For Indian information technology, the June quarter began on a dull note. At the onset, serious concerns emerged around the trade tariff-led impact on the US economy—a crucial market for the Indian IT sector. However, as the quarter progressed, the intensity of tariff uncertainties reduced to some extent. Still, the latest commentary from the Accenture management and various brokerages indicates that the demand scenario has not improved or worsened. While this is comforting for edgy IT investors, expectations about the upcoming results of an otherwise strong Q1 quarter are low.

Q1FY26 revenue growth is likely to be modest and uneven. The divergence between tier-1 and tier-2 IT companies would persist. HDFC Securities has pencilled in sequential constant currency (CC) growth in the range of -2.8% to +1.5% for tier-1 and -3.4% to +3.7% for mid-tier companies. Among large-caps, Infosys Ltd and LTIMindtree Ltd would lead growth. Wipro Ltd, HCL Technologies Ltd, Tech Mahindra Ltd and Tata Consultancy Services Ltd are likely to report a drop, hit by seasonality and client-specific challenges. That said, US revenue growth for most IT companies would be supported by favourable foreign exchange movements.

Within verticals, the banking financial services and insurance (BFSI) sector is seen as resilient to tariff woes and thus, continuing its growth momentum. Hi-tech, energy and utilities would support growth for select IT companies. However, the manufacturing, automotive and retail/consumer packaged goods segments would be under pressure.

Deal wins are expected to be steady, led by cost takeout and vendor consolidation projects. Revenue growth could be supported by the ramp-up of previously won deals, but since clients are in wait-and-watch mode, the uptick in discretionary IT expenditure is unlikely. Also, deal closures could be slow due to clients’ elongated decision-making cycles. So, as seen lately, despite a robust deal pipeline, actual revenue conversion in Q1FY26 may lag.

Margins range-bound

“Deal wins for the quarter should be decent. That said, total contract value (TCV) alone may not be a sufficient parameter to gauge growth, as vendor consolidation is a zero-sum game. Players’ outlook, therefore, will likely reflect the impact of losses/leakages in the existing book,” said JM Financial Institutional Securities report dated 30 June.

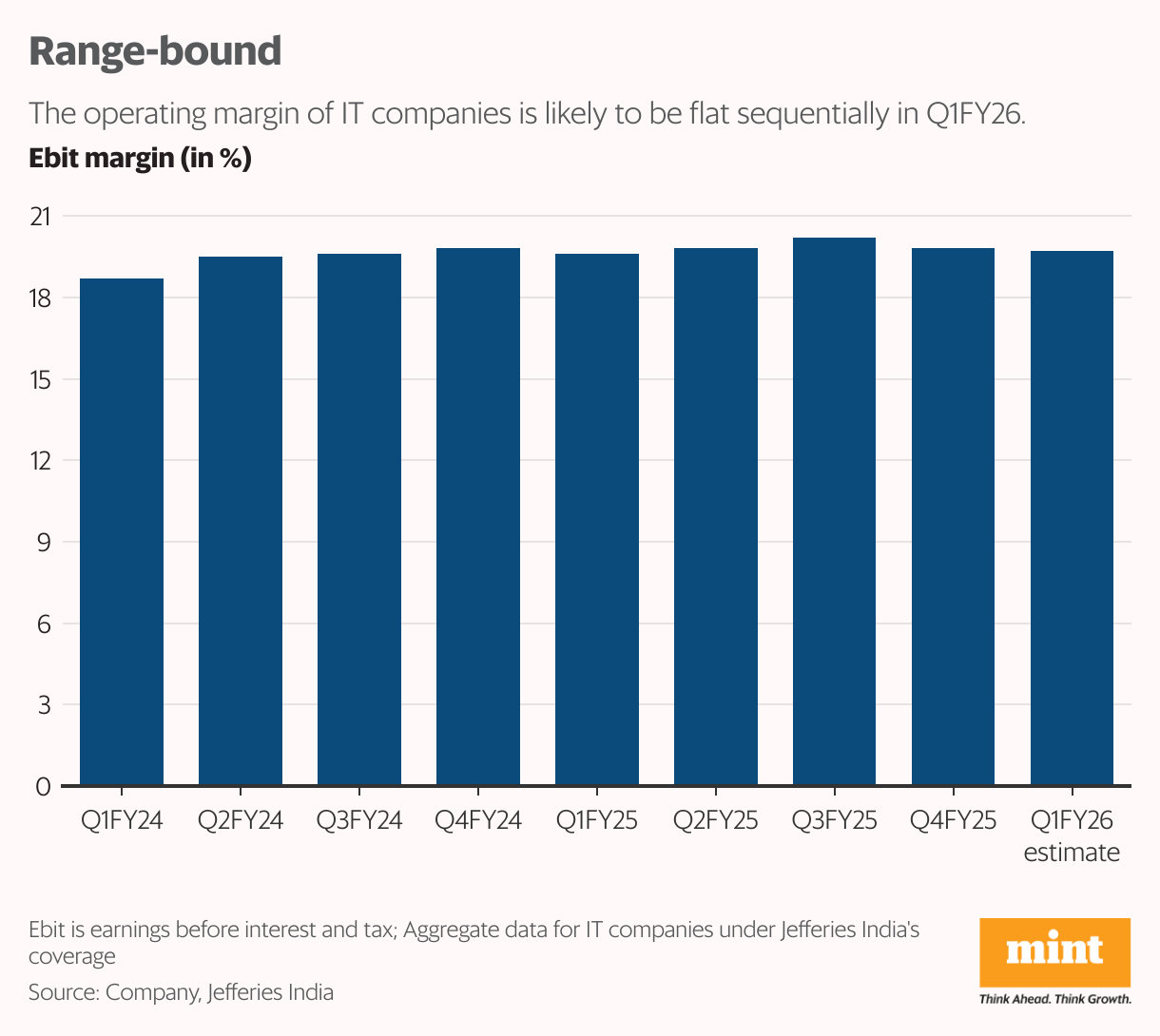

Now, in the absence of any meaningful revenue growth and dollar-rupee appreciation, margins should remain range-bound. This is despite the deferment of FY26 wage hikes by most IT companies. The movement in operating margin would also be a function of company-specific factors. For IT companies under its coverage, Jefferies India expects aggregate margins to remain flat at 19.8% in Q1FY26. “INR appreciation against USD should impact margins for most IT firms, however, firms with a higher share of Europe exposure may see a lower impact since most key European currencies have appreciated vs. INR,” it said in a report dated 30 June.

Among the other crucial monitorables is whether Infosys, HCL, and Wipro (quarterly guidance) are revising their FY26 and Q2FY26 revenue growth targets. Infosys’ FY26 current growth guidance is 0-3%, and HCL’s is 2-5%. Jefferies’ analysts would also be watching out for demand commentary given the worsening US macro and the potential impact of AI.

As things stand, the Nifty IT index has staged a smart recovery, rising around 20% from its 52-week low of 32,517 seen in April. The index is trading at a one-year forward price-to-earnings multiple of 24 times, according to Bloomberg data. A premium to the long-term average of 20 times. “While the worst case has not panned out, the environment remains uncertain,” according to the JM report. Given this, valuations appear expensive and hardly compelling unless the sector’s earnings downgrade cycle bottoms out.