Kotak Mahindra Bank, another large private sector bank, meanwhile, recorded a 14% growth in advances for FY25, compared to the 18% growth seen in FY24, reflecting a cautious approach. Kotak did not provide any forward guidance for FY25.

The slowdown in credit growth isn’t surprising, but it’s becoming more visible. Banks are lending, just a bit more carefully. With FY25 behind us, the tone for FY26 looks measured, not aggressive.

So, what’s behind the credit slowdown, and how is FY26 shaping up? Let’s take a closer look.

The credit slowdown is not limited to just two banks–it reflects an industry-wide trend.

According to the Reserve Bank of India, the banking sector’s credit growth almost halved to 11% in FY25, from a high 20% growth reported last year.

Factors contributing to this trend

First, the higher base effect played a role—FY24 saw sharp 20% credit growth, driven primarily by unsecured lending, including personal loans.

Second, the sector’s credit-to-deposit ratio surged past 75% (the optimal level), as credit growth outpaced deposit mobilisation. This imbalance prompted caution among banks, leading them to focus more on deposit growth while deliberately slowing down lending activities.

Third, NBFCs, which had borrowed aggressively in recent years, saw their bank borrowings rise to 22.6% in FY24, up from 21.7% in FY23 and 19.8% in FY21.

Adding to the concern, stress was building on their books due to rising non-performing assets, prompting the RBI to raise the risk weights on bank lending to NBFCs by 25 percentage points in November 2023. This move effectively increased the cost of lending for banks.

These factors together contributed to a broader deceleration in credit growth across the banking system.

However, as the increased risk weights had slowed down lending activity, the RBI rolled them back in February 2025. This decision came after NBFC borrowings from banks fell to just 17% in Q2FY25, as highlighted in the December 2024 Financial Stability Report.

Meanwhile, HDFC Bank’s total advances increased by about 5.4% in FY25. Axis Bank reported 8% growth, while ICICI Bank stood out with 13.3% growth in total advances, matching system-wide growth and outpacing peers.

Also Read: Canara Bank CEO expects corporate loan growth to pick up in second half of FY26

