The shift comes after a series of regulatory measures by the Securities and Exchange Board of India (Sebi) starting October 2024, aimed at curbing speculative excesses in the booming F&O segment. These included restrictions on weekly index option expiries and tighter margin regulations, which have led to a sharp drop in derivatives trading volumes since.

Index options average monthly turnover on the National Stock Exchange, India’s largest with around 79% market share in equity options, fell about 27% year-on-year to ₹9.44 trillion in FY26 so far.

According to CareEdge Ratings, total industry revenue from stock broking stood at ₹43,900 crore in FY25. While brokerages do not break out F&O income separately from cash equities, the impact on broking income has been visible.

For instance, broking as a percentage of total revenue at Angel One dropped from 65% in Q3FY25 to 61% in Q1FY26. At 5paisa, it fell from 52% to 46% over the same period. Motilal Oswal Financial Services and Geojit Financial Services, which have more diversified revenue models, saw less change.

“Their sources are diversified. After the curb by the regulator on F&O, now they may shift focus from one segment to another,” said Siddarth Bhamre, head of research (institutional equities) at ACMIIL.

Shifting to recurring revenue

With volatility in F&O earnings, brokerages are pushing harder into fee-based and interest-income businesses. These include wealth and asset management, mutual fund and insurance distribution, and lending against shares.

“Brokers now distribute mutual funds (MFs), insurance, and some have their own mutual funds also,” said Bhamre.

After seeing a drop in volumes, brokers may look at more ways to monetize and build the same customer who is coming for broking, said Nirav Shah, managing director at Equirus Capital. “The focus will not just be on broking but a 360-degree client servicing, as the same client will open a mutual fund account or take a loan against shares, MF or others.”

Dinesh Thakkar, founder, chairman and MD of Angel One, had also flagged this shift in an earlier interview to Mint. “Broking is volume-driven, while wealth and asset management are relationship-led. Our revenue model is fundamentally evolving. It is becoming more stable, recurring,” he had said.

Examples of this shift are already visible: Angel One has ventured into wealth management; Geojit Financial Services manages its own portfolio management services (PMS) and AIF (Alternative Investment Fund) platforms in addition to mutual fund distribution; Motilal Oswal has long operated both wealth and asset management arms.

