The Nifty IT index has corrected nearly 8% since 19 September, following the hike in H1-B visa fees by the US. Each such visa will now cost companies an additional $100,000. With 24,000 visa applications approved for the top five Indian IT firms in the first half of FY24 alone, the financial impact quickly adds up.

That said, tier-1 IT stocks have held up relatively better, and companies have also found reasonable success with offshoring. Wider margins and deeper pockets have enabled larger firms to scale up US-based hiring, subcontracting, and delivery centres.

As a result, while shares of Persistent Systems Ltd, Mphasis Ltd, and Coforge Ltd have fallen 10-14%, Infosys Ltd and HCL Technologies Ltd have slipped less than 6%. Some mid-cap IT companies have also shown resilience. A case in point is LTIMindtree Ltd, which is down only 6.4%.

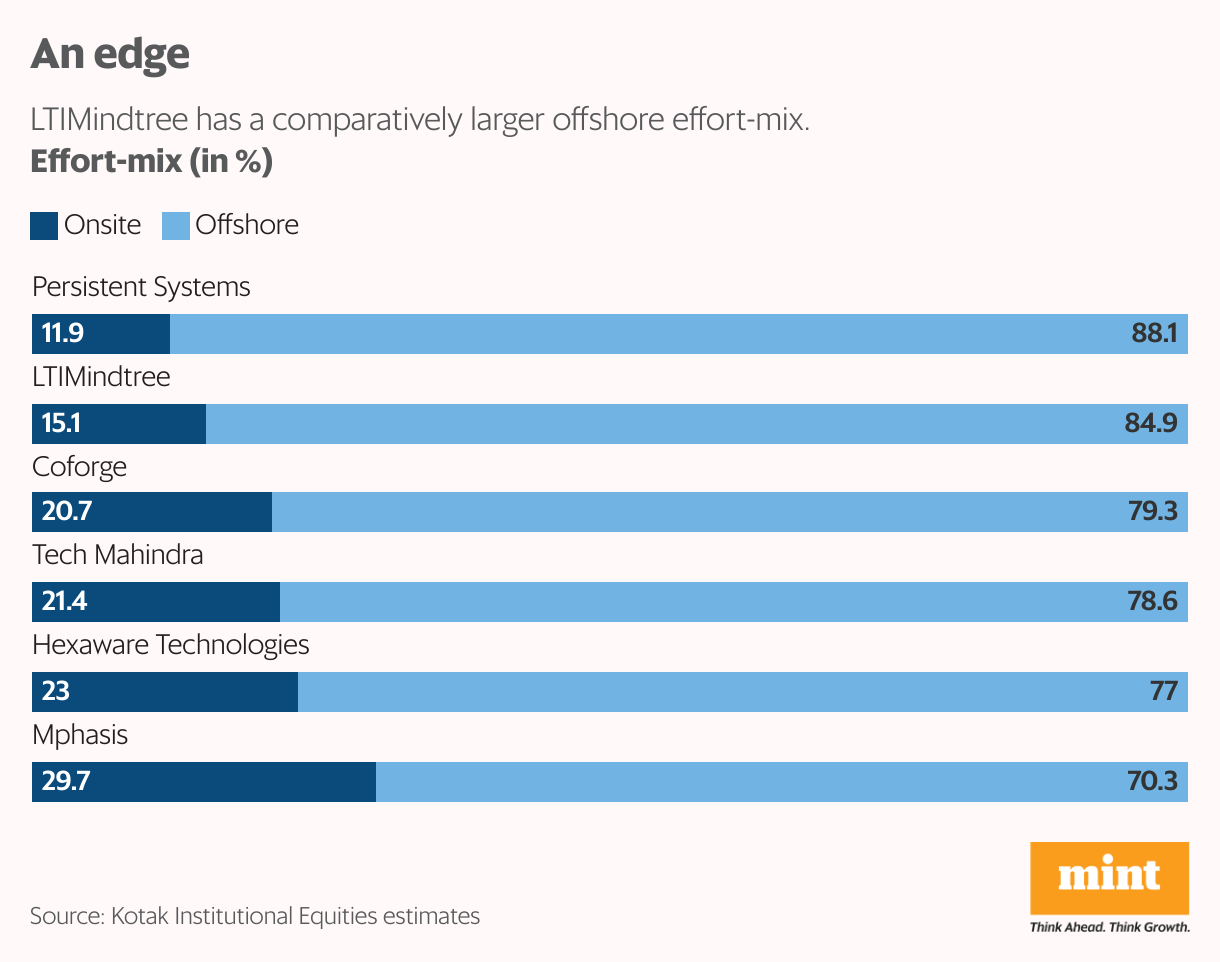

While Persistent Systems has been weighed down by its pricey P/E at 50.5x, LTIMindtree’s relatively reasonable valuation has offered comfort. Another reason investors are giving LTIMindtree some leeway is its smaller onsite revenue share. Against a 20-30% onsite effort-mix for most mid-cap IT firms, this number for LTIMindtree is only about 15%. Effort-mix refers to the proportion of person-hours spent onsite versus offshore.

Automation, artificial intelligence (AI)-led benefits, a client-led push to save costs, and diversified client exposure underpin this advantage. LTIMindtree’s top 10 clients contribute only about a third of its revenues.

Under pressure

Still, the company derives almost 75% of its revenues from the US and this poses a big risk amid the heightened policy uncertainty in the region currently. This is significantly higher than the 50% number reported by the industry on average, and leaves LTIMindtree particularly vulnerable to growth pangs at a time when US firms are tightening their IT spending.

This also takes its H-1B visa dependence to 35%—among the highest in the industry—despite low onsite effort-mix.

To add to its troubles, the company depends on discretionary IT spending by clients for 60-65% of its revenues. Despite 37% exposure to BFSI, which has posted good growth in IT spending in recent quarters, LTIMindtree’s revenue grew at a moderate 7.6% in the June quarter (Q1FY26). This can be blamed on the 4.2% growth reported in its key region, the US. Europe and the rest of the world saw 7-10% growth.

As such, excluding the tailwind from rupee depreciation, LTIMindtree’s overall growth is even lower at 4.4% year-on-year in constant-currency terms.

Even as the company has managed to control attrition at 14.4%, its direct costs have increased 9.6% year-on-year in Q1FY26, a factor driving Ebit margin down to 14.3% from 15.0%. Net profit margin expansion can largely be attributed to higher forex gains, and isn’t a reflection of core business profitability.

Unfortunately for investors, the string of management exits has continued this year. The president resigned in January, the COO in March, and the CEO in May, followed by a bunch of senior leadership exits. The exodus has revived concerns that cultural-mismatch led overhang from the 2022 merger of LTI Infotech and Mindtree may still be weighing on LTIMindtree’s performance.

The stock is trading 25% below its 52-week high of ₹6,767.95, and at 32x its trailing earnings, a discount compared to other mid-tier IT firms. But for the stock to sustainably pull out of its rangebound behaviour seen since 2021, quite a few pieces will need to fall into place.