When the cycle turns favourable, companies with scale, brand strength, and execution consistency tend to pull ahead, compounding value without drawing attention. The GST rate cut on vehicles has reignited demand by improving affordability.

That is where blue-chip auto names stand out.

These companies have strong market presence, brand loyalty, diverse revenue streams in the domestic and export markets, and strong balance sheets. Over time, they have shown an ability to protect margins, reinvest through cycles, and adapt to shifts in technology and regulation.

This editorial focuses on five such blue-chip auto stocks.

#1 Bajaj Auto

Bajaj Auto is a diversified automotive company engaged in the design, manufacturing, and sale of 2-wheelers (2W), electric vehicles (EV), and 3-wheelers (3W). The company targets the 125 cc-plus and 150 cc-plus segments.

Bajaj Auto has also acquired a controlling stake in struggling brand KTM, increasing its stake to nearly 75%. It manufactures KTM bikes in India for both domestic sales and exports to markets such as Austria. It’s currently driving a turnaround plan for KTM AG.

From a financial perspective, revenue increased 19% year-on-year (YoY) to ₹15,220 crore, crossing the ₹15,000 crore quarterly revenue milestone for the first time.

Bajaj’s volume growth was lower than the industry’s (15-17%) in Q3 FY26. Ebitda increased 22% to a record ₹3,160 crore, while margins expanded to 20.8%. Profit after tax (PAT) grew 21% to ₹2.540 crore.

Looking ahead, the management aims to outpace industry growth in the 125 cc-plus and 150 cc-plus segments. Bajaj has outlined a strategy to regain market share, especially in the 150 cc-plus segment.

The company acknowledged a product lifecycle “asymmetry,” noting that competitors offer newer products in the premium segments. To correct this, Bajaj launched seven product interventions (upgrades and refreshes) between November and January. This will be followed by eight more over the next four months.

In the 125 cc-plus category, the management confirmed plans for a new brand in the 125 cc segment and for potential expansion of the Dominar portfolio, while also exploring new formats such as off-road bikes.

In the geographic mix, the export business is expected to be robust. In the top 30 overseas markets (accounting for 75% of the industry) are expected to see Bajaj’s market share increase.

A significant focus for 2026 will be the operational turnaround of KTM AG (Austria), which will be fully consolidated into Bajaj Auto’s results on a line-by-line basis starting FY27.

The E2W business hit EBITDA breakeven, and the overall EV portfolio now delivers double-digit EBITDA margins.

