But 2025 is rewriting the script.

For the first time in over 20 years, India’s markets are being driven more by domestic conviction than foreign sentiment. Domestic institutional investors (DIIs) have officially overtaken foreign institutional investors (FIIs) in ownership across listed stocks, a watershed moment for Indian equities.

So far this year, while FIIs have pulled out ₹1.68 trillion from equities, DIIs have stepped in aggressively, investing ₹4.16 trillion.

Amid this structural shift, here are three penny stocks that quietly caught the attention of both FIIs and DIIs in the June quarter (Q1FY26).

#1 HFCL

HFCL tops the list, operating across telecommunications, defence, and systems integration.

In telecommunications, it manufactures and supplies optical fibre cables, networking products, and passive connectivity solutions. In defence, it delivers ground and coastal surveillance radars, electro-optics, electronic fuses, tactical cables, and wire harnesses.

The company also undertakes and maintains large-scale telecommunication and defence communication system integration projects.

In Q1FY26, HFCL recorded a sequential rise in institutional ownership, with DII holding increasing from 13.3% in Q4FY25 to 14%, and FII holding climbing from 6.9% to 7.8%.

The increase in institutional interest followed a fresh order announcement. In May 2025, HFCL secured a ₹1.6 billion order to supply optical fibre cables for the BharatNet Phase III Project in West Bengal. The order, placed by Tera Software, a partner in ITI’s consortium, will be executed over three years.

HFCL is also making inroads into European markets for optical fibre cables, benefiting from an exemption on anti-dumping duties. The company plans to ramp up production and sales of 5G Fixed Wireless Access equipment for both domestic and international markets.

To diversify its portfolio, HFCL is launching new products, including unlicensed band backhaul radios, switches, routers, and electronic fuses, to cater to next-generation access network demand. In addition, it is building a defence product portfolio, with the goal of generating 10–15% of total revenue from the defence segment by FY27.

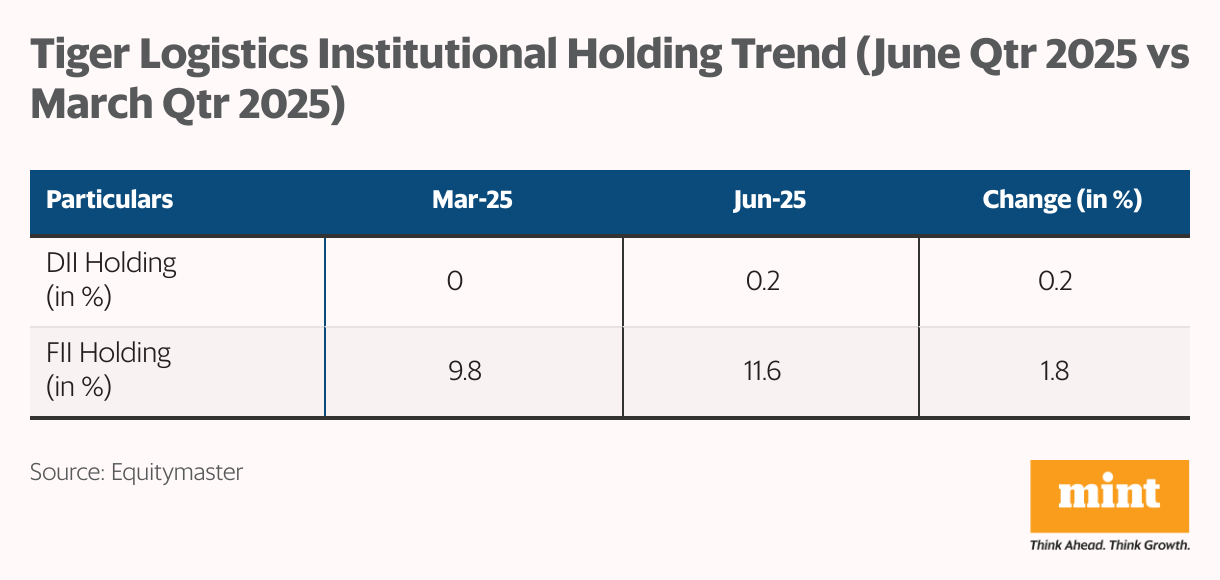

#2 Tiger Logistics

Next on the list is Tiger Logistics India, a leading international logistics company offering freight forwarding, transportation, and customs clearance solutions.

Operating on an asset-light model, the company partners with service providers to ensure timely cargo movement across the globe.

