He dances his way to the front stage, where a giant LED screen flickers with stock tickers and candlestick charts. He grabs the mic and fires off stock tips between sudden, jerky dance moves. A few attendees start swaying in their seats, and before long, half the front row has leapt up to join the gentleman boogying on stage.

Only in India can a stock-trading workshop be almost indistinguishable from a wedding sangeet. And why not? In a country where every moment, from birth to funeral feasts, plays out at full volume, why should the stock market be left out?

But the real problem with celebrations is not that they inevitably come to an end, but that someone always has to foot the bill.

Great Indian rope trick

Earlier in December, the Securities and Exchange Board of India (Sebi), India’s market regulator, came down against Avadhut Sathe, the grey-haired, dancing finfluencer mentioned above, and his trading academy. They were accused of running unregistered investment advisory and research operations dressed up as stock market education.

The regulator’s interim order stated that through slick advertising, Avadhut Sathe Trading Academy Pvt. Ltd had amassed an enormous ₹601.37 crore from more than 337,000 individuals since 2015. The regulator zeroed in on eight courses offered between January 2020 and October 2025 that accounted for ₹546 crore in collections, and ordered the seizure of this amount.

View Full Image

To check the trading academy’s claims regarding its courses on options trading and other strategies, Sebi obtained the profit and loss data of participants for a period of six months following completion of its most expensive ‘mentorship’ course, for which Sathe charged a hefty fee of ₹6.75 lakh.

The firm did not share PAN details, but exchanges’ records helped identify 186 of the 311 participants. Their combined outcome? A net loss of ₹1.93 crore. A total of 121 of the 186 traders (roughly 65% of the batch) ended the six-month period in the red.

In FY25 and FY26 (up to November 2025), Sathe and his company recorded steep cumulative trading losses of over ₹6.19 crore, even as they promoted themselves as market maestros capable of teaching others to beat the system.

Sathe’s firm said it will challenge Sebi’s order. He did not respond to an email seeking clarification from Mint.

But this was not an isolated case.

Among the defining moments for India’s markets in 2025 was the regulator’s crackdown on Jane Street, the Wall Street-based high-frequency trading (HFT) giant.

In an interim order in July, Sebi barred Jane Street from the domestic markets, accusing it of manipulating benchmark indices such as the Nifty and Bank Nifty between August 2023 and May 2025, and asked it to disgorge unlawful gains of a whopping ₹4,844 crore. Jane Street paid the amount but has challenged the order in the Securities Appellate Tribunal (SAT).

The episode pulled back the curtain on just how exposed small traders are when pitted against sophisticated global firms armed with cutting-edge strategies and lightning-fast execution at speeds ordinary investors can’t even fathom.

A study from the regulator released earlier this year, covering FY22 to FY25, delivered a stark statistic: 91% of individuals trading derivatives lost money. The average loss per trader climbed to ₹1.06 lakh in FY25, up from ₹74,812 the previous year.

A study from the regulator released earlier this year, covering FY22 to FY25, delivered a stark statistic: 91% of individuals trading derivatives lost money.

In other words, the Indian futures and options (F&O) market can be considered a unique wealth transfer scheme where the poor (retail investors) bankroll the ultra rich (multibillion dollar algo firms).

The regulator has taken multiple measures in recent times to cool the frenzy in the derivatives market, but the lure of supposedly quick gains seems too seductive for retail punters.

“I get very nervous when I see youngsters and even housewives venture into risky segments like derivatives, crypto, etc. People must understand that F&O is a zero-sum game, meaning someone has to lose in order for someone else to make money,” Kranthi Bathini, director, equity strategy, WealthMills Securities, told Mint.

“As a newbie, you might be making some money initially, but one wrong trade will wipe you out completely. It will be better for you to heed the regulator’s multiple warnings on the dangers of the derivatives segment, otherwise the market will sooner or later teach you a very expensive lesson,” he added.

