The offer includes a fresh issue of shares worth ₹2,500 crore and a ₹1,000 crore offer for sale by its New York-based promoter Brookfield Asset Management, according to the company’s red herring prospectus. Investors can subscribe to shares of Schloss Bangalore, the sole owner of the Leela brand, at ₹413– ₹435 apiece during 26–28 May.

The IPO also serves as a litmus test for sentiment in a sluggish primary market, especially with heavyweights like the National Stock Exchange still await clearance to list.

Read this | Leela to retain its ‘niche, complete luxury’ hotel identity even after IPO: CEO

Still, subdued investor sentiment has resulted in a more rational valuation for Leela’s stock, despite recent fierce returns from rivals, said Taher Badshah, CIO at Invesco Asset Management (India).

“Leela may not necessarily offer immediate listing day gains. But it is definitely providing a cheap entry into the luxury segment which is expected to grow faster than the broader hospitality sector, especially in terms of value,” Badshah said.

Demand for premium experiences is driving a strong upcycle in the hotel industry, bolstering margins and profitability across luxury operators, according to industry experts. With high average room rates and strong brand positioning, luxury hotels are well-placed to sustain bottomline growth, something increasingly rare in India Inc.

Leela currently operates 13 hotels, with average room rates (ARR) and revenue per available room (RevPAR) of ₹22,545 and ₹15,306, respectively, for FY25, about 1.4x the luxury segment average in India. It also boasts the highest Ebitda margin in the industry at nearly 50%, one of its key strengths, at least on paper.

