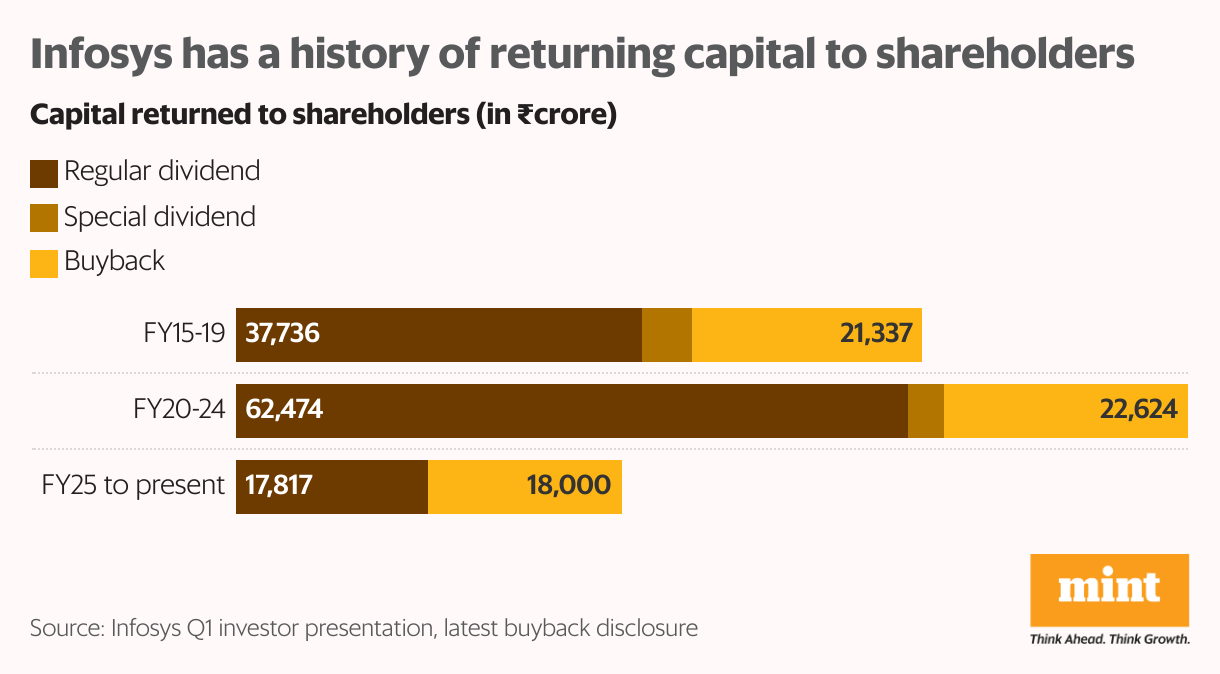

Companies use buybacks and dividends to reward shareholders. Historically, Infosys’s buybacks have been received positively, with the stock appreciating over the subsequent three to six months. The latest buyback has also lifted sentiment – Infosys stock has risen by almost 7% since the announcement on Monday.

However, the timing of this cash distribution is raising eyebrows. The company’s most recent buyback was in FY23, when it clocked more than 19% topline growth. But muted growth in the years since has left investors wary. Simultaneously, Indian IT’s ability to keep up with evolving technologies is being questioned. One could argue that against this backdrop, Infosys should be reinvesting excess cash into upskilling or technological advancements rather than giving it to shareholders.

Is Infosys trying to lift short-term sentiment at the cost of long-term gains? When the going gets tough, should you throw a party?