Circle of life

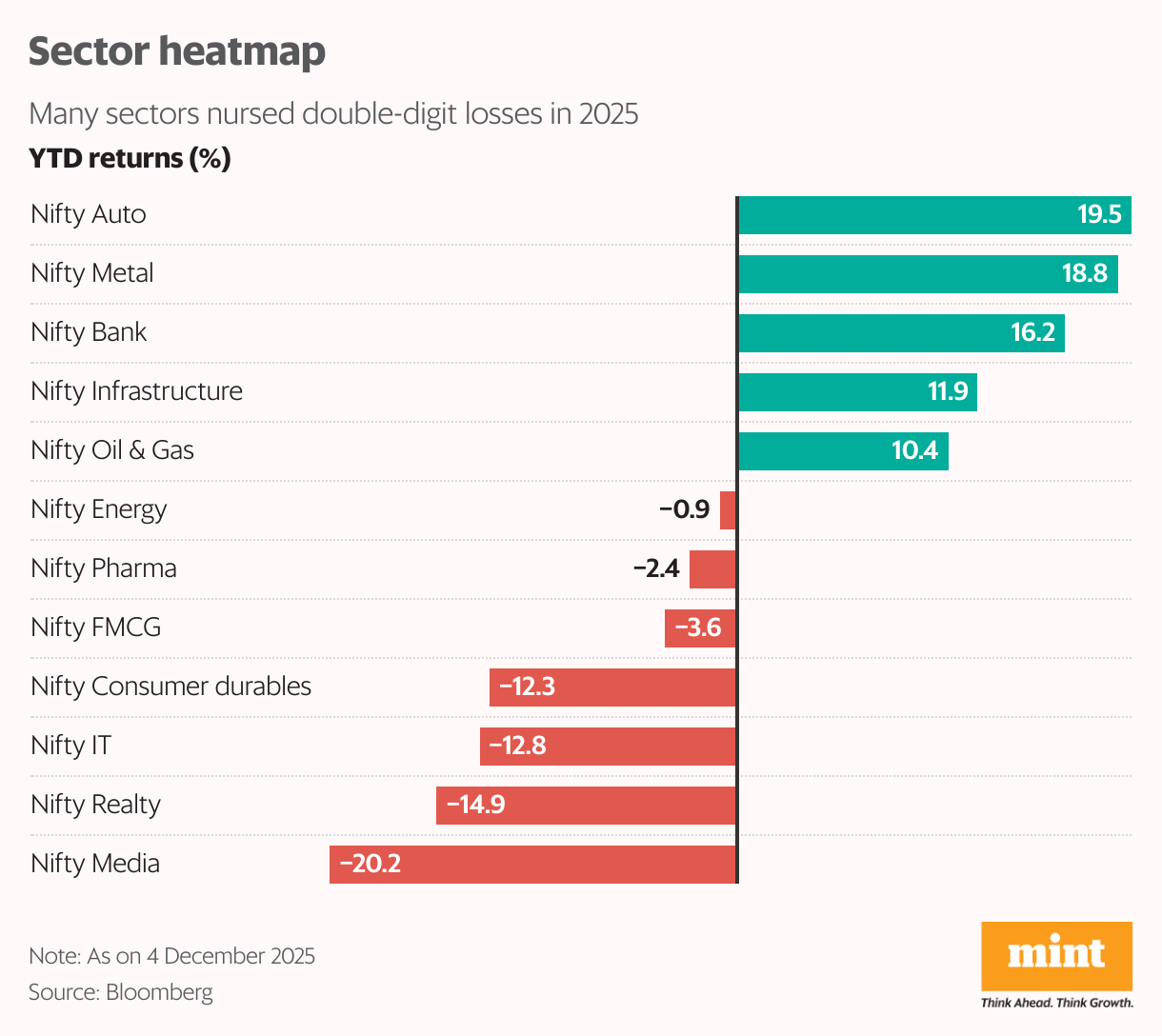

With gains of nearly 10% in 2025, the Nifty has now delivered a decade of uninterrupted positive returns—an extraordinary streak by any measure. But peel some layers, and the story is more sobering.

