services.

Risks include the potential negative impact of stricter Sebi rules on its products and revenue, such as changes to derivatives tenures, and the general risk of future enforcement actions for laxity in oversight or systemic flaws.

The company recorded 105% revenue growth for FY25 on the back of increased market activity. Ebitda margins came in at a record 58% for the year, up from 45% in FY24.

Management is cautiously optimistic about the IPO market and broader capital-market activity, but acknowledges macro and regulatory uncertainties.

BSE’s stock has jumped 144% over the past year on the back of exceptional financial performance.

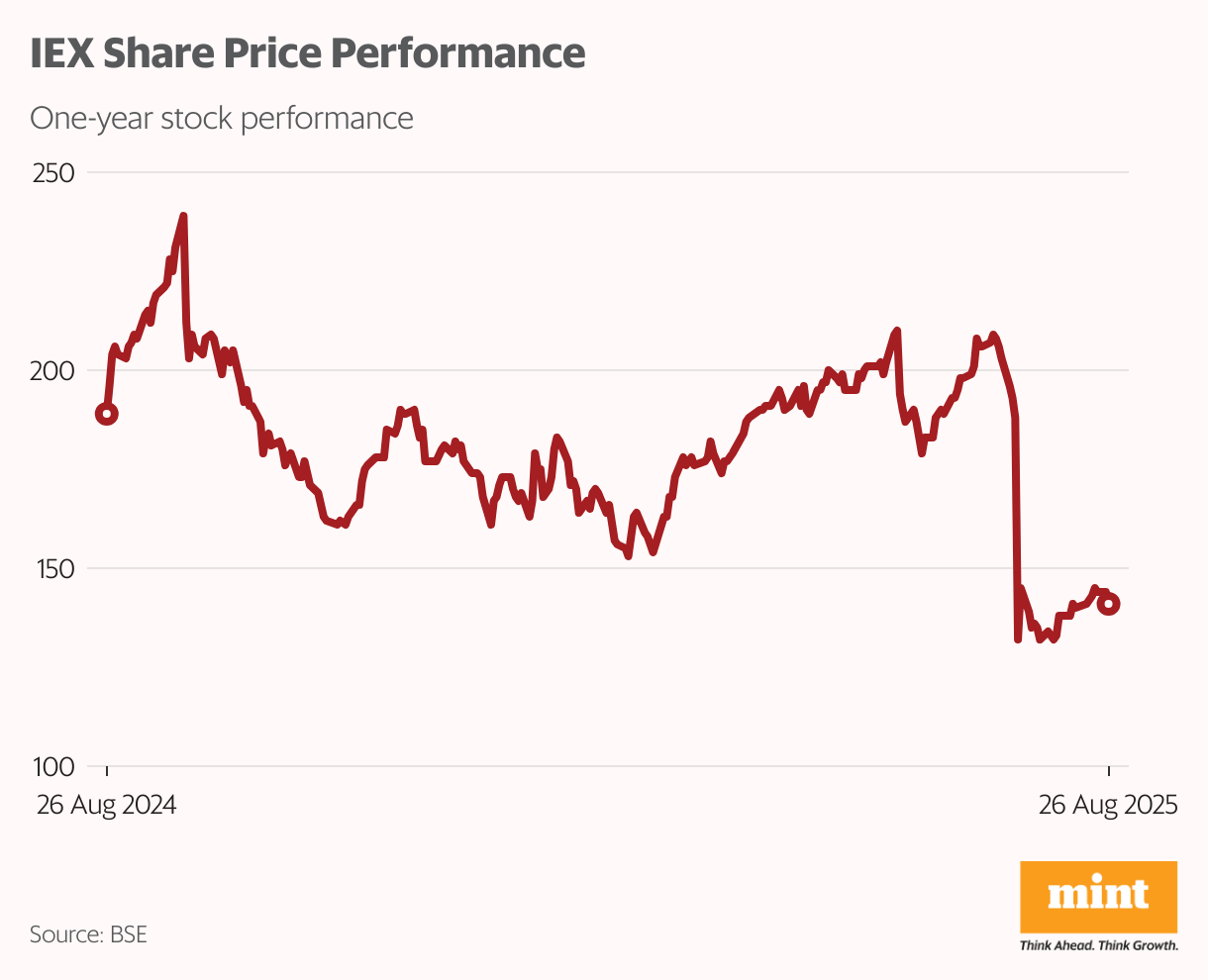

#3 Indian Energy Exchange

Incorporated in 2007, Indian Energy Exchange Ltd (IEX) provides an automated platform and infrastructure to trade units of electricity. It ispremier electricity exchange”>India’s premier electricity exchange with an85% market share, offering a nationwide, automated trading platform for the physical delivery of electricity, renewable power, renewable energy certificates, and energy-saving certificates. It improves price discovery, market accessibility, and trade efficiency in India’s power sector.