Tough times for technology services

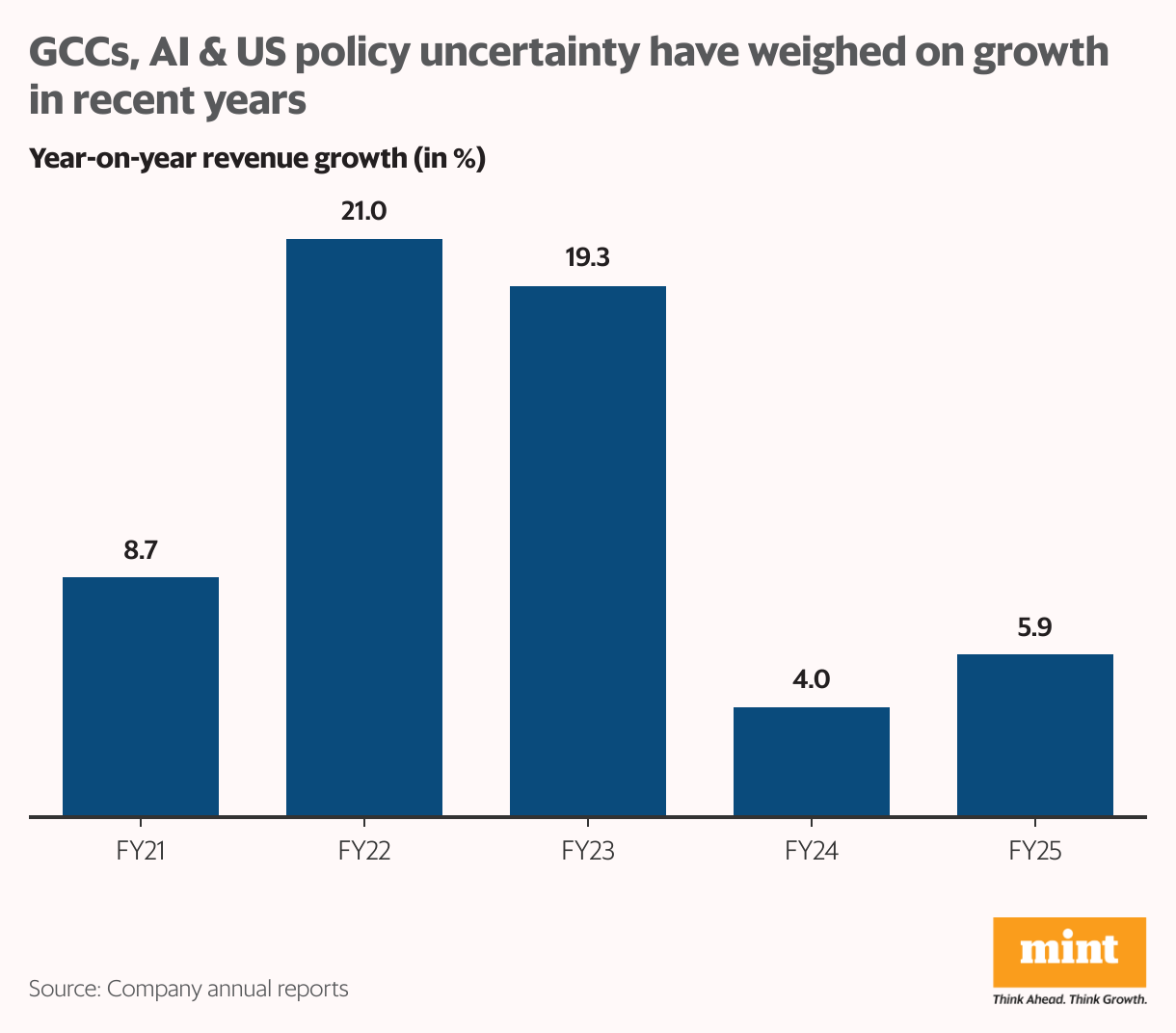

The pandemic-induced lockdowns caused businesses to turn swiftly towards digitisation, bringing windfall gains for Indian IT service providers. Infosys posted about 20% year-on-year growth in revenue in FY22 and FY23.

But things took a turn for the worse soon after. Competition from mid-cap players intensified. Global capability centres (GCCs) came up, giving international firms a way to access cheap technology talent without having to pay IT majors’ hefty fees. AI made matters worse, with clients demanding a passthrough of (over)estimated AI productivity-led cost-savings.