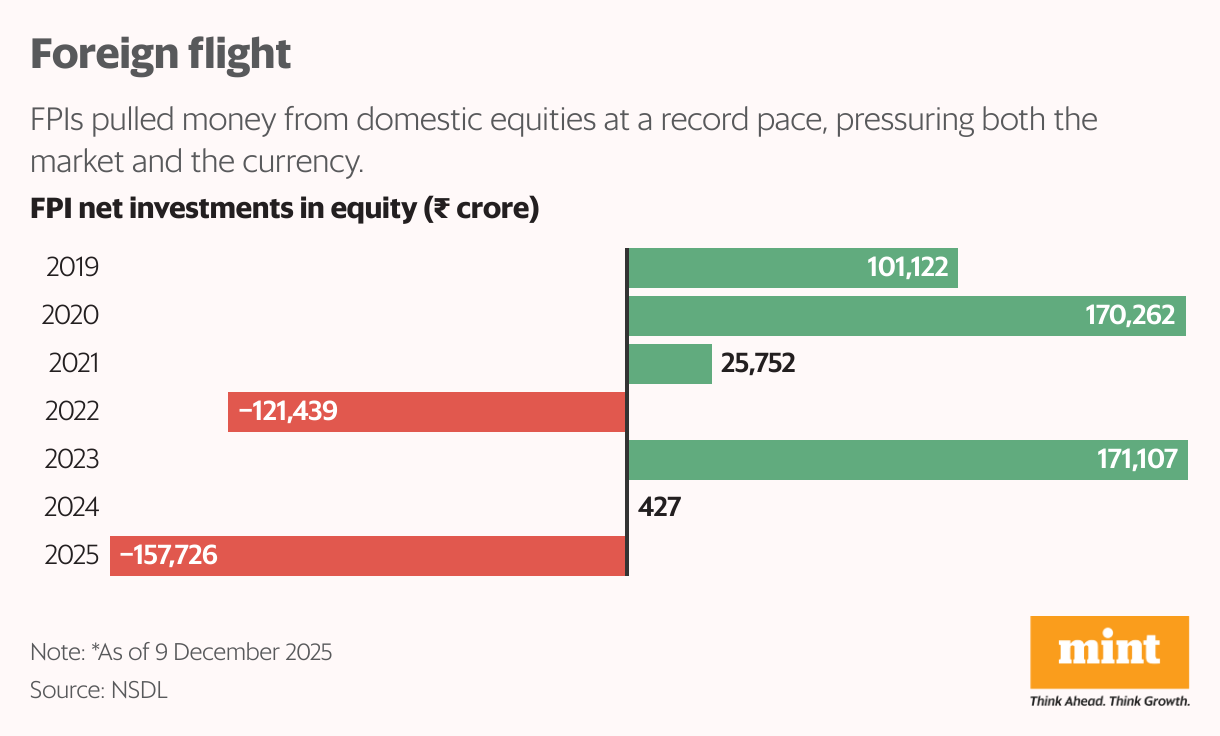

India was the worst performing major market globally this year in dollar terms, and has among the most underweight positions in global portfolios. Foreign portfolio investors (FPIs) have sold a record $17.7 billion of domestic stocks this year amid single-digit earnings growth, elevated valuations and absence of thematic plays like artificial intelligence (AI) and semiconductors.

Beyond the benchmarks, the pain is more evident. The mid-cap index has inched up just 3%, while the small-cap gauge has tumbled 10%. While the Nifty has managed to hit its all-time highs in the past few weeks, the small-cap and mid-cap indices are languishing up to 12% from their 52-week highs, with many constituents losing a whopping 50-60% value—a grim reminder of just how narrow this year’s rally has been.

After years of loading up on small- and mid-cap stocks, many investors overlooked a stubborn truth about the market: it’s always cyclical.

Mid- and small-caps had already vaulted more than 40% in 2023, 20% in 2024, after similar outsized moves post the covid-19 pandemic outbreak. To expect this party to go on indefinitely is akin to expecting a bachelor with steady bathing habits during winters. It happens, but it’s very rare.

Cyclicality, in fact, is the defining trait of most assets—a lesson that caused considerable heartburn this year. Having already watched real estate prices race ahead in recent years, many equity investors found themselves doubly frustrated in 2025 as gold, with a scorching 60%-plus rally, comfortably outshone their carefully chosen stocks.

“Asset allocation and diversification will always be the most important part of wealth creation. In 2025, gold witnessed a very strong rally largely driven by central-bank buying, macroeconomic uncertainty, geopolitical risk, currency/de-dollarization trends, and real-yield dynamics. Investors bought Indian equities during the year on the back of economic recovery and growth in corporate earnings,” Nandish Shah, assistant vice president, PCG research and advisory, wealth management, Motilal Oswal Financial Services, told Mint.

He pointed out that diversification and asset allocation help reduce the volatility and guard against single-asset ownership risk.

“By owning a mix—equities, commodities (gold), real estate (or real estate investment trusts), maybe even bonds or alternatives—the impact of a bad outcome in one asset class can be partially offset by gains (or stability) in another. A well-constructed diversified portfolio tends to have smoother returns over time and lower drawdowns relative to a concentrated bet,” Shah added.

V for valuation

Ask any old hand on Dalal Street and they’ll tell you that markets generate lessons before they generate returns. And in 2025, one of the loudest lessons has been that valuations matter.

If investing were merely about owning quality companies, it would be the easiest job in the world. Just buy names like HDFC Bank, Titan, Nestlé and Hindustan Unilever, and relax. But investing is not about what you buy but what you pay.

A wonderful business bought at unreasonable prices can mean years of underperformance, while an average company bought at a giveaway price can deliver life-changing returns. When the price you pay for a stock is modest, mistakes get forgiven and time works in your favour. But if valuations are stretched, the margin for error vanishes and a company would need everything going in its favour for a long time to justify the stock price.

