In a handful of midcaps,foreign institutional investors (FIIs) have started trimming their stakes.

The FII pullback is not broad-based, but it stands out against the backdrop of strong domestic flows.

Whether it’s on account of weak earnings, execution delays or simply stretched multiples, these 5 midcaps have seen a notable drop in FII ownership in the June quarter.

Here’s a closer look…

#1 Kajaria Ceramics

Kajaria Ceramics is one of India’s largest ceramic and vitrified tile manufacturers. The company has a strong pan-India presence and growing international ambitions.

FII holding fell from 16% in March 2025 to 12.6% in June 2025.

FY25 was a challenging year on the profitability front. While revenue remained steady at ₹4,600 crore, Ebitda and net profit fell. It was weighed down by losses in the UK business, one-time provisions in the now-discontinued plywood division, and margin pressure in the bathware segment.

Yet Kajaria managed to grow faster than the industry. Tile volumes rose 6% year-on-year (YoY) to 114.7 million square meters, outpacing the broader market, which barely grew 2-3%.

There were export headwinds, especially due to the Red Sea crisis. The management expects a bounce-back in global shipments as freight rates normalise.

Kajaria has undertaken a major restructuring. Its three sales teams – ceramic, polished vitrified and glazed vitrified – are being unified into a single team under one state head.

The aim is to streamline costs and improve dealer engagement. Margins have already improved to 16.7% in Q1FY26 from 10% in Q4FY25.

Kajaria has exited the plywood business and rationalised its UK operations. The company is now doubling down on its core areas: tiles, adhesives and bathware.

The adhesives business revenue jumped 64% in FY25. A new plant in Erode, Tamil Nadu, will expand capacity and improve regional servicing.

The bathware segment saw a dip in margins to 4% in FY25 due to initial costs at a new high-end plant. However, the company expects the segment to become profitable in FY26 as capacity utilisation rises. Kajaria is net-debt free with ₹420 crore in cash.

