Indian stock markets wrapped up the week largely flat as investors parsed the first batch of December-quarter earnings, finding no clear cues to take fresh positions in the week ahead.

The Nifty 50 closed the week at 25,693.85 and the BSE Sensex at 83,556.87, as global volatility eroded investor confidence and triggered profit booking, capping gains through the week.

Sentiment got a mild boost after the commerce secretary on 15 January said the first tranche of the India–US trade deal was nearing finalisation. Separately, easing US–Iran tensions after reports said Washington assured Tehran of no imminent strikes helped soothe investor nerves.

Still, buying stayed selective in heavyweights, while broader sentiment remained cautious, experts said. Metals topped the charts with nearly 5% weekly gains, trailed by IT at 2.7%. Sentiment in tech was boosted by Infosys, which jumped 5.6% on Friday after its better-than-expected results and an upward revision to its full-year revenue guidance.

Banks also rose around 2% as mid-cap lenders delivered better-than-expected Q3 prints with improving asset quality and margins. On the flip side, capital goods, consumer durables and realty remained under pressure, keeping the broader market locked in a narrow range.

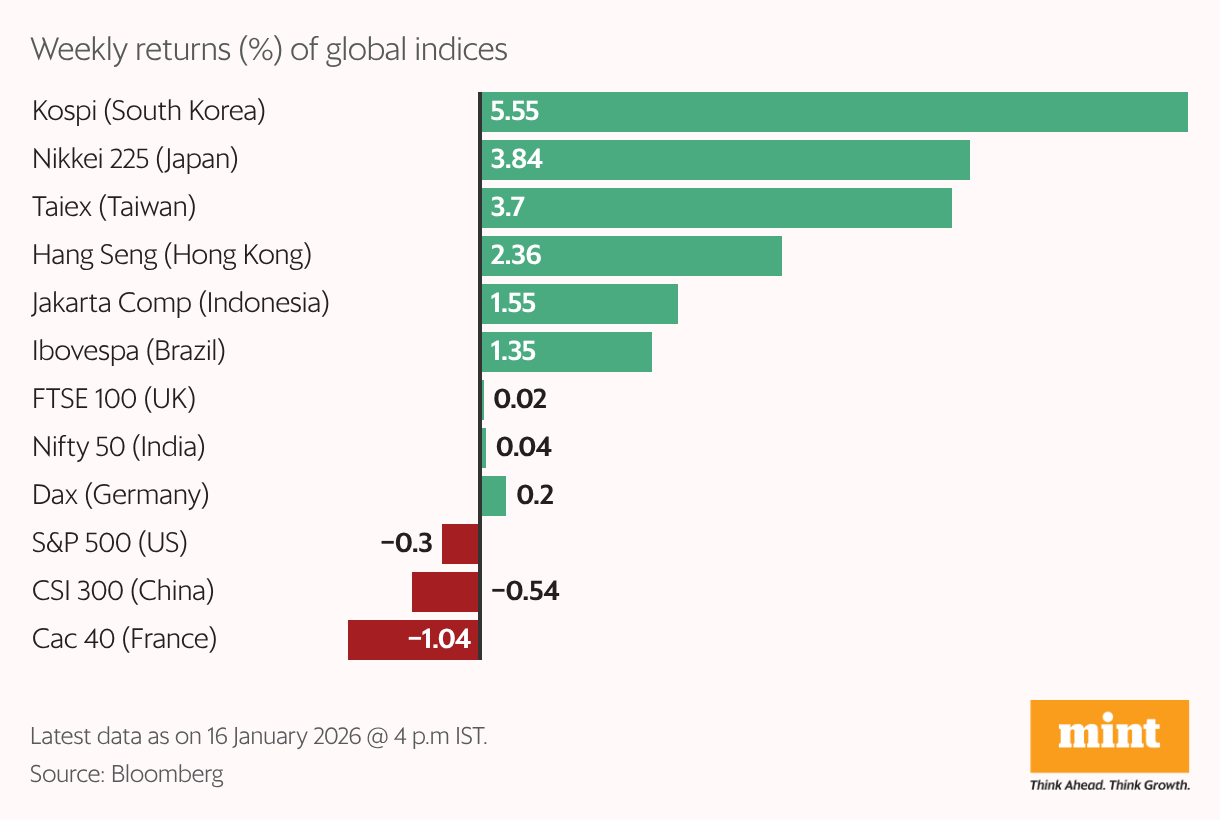

The cautious tone in domestic markets is also due to the gap between India and its emerging-market peers in foreign investment. South Korea and Taiwan emerged as top gainers, drawing foreign flows for a third straight week.

South Korea and Taiwan sit at the centre of the artificial intelligence hardware and semiconductor value chain, benefiting from sustained earnings upgrades and solid order books, said Robin Arya, smallcase manager and founder at GoalFi, a Sebi-registered corporate research analysis firm. India lags due to foreign investor outflows and lingering earnings doubts, compounded by its limited AI-linked exposure, he added.