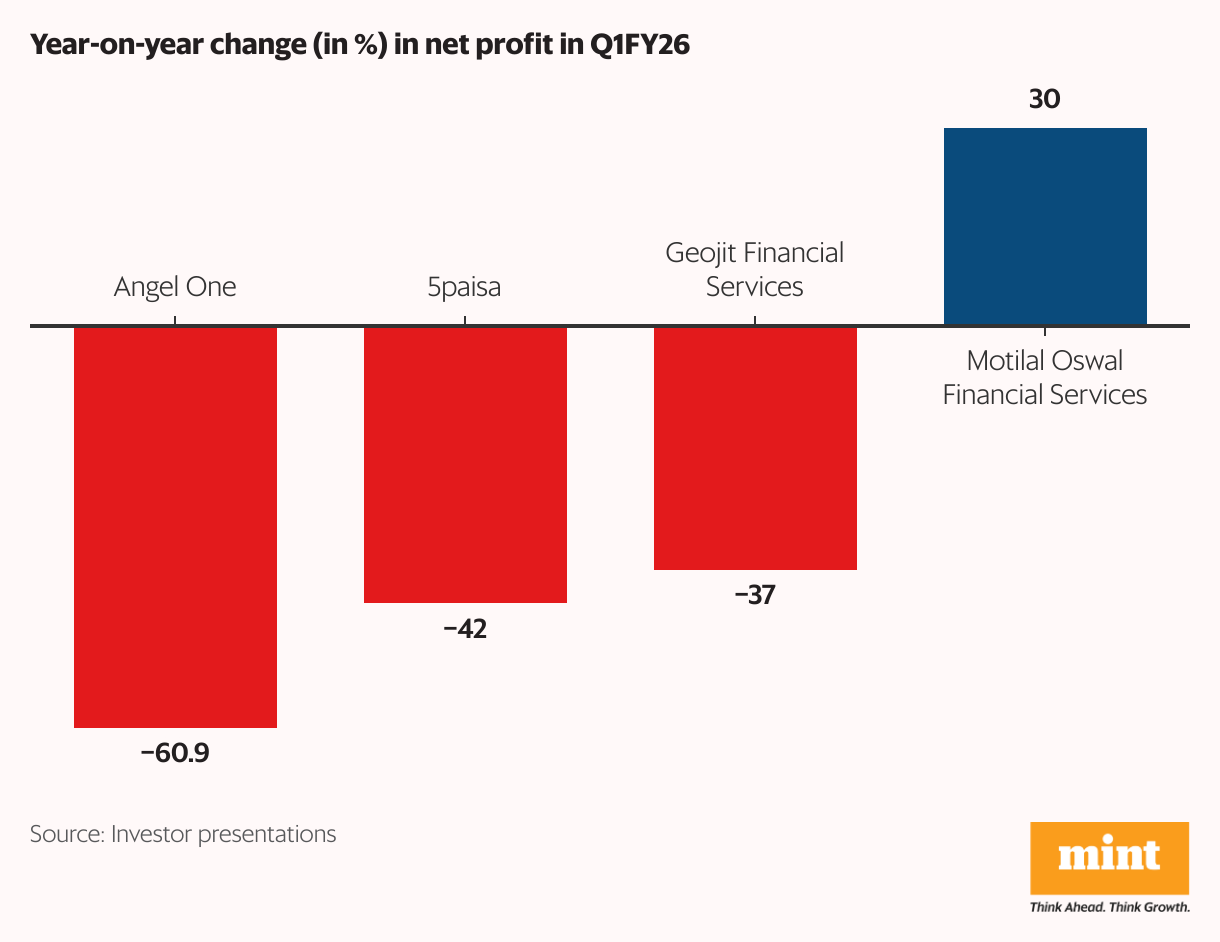

Profits under pressure

The financial impact has been stark.

For the quarter ended June (Q1FY26), profits at Angel One, Geojit Financial Services, and 5paisa Capital fell between 37% and 60% year-on-year. Revenues declined 15–24% over the same period.

Motilal Oswal Financial Services was a notable outlier, posting a 30% rise in profit and 17% revenue growth in Q1FY26. The firm derives only 25% of its income from broking; the rest comes from management fees, distribution, advisory, and net interest income. Even so, its broking revenue fell 11% to ₹359 crore during the quarter.

Jones George, executive director at Geojit Financial Services—which began diversifying into distribution and asset management back in 2015—said broking remains a cyclical business with earnings closely tied to trading volumes.

“It is also prone to margin pressure as when market activity slows, fixed costs like compliance and technology remain constant,” George said.

In contrast, wealth management and distribution operate on a fee-based model that, while lower margin initially, offers greater income stability. “While it takes years to build meaningful earnings from wealth clients, especially through SIPs (systematic investment plans) or AUM (assets under management) growth, this segment offers long-term revenue visibility,” he added.

Adding weight to the shift, net inflows into equity mutual funds rose 24% month-on-month in June to ₹23,567 crore, even though inflows for the April-to-June quarter were down 29% year-on-year, according to data from the Association of Mutual Funds in India (Amfi). Meanwhile, the mutual fund industry’s total assets under management rose 3% sequentially to ₹74.14 trillion in June, marking a new milestone.

The PMS industry also expanded, with AUM rising 10.3% sequentially to ₹87,679.88 crore in the June quarter.

Recent data from brokerages reflect this structural transition.

At Angel One, interest income accounted for 31% of gross revenue by end-June, up from 28% in December, the quarter when Sebi’s regulations took effect. The share of broking revenue declined from 65% to 60% over the same period.

At 5paisa, revenue from allied businesses rose from 19% to 23%. For Motilal Oswal, the revenue mix remained unchanged, with 75% coming from non-broking segments.

Costs rise, margins fall

While top-line revenue is falling for many brokers, operating costs remain sticky or even rising.

Margins are coming down because of rising competition and higher costs, said Arun Chaudhry, director and chief business officer at m.Stock by Mirae Asset Capital Markets, adding that brokers are investing heavily in technology and customer service to stay competitive, further inflating their cost base.

“Earlier, many broking firms were operating at 35-40% operating margins, but now they are seeing margins drop to 20-25%,” said Chaudhry. And this is expected to sustain, as more players are entering the industry and everyone is targeting the same customer base, he added.

Moreover, as the industry consolidates, every broker is spending on customer acquisition as well, say industry executives.

There will also be significant investment driven by the deployment of AI (artificial intelligence), ML (machine learning), and other technology upgrades, as brokers need to modernize their platforms to stay competitive, said Shah of Equirus Capital.

Beyond the numbers, the pivot to new business lines also reflects an effort to escape broking’s regulatory drag.

“Brokers are increasingly entering wealth management business and asset management business in the form of PMS or AIFs,” said Trivesh D, COO at Tradejini. “These businesses have relatively lighter regulatory requirements compared to broking. Unlike broking, which demands daily reporting and large compliance teams, PMS and AIFs involve monthly or quarterly reporting and can operate with lean teams once the technology is in place.”

“Also, brokers with an existing client base can leverage their distribution network to scale wealth businesses or an asset management [arm], which can give them an edge in the start to build an AUM,” he added.

Trivesh added that while broking alone could still deliver mid-teen returns, scaling would require diversification.

“For conventional brokers not working towards a particular niche audience, relying alone on broking may not be sustainable. Their income is being squeezed through the new measures on F&O with only one-week expiry being the prominent case. At the same time, compliance requirements—like stricter reporting, fund flow monitoring, and margin allocation—have increased, raising operational costs,” he said.

However, scaling an asset management business can take time, as increasing the AUM to a certain scale can be difficult even with a head start from the broking business, industry experts say.