At its core, this reflects a steady rise in per-capita income, which has increased discretionary spending. As a result, consumers are increasingly moving towards more expensive products with stronger brand recall.

While premium products can help companies achieve faster revenue growth, the greater benefit is seen in profitability. Higher realizations and better product mix boost companies’ margins, leading to faster bottom-line growth than revenue growth.

This shift in consumption behaviour is also reshaping the Indian spirits industry. Premiumisation in this segment is supported by structural factors such as rising affluence, evolving consumer preferences, greater exposure to global drinking trends, and a gradual expansion in the legal drinking population.

Together, these elements are nudging demand away from mass segments toward the prestige and above (P&A) category. In fact, P&A is growing faster than the overall market and the mass category.

Radico Khaitan has emerged as one of the first companies to move towards premium products. This repositioning is reflected in the nearly 600% rise in its stock price over the past five years. Now, the main question is: how is Radico positioned to continue surfing the premiumization wave?

Diversified portfolio built for premium-led growth

Radico has a well-diversified brand portfolio across the Indian-made-foreign-liquor (IMFL) segment, which spans whisky, brandy, rum, gin and vodka. Notably, IMFL value growth is expected to increase at a 11.2% compound annual growth rate (CAGR) during 2024-2029, outpacing volume growth of 8.4%. It has built this portfolio largely organically, with no major acquisitions, and now has eight brands that have crossed sales of one million cases a year.

This category includes brands such as After Dark whisky, which sold 1.9 million cases in FY25; Magic Moments vodka (7 million), Morpheus brandy, Ola Admiral brandy, and others. Together, this range provides scale in the premium segment, offering consumers a natural pathway to higher-priced offerings.

Luxury and semi-luxury brands anchor ‘Indi-Lux’ ambition

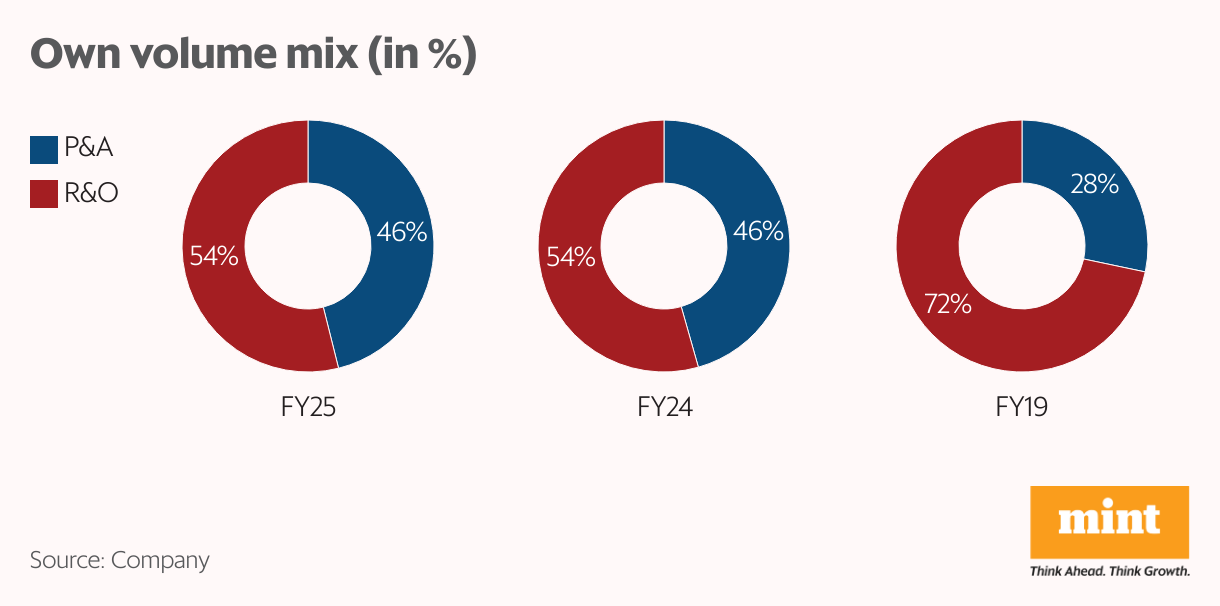

The P&A segment is central to Radico’s premiumisation strategy and includes luxury, semi-luxury, and super-premium offerings across spirit categories. The impact of this strategy is visible in the operating data. P&A brands have grown at a CAGR of 13% since FY19, and in FY25 accounted for 46.1% of Radico’s total volume, up from 28.3% in FY19.