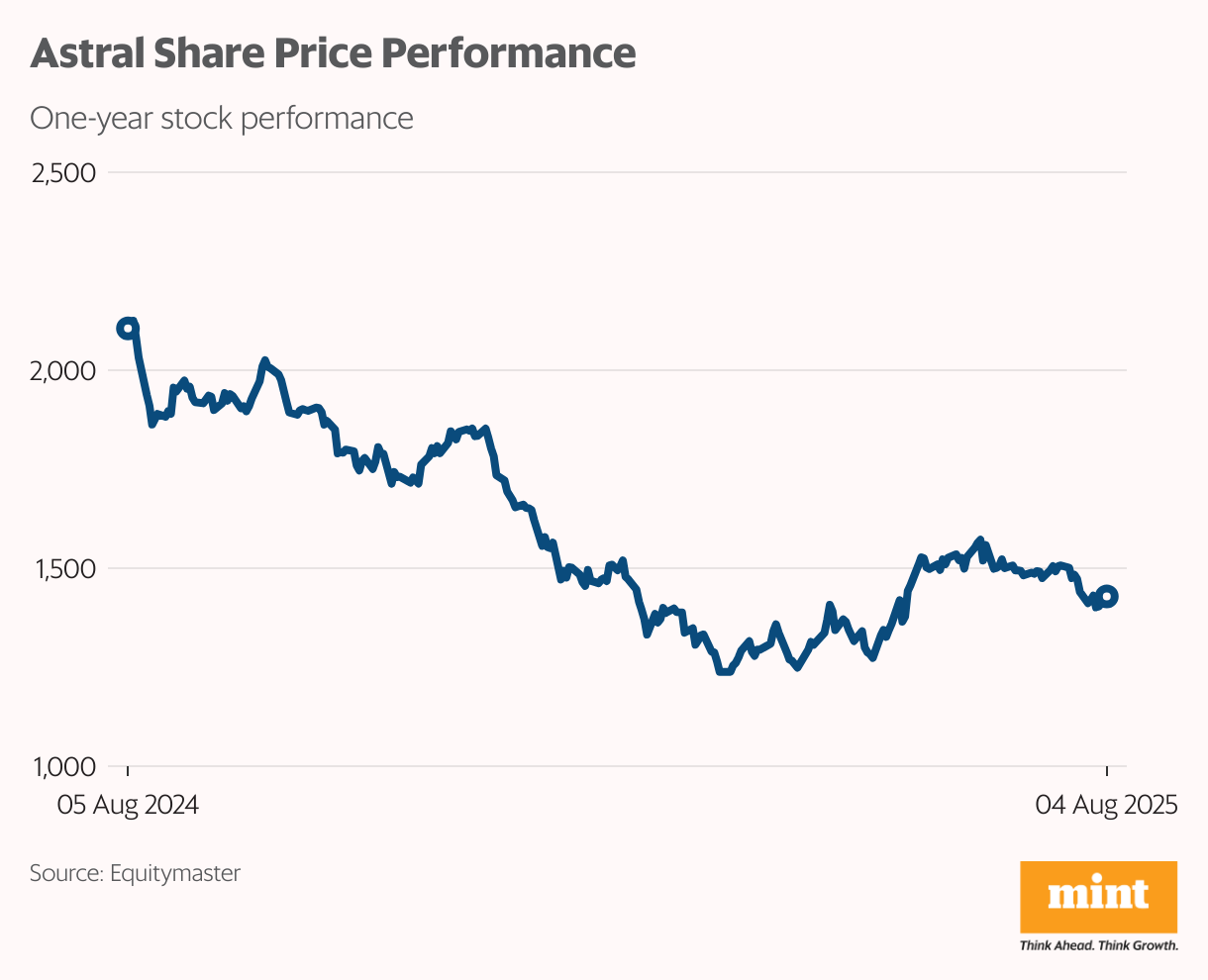

#2 Astral

Astral has quietly evolved from a pipe company into a building materials company with interests in plumbing, adhesives, paints, and even sanitaryware.

In June 2025, FII ownership stood at 20.15%, which was down consistently every quarter from 22.3% in September 2024.

Astral clocked revenue of ₹5,830 crore in FY25, up just 3.4% over FY24. Net profit dipped 4.9% to ₹520 crore, partly due to higher depreciation and interest costs from recent capacity expansions.

This came on top of a soft FY24, making FY25 the second year of subdued bottom-line growth.

The plumbing segment, which accounts for 72% of revenue, grew just 1.3% to ₹4,200 crore. The paints and adhesives segment did the heavy lifting, growing 9.1% to ₹1,640 crore. It now forms 28% of the topline. The company is targeting a 60:40 split between the two segments in the medium term.

Despite weak demand conditions in the core piping market, the company maintained EBITDA margins near 17%. It’s also sitting on ₹460 crore of net cash, giving it room to invest without stretching the balance sheet.

On the capacity side, Astral expanded its pipes and fittings capacity to 310,000 metric tonnes per annum and ramped up production at its recently launched Aurangabad paint plant.

Its sanitaryware business under the “TRUFLO” brand is scaling up gradually and is expected to break even in FY26.

The management is betting big on branding, consistently spending 2.5-3% of revenue on advertising.