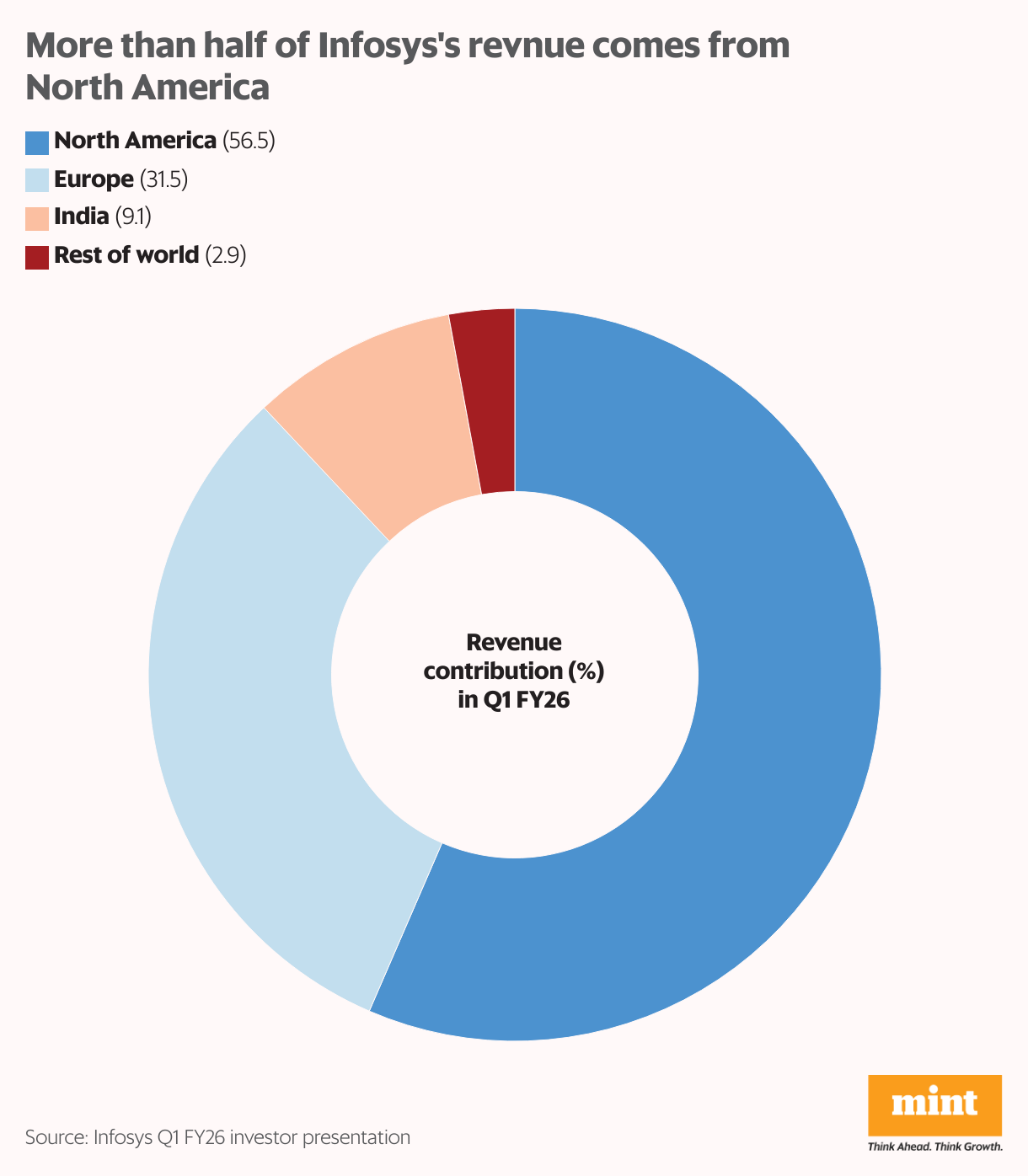

In 2025, tariff and immigration policy uncertainty in the US further constrained US firms’ IT spending. Indian IT derives about half of its revenues from the US, and for Infosys that number is 56%. So, when US firms hold back on IT spending amid uncertainty, the growth of Indian IT majors like Infosys is severely affected. Infosys’s topline has grown by just 1% in the first six months of 2025.

