Marquee IPOs from Aequs, Meesho, Vidya Wires, and Wakefit Innovations hit the Street in December and are set to take total fundraising for the year past ₹1.61 trillion across 97 issues this week surpassing last year’s ₹1.59 trillion raised from 91 issues. More IPOs are lined up for the rest of the month, making it almost certain that the calendar year will end with an even bigger bounty for companies listing for the first time.

Retail allotments now command a 24% share in the amounts raised this year, a noticeable surge from the 21% share recorded in 2024, according to Prime Database. Though this remains lower than a retail share of 27% in 2023 when ₹ 49,435.5 crore were mobilized.

Retail roar

Retail investors have seized the spotlight this year, showing unprecedented conviction in new offerings.

This year, retail investors were allotted ₹36,431 crore across 93 IPOs.This figure marks their highest capital absorption in three years, comfortably eclipsing the ₹32,957 crore received in 2024.

The rebound follows a subdued 2023, when retail absorption was around ₹13,553 crore across 57 issues, after having stood at ₹14,034 crore across 40 issues in 2022. While 2025 features a larger and more competitive issuance pipeline, the sheer volume of retail money poured into the market is a testament to their bullish sentiment.

Market participants believe this turnaround is being driven by a mix of stronger deal quality and better pricing.

“Retail participation has rebounded sharply because Indian IPOs continue to offer reasonably priced opportunities with strong near-term return potential,” said Bhavesh Shah, managing director & head – Investment Banking at Equirus Capital.

“Retail investors tend to be momentum-driven and look for quick listing gains rather than long-term compounding, and strong institutional demand gives them additional confidence.”

Headwinds ahead?

But as the calendar flips to 2026, will this surge in retail participation intensify?The outlook looks tempered as these companies typically offer a lower retail quota than the standard 30%.

“Given the significant pipeline of such issues in 2026, we may see an impact on overall retail participation,” said Pranav Haldea, managing director at Prime Database. “As a result, the numbers could remain within the 23–28% range. Since allocation is size-based and several large tech offerings are lined up, a similar pattern may repeat next year.”

Yet the enthusiasm is here to stay as analysts believe the retail revival is not only about short-term excitement but a more fundamental behavioural change is underway on how Indian households manage their savings.

According to Ravi Singh, chief research officer at Master Capital Services, the shift reflects the continuing financialisation of savings. “Retail investors increasingly view equities as a core asset class, and this structural trend means participation is likely to rise across every segment of the market over time,” he said.

HNIs stable, QIBs softer

While retail surged, high-net-worth individuals (HNIs) held steady.HNIs accounted for 13% of IPO allotments in both 2025 and 2024, in line with their shares in 2022 and only slightly lower than 15% in 2023.

In absolute terms, HNIs received ₹19,724 crore this year—almost identical to the ₹20,050 crore allotted in 2024, but far above the weaker levels seen in 2023 ( ₹7,282 crore) and 2022 ( ₹7,629 crore) .

This stability suggests that while HNIs remain an important part of IPO demand, they are not driving the expansion of the market in the way retail investors are.

Participation from qualified institutional buyers (QIBs) has softened slightly. QIBs absorbed 63% of IPO allotments in 2025, down from 65% last year but still higher than in 2023 and 2022. In absolute numbers, QIBs were allotted ₹96,357 crore—just below the ₹1 trillion distributed last year.

But the decline is not significant, according to Haldea.

“I don’t think we should overstate this difference—it will likely stay in the 63–65% range,” he said. “There could be some fluctuation because, even with tech issues that have lower retail allocation, any unsubscribed retail portion can still be absorbed by QIBs. I don’t expect that to move drastically.”

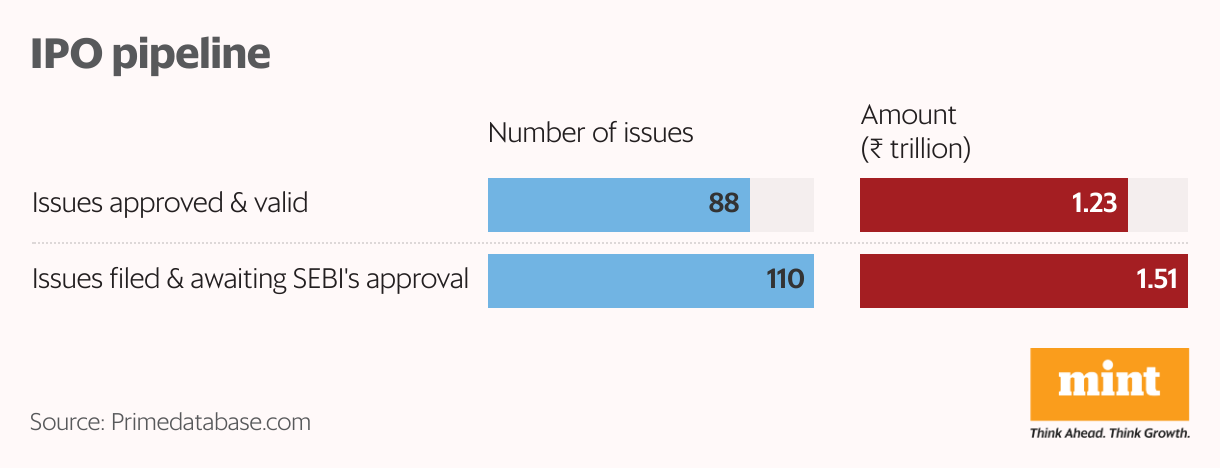

A booming pipeline

The frenzy is far from over. The market is bracing for an equally active 2026.

As of now, 88 companies have received the regulator’s approval to raise ₹1.23 trillion, while another 110 firms are awaiting approval for issues worth around ₹1.51 trillion.

According to Ratiraj Tibrewal, CEO of Choice Capital, both cyclical and structural factors are sustaining the wave of retail interest.

“A strong equity rally and steady listing gains have lifted confidence, while record SIP flows, rapid demat additions and easy-to-use digital platforms have made equities a routine part of household savings. These trends point to continued retail strength in 2026, barring a sharp market correction or a few weak listings. Retail investors are increasingly emerging as a steady, influential force in India’s primary markets.”

“If the current domestic momentum sustains, 2026 could remain an active year for the primary market, though disciplined pricing and attractive offerings will be crucial to sustain a broader participation,” said Singh.