SBI missed credit guidance

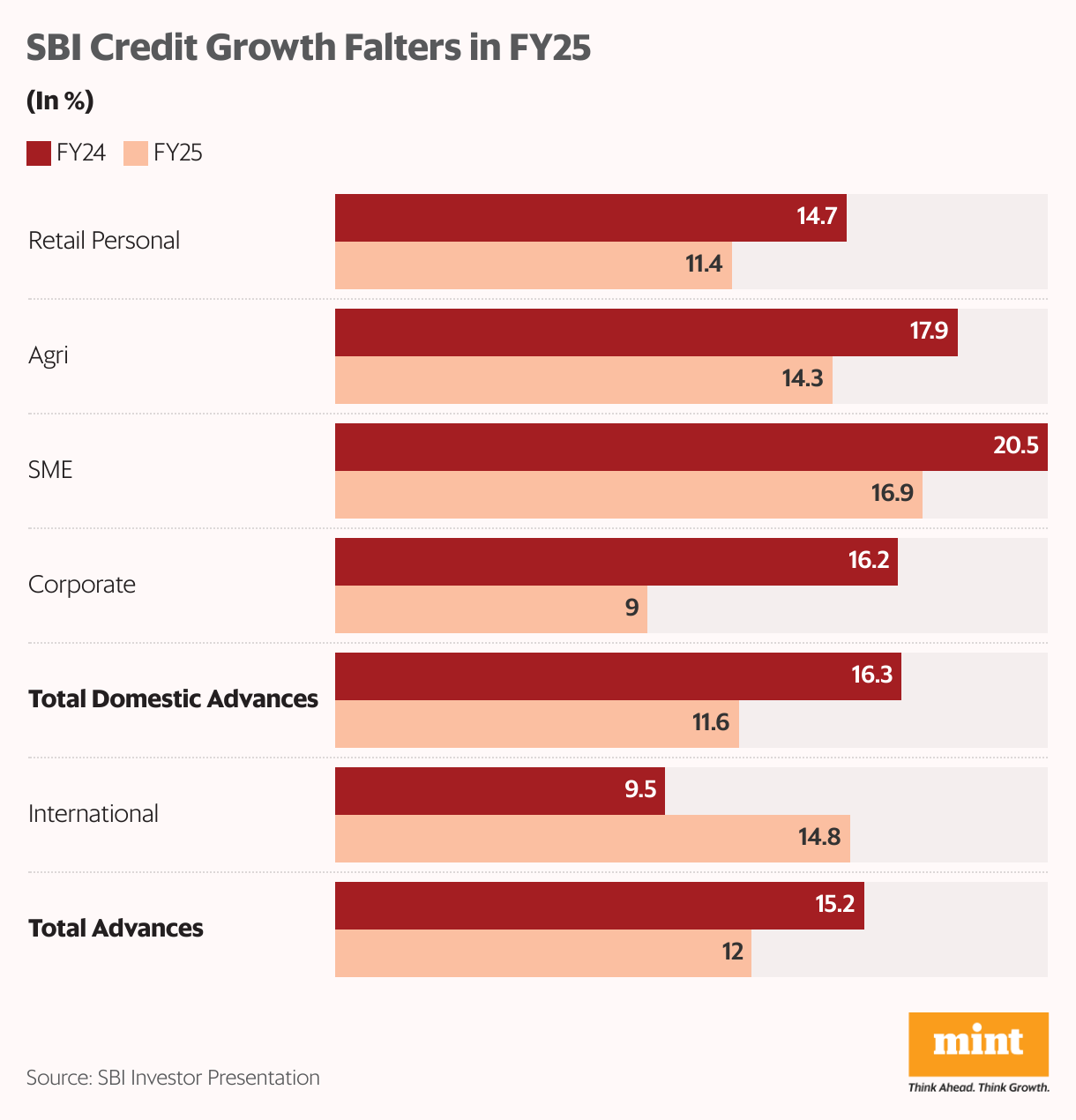

SBI total bank advances increased by 12% in FY25 to ₹42 trillion, lower than 15% growth in FY24. With this, the bank also missed its revised guidance of 14%, which was revised downward from a 14-16% range guided in Q2FY25.

In FY24, the bank clocked 16.3% growth in domestic and 9.5% growth in international advances. Domestic growth was broad-based, aided by a heated economy.

However, liquidity remained tight for the sector as the economy lost momentum in FY25, driven by subdued government spending and deliberate credit tightening. SBI’s total advances rose just 12% (in FY25), lower than the 15% in the previous year. While international lending picked up, growing 14.8%, domestic credit growth slowed to 11.6%.

Unlike last year, the slowdown was more visible across retail, agri, SME, and especially corporate lending. Retail personal lending grew by just 11.4%, agri by 14.3%, and SME by 16.9%—each moderating from FY24 levels. The corporate loan book, however, was the biggest drag, growing just 9%, down from 16.2% in FY24.

According to the management, an unexpected slowdown in the corporate segment and unusually high prepayments from the public sector undertaking led to slower credit growth. Large companies used equity proceeds to repay debt and deleverage. The bank cited NTPC’s ₹10,000 public issue as an example.

Also Read: Treasury gains save SBI’s day, but couldn’t avert earnings downgrades

SBI’s credit growth ahead

Looking ahead, the bank expects a recovery in corporate credit demand, supported by a robust pipeline of ₹3.4 trillion, of which 50% is already sanctioned. This is expected to be driven by rising demand from the lower-income salaried segment.

Additionally, SBI added 6.5 lakh new corporate salary accounts, which is expected to aid growth further. The bank expects demand revival in infrastructure, renewable, data centres, and commercial real estate to support credit growth.