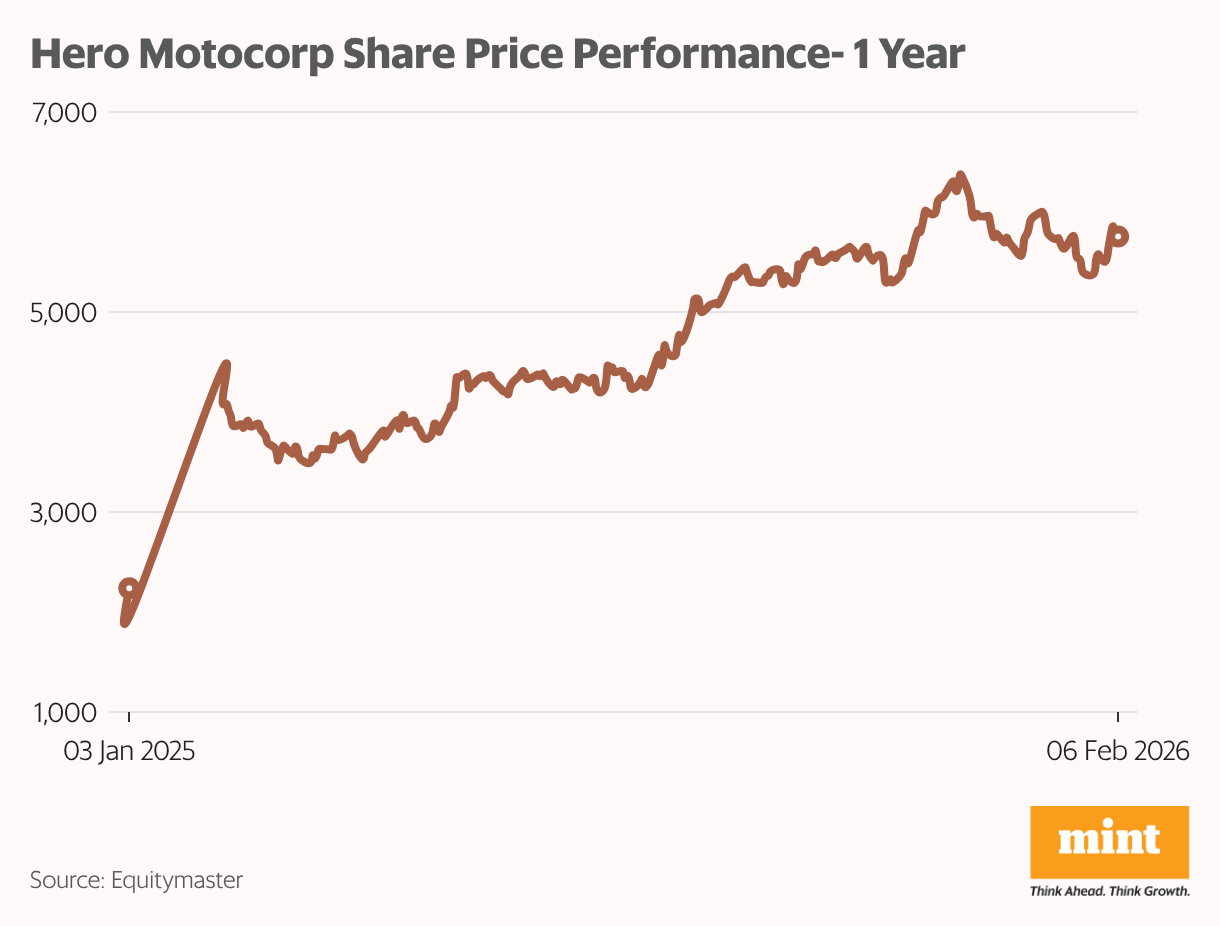

#2 Hero MotoCorp

Hero MotoCorp is the world’s largest 2-wheeler manufacturer, a title it has held for 25 consecutive years.

Under the new CEO, Harshvardhan Chitale, Hero is focusing on areas where it has historically been underrepresented but sees growth potential. These five pillars are scooters, premium motorcycles, global business, EV, and parts & accessories.

Hero is aggressively expanding its EV footprint under the VIDA brand. VIDA’s market share expanded to 10.8% in Q3 FY26, driven by the new VIDA V1 and VX2 portfolio.

VIDA reported revenue of ₹4.5 bn in Q3. The company approved an additional investment of ₹2.7 bn in Euler Motors, an electric commercial vehicle manufacturer.

In the global business, the company recently entered European markets, including Italy, Spain, and France. In Q3 FY26, export volume grew 41%, with the premium portfolio accounting for 40% of global volumes.

To capture the higher-margin segment, Hero is expanding its portfolio and retail experience for premium motorcycles. The company has expanded its 2025 Harley-Davidson lineup with models such as the H-D X440T, Road Glide, and Street Glide.

While traditionally a motorcycle-dominant player, Hero is gaining traction in scooters, with the highest Q3 market share in the 125 cc scooter segment in five years. Growth was driven by the Xoom and refreshed Destini portfolios, which now account for over 50% of scooter volumes.

The parts and accessories segment is a key revenue driver. Business revenue grew 8% in Q3 FY26 to its highest-ever quarterly revenue of ₹1,670 crore.

Overall, the management expects demand to remain strong in Q4 FY26. But Hero anticipates industry growth to moderate to high single digits in FY27.

The company’s revenue grew 21% YoY to ₹12,330 crore in Q3 FY26, driven by 16% volume growth. Ebitda rose 23% to ₹1,810 crore, while the margin was 14.7%. The net profit (excluding the impact of one-time exceptional charge due to new labour codes) increased 20% to ₹1,440 crore.