IEX operates in various segments such as the day-ahead market (44% of revenue), real-time market (29%), certificates (11%), term-ahead market (7%), green market (7%), and others (2%).

It has more than 8,100 registered participants including more than 850 electricity generators, 75 distribution companies (discoms), and 5,000 commercial and industrial consumers. Its network includes more than 2,400 renewable energy generators & obligated entities, 200 ESCert entities, and 20 cross-border portfolios.

IEX’s recent struggles are due to are due to theCentral Electricity Regulation Commission’s (CERC) approval ofpower market coupling,a regulation expected to consolidate price discovery across multiple exchanges and dilute IEX’s market dominance and revenue.

This regulatory change reduces IEX’s current edge and has led to a sharp drop in its share price, with analysts predicting a significant decline in its market share.

IEX reported robust 19.6% growth in consolidated revenue for FY25. Ebitda margin remained consistent at 84% and profit after tax grew 20%.

Management expects to retain a dominant market share post-coupling, citing deep customer relationships, tech and service edge. Also, only the day-ahead market is being coupled for certain; there’s ambiguity around including the green day-ahead market.

The company’s stock is down 25% over the past year owing to these regulatory challenges.

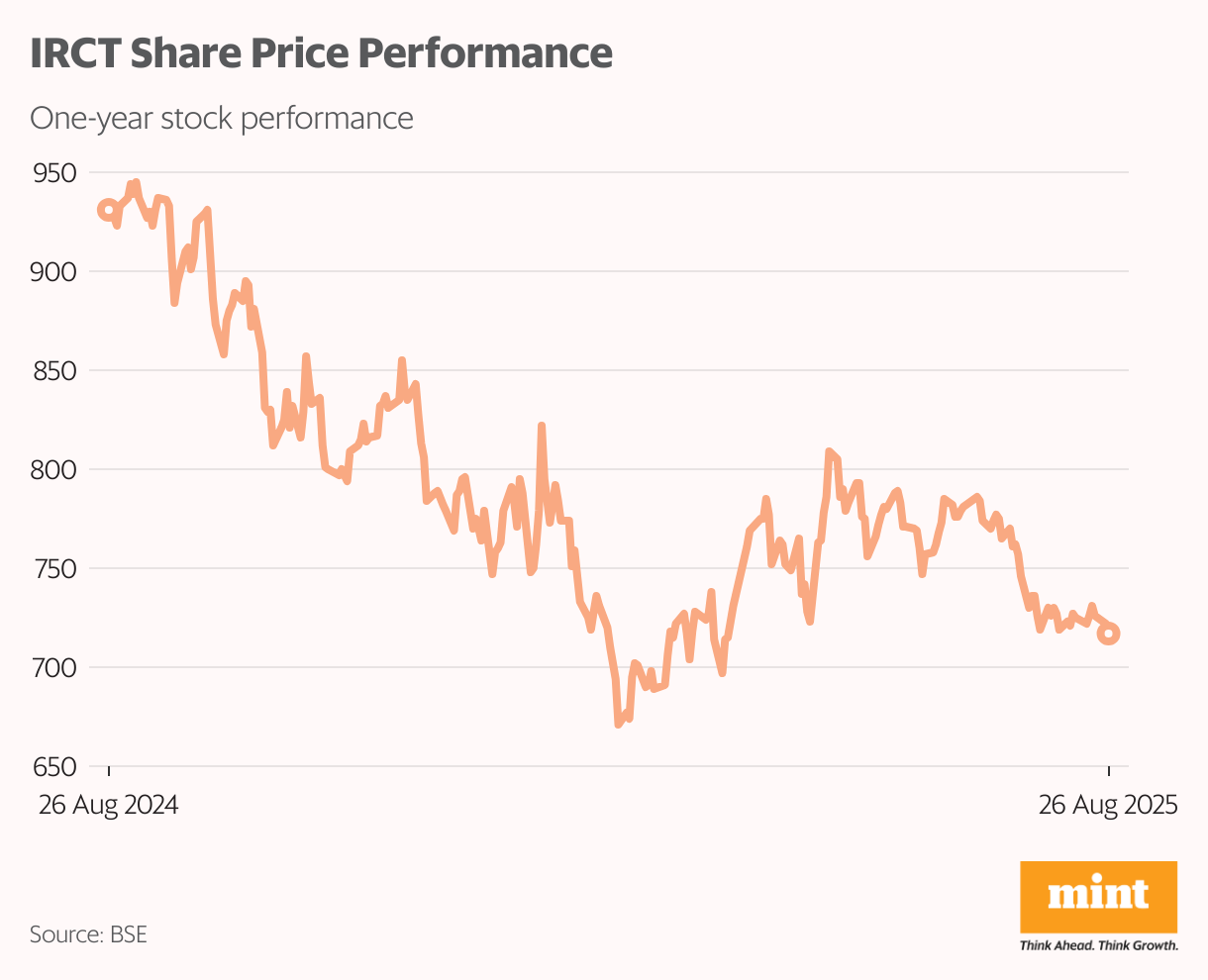

#4 Indian Railways Catering and Tourism Corporation

Incorporated in 1999, IRCTC is a ‘Miniratna’ public-sector unit and the only company authorised by the Indian government to provide online railway tickets, catering services, and packaged drinking water at Indian railway stations and trains.

The company has four business segments:

