REL will retain control of Care Health Insurance, while lending, broking, investment, and ancillary activities would be transferred to RFL.

Even though the demerger promises the unlocking of shareholder value, investors were not impressed. REL has corrected by 9% since 14 February, bringing the stock close to its support at ₹220 apiece. Despite five years of multibagger returns which tripled investor wealth, the stock is still trading below its listing price.

Let’s dive into what has been weighing on sentiment, and if the demerger can flip the story.

The demerger details

REL would effectively become Care Health Insurance, and RFL will be listed as a separate entity with the remaining financial services businesses clubbed under it. REL shareholders would receive one share of RFL for every REL share.

The demerger is subject to regulatory approvals which are expected by Q2FY27, followed by shareholder and creditors’ approval which are not likely before Q4FY27. So, it is only around Q1FY28 that one can reasonably expect the demerger to take effect.

The hope is that the creation of two independent entities will help enhance strategic and governance focus, attract capital, and unlock shareholder value. REL CFO Pratul Gupta expects the demerged entities to emerge “as leaders in their respective domains, each with the resources, focus, and flexibility to capitalize on significant growth opportunities ahead.”

Not much reason to cheer yet

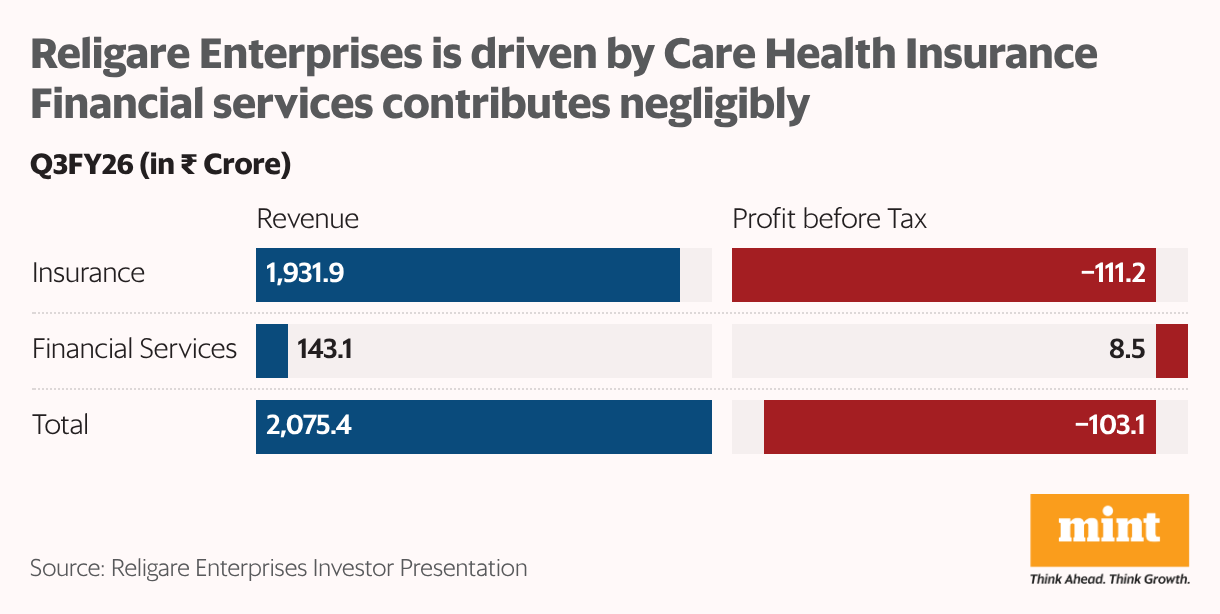

The demerger will result in a grossly uneven split of Religare’s businesses–of the ₹2,075 crore in revenue clocked by Religare during Q3FY26, more than ₹1,900 crore is attributable to Care Health Insurance. With less than ₹150 crore coming from RFL, its shareholders will be left holding a currently minuscule portion of Religare’s business.