In the June quarter, both DII and FII shareholding in Tiger Logistics increased, reflecting rising institutional confidence.

As of 29 April, Tiger Logistics secured key contracts with BHEL, handling a wide range of services including customs clearance, warehousing, transportation, FCL and LCL import/export, air freight, break bulk, and over-dimensional cargo (ODC). It also won five major ODC projects from Italy for BHEL, with two heavy shipments already en route to India.

Additionally, the company emerged as the lowest bidder for a large air cargo contract with HPCL, which is expected to involve significant monthly shipment volumes.

Tiger Logistics has also applied for a direct listing on the NSE Main Board as of 16 July.

Looking ahead, the company aims to expand its footprint and strengthen its market share in India’s fast-growing logistics sector.

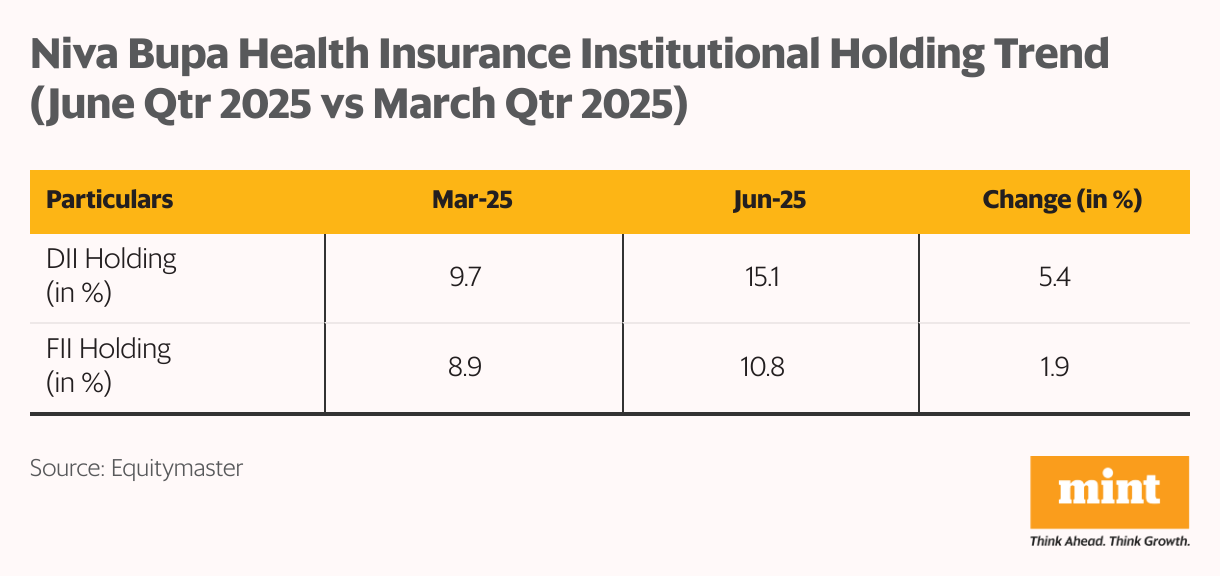

#3 Niva Bupa Health Insurance

Rounding out the list is Niva Bupa Health Insurance, founded in 2008 as a joint venture between Bupa Group and Fettle Tone LLP.

Backed by Bupa’s six decades of healthcare expertise and a global customer base of 29 million across 190 countries, the company has built a strong reputation in India’s health insurance space.

In the June 2025 quarter, Niva Bupa saw a sharp uptick in institutional interest. DII holding surged from 9.7% to 15.1%, while FII holding climbed from 8.9% to 10.8%.

The optimism stems from its robust financial performance. In Q4 FY25, Gross Written Premium (GWP) stood at ₹23.9 billion, up 36% YoY, while net profit rose 31.2% YoY to ₹2.1 billion. For FY25 as a whole, GWP grew 32% YoY to ₹74.07 billion, and profit after tax more than doubled to ₹2.1 billion from ₹820 million in FY24.

The company also inched up its retail health market share from 9.1% in FY24 to 9.4% in FY25.

Looking ahead, management plans to strengthen brand differentiation, accelerate digital transformation, and expand distribution channels to deepen market penetration.

Conclusion

A rise in both FII and DII stake can indicate institutional confidence, but it’s not an investment green light on its own.

Institutional investors have deeper access to data, sophisticated risk management, and a long-term horizon. Retail investors should evaluate fundamentals, corporate governance, and valuations before making any move.

As always, do your own homework before following the big money.

Happy Investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com