The latest amendment by the Reserve Bank of India to bank lending norms hits a critical cog: cheap leverage.

The RBI has barred banks from deploying depositor money to fund proprietary trading and has mandated stricter collateral rules for capital market intermediaries (CMIs), including brokers and exchanges. This comes on top of the government’s upcoming hike in securities transaction tax (STT) — 2.5x on futures and 1.5x on options — which is anyway likely to raise trading costs.

Whether these measures will materially curb retail speculation will be evident only from the next financial year when the new measures kick in.

But, experts are clear on one near-term effect: liquidity could tighten for institutions that offer and facilitate derivatives trading. Market players predict derivative volumes will shrink with one pegging the contraction at 15-20%.

Brokers, proprietary desks, and exchanges are most exposed to the hit.

Still, some experts believe that markets will adapt. This time, the escape valve may lie in the commercial paper (CP) market.

Mint explains.

What are the new rules of the game?

From 1 April, banks can extend credit to CMIs only on a fully secured basis. In practice, this redraws several long-standing funding arrangements in capital markets.

Until now, brokers could negotiate funding flexibility. A large credit line would be backed partly by collateral, typically fixed deposits or securities, and the other part by promoter or corporate guarantees. Such guarantees allowed banks to extend partially-secured credits or leverage to brokerages.

Come April, that flexibility ends. Under the revised regime, for every ₹100 credit exposure, the bank must hold ₹100 in eligible, tangible collateral. Personal and corporate guarantees will no longer count. They can be an additional safety layer but cannot replace collateral.

Even that collateral has become more conservative. Listed shares remain eligible, but banks must apply a minimum 40% haircut. This means they must value a pledge of ₹1 crore in equities at only ₹60 lakh.

The controls don’t end there. The RBI has also made it costlier for brokers to obtain trading limits.

Currently, brokers use bank guarantees (BGs) as collateral with exchanges and clearing corporations to access trading limits. For sure, BGs are not free but they wouldn’t lock up large chunks of brokers’ capital either. A modest collateral could support a large BG, providing disproportionate leverage to brokerages.

From April, however, every ₹100 of BG exposure must be backed by at least ₹50 of collateral. Of that ₹50, at least half must be maintained in pure cash or cash equivalents. Consider how this will play out on a ₹1,000 crore BG. Under the new rules, the broker must lock up ₹250 crore in cash and another ₹250 crore in other eligible collateral.

Yet another change to lending norms: the RBI has also curbed banks’ ability to fund intraday margin requirements. Earlier, brokers could rely on short-term bank lines to bridge temporary margin blocks, particularly for large institutional trades. From April, such funding is permitted only for settlement mismatches, not trading margins — pushing brokers to hold larger idle cash buffers.

Experts are calling this the “cash trap”.

“Capital efficiency declines sharply when leverage channels are restricted,” explains Mitesh Dalal, head of broking at Sanctum Wealth. “Strategies such as arbitrage, high-frequency trading and jobbing are low-margin, high-volume businesses. Their economics depend critically on inexpensive funding and margin flexibility.”

If leverage becomes costlier or harder to access, liquidity may dry up and spreads may widen, warns Dalal. He expects the RBI’s moves to trim derivatives volumes by 15-20% when viewed alongside recent STT hikes and adjustments to derivatives expiry structures.

Why is it worse for prop traders?

Institutions or individuals who trade with their own capital — a.k.a proprietary traders or prop traders, in short — are likely to bear the brunt of RBI’s lending crackdown. Firstly, banks will be strictly prohibited from financing prop traders. Moreover, they will have to lock in 100% collateral when issuing BGs to prop desks, half of which has to be either in cash or cash equivalents.

Without cheap credit and BG-supported leverage, prop traders’ position sizes may shrink. This is a concern because they contributed 60% of overall equity derivative (notional) turnover in 2025, according to National Stock Exchange (NSE) data.

Hence, their reduced participation can thin order books and have profound impact on volumes and liquidity, particularly in options where turnover intensity is highest, said Dalal.

Lower liquidity widens bid-ask spreads. Wider spreads increase execution costs. Higher costs reduce trading profitability. Lower profitability further dampens turnover which ends up affecting discount brokers too.

Market leaders like Groww and Angel One derived 53% and 49% of their revenue from equity derivative broking in the December quarter respectively. Even diversified players like Anand Rathi Share and Stock Brokers see about a quarter of their income from this stream, implying that the knock-on effects of RBI’s rules would extend beyond proprietary desks.

How will exchanges fare?

While NSE derived 53% of its revenue from equity derivatives turnover in Q3 FY26, BSE’s revenue share was more concentrated at 63%. Exchanges rely significantly on transaction charges linked to options premium turnover. Hence, tighter funding norms alongside higher STT could dampen derivative volumes, posing a potential drag on their revenue growth, said experts.

In such a scenario, BSE could be worse off since it has relatively negligible exposure to other revenue streams like the equity cash or futures markets. Given that proprietary traders account for almost half of BSE’s equity options premium turnover, Jefferies estimates a potential 10-12% drop in options turnover, implying a similar drag on earnings.

But Manish Jain, head of fund management at Centrum Broking cautioned against jumping to conclusions. “Markets adapt. We will find a way around before the changes come into effect,” Jain said. “Alternate funding channels like CPs and structured credit will likely absorb part of the shock. I doubt this will become a structural issue.”