- Catering (47% of revenue): The company offers food and beverage delivery services to train passengers. It serves more than 1.6 million meals daily through a network of 2,000 partners.

- Internet ticketing (30%): IRCTC also sells tickets through its website and mobile app, which accounted for82.68% of Indian Railways’ online bookings in FY24. It operates an e-ticketing system with a high-capacity server that can handle more than 28,000 tickets a minute.In FY24 it sold an average of 1.2 million tickets a day, up 8% from 1.1 million in FY22.

- Tourism (16%): IRCTC offers packages for various durations and themes, catering to religious pilgrimages, wildlife adventures, and leisure getaways. It also provides domestic and international air travel packages. It has specially designed tours for NRIs, Ram Katha Yatra, Kashi Tamil, Saurashtra Tamil Sangam, and so on. In FY24 it organised 337 trips of Aastha trains, carrying half a million passengers.

- Rail Neer (7%): Rail Neer is a brand of packaged drinking water bottled and distributed by IRCTC to more than 410 Indian railway stations.

The company’s primary regulatory risks stem from its government ownership and dependence on the ministry of railways for policies and pricing, which could hurt its revenues and market share.

IRCTC Ltd reported 9.7% growth in revenues for FY25, while profit after tax grew 10.4%. Ebitda margin deteriorated from 34.4% in FY24 to 33.2% in FY25.

Management expects catering revenue growth to continue at a 15% compound annual rate, with potential upside from future tariff hikes. The company also anticipates further growth in ticketing revenues from expanded services, including flights and buses.

Shares of IRCTC are down 23% over the past year owing to weak operational and financial performance.

