Close on the heels of industry-beating growth, recent reports of back-to-back strategic acquisitions promise to further cement Marico’s leadership.

The stock has gained 4.5% since the announcement of the acquisition of 4700BC on 26 January. But risks can limit earnings upgrades. Let’s discuss.

Acquisition heft lifts sentiment

The FMCG major has completed three acquisitions in three weeks. It acquired gourmet snacking brand 4700BC on 26 January, functional wellness brand Cosmix on 4 February, and Vietnam’s skin-care brand Candid on 9 February.

Over 93% stake in 4700BC of Zea Maize was acquired from PVR Inox, through which 4700BC commands a deep consumer connect.

Cosmix, in which Marico has acquired a 60% stake, tops the list of bestselling plant-based proteins across e-commerce and quick-commerce platforms. Marico’s 75% stake-acquisition in Skinetiq gives it access to Candid as well as exclusive distribution rights for Murad in Vietnam.

On top of proven capabilities, the acquired brands stand to benefit from Marico’s R&D capabilities, supply-chain efficiencies, presence across ecommerce channels, and general trade distribution network.

By FY30, Zea Maize is expected to triple from its current annual revenue run rate of ₹140 crore (based on the October-December quarter). The acquisitions are cumulatively expected to grow into 5% of Marico’s consolidated business during the period.

Capitalizing on industry tailwinds

The near-term demand outlook for the industry appears promising, buoyed by rural demand, which has sustained on mellow inflation and healthy monsoons, while urban demand has received a booster shot from GST 2.0. Demand has also received a leg up from the accelerated adoption of e-commerce and quick commerce.

Margins also stand to expand as raw-material prices trend lower. Copra prices have declined 30% off their peak, helping Marico’s gross margin expand sequentially from 42.6% to 43.5%. While the company recognized a ₹6 crore hit to profitability from the new labour codes, raw-material prices are expected to remain benign, thus supporting margins.