But REL shareholders do not have much to celebrate either. Rising healthcare costs have weighed on the health insurance industry, resulting in losses at Care Health Insurance. In fact, Care’s ₹111 crore loss in Q3FY26 has overshadowed the ₹8 crore profit before tax booked by RFL, resulting in an overall consolidated loss.

Investors spooked by governance blackhole?

Religare has had a tough ride, facing one governance issue after another. The fund diversion from RFL by the erstwhile promoters a decade back was followed by a few years of stability until Dabur’s Burmans’ apparently hostile takeover made it to the news. Besides, there was a corporate power struggle against former chairperson and director Rashmi Saluja, which had opened a can of worms, from allegations of insider trading to Esop allocations that had drawn the ED’s ire.

The Burmans managed to eventually assume operational charge in February 2025 after removal of Saluja from the board with an overwhelming shareholder majority. It took only a few months after that for the RBI to lift the seven-year-long corrective action plan (CAP) imposed on RFL. This allowed RFL to resume normal business operations from July 2025. Fund infusion plans of ₹1,500 crore have also been approved, clearing the way for improved growth, and a stronger balance sheet.

But the stock has remained flat over the past one year. Most of the gains leading up to the lifting of CAP in July 2025, have been given up, and the announced demerger has not managed to lift sentiment either. Investors appear to be waiting for tangible proof of a much-needed governance makeover.

Behind Care’s losses

As India’s second-largest standalone health insurer, Care Health Insurance commands over 11% share of the market. But it is in losses, which have, in fact, expanded over the past year, from ₹69 crore in Q3FY25 to ₹111 crore in Q3FY26. Even after excluding the one-time impact of ₹13.5 crore from the new labour codes incurred during Q3FY26, Care’s profitability has worsened year-on-year.