Chink in the armour

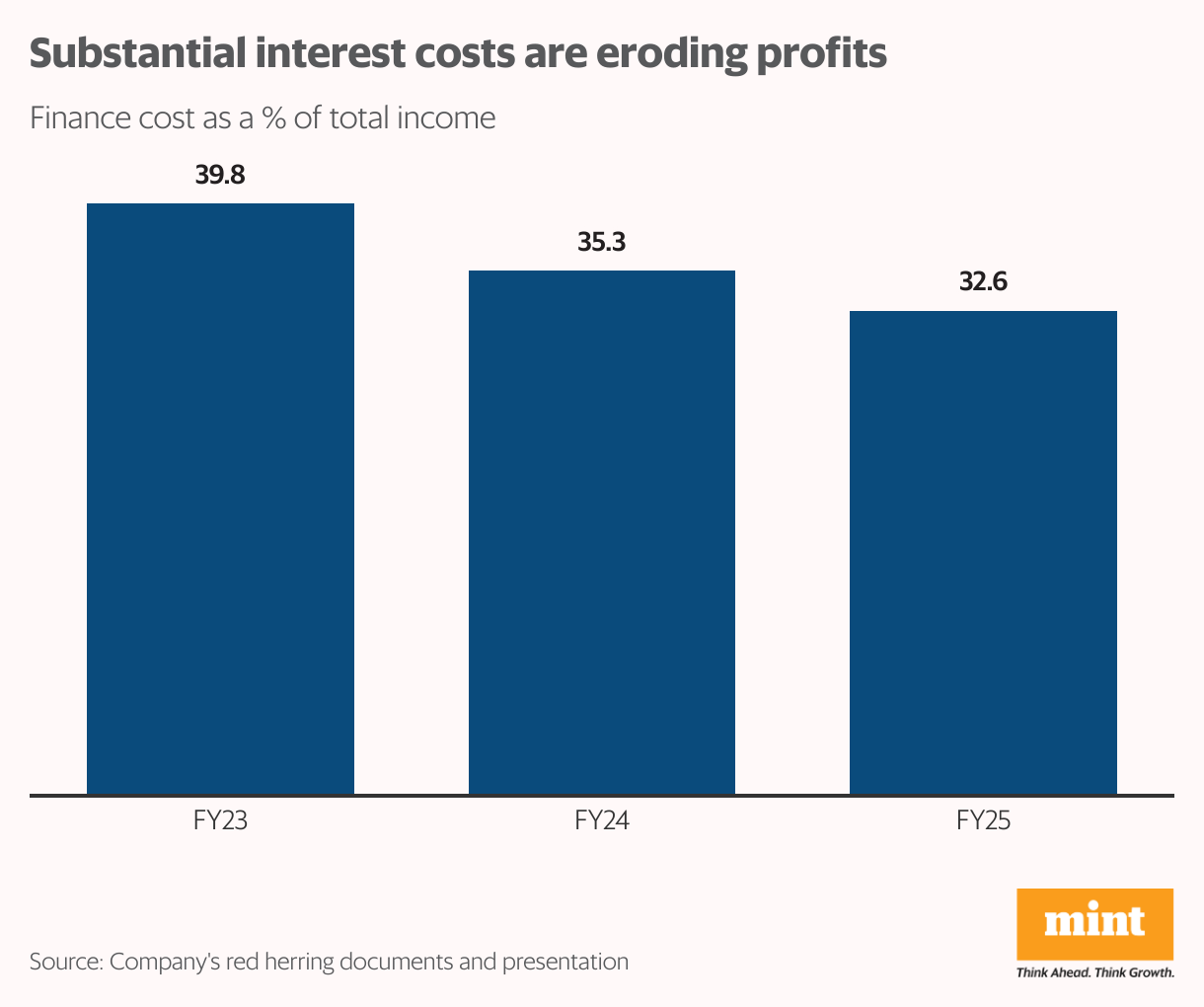

However, the company’s crushing net debt of ₹2,567 crore eats into most of its profits through interest payments. Despite its high operating profitability, Leela has posted losses until FY24 and is set to deliver the lowest net margin, at 3.4% among peers in FY25, per its prospectus.

Much of the IPO proceeds of ₹2,300 crore will go towards debt repayment. That raises key questions: Will Leela have enough free cash flow to fund its capital expenditure plans? How will it strike a balance between growth and deleveraging?

Read this | Travel startups and indulgent Indians: A match made over dream destinations and luxury escapades

“Post IPO, the company’s net debt will be close to zero. This means there will be ample liquidity available through internal accruals to finance future capex,” Ankur Gupta, managing partner and head of Asia Pacific and Middle East at Brookfield Asset Management told Mint.

“Even at the project level, we can borrow for construction and then pay it down with accruals from that property over a period of time. A combination of minimal debt and internal accruals should be sufficient for the current pipeline,” he said.

Leela plans to add 678 rooms across seven new hotels by 2028. Some will be owned and operated by Schloss Bangalore, while others will follow a management-contract model. The expansion includes palace-style hotels in Agra and Srinagar, wildlife resorts in Ranthambore and Bandhavgarh, a Hyderabad hotel, and serviced apartments near Mumbai airport.

Still, analysts caution that rivals have more aggressive expansion plans to tap into India’s growing demand for luxury hotels, potentially limiting its market share gains.

In FY24, Leela’s average occupancy rate stood at 63%, well behind Indian Hotels Company’s 77%, underscoring the intensity of competition. Experts attribute this gap to stronger brand recall enjoyed by rivals like Taj and Oberoi. Leela’s smaller, less diversified portfolio also makes it more vulnerable to seasonal swings in tourism demand, they noted.

Since most of Leela’s new properties won’t be operational until 2028, the company also risks missing out on capitalising fully on the current luxury upcycle.

Also read | Where are Indians travelling in 2025?

That may partly explain its lower valuation: Leela has been priced at 27 times enterprise value to Ebitda for FY25, compared to 30–34x for peers like Chalet Hotels and IHCL, according to a source managing the IPO.

Luxury tailwinds

Despite slower volume growth, Leela’s premium positioning could still deliver meaningful value growth.

Supply addition is typically slower in the luxury segment, so room rates might hold up better even during a downturn, as consumers are less sensitive to prices in this segment, said Invesco’s Badshah.