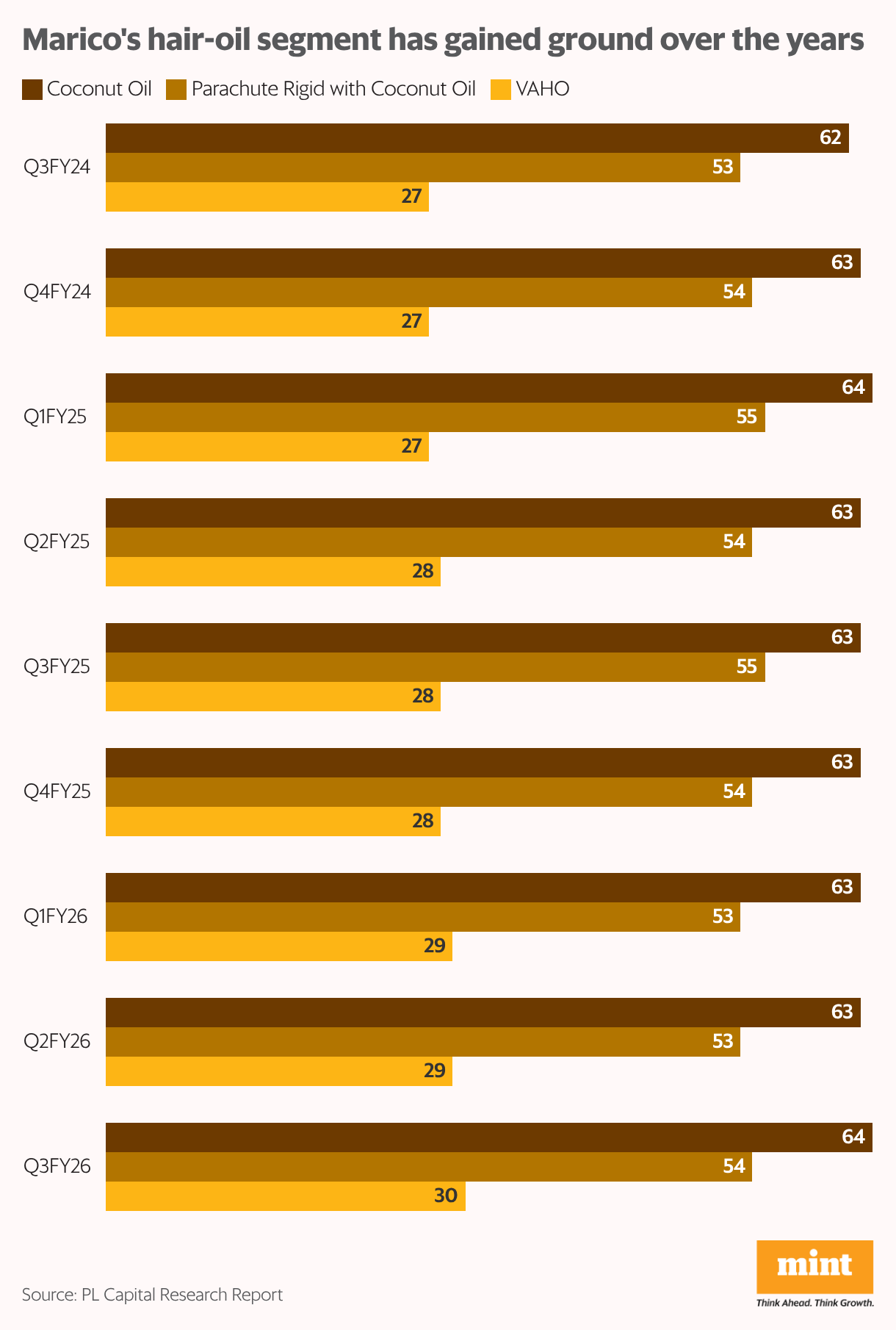

Against these bright industry prospects, Marico has been gaining ground on competitors, thanks to a favourable product mix tilted towards high-margin value-added hair oils (VAHO).

Despite intense competition in the amla segment, which the company has held back on, VAHO saw 29% value growth in Q3FY26, taking cumulative gains in its market share to 3 percentage points.

Marico’s coconut oil segment, through brands like Parachute and VAHO, has gained ground over the years. The management is expected to double down on premiumization going forward.