Market outlook

Analysts expect market sentiment to remain fragile and see a further downside, flagging that Q3 earnings may not yet mark a broad-based upcycle.

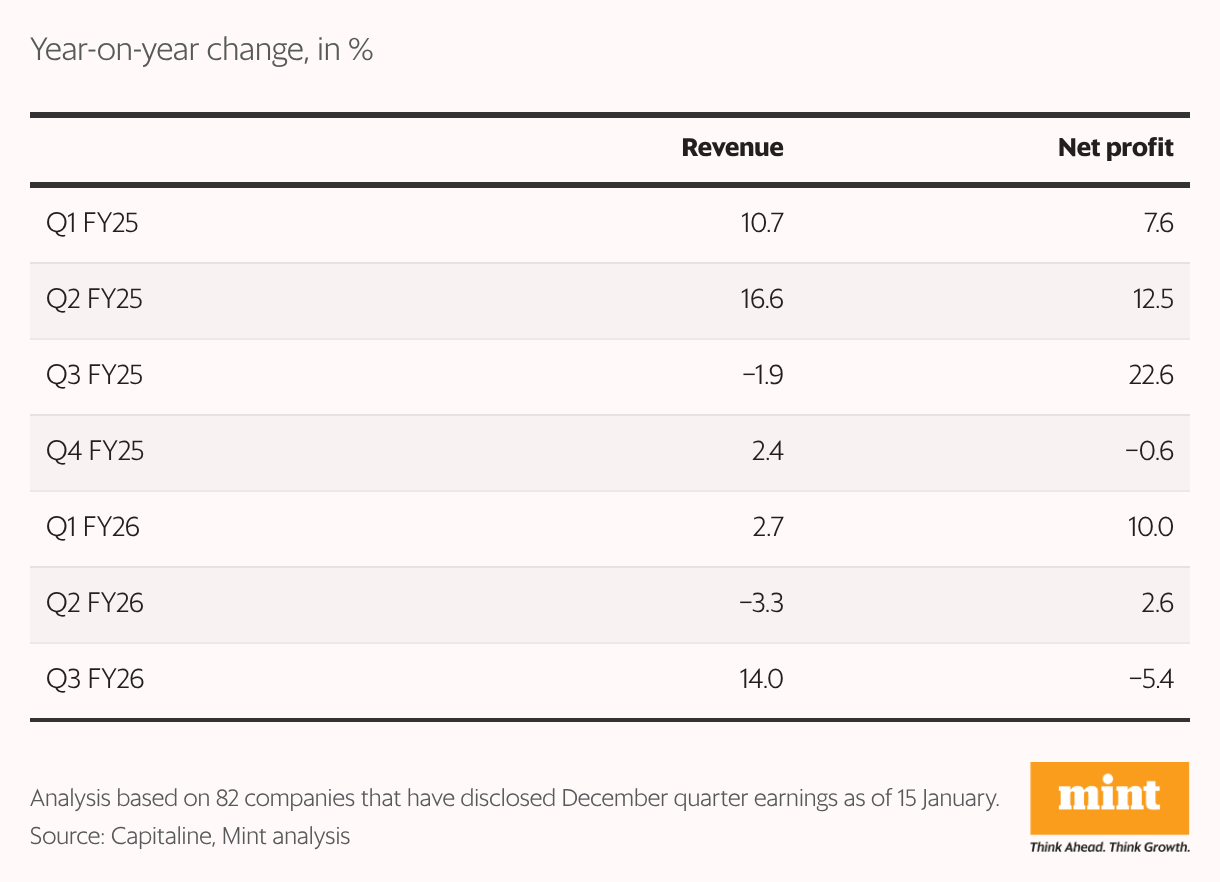

As the December quarter results kicked in this week, a Mint analysis of 82 companies (that declared their Q3 results so far) showed a 5.4% year-on-year drop in combined profits–a seven-quarter low. In contrast, revenue growth hit a five-quarter high of 14%, albeit on a low base.

Analysts expect stock-specific moves to dominate the market going ahead, as seen in Groww and State Bank of India this week. Both stocks outperformed the broader market over the past month, with Groww gaining 8% and SBI 4% this week.

Groww’s rally has been supported by a ₹580 crore investment from State Street Global Advisors in its asset management business, stronger-than-expected Q3 numbers and bullish brokerage views, despite heightened volatility since its listing two months ago.

However, Arya cautioned that the earnings of capital market-linked stocks will stay cyclical, moving in line with market volumes and sentiment. Valuations are expensive across the board, making stock selection and earnings visibility crucial, he added.

SBI, meanwhile, has emerged as a core compounder amongst investors rather than a tactical trade, noted Arya. Investors have confidence in its asset-quality improvements, stable margins, solid balance-sheet metrics and consistent profitability, he said. As a result, the stock hit a 52-week high this week.

Markets are expected to remain range-bound in the coming week, with Q3 results and trade-deal progress driving stock-specific action, while geopolitical tensions remain a key overhang.