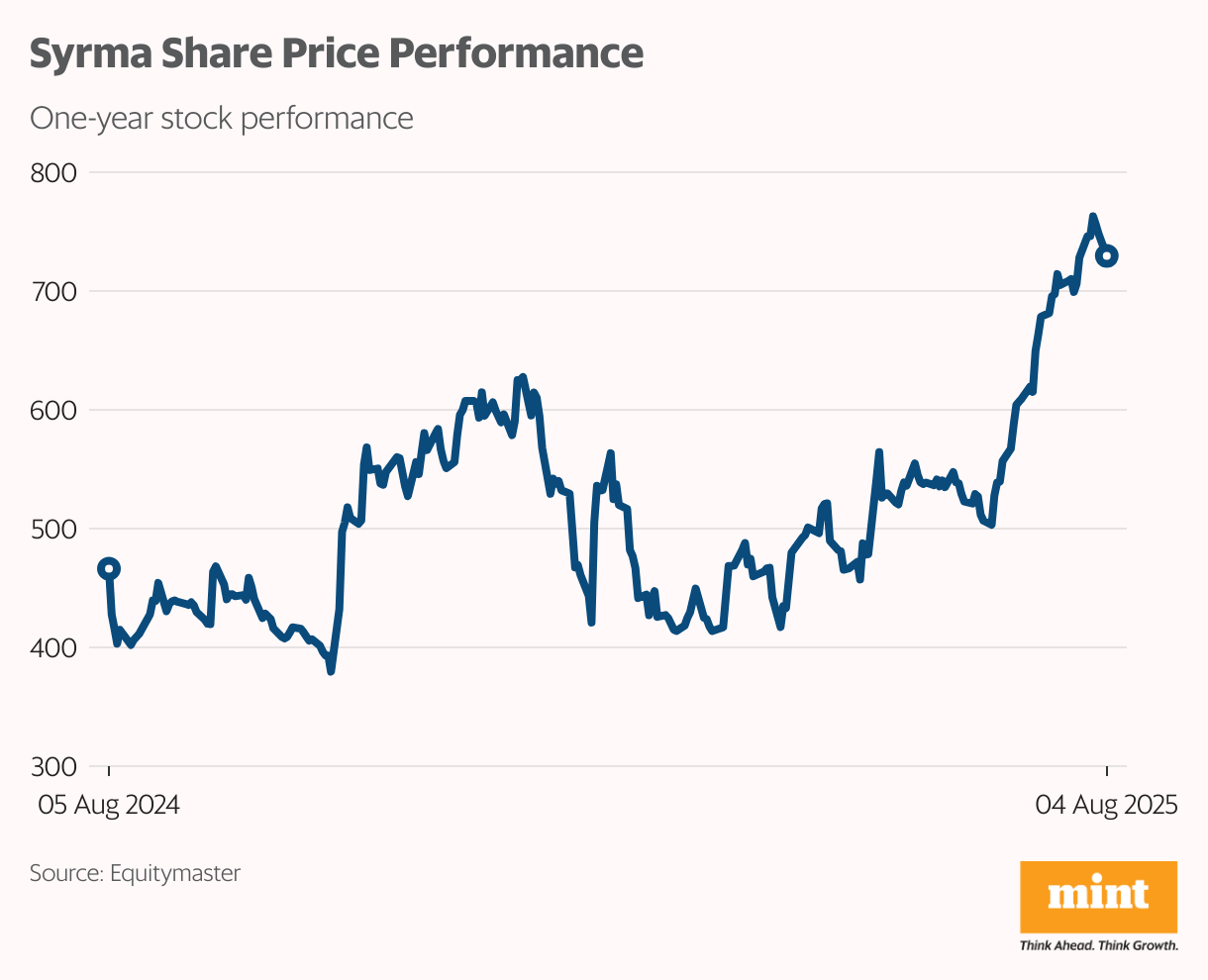

#3 Syrma SGS Technology

Syrma SGS Technology is carving out a space for itself in India’s electronics manufacturing landscape by focussing on high-margin, export-driven segments.

In June 2025, FII shareholding stood at 6.34%, down from 10.32% in September 2024.

While FY25 ended on a softer note due to a fall in global electronics demand, the company kicked off FY26 with a strong rebound in earnings.

In Q1FY26, Syrma posted revenue of ₹960 crore. While that was down 18% from a year ago, EBITDA jumped 69% YoY to ₹103 crore. Operating margins improved to 10.7%, reflecting better cost control, shift in revenue mix and reduced input price volatility.

Exports now account for 25% of revenue. Among verticals, industrials and auto were strong performers. The industrial segment grew 34% YoY in Q1FY26, while auto rose 18%.