Europe is the next-largest revenue driver for Indian IT, responsible for about a third of its revenues. The region has had troubles of its own – the war in Ukraine, runaway energy inflation and, more recently, sluggish growth. With IT spending constrained in major geographies, Infosys’s revenue growth has been in the low to mid single digits since FY24.

Large caps lag

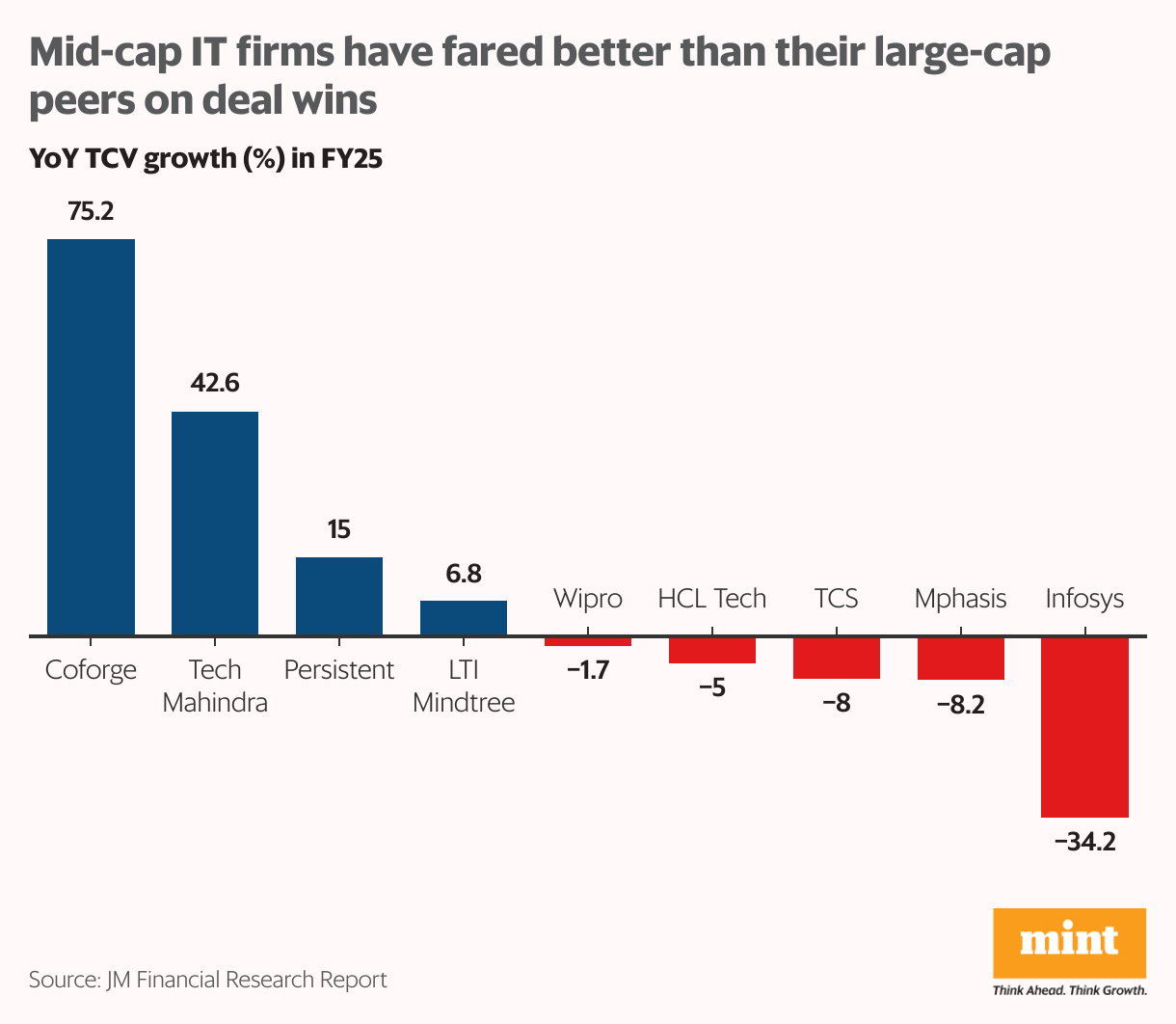

Infosys won deals with a total contract value (TCV) of $11.6 billion in FY25, down from $17.7 billion in FY24. In Q1 FY26, Infosys bagged $3.8 billion worth of deals, and 55% of this was net new deals. When times are uncertain, clients prefer to sign new, smaller and shorter deals instead of renewing old ones. This has been seen across almost the entire large-cap IT space.

Interestingly, mid-tier players have been faring better. Even if we leave out Coforge, which has benefited from its acquisition of Cigniti, and Tech Mahindra which, is a turnaround story, mid-cap IT firms improved their deal momentum in FY25.