Global winds cut both ways

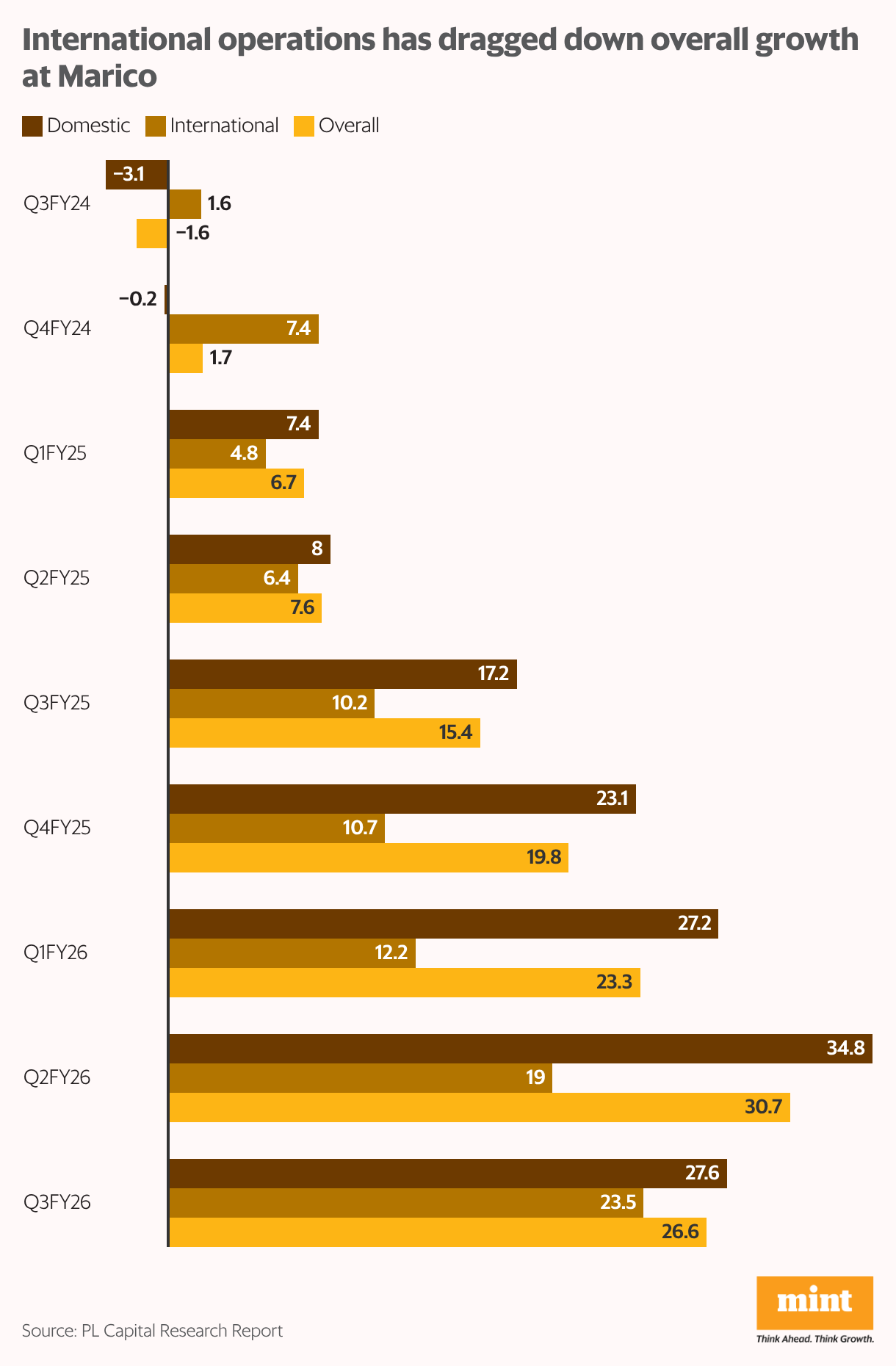

Marico has a significant global presence, with 25% of its revenues coming from international operations through globally recognized brands like Parachute, HairCode, Caivil, and Hercules. Its key international markets, Bangladesh and Southeast Asia, contribute almost three-quarters of international revenues and have picked up pace over the years. This can be attributed to steady core business and scale-up of new segments in Bangladesh, even as hopes of a recovery rise in Vietnam.

This has more than made up for the slowdown in the Middle East and Africa. While the Gulf region and Egypt have clocked robust growth, the Middle East and North Africa have seen growth cut in half from 35% to 17% between Q3FY25 and Q3FY26. Overall, global growth has lagged domestic growth, making domestic operations the primary growth engine for Marico.

