Notably, the multibagger stock has delivered a staggering 1,100% gain over the past five years. And with strong fundamentals driving momentum, the rally may still have room to run.

The light commercial vehicle (LCV) manufacturer recently secured a contract to supply 2,978 Force Gurkha light vehicles to the Indian Defence Forces, marking its foray into the defence sector. Before that, it bagged an order for 2,429 ambulances for Uttar Pradesh’s Medical Health and Family Welfare Department. These wins, coupled with robust earnings, have fueled investor optimism.

Read this | Hero MotoCorp has hit a speed bump—can it rebound?

But the bigger story lies in Force Motors’ aggressive diversification strategy—expanding beyond its core strengths, moving into premium segments, scaling globally, and making a bold push into electric vehicles (EVs).

Can these moves sustain Force Motors’ momentum, or will the rally face hurdles ahead?

Shifting gears

Force Motors is repositioning itself in the LCV space by targeting high-end commercial vehicles with Urbania, a premium offering launched 18 months ago. Traditionally, the company has dominated the passenger LCV market—think school buses and ambulances—holding a 70-75% market share. Now, it’s betting on new segments such as corporate commutes, elite tours, and hospitality, where demand for luxury vans is rising.

The response so far has been promising. Large corporations like Boeing and JP Morgan have added Urbania to their fleets, signalling its appeal. And while the premium segment is new territory for Force Motors, the company is no stranger to the luxury auto space. It already manufactures and assembles engines for BMW and Mercedes-Benz at its plants near Chennai and Chakan, respectively, and has longstanding collaborations with Daimler, Rolls-Royce, Bosch, and MAN.

Beyond Urbania, Force Motors has also introduced 33-seater and 41-seater monocoque buses, directly challenging industry heavyweights like Tata Motors and Eicher. The strategy is already paying off, with the company grabbing a 7% market share in this segment within the first year.

Meanwhile, it has also streamlined operations, exiting the tractor segment in FY24—a segment where it struggled to gain traction in a highly competitive market.

Global expansion and EV bet

Historically, Force Motors has prioritized domestic demand over international expansion, largely due to its right-hand drive (RHD) portfolio. That’s changing.

With the introduction of left-hand drive (LHD) variants, the company is eyeing new markets in the Middle East, Africa, and South Asia.

Its first overseas assembly line, located in Kenya, is a key step toward this goal, focussing on producing Traveller vans for African markets. Force Motors expects exports to reach 3,000-4,000 units annually once all planned models hit the market.

Simultaneously, the company is preparing for an electric future, earmarking ₹2,000 crore for investments across its value chain over the next 3-4 years. Of this, ₹200-300 crore will be directed toward EVs and sustainability initiatives.

Read this | US tariffs, EV slowdown pose global hurdles for Indian auto

The EV roadmap includes launching electric versions of its entire van lineup in a phased manner, starting with the Traveller. A new variant is expected every six months, with an electric Urbania slated for rollout by the end of next year. The company is also exploring an electric version of its rugged off-roader, the Gurkha.

A financial turnaround in motion

Force Motors has staged an impressive financial comeback over the past two years, with FY24 marking its best year on record.

Revenue hit ₹6,992 crore, while net profit soared to ₹388 crore—its highest ever—on the back of increased volumes. This turnaround is particularly striking given that the company reported losses in the two preceding years.

Like its peers, Force Motors struggled through the pandemic as school transportation, employee commutes, and tourism ground to a halt. But with demand rebounding, sales have picked up sharply.

Also read | Likely UK plant closure a positive for Ashok Leyland. High promoter pledge isn’t.

Margins, too, have improved. The company’s Ebitda margin expanded to 13% in FY24, compared to a five-year average of just 6.2%. While volatile raw material costs remain a concern, ratings agency Crisil Ltd expects margins to stabilize at 12-13%, driven by a better product mix.

Debt reduction has been another priority.

Force Motors plans to become external debt-free by the end of FY25, using its cash reserves to pare down liabilities. As of FY24, total debt stood at ₹525 crore, down from ₹1,069 crore in FY22, with ₹150 crore owed to parent company Jaya Hind Industries Ltd—a sum requiring no repayment. The debt-to-equity ratio has improved from 0.61x in FY22 to 0.23x in FY24.