As Wall Street legend Peter Lynch explained succinctly, if a company is growing at a commendable 25-30% a year, but you’ve bought the stock at a price-to-earnings (P/E) ratio of 50 or 60, this essentially means you’ve paid for the next 10 years of growth in advance. One little mistake and you’re staring at either a huge loss or years of waiting for the stock to recover.

But the same company growing 25-30% a year available at 12 or 15 times earnings will be a multibagger.

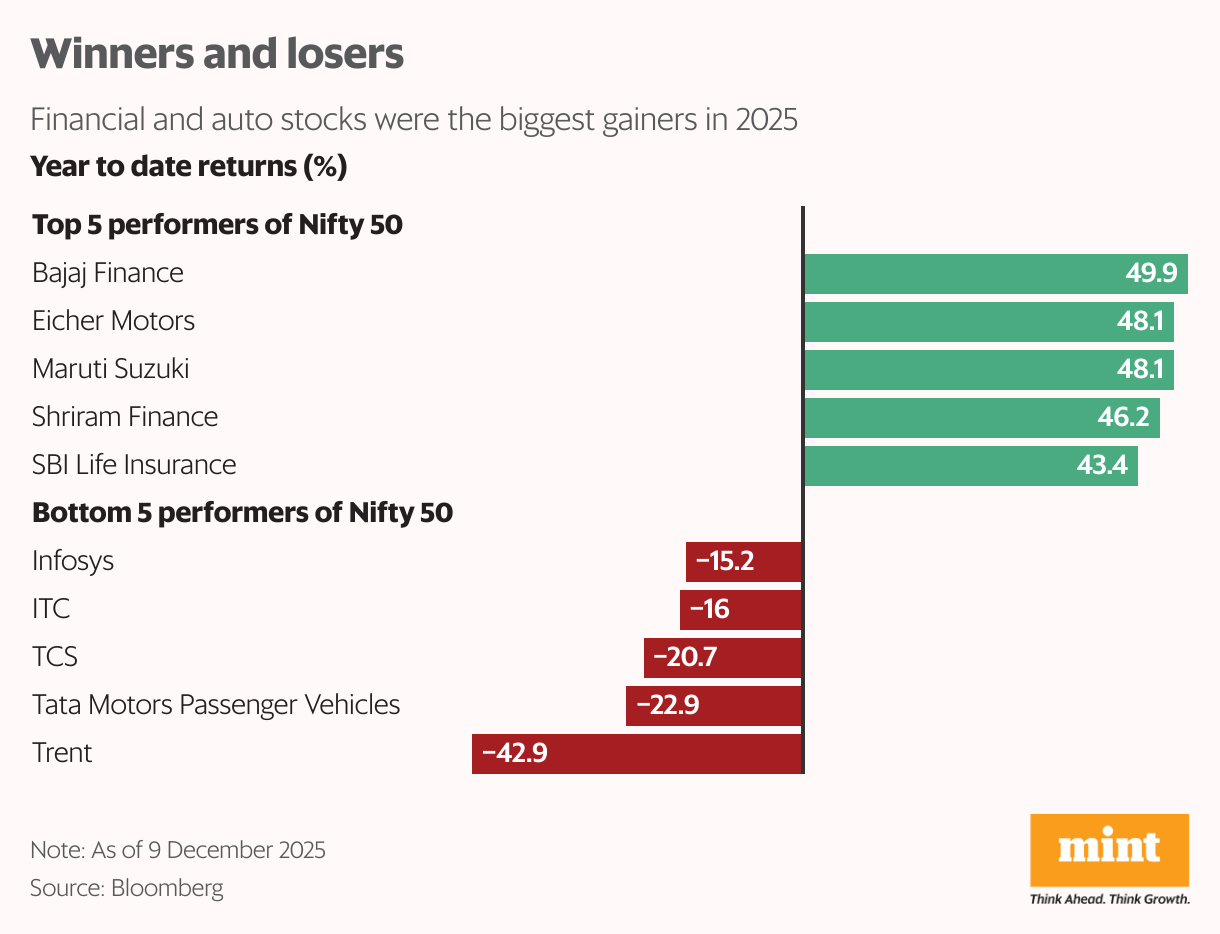

A lot of celebrated names blew up investor portfolios this year, chiefly because of nosebleed prices they paid for those stocks. Look at the Nifty’s biggest laggard of 2025—Trent, the Tata group-owned retailer which for some unfathomable reason was trading upwards of 150 P/E for the past many quarters. After a 40% slump this year, it still trades at a hefty 90-times earnings.