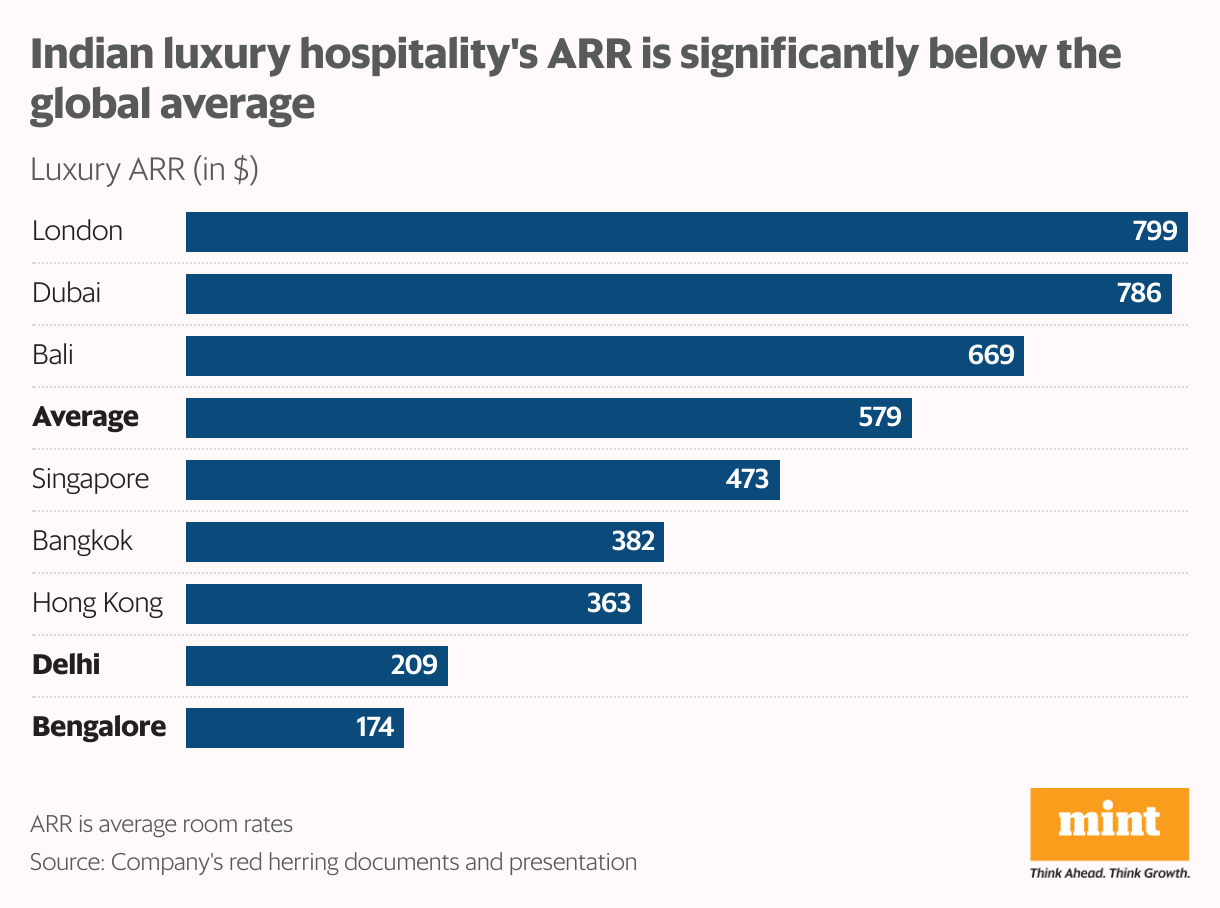

In fact, India’s luxury ARR at $175-200 is significantly lower than the global average of $579. Meanwhile Leela projects excess demand for luxury hotel rooms to result in an 8% compound annual growth rate for the industry’s ARR till FY28, according to the red herring prospectus.

This indicates a significant opportunity for value growth in the luxury segment given the current demand-supply mismatch expected to persist there.

Also read | JP Morgan’s Mookim seeks bright spots amid earnings lull in Indian markets

“Leela operates in and leads a niche segment which is somewhat immune to economic cycles. Now that it is somewhat cheaper, it can be a good long-term play,” Badshah said.