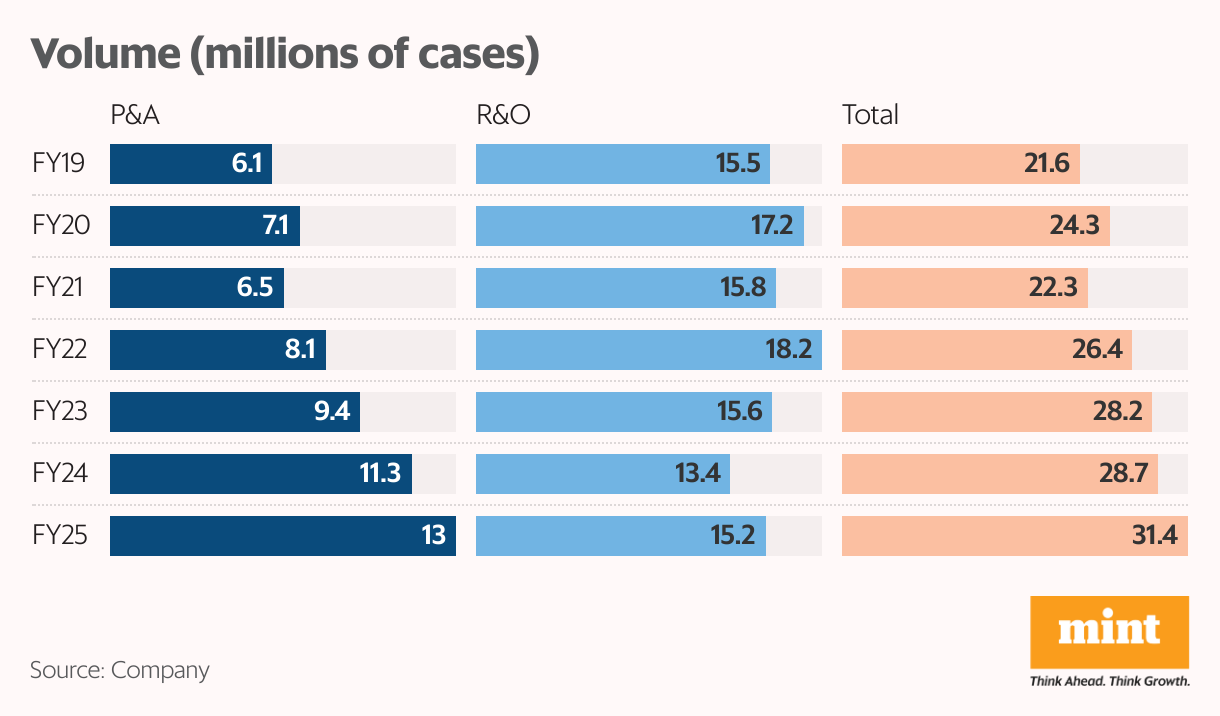

Over the same period, the share of regular and others (R&A) has declined steadily. This shift played out clearly in volume terms. P&A volumes have more than doubled, rising from 6.1 million cases to 13 million, while R&O volumes remained largely flat around 15.2 million. The shift was even more visible in value terms.