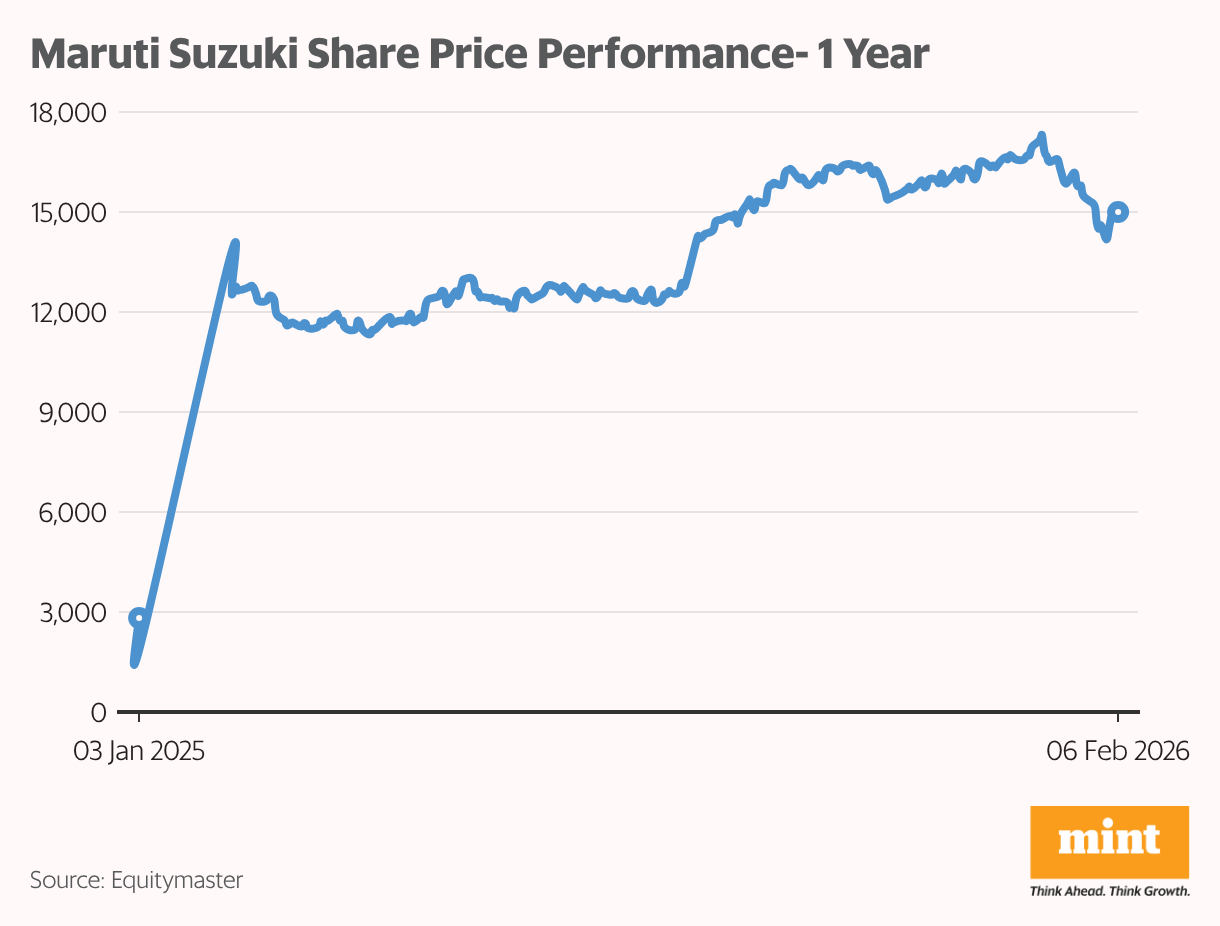

#3 Maruti Suzuki India

Maruti Suzuki’s product mix spans the passenger vehicle market, from entry-level hatchbacks to premium SUVs and EVs. It is a leader in the mass market segment.

The company has shifted its focus to the growing SUV segment, with models such as the Grand Vitara, Jimny, Fronx, Brezza, and Invicto.

Maruti has entered the EV space with the e-VITARA, its first electric vehicle. It’s already being exported to 29 countries, including the UK.

The company is currently experiencing robust demand following GST reform, which reduced taxes by 5-10%. Maruti grew faster in the domestic market, at 22%, outpacing the industry’s 20.5% growth.

The company has a healthy order book of around 175,000 vehicles. Inventory is at an all-time low of just three-four days. The company is currently supply-constrained rather than demand-constrained.

The management remains cautious about the long-term sustainability of this growth once the initial euphoria of the tax cuts settles.