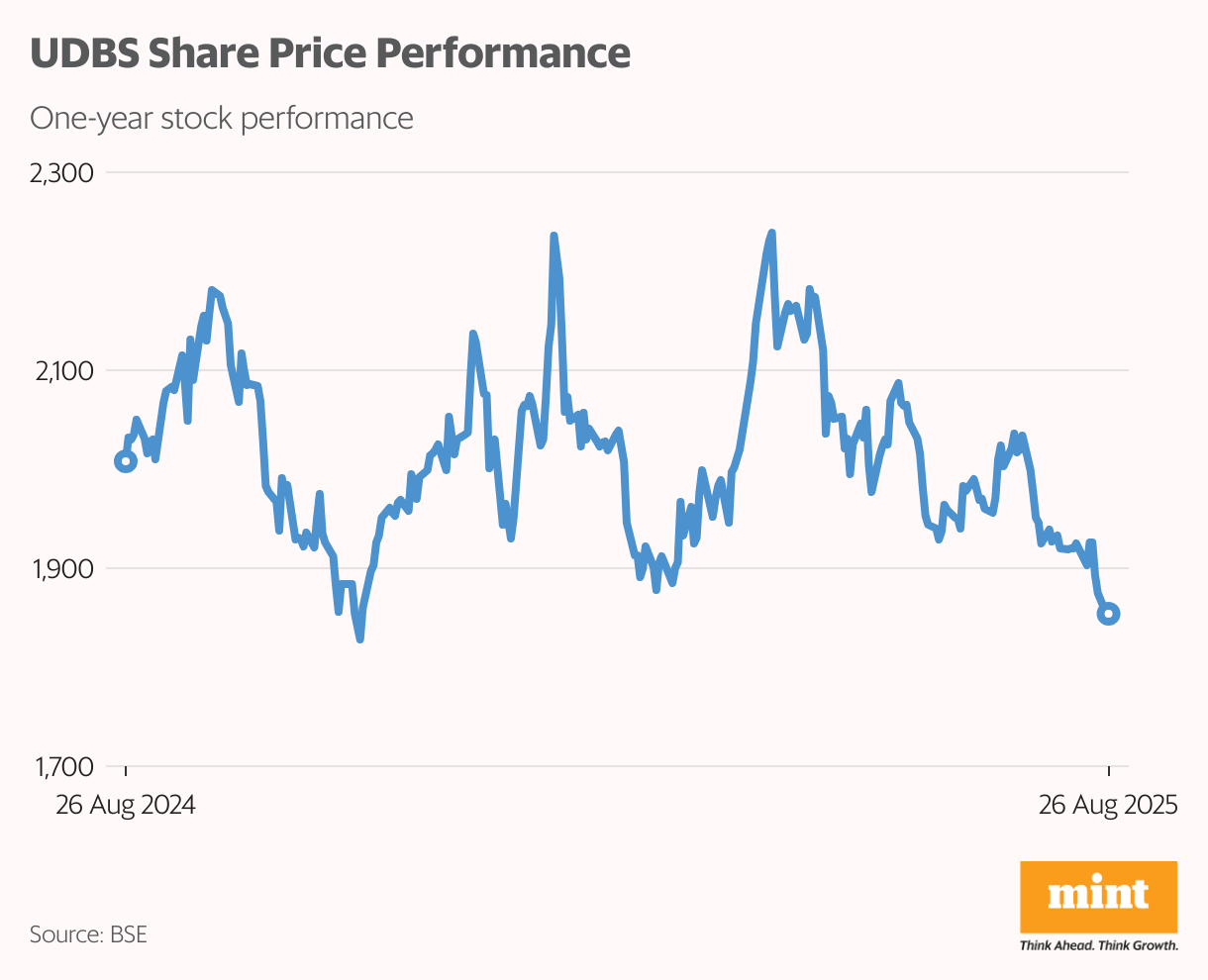

#5 United Breweries

United Breweries Limited (UBL) manufactures and sells beer and non-alcoholic beverages. Its most popular products include Kingfisher Premium, Kingfisher Ultra, Kingfisher Strong, Kingfisher Ultra Max, UB Export Lager and London Pilsner. It has a 54% share of the Indian beer market.

United Breweries also has a presence in more than 50 countries and plans to continue expanding into new markets in the future. However, it derives 99% of revenue from the Indian market and only 1% from exports.

The company owns 20 facilities and has 10 contract manufacturing arrangements across India. It has expanded its Kingfisher Ultra Draft offering in the lighthouse market of Maharashtra.

United Breweries faces regulatory risks from varying and evolving state-level alcohol policies, high and unpredictable state excise duties and taxes, and government intervention in pricing and distribution.

The company reported muted 5.6% growth in consolidated revenue from operations for FY25. Ebitda margin improved to 4.3% from 3.8% in FY24, leading to a 7.7% increase in profit after tax.

Management is extremely cautious in terms of outlook for gross margins, expecting short-term pressure owing to contract brewing and input cost inflation, but is confident of an improvement in the medium term as capacity and bottle recovery improve.

Shares of United Breweries are down 8% over the past year due to its underwhelming financial performance.

Conclusion

The Indian equity market continues to offer attractive investment opportunities through companies with strong market positions, consistent profitability, and long-term growth potential.

However, even market leaders are not insulated from external headwinds, particularly those arising from regulatory changes.

While this is a necessary evolution to ensure transparency, consumer protection, and long-term sectoral health, it introduces an additional layer of complexity for investors.

That’s what robust due diligence must include not just financial analysis but an in-depth understanding of sectoral regulations, government policy direction, and possible legal overhangs.

Past performance or market leadership is no guarantee against regulatory interventions that can upend business models overnight.

As always, investing decisions should be guided by your individual risk tolerance, financial goals, and proper due diligence. Remember the challenges before diving in headfirst.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com