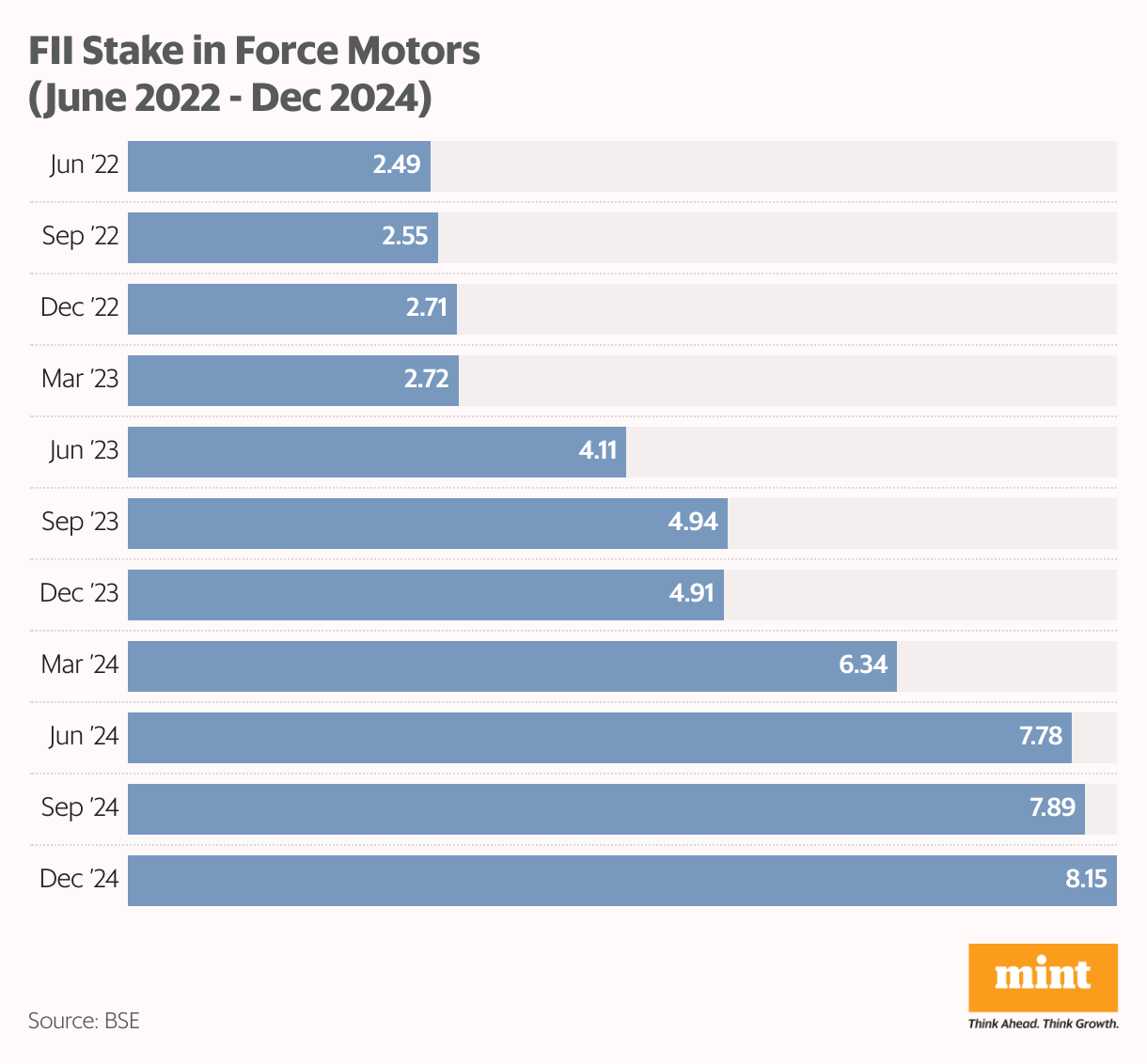

FIIs have taken notice. Since June 2022, foreign institutional investors have steadily increased their stake, which now stands at 8.15% as of December 2024.

That said, the stock isn’t cheap. It currently trades at a price-to-book value (P/BV) of 4.65x—a 235% premium to its five-year average of 1.39x.

Looking ahead

For FY25, the company is targeting top-line growth of 10-15%. It aims to sustain a 40% growth rate for at least two more years, mirroring its trajectory over the past two. Management also expects production to return to its peak of 25,000–26,000 units, last seen in 2015-16.

The momentum so far is encouraging. Revenue has climbed steadily over the last three quarters, and unit sales have risen consistently month after month.

For more such analyses, read Profit Pulse.

As the company accelerates its transformation, execution and profitability will be critical in determining whether the rally has further legs. While strong growth prospects and improving fundamentals fuel optimism, strategic missteps or external headwinds could pose risks to future performance.

About the author: Ayesha Shetty is a research analyst registered with the Securities and Exchange Board of India. She is a certified Financial Risk Manager (FRM) and is working toward the Chartered Financial Analyst (CFA) designation.

Disclosure: The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.