Nowhere was the valuation mania more starkly at play than in the initial public offering (IPO) market.

With a wave of listings and a record ₹1.7 trillion capital raised, India was one of 2025’s liveliest IPO arenas. Yet around half of the stocks are trading below their issue price, including the biggest IPO of the year, Tata Capital. Lenskart’s richly priced offering and subsequent underperformance once again showed how the price you pay is (or should be) the most important variable for retail investors.

“There cannot be a template methodology for pricing these offerings by new age companies. Investors have realised that when companies are well governed, backed by strong business fundamentals and a scalable business model, valuations are a derivative of such a growth story,” Neha Agarwal, managing director and head, equity capital markets, JM Financial Institutional Securities, said.

“Furthermore, companies in sectors with real, structural demand continue to deliver, but that outcome depends heavily on company selection and valuation discipline. This, in turn, helps retail investors by creating a more liquid, accessible and confidence-driven market,” she added.

Her message to investors is to go beyond the buzz and prioritize companies with credible business models, sustainable growth paths and reasonable valuations.

Also crucial is adopting a long-term horizon and treating IPOs as part of a wider portfolio, not a quick-flip gamble.

“Many IPOs may need two-three years for business performance to play out before meaningful value accrues,” she added.

Home and the world

Home is where the heart is. And increasingly, where the ownership sits.

FPI ownership of the Indian equity markets fell to a 15-month low of 16.9% in Q2 FY26, as per National Stock Exchange data. In contrast, domestic mutual funds, buoyed by record systematic investment plan (SIP) inflows, extended their overall ownership to 10.9%—their ninth consecutive quarterly high.

Promoter holdings and direct ownership by individuals were broadly steady at 50.1% and 9.6%, respectively. Taken together with mutual funds, individual investors now account for 18.75% of listed equities—the highest in 22 years.

It’s tempting to read this as a sign of a newly “self-reliant” market, one where domestic institutions can easily offset even record bouts of foreign selling. Yet, as 2025 showed, Dalal Street remains acutely exposed to global crosswinds.

From Donald Trump’s tariff pirouettes to the rapid shifts in AI that have dragged down India’s information technology (IT) heavyweights and the recent plunge in the rupee, the market is nowhere close to being decoupled from the world.

“India is more insulated than it once was — deepening retail participation, pension reforms, insurance penetration and systematic SIP culture have created a stable domestic bid. But markets remain global theatres. Foreign capital is still dominant in large-cap ownership; currency and commodities are external variables; geopolitics can swing sentiment in minutes,” Pradeep Gupta, co-founder and vice chairman at Anand Rathi, stated.

Compared with peers, India may be less fragile, but it is not unshakable.

“The structure is sturdier, yet the winds still matter. The sensible conclusion is neither triumphalism nor fatalism. India is building a resilient base — but resilience is not the same as decoupling,” he added.

Self-reliance, it seems, does not grant immunity.

Road ahead

2025 was a year of consolidation and recalibration where fundamentals replaced frenzy for Dalal Street, and broad-based rallies were replaced by sector and stock-specific opportunities. Experts say this trend is expected to continue in the new year, even as the overall outlook remains optimistic.

With sectoral returns diverging, a diversified portfolio is wiser than concentrated sector bets. — Pradeep Gupta

“After having reclaimed the highs, we expect a new leg of uptrend in markets, especially as corporate earnings environment has improved owing to multiple factors such as stimulative fiscal and monetary measures, better liquidity, a likely thaw in the abruptly strained Indo-US relationships and a softer base for demand and earnings,” Motilal Oswal’s Shah said.

He also suggests adopting a sector-specific approach.

“We raise Indian IT services to mild-overweight by trimming our position in consumer discretionary and healthcare names. Our preferred sectors are diversified financials, IT services, automobiles, telecom and capital goods, whereas our key underweights are energy, metals and utilities,” he added.

For retail investors, the present market calls for balance rather than bravado, Anand Rathi’s Gupta opined.

“With sectoral returns diverging sharply, a diversified portfolio is wiser than concentrated sector bets. Systematic investing—through SIPs or staggered entry — helps counter volatility and avoids the trap of timing peaks. High-quality businesses with strong cash flows and reasonable valuations remain safer than momentum-driven plays. Keep expectations moderate; 2025 has rewarded selectivity, not indiscriminate enthusiasm,” he said.

Most importantly, investors would do well to stay anchored to asset allocation, maintain an emergency fund, and resist reacting to every global tremor.

In uncertain markets, discipline, patience and process often outperform cleverness, he added.