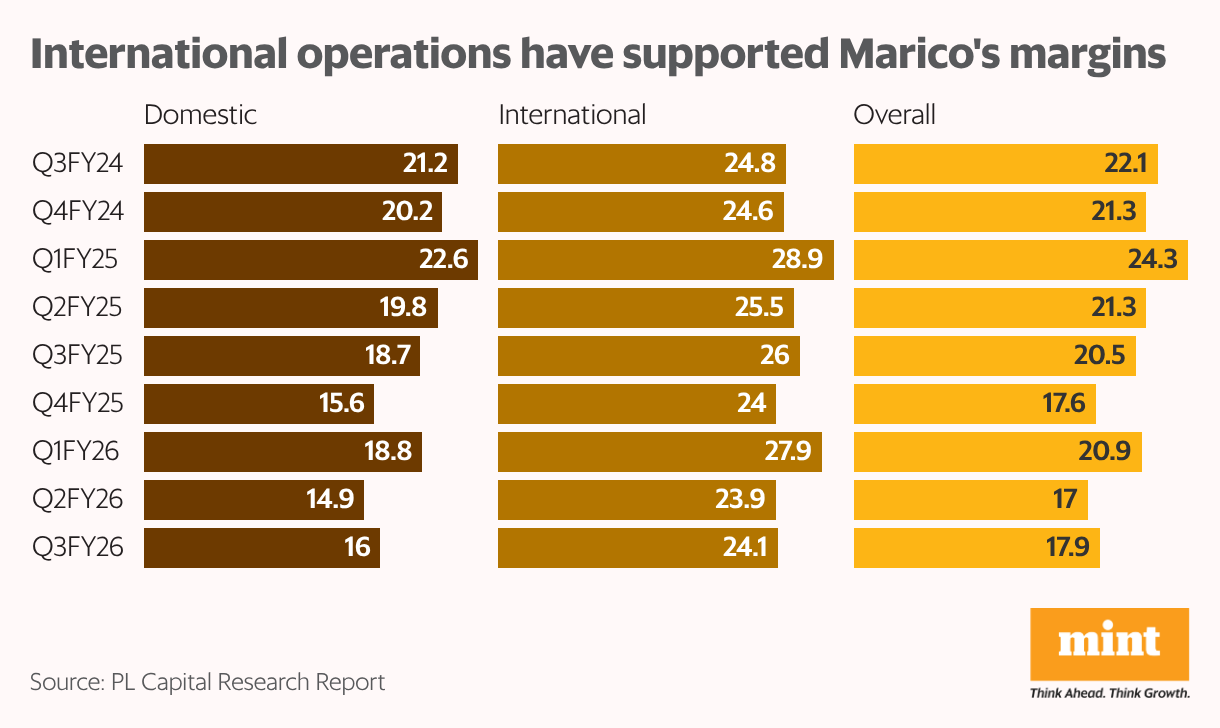

That said, margins have received a consistent push from the high-margin international operations.

While domestic Ebit margins have compressed from 21% to 16% over the last couple of years on rising competition, international margins have held their ground at about 24%, arresting the fall in overall Ebit margins. Ebit is earnings before interest and taxes.

Growth outlook promising

The management is upbeat on near-term demand prospects and recovery in global markets. The company’s project Setu can push the pedal on growth in general trade through strategic expansion of its distribution network. The company also hopes to position itself on the correct side of the emerging health wave with new health-focused product launches and brand-building campaigns like the AI-powered “Heart-to-Heart Talk.”

Notwithstanding the temporary trade-channel disruption in Q2FY26 ahead of the implementation of the new GST rates, volume growth has picked up pace in recent quarters, coinciding with a turn in sentiment in the stock.

The management is expected to push persistent premiumization to drive even faster sales growth. With pricing intervention, the management hopes to beat the industry with double-digit sales growth in FY26. The continued traction in non-amla VAHO franchise speaks to the sustained momentum in premium formats.

Margin expansion on the horizon

Premiumization achieved through growing focus on brands like Beardo, Just Herbs, and Plix, is also expected to bode well for margins, which have seen year-on-year compression due to a sharp 84% year-on-year acceleration in the prices of copra, along with increases in other raw-material prices.

The medium-term outlook on margins is promising. Despite calibrated price increases, smaller packs, and cost-optimization, Marico’s margins have taken a hit in recent quarters, falling from over 20% in Q3FY25 to less than 18% in Q3FY26. But copra and rice-bran oil have moderated sequentially in the December quarter, and are expected to remain benign.

Furthermore, supported by 4-5x growth in its foods and premium personal care businesses, Marico expects 250 bps margin expansion in FY27. As operating leverage kicks in with scale in the foods segment, and premiumization in personal care improves profitability, Ebitda margins in these segments are targeted in the mid-teens by FY30. Ebitda is earnings before interest, taxes, depreciation, and amortisation.

Risks linger

While robust value-performance, particularly with pricing intervention in hair oils, has supported sales growth, volume growth has been lacking. Parachute, for instance, reported the fourth consecutive quarter of volume decline during Q3FY26, as the company continued to prioritize margin protection amid raw material price increases.