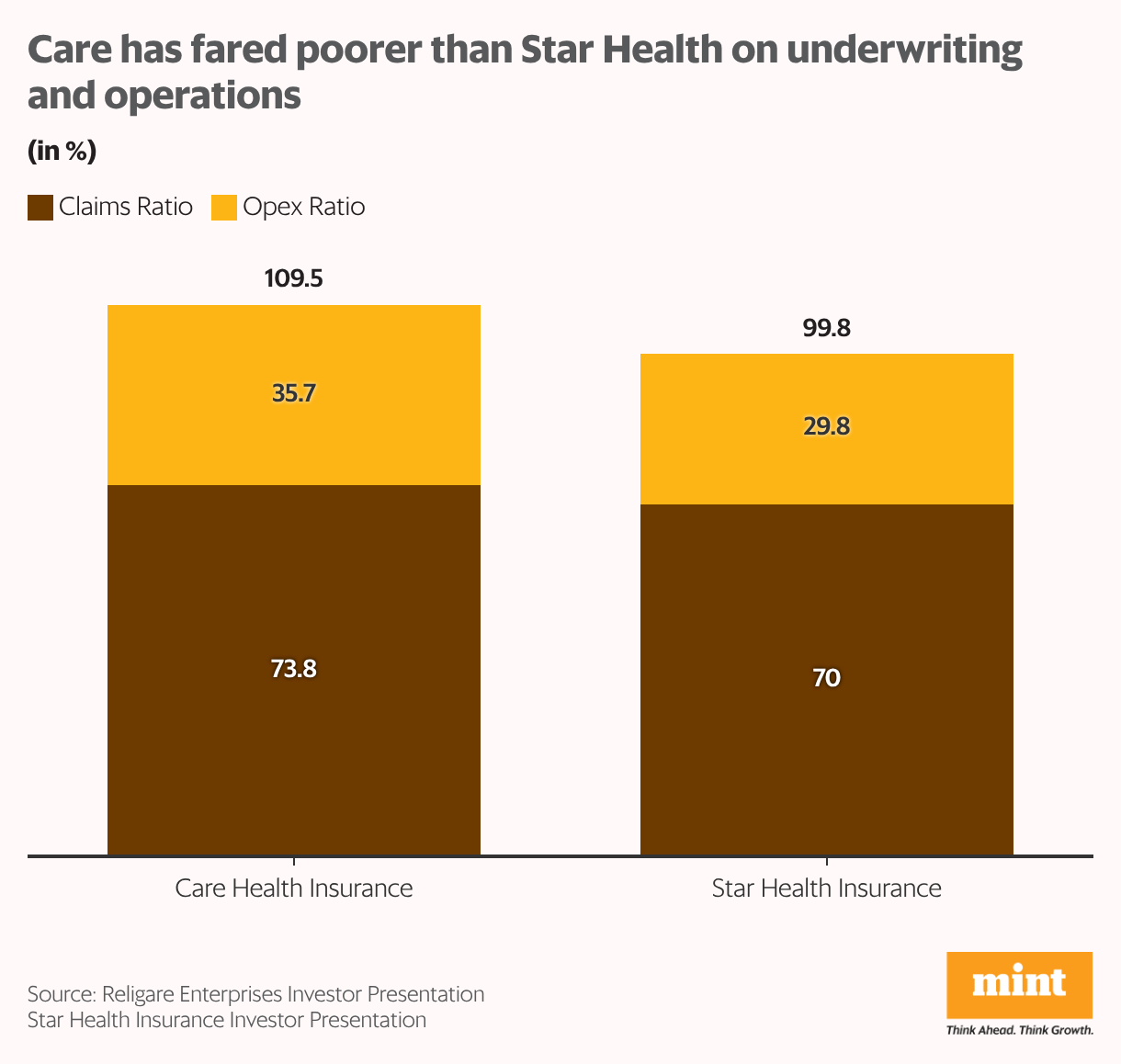

Sure, some of the poor fortunes can be chalked up to industry-wide stress, thanks to rising healthcare costs. With an increasing claims ratio, Care’s combined ratio has expanded from 105.2% in 9MFY25 to 109.6% in 9MFY26. Combined ratio refers to paid-out claims, related costs, and operating expenses as a percentage of earned premiums. Combined ratios over 100% indicate underwriting losses, and higher numbers point to bigger losses.

But comparison with larger peer, Star Health, points to company-specific issues at Care. Star’s Claims Ratio – paid-out claims as a percentage of premiums collected – has improved from 71.2% to 70.0%, while that of Care has worsened significantly from 66.7% to 73.8% between 9MFY25 and 9MFY26. Care’s opex ratio at 35.7% is also markedly higher than Star’s 29.8%, indicating that Care has lagged behind due to its poorer underwriting practices and operational inefficiency partly attributable to its smaller scale.

Regulatory issues at Care

Going forward, the regulatory crackdown on the agency channel can weigh on Care, given that half of its distribution channel comprises agents. The broker channel contributes another 32%, and could be at risk if the commission-structure overhaul planned for September 2026 rocks the boat too much.

Its solvency ratio at 1.7x is another red flag as it lingers precariously close to the regulatory minimum of 1.5x, warranting fund infusion by the parent. But fund infusion alone won’t be sufficient to sustain sentiment if governance issues persist.

The insurance regulator had issued warnings and slapped a fine on Care last year for claim settlement lapses. This indicates that good governance and protection of policyholders’ interests have not yet made it into the insurer’s corporate culture.