To meet the surging demand, Maruti is aggressively expanding its production capacity. A second plant at the Kharkhoda facility is scheduled to be operational by April 2026.

A fourth production line at the existing Gujarat facility is being commissioned. Each of these new lines will add 250,000 vehicles annually.

From a financial standpoint, revenue increased 28.7% YoY to ₹49,900 crore in Q3 FY26, driven by 17.9% volume growth.

The mini segment saw significant recovery with 27.9% growth, and compact cars grew 25%. UVs (SUVs) continued to perform strongly, with 20.8% growth.

Operating Ebitda grew 10% to ₹5,570 crore, while margins stood at 11.7%, down 210 bps. Higher commodity prices, a one-time provision, and price reduction on some models impacted margins.

As a result, net profit rose 3.7% to ₹3,790 crore, weighed down by a one-time provision of ₹590 crore due to the new labour code.

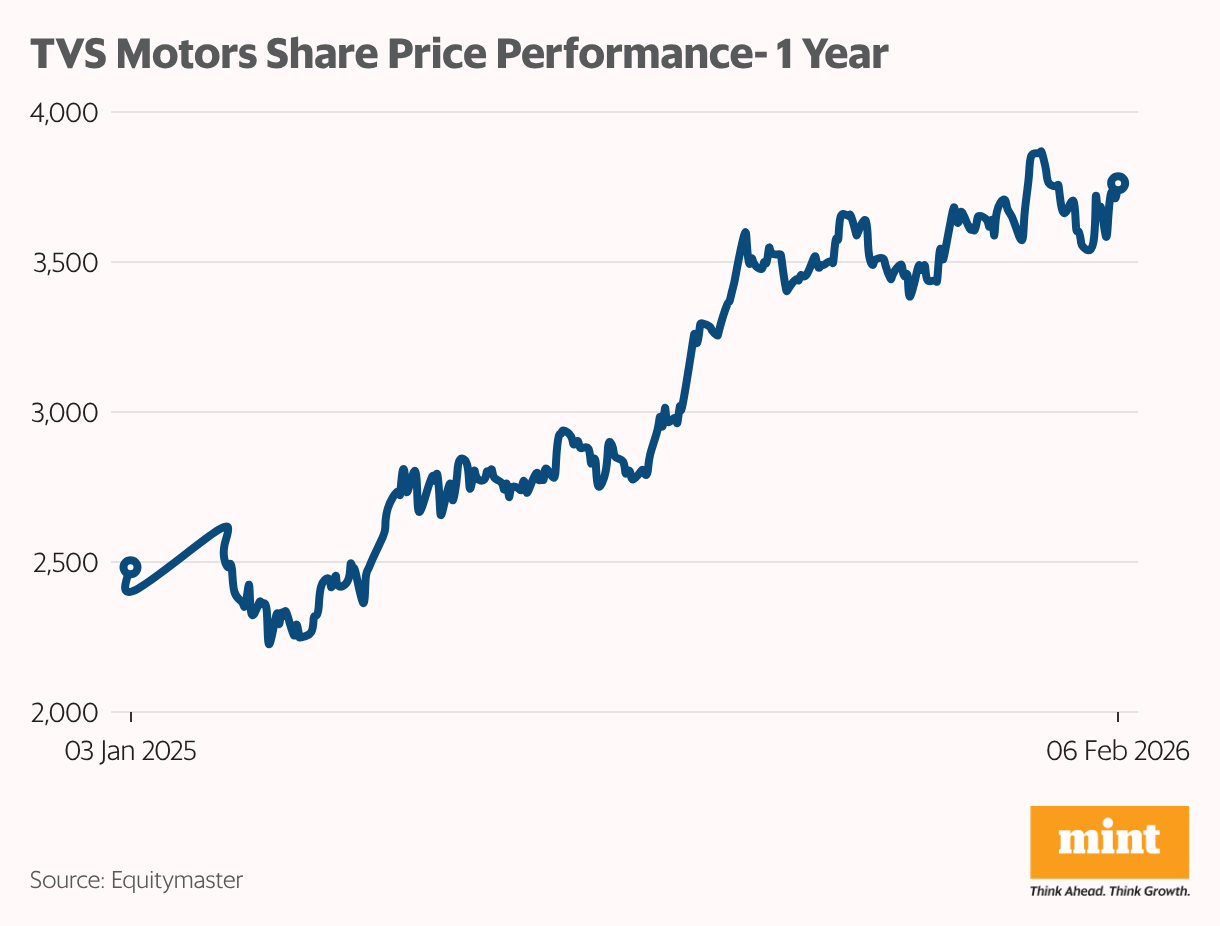

#4 TVS Motor

TVS Motors, part of the TVS Group, is India’s leading manufacturer of 2W/3W vehicles. Its portfolio also includes Norton Motorcycles (UK) and TVS Ebike Company AG in Switzerland.

