The implementation of the new labour codes posed a significant challenge this earnings season, forcing companies to increase provisions for employee benefits, which weighed on their bottom lines. This one-time hit slowed profit growth to low double digits, even as top line challenges persisted and the gap between headline growth figures narrowed.

How did the market, already grappling with the Union budget, the finalized India-EU free trade agreement, and ambiguous progress on US trade talks, react to these earnings pressures?

Since TCS kicked off the Q3 earnings cycle on 12 January, the market has navigated a volatile path, swinging from the ‘budget blues’ caused by the securities transaction tax (STT) hike on derivatives to optimism around a breakthrough in US-India trade negotiations.

Earnings drive result-day moves

Against this choppy backdrop, about 58% of companies with data available saw their stocks rise on result day following an expansion in their top and bottom lines. Most gains (84%) were steady at under 5%, but nearly a quarter of them saw more dramatic pops, with 14% gaining up to 10% and 9% posting double-digit gains. For the analysis, companies with a market capitalization over ₹1,000 crore were considered and their interim performance was based on a yearly comparison.

“Markets are increasingly being driven by earnings,” said Sachin Jasuja, head of equities and founding partner at Centricity WealthTech. “Companies delivering growth are generally rewarded, while those reporting weaker numbers face immediate pressure. ” He added that reactions tend to intensify when both revenue and profit decline together, marking a shift from previous years, when liquidity and sentiment often led rallies.

However, the headline profit numbers were not uniform. VK Vijayakumar, chief investment strategist at Geojit Investments, pointed out that reported net profit growth varied depending on whether the numbers were adjusted for exceptional items. “One study has reported 14.7% growth in net profit year-on-year after adjusting for exceptional items. This is the best in eight quarters and shows resilience,” he said.

At the same time, he cautioned, much of the earnings growth has been driven by a handful of sectors such as banking, financials, oil refining and metals, suggesting a narrow recovery.

Short-lived gains

Even stocks that rallied on result day have found it hard to sustain these gains. Only a little over a quarter of these stocks maintained their momentum and closed in the green the following day and have shrugged off the broader market volatility since then, Mint’s analysis showed.

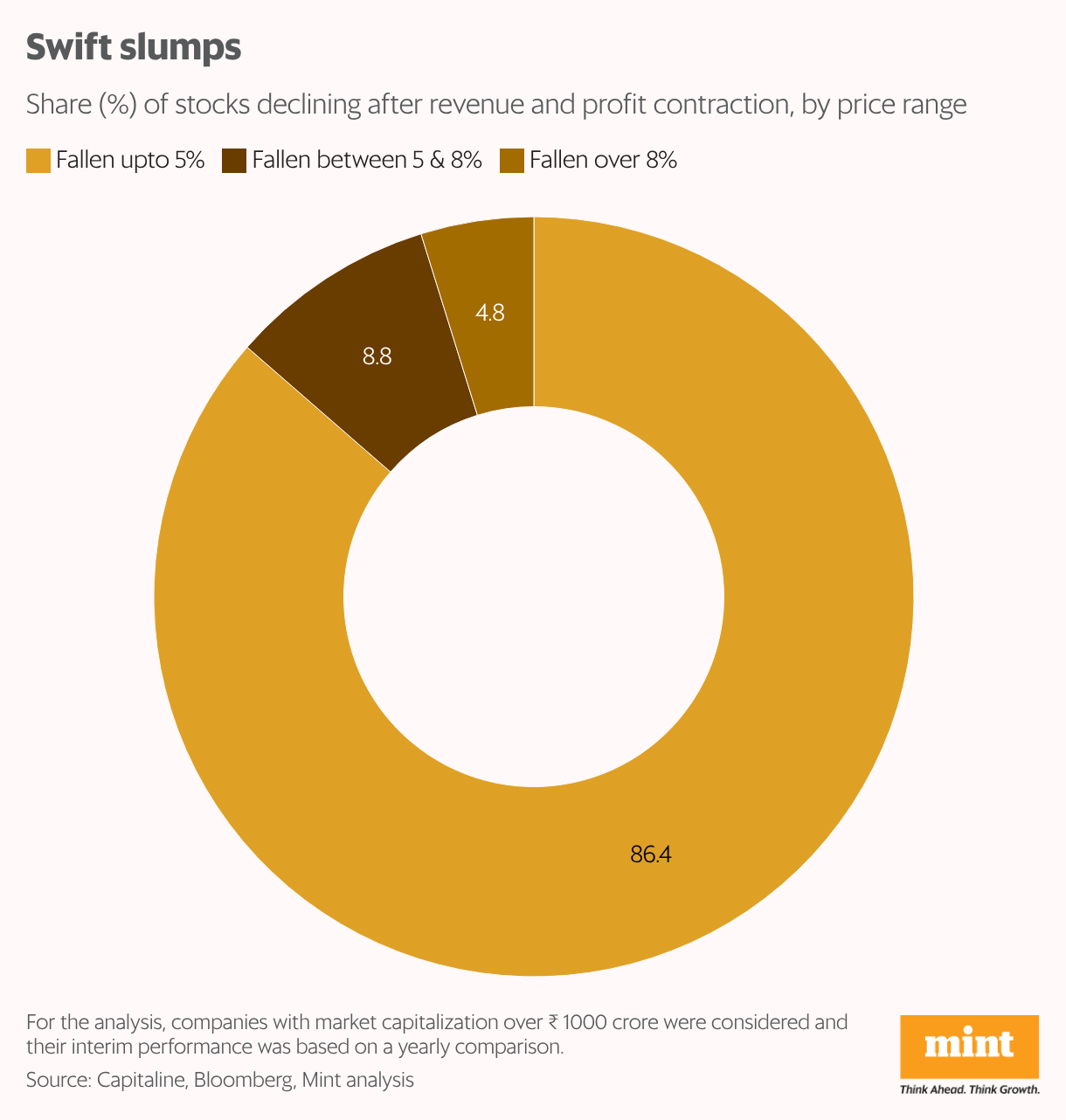

Poor financial performance was also punished quickly. Among the companies with shrinking top and bottom lines, about 61% slumped on their result days. But most of these hits were contained, with 86% falling less than 5% and only 14% shedding more than 5%. Notably, this downward pressure persisted for many. Of the stocks that fell on result day, 53.6% continued to slide the following day and have remained in negative territory since then.

Top line takes priority

Market experts said companies’ focus on the top line is a direct result of the current economic climate, particularly in consumption-driven sectors. “Demand is surely the biggest driver of revenues,” said Ashwin Patil, head of fundamental research at LKP Securities. “In the quarter gone by, several consumption sectors such as autos, FMCG, and retail have reported strong topline growth, and we have seen the reaction to that in the stock price.”

The data corroborates these findings. For instance, Atul Auto, a leading three-wheeler manufacturer, saw its stock surge nearly 9% on result day after reporting a more than 20% year-on-year jump in both standalone revenue and profit for the December quarter. Similarly, Trent saw its stock rise 5% following an impressive performance, with top-line growth of 18% and a 36% expansion of its bottom line.

Patil said investors are increasingly able to look past one-time costs and margin pressures if the core business—revenue generation—is healthy. “The market was aware that the raw-material basket had gone up and there would be one-time labour code costs that would dampen the bottom line. Even after removing this impact, the bottom line grew slightly lower than expectations. Still, the stocks moved up.”

This suggests that in the current environment, a strong top line is viewed as a sign of pricing power and robust demand, which are more sustainable drivers of long-term value. Factors such as input costs are often seen as temporary or “already factored in”.