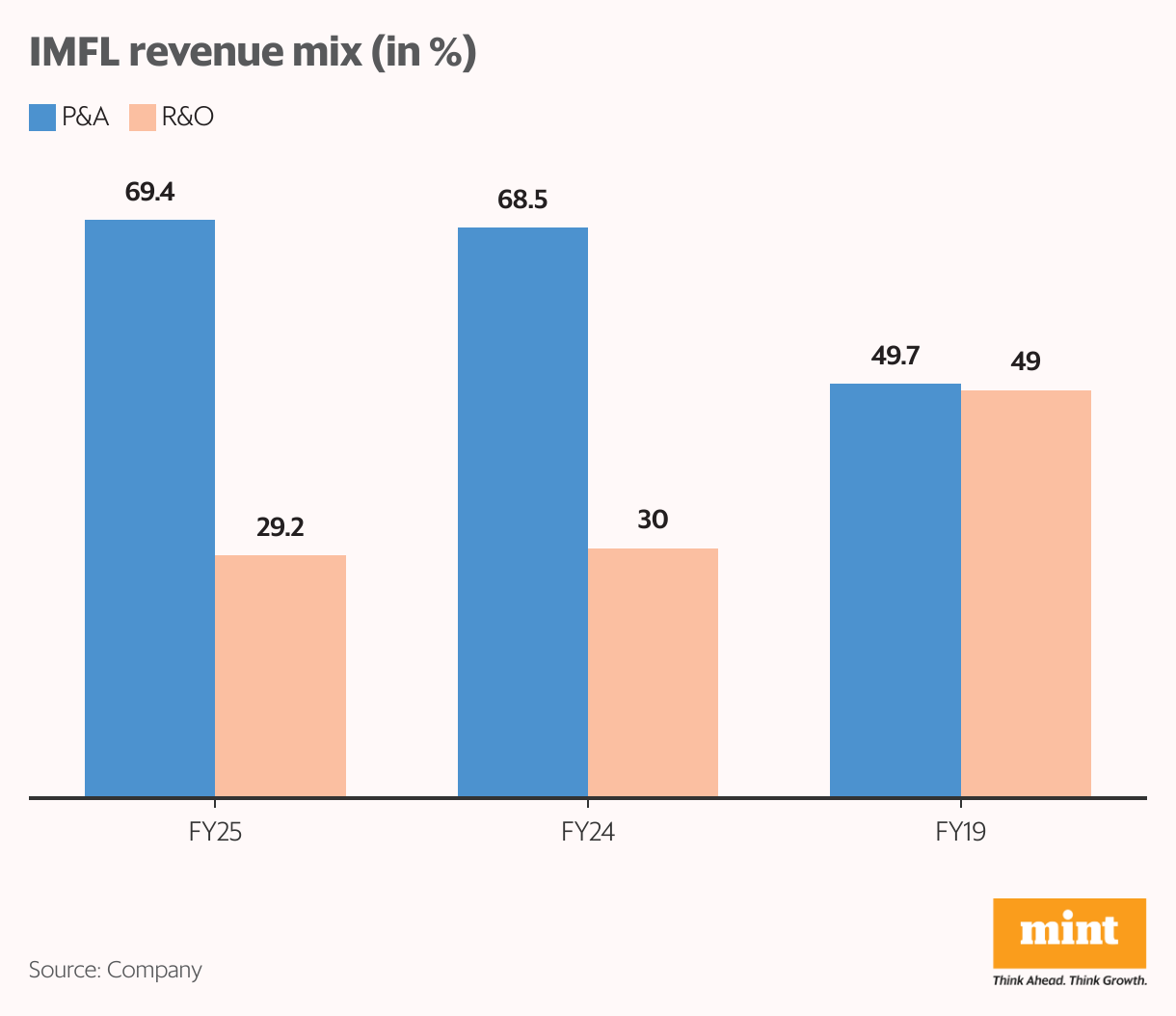

P&A brands contributed 69.4% of IMFL sales value in FY25, up from about 49.7% in FY19.

Within the P&A portfolio, luxury and semi-luxury brands accounted for about ₹340 crore, or nearly 10%, of overall IMFL sales of ₹3,371 crore in FY25. This contribution is expected to increase further to ₹500 crore by FY26.

Rampur Indian Single Malt Whisky, launched in 2017, is the cornerstone of its luxury portfolio. Other brands include Jaisalmer Indian Craft Gin, The Kohinoor Reserve Indian Dark Rum, and Royal Ranthambore Heritage Collective Whisky.

The premium and super-premium categories include both established leaders and fast-rising brands such as Magic Moments vodka, which commands a 60% market share of the Indian vodka market across segments. Globally, it ranks sixth among vodka brands. Another brand, Morpheus Brandy, is the fourth-fastest-growing and 10th-largest brandy, holding more than 60% of India’s premium brandy market.

This portfolio is anchored in its ‘Indi-Lux’ vision, which seeks to position Indian spirits on the global stage. The company exports to more than 100 countries, with exports accounting for 9% of revenue in FY25.

