Domestic demand-driven sectors are expected to carry much of the weight in a quarter marred by external shocks, including US tariff threats, geopolitical tensions in West Asia, and heightened cross-border strain following the 22 April Pahalgam terror attack and India’s subsequent Operation Sindoor in May, which targeted terrorist camps in Pakistan and Pakistan-occupied Kashmir.

“Rate sensitive sectors like banks, NBFCs (non-banking financial companies), select auto [companies] and realty are likely to benefit,” said VK Vijayakumar, chief investment strategist at Geojit Investments. “Aviation, telecom and hotels will continue to do well, while IT will remain a drag on earnings.”

Jay Kothari, lead market strategist at DSP Mutual Fund, finds oil marketing companies (OMCs) and gas distributors tactically attractive. “Lower energy costs should improve [OMCs’] marketing margins in Q1, while export-linked sectors like IT, pharma and textiles may face near-term earnings headwinds,” he said.

Even so, analysts expect gains to remain concentrated in pockets, with some sectors continuing to lag and rich valuations limiting market-wide upside.

Earnings growth faces structural constraints

India’s post-pandemic bull run has yet to coalesce around a defining macro theme. Unlike the capex-led cycle of the 2000s or the consumption surge of the 2010s, recent gains have been driven more by margin expansion than robust demand growth.

“I’m cautiously optimistic that the earnings cycle has sort of bottomed out and we could be looking at 12–14% [Nifty] earnings growth in FY26,” said Manish Jain, head of fund management at Centrum Broking. “But I don’t expect any dramatic changes in Q1 compared to Q4.”

In Q4FY25, corporate India’s earnings per share (EPS) rose 10-12%, but full-year earnings growth came in below 5%. Moreover, earnings downgrades continued to outpace upgrades, indicating that analysts are tempering their expectations heading into the new fiscal year.

A recent report from Nuvama Institutional Equities notes that the margin expansion story may be nearing its limits. Corporate restructuring has largely run its course, and premiumization trends are beginning to normalize across sectors.

This has led India Inc.’s profit growth to slow and align more closely with revenue growth, which remained sluggish in FY25. In fact, India’s revenue growth has trailed other emerging markets (EMs) post-Covid, averaging below 10% for eight consecutive quarters, according to Nuvama.

As India’s earnings differential narrows with other EMs, the risk of foreign institutional outflows increases, the report warned.

Despite this, the market still expects mid-teens EPS growth over the next two years, forecasting continued expansion in both margins and topline. If these expectations aren’t met, the gap between actual and projected earnings could lead to more sustained earnings downgrades, according to the report.

Domestic consumption: A swing factor

While India’s economy has demonstrated resilience to external shocks in recent quarters, high-frequency indicators suggest that a secular pickup in consumption remains out of reach.

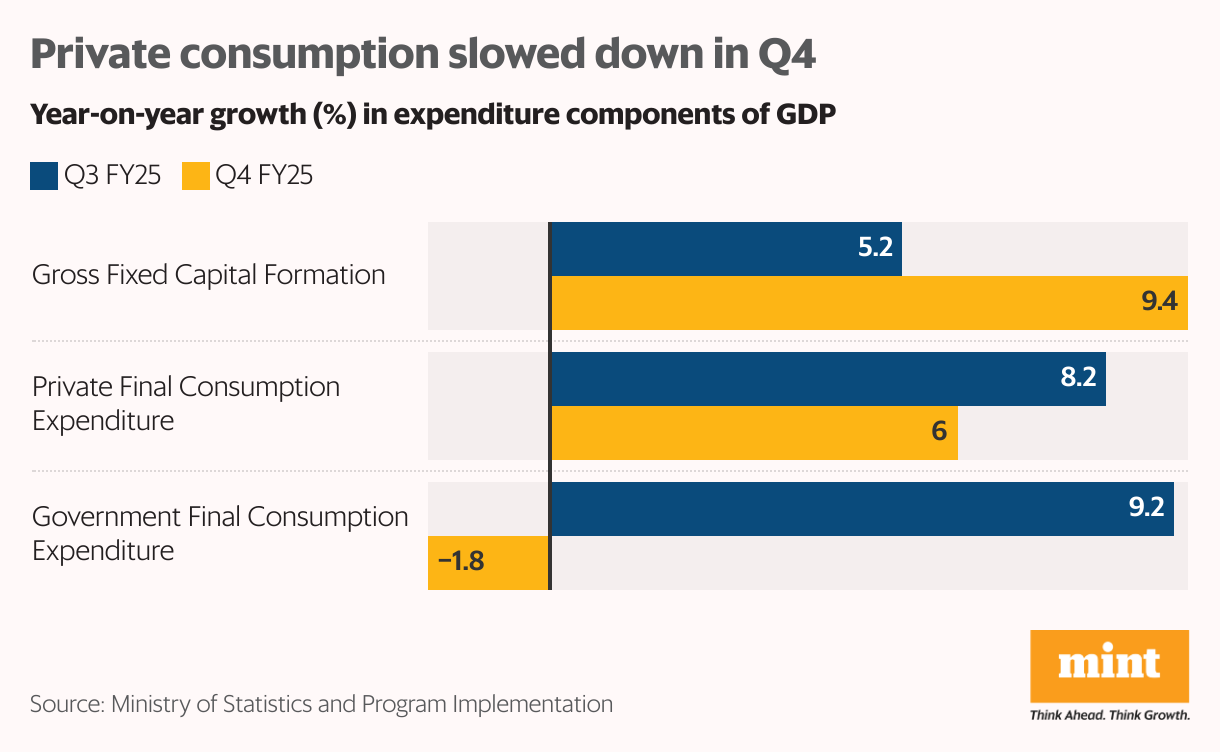

Economists expect GDP growth to moderate to 6.5% in Q1FY26, down from 7.4% in Q4 FY25. That jump in Q4 was partly supported by a sharp 41% on-year drop in government subsidy payouts, which helped lift the headline GDP. Gross value added (GVA), a cleaner measure of underlying activity, rose 6.8%, revealing weaker momentum.

Private consumption, which made up 56.5% of GDP in FY25 according to CMIE data, continued to lag. Urban demand remains inconsistent, with household consumption slowing in Q4 from Q3. Much of the hope for a broader uptick now rests on rural demand.

Radhika Rao, senior economist and executive director at DBS Bank, noted that falling inflation should improve household finances and support private consumption in the coming quarters. Rural households are likely to benefit more from better crop yields due to a timely monsoon, she said.

“Following a strong Q4 our proxy gauge for rural demand has held up into April as well. Volume growth appears stronger in non-food categories,” Rao added.

Manish Jain of Centrum Broking expects consumer durables, NBFCs, and select auto companies to benefit from the rural recovery theme.

Debopam Chaudhuri, chief economist at Piramal Group, also sees signs of revival in budget-focused segments. “I remain optimistic about a broader demand revival as the 2025 festive season approaches,” he said.

Valuations leave little room for error

Even as near-term demand trends show improvement, markets are pricing in a strong recovery. Yet, sector leadership has remained fluid, with most themes—from manufacturing to consumption to digital, having already enjoyed their spotlight post-Covid.

According to Nuvama, five-year compound annual growth rates for all sectors now range between 10–30%, leaving little that looks fundamentally cheap.

“I don’t think the flavour of the market is going to change a whole lot from what we have seen in the last five years,” said Jain. “One has to be very sharp and nimble to keep pace with the sector rotations in large caps. With small and mid-caps, it is always a growth-driven bottom-up approach.”