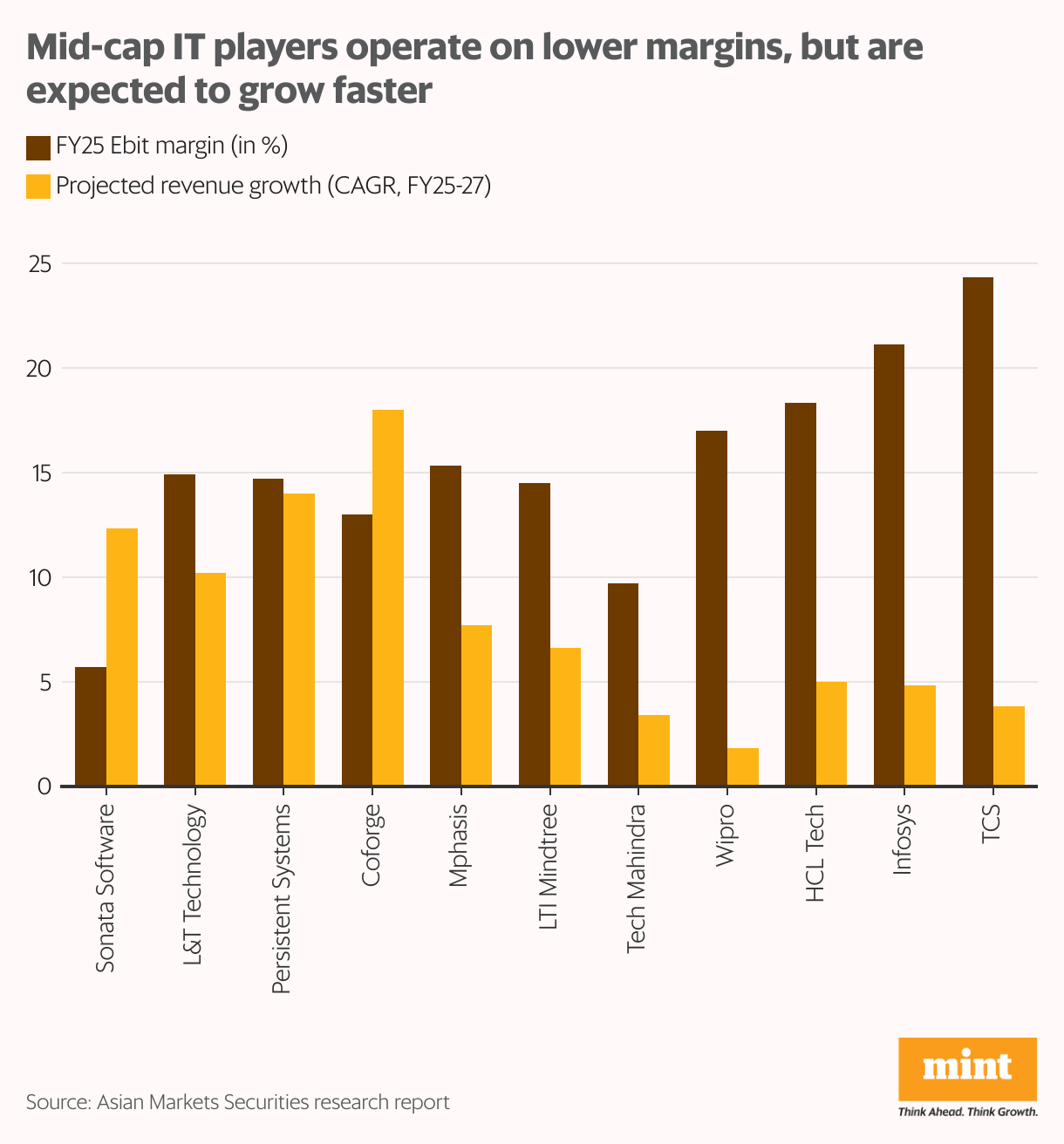

While mid caps have had to compromise on margins, their growth has held up better. According to a report by Asian Markets Securities, mid cap IT players should grow at a double-digit compound annual rate between FY25 and FY27. Meanwhile, large-cap players are expected to clock less than 5% CAGR growth. Infosys has been among the worst performers on both TCV and topline growth.

Short-term gain for long-term pain?

Mid caps IT companies’ outperformance could be attributed to their higher agility, competitive payment structures, and more efficient organisational structures. Unlike IT majors, which have operated in hierarchical org-structures and on resource-based payment, mid-cap players have chosen outcome-based payment models delivered through project-centered teams.

To be sure, the need for a change is not lost on the large firms. TCS recently made headlines for laying off 12,000 employees due to “skill-mismatch” – a euphemism for removing middle management to make room for leaner teams and freshers skilled in AI.

That said, with less than 1% of revenues spent on R&D, India Inc. is miles behind other countries when it comes to focussing on innovation. Sectors such as pharma are among the top R&D spenders in India, and despite the AI upheaval, IT ranks low on this metric.

Another point to note is that while Accenture has started reporting AI-led business, Indian IT firms are still reporting metrics such as AI-ready workforce. Considering the large AI investments being made abroad, Indian IT investors now expect more clarity on its tangible benefits. The Nifty IT index has corrected by 16% over the past year, significantly underperforming the broader market, which has remained flat during this period.

Against this context, it is worrying that Infosys is going a different way. While the company has a history of returning capital to shareholders through dividends and buybacks, the ₹24,500-crore cash balance on its books would have been better spent elsewhere at this time. Instead of cutting costs amid slowing revenues, reorganising its team structures to keep up with the competition, and investing in imparting new skills to its workforce, Infosys seems to have prioritised short-term market sentiment.