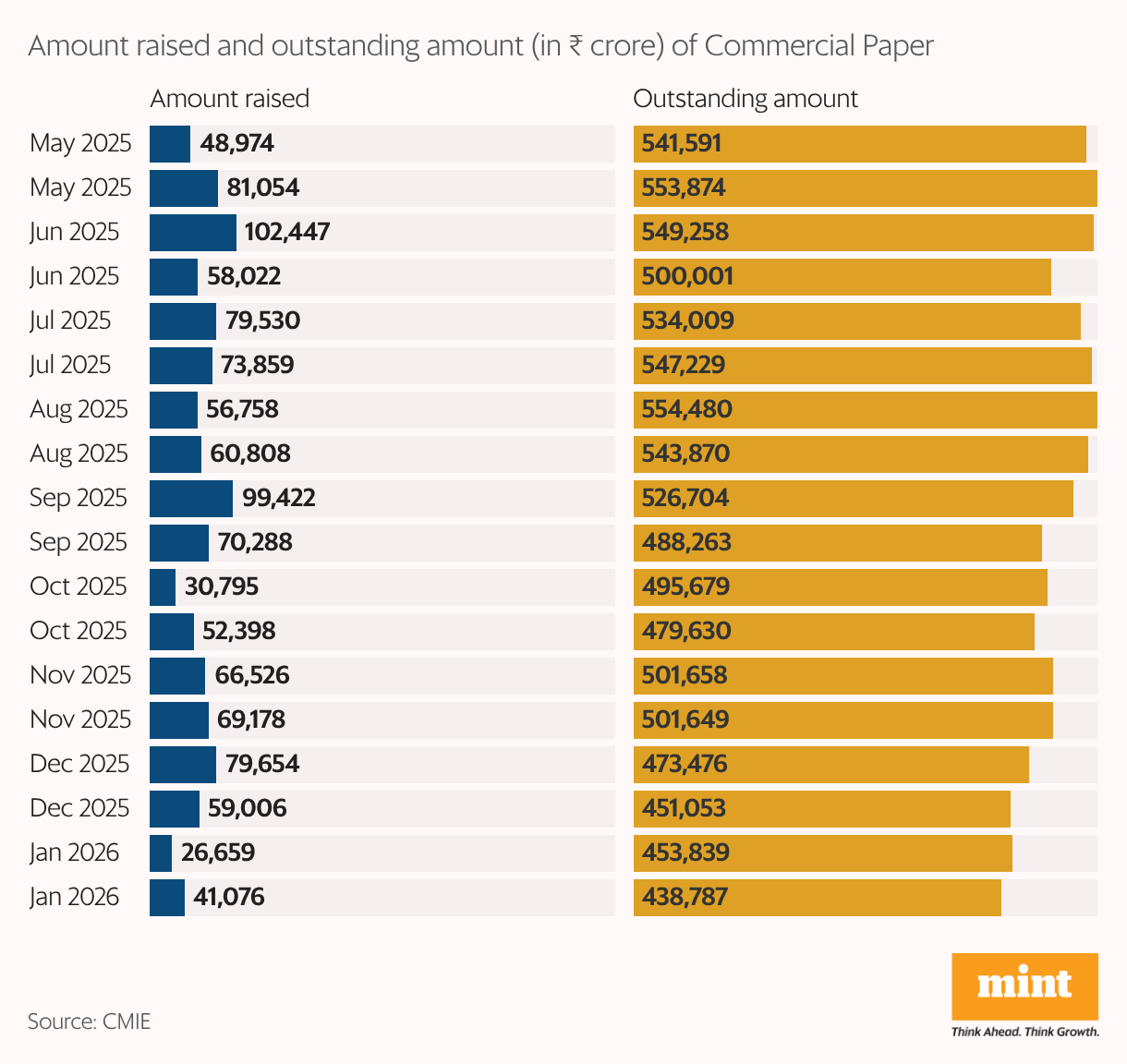

Can CPs offer a way out?

As bank funding tightens, debt fund managers say brokers might lean more heavily on commercial papers. CPs are short-term unsecured debt instruments issued by companies to meet working capital needs. Their maturities typically range from three months to one year.

“It is very much possible that CP issuances rise as brokers adjust to tighter bank funding norms,” said Pratik Shroff, fixed income fund manager at LIC Mutual fund.

Debt market experts noted that broking firms already rely on CPs to fund their margin trading facility (MTF) books. They now anticipate an increase in incremental CP supply, as bank guarantees placed with exchanges will require higher cash or near-cash collateral, creating short-duration liquidity needs well suited to CP instruments.

However, experts warn that increased CP issuance may push yields higher, inflating borrowing costs. That could compress margins for brokers and prop desks. But given the current supply and liquidity conditions, one-year CP rates still appear “manageable”, said Shroff.

Outstanding CP issuances have declined by just over ₹1 trillion since August 2025, falling to approximately ₹4.4 trillion for the fortnight ended January 31, shows CMIE data. Recent investor preference for bank certificates of deposit has kept CP supply subdued, said experts. Hence, the low base could absorb fresh brokerage issuance without materially pushing yields up. Still, it remains unclear if CPs would retain a cost advantage over bank funding for brokerages.