Revenue rose 37% YoY to ₹12,480 crore in Q3 FY26, driven by a 27% increase in sales volume and outperformance across multiple categories.

Domestic ICE 2W sales grew 21%, outpacing the industry growth of 16%. Export business exports grew 35%, outperforming the industry export growth of 23%.

Total ICE 2W sales grew 25%, compared to industry growth of 17%. EV sales grew 40%, reaching 106,000 units compared to 76,000 units in Q3 of the previous year.

With operating leverage, operating Ebitda grew 51% to ₹1,640 crore, while margins expanded 120 basis points (bps) to 13.1%. As a result, the net profit increased 51% to ₹940 crore.

Looking ahead, the company expects the two-wheeler industry to grow by more than 15% in Q4 and to outpace broader industry growth. This follows a strong Q3, during which the industry grew 20% following the GST reduction, which has positively impacted demand.

TVS’ growth is expected to be driven by strong demand for its products in the domestic and export markets. In the international market, Africa and Latin America continue to grow, while Sri Lanka is recovering. The European market may take a few more quarters for performance to improve.

The positive momentum could continue in the first half of FY27 as the benefits of GST reduction fully permeate the market.

The company is focused on scaling up its EV business and achieving profitability in this segment. The management is confident the EV business will be Ebitda positive as volumes grow and margins improve.

The company has also revised the investment guidance upwards to ₹2,900 crore. It’s investing in capacity expansion to meet demand for the iQube and to ramp up production of the TVS Orbiter.

The company is also preparing to launch new Norton products (Manx and Atlas families) in 2026. These products target the super-premium luxury segment, with a differentiated strategy planned for India.

#5 Tata Motors Passenger Vehicles

Tata Motors, part of the Tata Group, is a leading global automobile company. It sells PVs, UVs, and CVs in about 125 countries. It also has a presence in the premium PV market via Jaguar Land Rover (JLR).

It leads the CV segment in India and ranks third in the PV segment. Moreover, it dominates the electric vehicle (EV) segment, holding a 46.3% market share as of December 2025.

Tata Motors expects to outperform the industry, targeting mid-teens growth for FY26.

The Sierra is a primary volume driver, having secured over 70,000 bookings on its first day. Production is being ramped up to meet this demand.

Other growth levers include the Punch facelift, the introduction of petrol variants for Harrier and Safari, and a re-entry into the fleet segment.

The pain in the JLR business continues to persist. Following the cyber incident that significantly impacted Q3, production at key plants (Solihull and Nitra) has fully normalised.

The management expects Q4 FY26 production to return to normal levels with no residual issues from the cyber event. JLR is entering a significant launch phase. Deliveries are scheduled to commence this year. JLR continues to face challenges in the Chinese market.

From a financial perspective, revenue declined 25.8% YoY to ₹70,100 crore, weighed down by JLR. The India business delivered its best-ever revenue of ₹15,320 crore in Q3 FY26, up 24%.

Wholesale volumes increased 22.5%, while EV volumes grew 50%. JLR volumes, on the other hand, declined 43.4%. The Ebitda margin declined 80 bps to 7%, while the profit before tax was flat at ₹300 crore.

Bottomline

These companies illustrate how scale, brand strength, and good execution can shape outcomes across cycles in the auto sector.

Each business reflects a different approach to growth, through exports, premiumisation, electric mobility, or capacity expansion, while operating within the same evolving industry environment.

That said, the recent increase in commodity prices could act as a headwind.

Observing how large, established players navigate shifts in demand, technology, and regulations can provide insight into the broader direction of India’s auto sector.

However, instead of relying on hype, investors need to carefully analyse the company’s fundamentals, including financial performance, corporate governance practices, and growth strategies.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com