Where do we go from here?

When a company buys back shares, earnings-per-share and return-on-equity numbers get a short-term boost. It also usually signals management’s confidence in future cash flows. But that’s not the case for Infosys’s latest buyback. The sector’s mellow prospects aren’t news to anyone. Infosys management itself has guided for mere 1-3% constant-currency growth in FY26.

The US economy’s growth is expected to slow down from 2.8% in 2024 to 1.7% this year. The euro area is expected to post sub-1% growth. Amid geopolitical and economic uncertainty, the long-term prospects for these regions look uncertain as well. Thirty-year US treasury yields touched 5% a couple of months ago, and those in the UK touched 5.7% recently. Struggles in these key geographies could hamper Infosys’s growth.

That said, the company’s diversified verticals offer some comfort. No vertical contributes more than 30% of revenue. The latest reported quarter saw a sequential improvement, coming in better than estimates. Inorganic expansion and the recently announced Versent deal could also improve growth prospects. Management has raised the lower end of its FY26 growth guidance from flat to 1%.

Investors will hope that with short-term sentiment sorted, the company will now focus on structural improvements – upskilling, tech advancement and the works. The stock’s undervaluation is another factor in its favor. It trades at 20 times projected earnings, a discount to the sector’s price-to-earnings ratio as well as its own five-year average PE of 25. Owing to uncertainty in its business, brokerages have a wide range of price targets – ₹1,660 to 1,940 – reflecting 8-27% upside from current levels.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author holds shares of some of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.