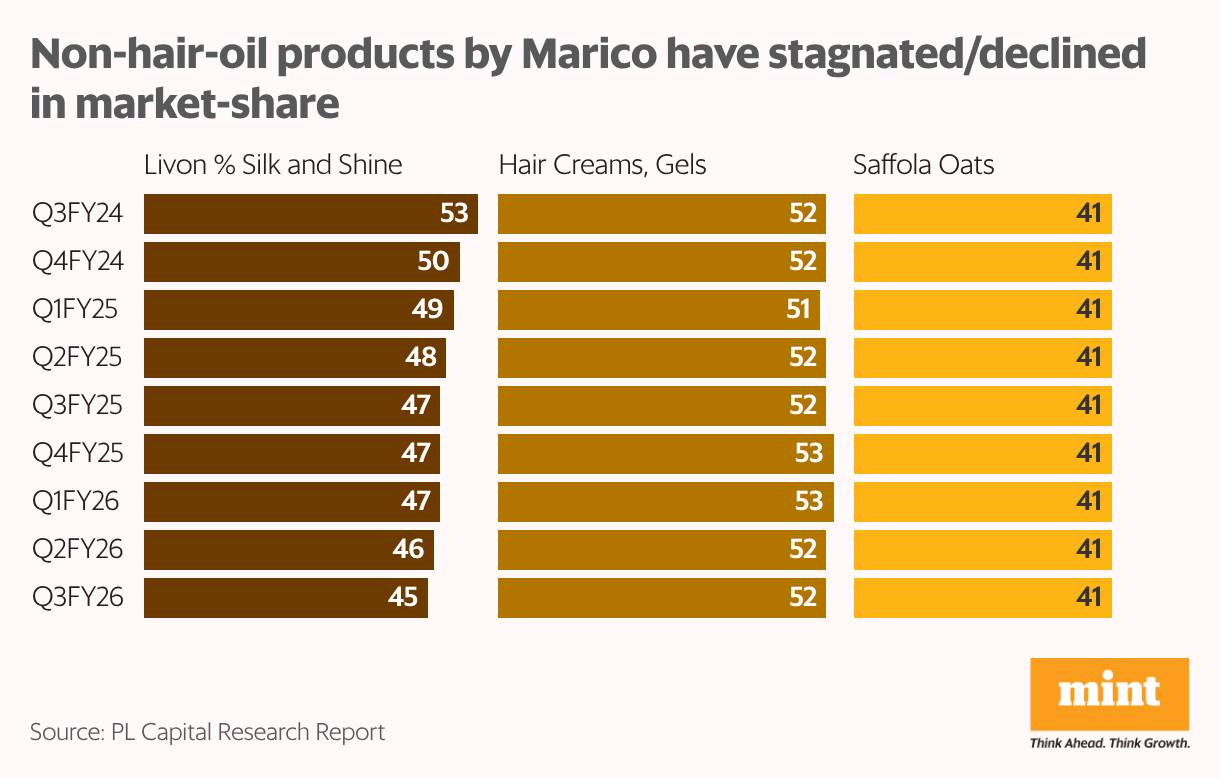

Marico has also been stagnating or losing ground in other segments. Livon and Silk and Shine has gone from being market leaders with dominant 53% share in Q3FY24 to 45% in Q3FY26. Hair creams and gels, as well as Saffola Oats, have also seen market share stagnate at 52% and 41% respectively, leaving them at the mercy of industry growth.

While Marico continues to remain the market leader in coconut oils, Parachute Rigids, Saffola Oats, VAHO, post-wash leave-on serums, and hair gels, waxes, and creams, competition has continued to heat up in the space. Rising marketing expenditure amid competition can weigh on margins going forward.

While acquisitions pave the way for growth in foods and premium personal care, execution will be key. Successful integration and profitable scale-up of previous acquisitions raise hopes.

Beardo delivered double-digit profit margins, innovation and expanded digital distribution have ensured robust momentum in plant-based nutraceuticals under the Plix brand, and True Elements has meaningfully expanded its product range. But the stock appears priced to perfection at 47 times FY27 earnings, based on PL Capital’s estimates, leaving little room for misses.

For more such pieces, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.