Consumer electronics, hit hard by destocking and global demand weakness, were down 48% YoY but showed a sequential recovery.

Syrma specialises in building complex electronics for global OEMs. That includes products like PCB assemblies, magnetics, and RFID solutions, often co-developed with clients.

The company has ₹314 crore in net borrowings as of June 2025 but the balance sheet is stable due to rising cash flows.

Going forward, Syrma’s pipeline remains robust. The management has reaffirmed its full-year guidance of ₹4,500–5,000 crore in revenue for FY26, with operating margins in the 10–11% range.

A new dedicated facility for automotive EMS is under development, which should start contributing in the second half of FY26.

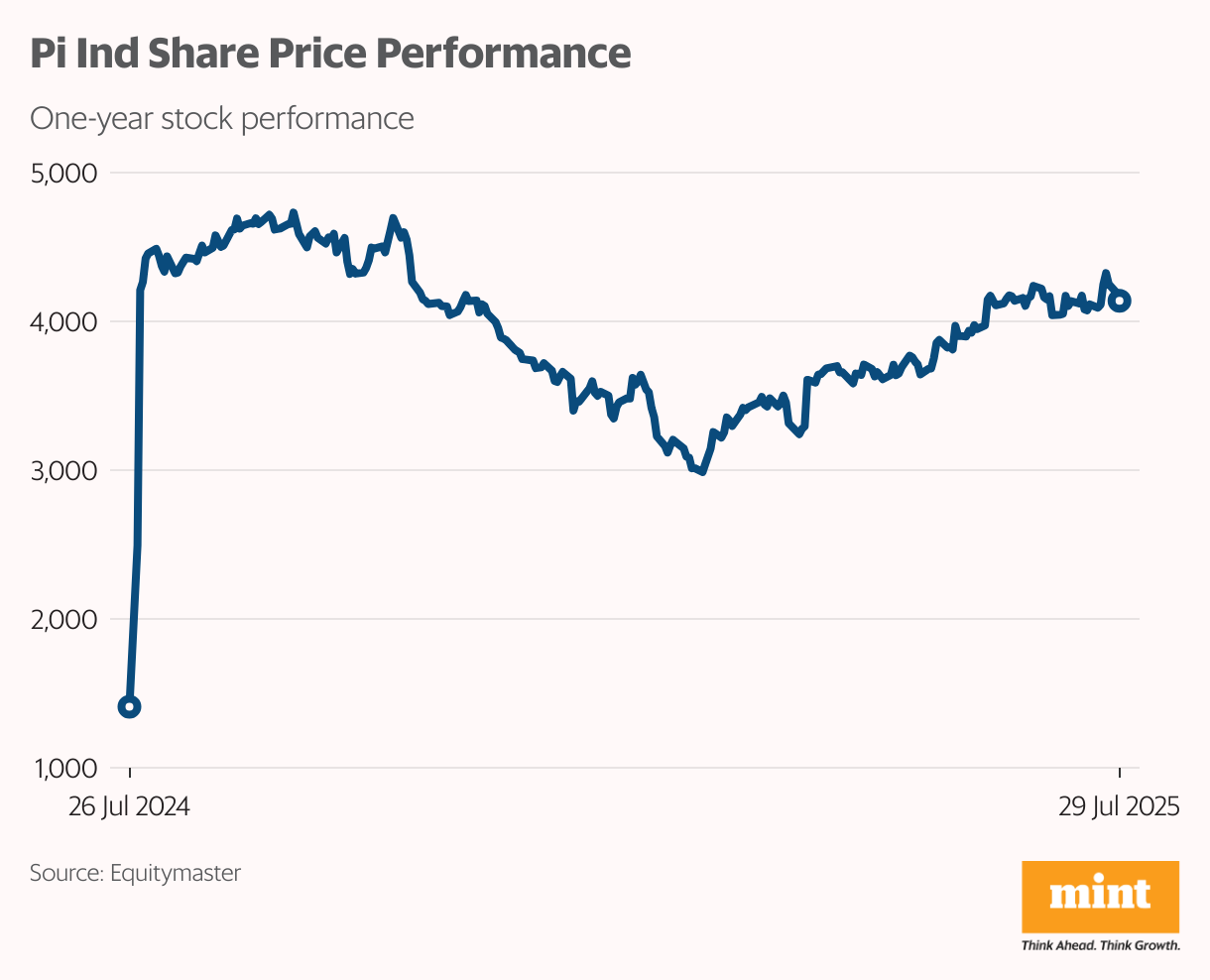

#4 PI Industries

PI Industries is one of India’s most diversified and research-led life sciences companies. The company is scaling up across verticals, aiming to become a global contract research and manufacturing powerhouse, from agri-inputs to custom synthesis to biologicals and pharma.

FII shareholding was 16.98% as of June 2025, down from 19% in September 2024.

FY25 was a year of moderate top-line growth but expanding capabilities. PI reported consolidated revenue was up 4% YoY. Gross margins improved to 53%, thanks to a better product mix and growth in higher-value segments, like biologicals and new molecule exports.

Domestic agri-branded revenue rose 6%, driven by strong Rabi season demand, while export revenues grew 5% despite price corrections. Biologicals were a bright spot, rising nearly 20% YoY.

What sets PI apart is its aggressive investment in innovation. Its in-house R&D team includes 700 scientists and over 200 PhDs. The company has filed more than 210 patents (44 in FY25).

New product contributions stood at 15% of revenue. The biologicals pipeline now includes over 20 products across multiple geographies.

PI now operates 15 multipurpose plants and is scaling up both domestic and overseas capacity.

Pharma, via its PI Health Sciences arm, now contributes 6% of exports. Q1 FY26 showed a 33% sequential jump in pharma revenues.

The management aims to be a differentiated CRDMO player over the next 3-5 years.

PI’s balance sheet remains rock-solid. It ended FY25 with surplus cash of ₹4,090 crore and almost negligible debt.