The worst may be over for RFL

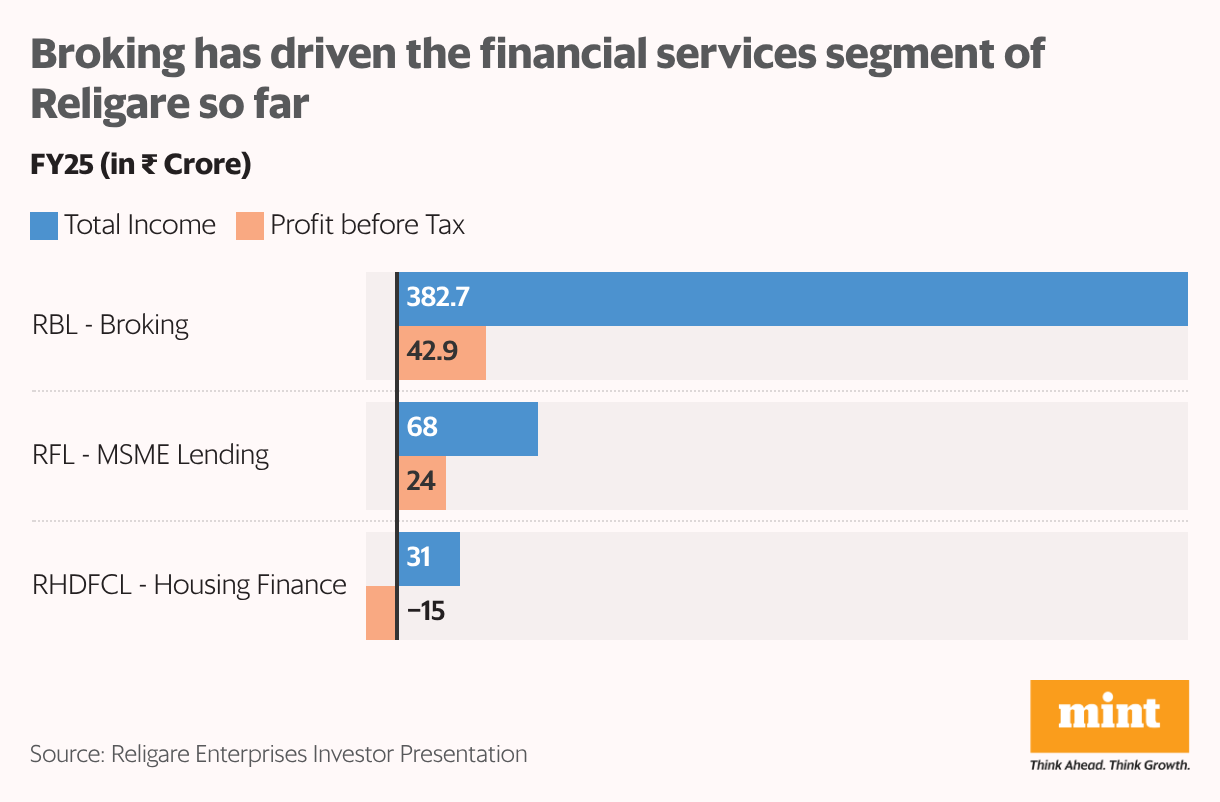

Following the demerger, the broking and lending businesses of Religare will sit under RFL. Based on FY25 numbers, broking is likely to be the key segment under RFL, at least to start with.

On the back of the sustained rise in retail investor participation following the pandemic, Religare Broking picked up the slack while RFL’s MSME lending was on pause under RBI’s CAP, and the housing finance arm struggled to post profits.

But derivative trading makes up more than 97% of the average daily turnover at Religare Broking. Following persistent regulatory curbs on F&O, this could take a hit. That said, RFL is likely to more than make up for the shortfall, now that past dues have been cleared, stressed MSME loans have been written off or provisioned for, and the “fraud” tag has been removed by banks.

RFL posted a 79% year-on-year growth in total income during Q3FY26 – the first full quarter after RBI’s CAP was lifted. But the high NPA of 4.7% and persistent losses in the housing finance segment can rain on the parade. Against the context of current underlying issues, Religare’s valuation at 2.55x P/B appears demanding. But if the successful execution of the demerger attracts strategic investors and results in material equity infusion, and confidence is restored in the group’s governance, it can prove to be a game-changer.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.