Realisation-led growth strengthens margins and cash flows

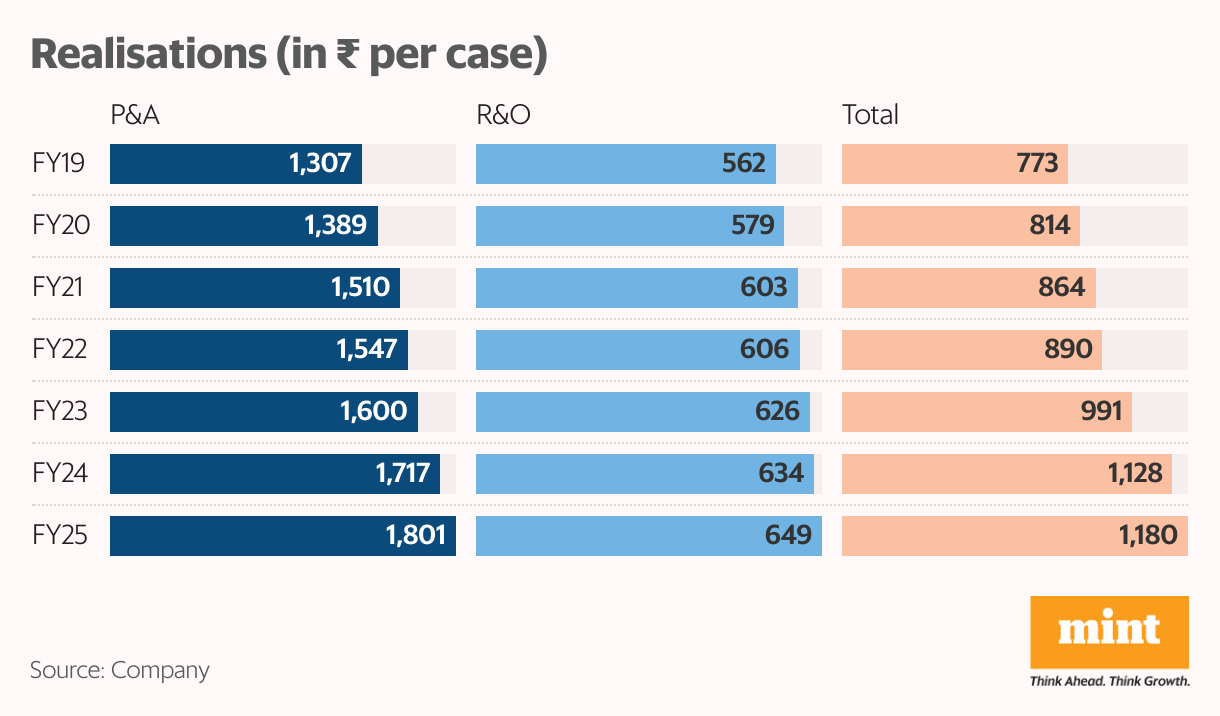

Overall, the P&A segment has emerged as Radico’s primary value driver and has consistently outperformed the broader IMFL industry. This outperformance is clearly reflected in the company’s improving product mix and sustained realisation gains. Over FY19-25, P&A realisations (per case) increased by 38%, from ₹1,307 to ₹1,801.

In contrast, realisations in the R&O segment grew at a much slower pace, increasing by about 22% to ₹649. Despite this divergence, Radico’s overall realisation improved meaningfully, rising 53% over the same period to ₹1,180, underscoring the growing product mix towards premium products. Management is highly confident it can sustain this growth rate.

Premium growth sets the stage for operating leverage

Radico’s core strategy remains focused on the P&A category, where the company is confident of strong double-digit growth. It also aims to sustain operational efficiency, maximize plant throughput, and translate these gains into margin expansion and strong cash flows. It plans to use this cash to pare its debt ( ₹631 crore in FY25) and aims to become debt-free by FY27, thereby improving future profitability. Its debt-to-equity ratio stands at 0.23.

Radico, a major importer of bulk Scotch for blending, also is expected to benefit from reduced import duties under the UK-India Free Trade Agreement. Management believes any reduction in duties will lead to significant cost savings and improved margins. The company expects the Ebitda margin – which was 13.8% in FY25 – to expand by 150 basis points (bps) in FY26, and 125 bps each in FY27 and FY28.