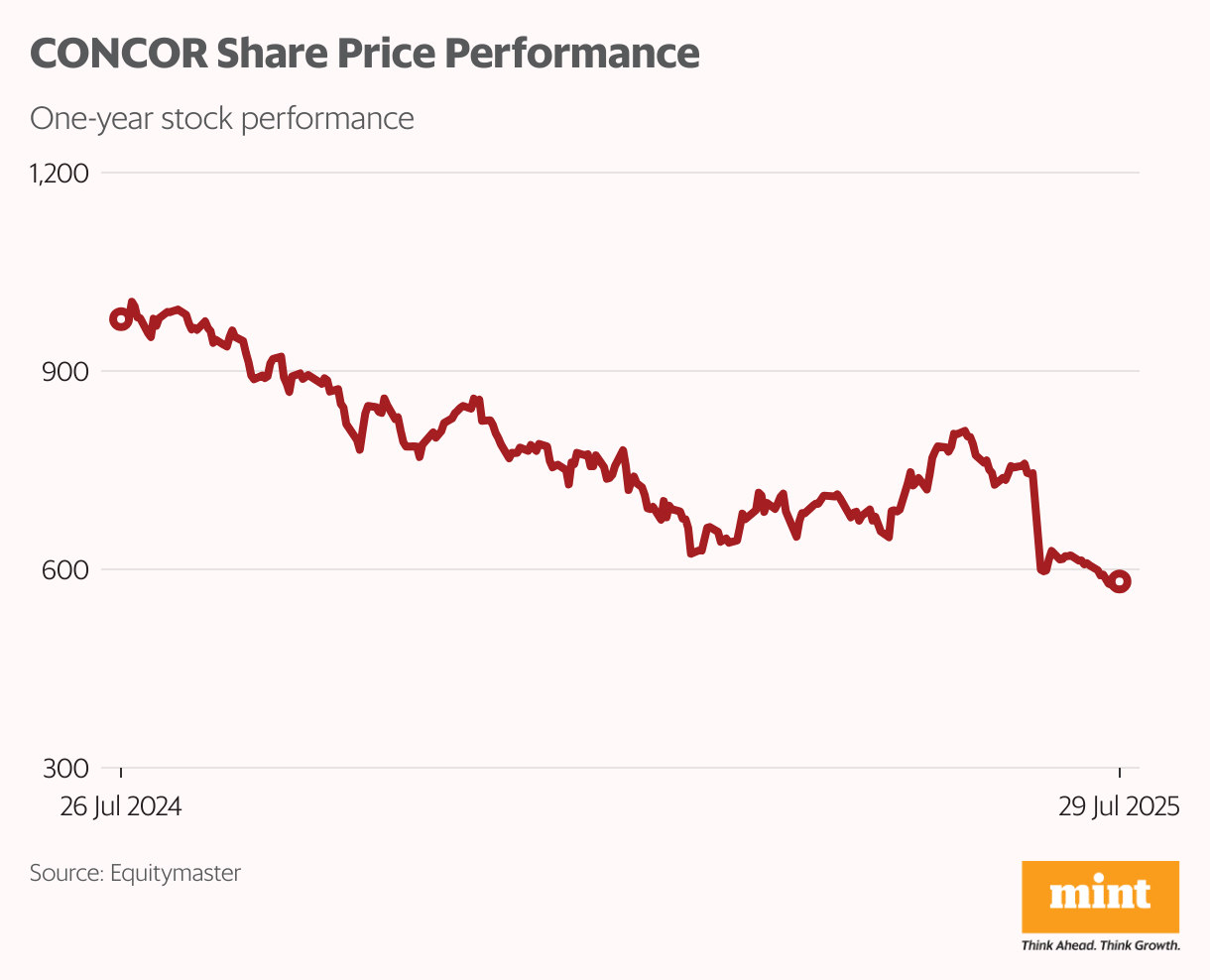

#5 Container Corporation of India

Concor is India’s largest rail-based container operator and acritical player in the country’s freight logistics chain.

The company stands to be one of the biggest infrastructure beneficiaries of the logistics upcycle, with India’s container handling capacity expected to double over the next five years.

FII holding stood at 12.69% as of June 2025, down from 16.15% a year ago.

In the June quarter of FY26, Concor clocked volume growth of 9% YoY. Revenue for the quarter stood was up 11% and net profit rose 22.8%, aided by better lead distance, higher double-stack movement, and improved realisations ( ₹18,283 per TEU).

The domestic segment remains a margin sweet spot. While it accounts for less than a quarter of overall volumes, it delivers higher EBITDA per TEU than EXIM does. This helps Concor manage profitability even in a weak global trade environment.

Concor is upgrading infrastructure with the Dedicated Freight Corridor (DFC) set to be fully commissioned by FY26.

It already operates 63 terminals across India and is building a new multimodal logistics park in Varnama, Gujarat. Land acquisition for new terminals is underway in Jharkhand, Haryana, and UP.

Capex for FY25 is pegged at ₹650 crore, largely aimed at DFC readiness, equipment upgrades, and terminal expansion. The company is debt-free and ended FY25 with ₹2000 crore in cash on its books.

Conclusion

When foreign investors start selling, it’s worth asking why. FIIs aren’t always right, but their exit often reflects more than just short-term noise.

Whether it’s stretched valuations, earnings disappointments or shifting global capital allocations, large investors usually move for a reason.

But following them blindly has its own risks.

Stocks that FIIs exit sometimes turn out to be long-term winners for those who stay patient. The key is to understand the “why” behind the move.

Falling FII ownership is not a verdict. It is a signal. Use it to sharpen your lens, not to shut the door.

To know what’s moving the Indian stock markets today, check out the most recent share market updates here.

Investors should evaluate the company’s fundamentals, corporate governance, and valuations of the stock as key factors when conducting due diligence before making investment decisions.

Happy Investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com