The bank expects credit growth of 12-13% in FY26, similar to FY25 and in line with system expectations. Motilal Oswal expects industry credit growth to remain modest at 12% in FY26.

On the financial front, the bank’s net interest income (NII) increased by a muted 4.4% to ₹1.67 trillion, while the NII margin contracted by 19 basis points to 3.09%. To this end, there remains a risk of further margin contraction if the RBI cuts rates. However, SBI sees limited pressure due to a higher share of MCLR-linked loans.

Net profit increased strongly by 16% to ₹70,901 crores, driven by a 4 percentage point improvement in the cost-to-income ratio to 51.6%. Asset quality also remained strong.

Credit growth for Kotak

Much like SBI, Kotak also saw muted loan growth across segments. Net advances in FY25 rose by just 14%, lower than 18% in FY24, and below analyst expectations.

This was despite acquiring Standard Chartered’s personal loan portfolio of ₹3,330 crore in January 2025. The bank did not provide any forward guidance for FY25, possibly due to the RBI’s restrictions on onboarding new customers in April 2024.

Even so, Kotak recorded the highest loan growth among the top five banks, outperforming both ICICI and SBI.

That said, the moderation in growth was visible across most key segments. Consumer loan growth slowed to 17%, down from 20% in FY24. A sharp decline in unsecured lending–credit card loans fell by 7%, after rising 44% last year–weighed on retail lending. Notably, the RBI’s 10-month ban on new credit card issuance, which was lifted in February 2025, dragged the performance.

Commercial loans grew just 6%, compared to 20% in FY24. Kotak also scaled back its exposure to retail micro-credit–a segment seeing rising stress, leading to a 33% decline, versus 60% growth last fiscal.

Like SBI, Kotak corporate credit growth fell to 6%, compared to 21%. However, SME lending surprised on the upside, growing 31%, against 18% in FY24.

Looking ahead, Kotak expects loan growth to rebound, supported by a recovery in unsecured lending and credit card issuance. Despite modest growth in FY25, Kotak remains optimistic about accelerating loan growth to 1.5- 2x nominal GDP. This is expected to be driven by a rebound in consumer lending and unsecured credit.

With the ban lifted, the bank expects credit card issuance to recover, aided by new product launches. Kotak aims to push unsecured loan growth into the mid-teens and will sharpen its focus on retail and SME lending.

On the financial front, Kotak’s net interest income increased 9% from last year to ₹28,342 crore in FY25, while net interest margin fell 36 basis points to 4.96%. Its cost-to-income ratio declined by 2.63 percentage points to 43.4%. However, despite that, net profit remained flat at ₹13,720 crores, due to sharp 87% jump in provisions.

Also Read: Are banks hiding weak asset quality with higher loan write-offs?

SBI trades at discount to peers, Kotak in line

From a valuation perspective, SBI trades at a price-to-book (PB) multiple of 1.4, a slight premium to its 10-year median of 1.2. Kotak, on the other hand, trades at 2.6x PB, about a 40% discount to its 10-year median of 4.2x.

SBI trades at a deep discount to HDFC Bank (2.9), ICICI Bank (3.3), Axis Bank (1.9), and even Kotak Mahindra Bank.

Kotak’s discount to ICICI Bank is justified, given ICICI’s outperformance—not just over Kotak, but across the broader banking sector.

Though the current elevated credit cycle has peaked, with rising credit costs and non-performing assets across the sector, stress in the loan books of larger banks like SBI and Kotak has remained relatively muted.

The higher cost-to-deposit ratio, which had been a drag on loan growth, also shows the first signs of reversal. With tax cuts, credit demand is expected to pick up in FY26, though at a more gradual pace, and it may take time to return to the peak levels seen in FY24. However, rising geopolitical tensions and economic slowdown could be a drag.

For more such analyses, read Profit Pulse.

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specialises in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.