Volume growth and mix improvement lift profitability

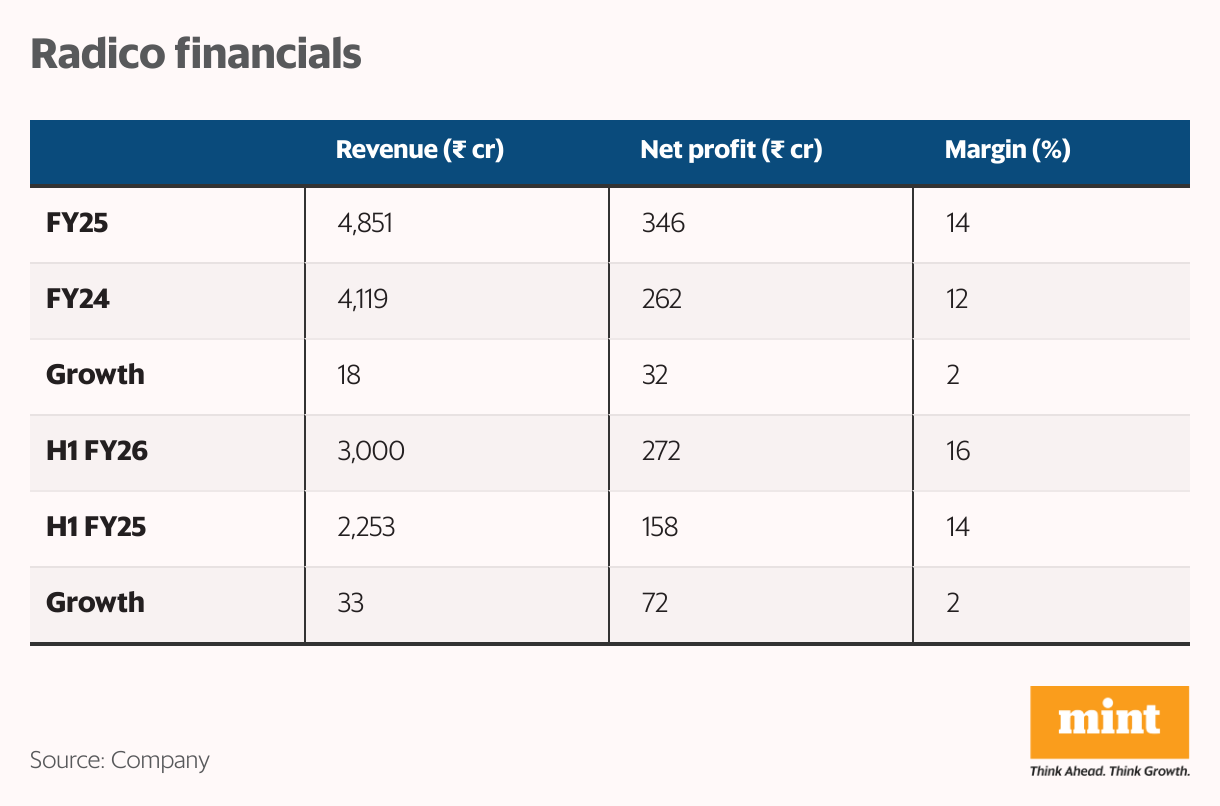

Radico’s revenue increased 17.8% year-on-year to ₹4,851 crore in FY25, supported by a 9.2% increase in total sales volume to about 31.4 million cases. Growth was led by the P&A segment, where volumes increased 15.5%, while R&O volumes grew 13.3%. IMFL revenue increased 19.5% to ₹3,371 crore, accounting for nearly 69.5% of total revenue.

Improving the mix and operating leverage drove strong profitability growth. Ebitda margin expanded by 150 bps to 13.8% in FY25, translating into a 32.1% rise in net profit to ₹346 crore. The momentum extended into the first half of FY26, with revenue rising 33.2% year-on-year to ₹3,000 crore, largely driven by a 48% increase in volumes.

While P&A volumes maintained strong momentum with 30.5% growth, R&O volumes also rose by 64%. The acceleration in the R&O segment was primarily due to route-to-market changes in Andhra Pradesh, where Radico’s market share expanded from about 10% to 30%. With operating leverage playing out, Ebitda margin expanded by a further 180 bps to 15.6% in H1 FY26, resulting in a 72.2% increase in net profit to ₹272 crore.

After a sharp re-rating to ₹3,224 per share, Radico is trading at a price-to-earnings ratio of 93, higher than the five-year median of 78. It now trades at a premium to United Spirits (P/E: 61) but at a discount to United Breweries (115). Radico’s premium valuation leaves limited room for error. Consistent execution and sustained, premiumisation-led earnings growth, therefore, remain the key variables to track.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.