But here’s the kicker. It still trades at a price to earnings (PE) ratio of 73. So, what are investors seeing in the company?

Well, it’s not just the advertising story. There is an artificial intelligence (AI) story underneath. Investors are betting that Affle isn’t just another ad-tech player but a ‘tech-first company’ using AI to reshape how digital ads work. This narrative, combined with actual profitability and growth, has kept investors interested.

What Does Affle India do?

At its core, Affle is an ad tech company. It helps brands show the right ad to the right person at the right time, mostly on mobile apps.

Think of it as the behind-the-scenes tech that decides which Swiggy or Samsung ad pops up when you’re playing Ludo or Woody on your phone.

Affle gets paid only when the ad works. That means when someone actually clicks, signs up, or buys something. They call this ‘cost per converted user’, or CPCU. This is not your traditional digital advertising where you pay for impressions or clicks. Here, advertisers pay only when there is a meaningful action.

That keeps Affle on its toes. It needs to deliver real conversions to earn its revenue. The smarter the targeting, the better the conversion, and the more they earn. This is why machine learning and AI are so central to the business.

The role of AI

Affle’s business runs on data. It reads your app habits – what you open, how long you stay, what you ignore.

Then it trains its AI systems to predict what you might do next: Which ad will get your attention? Which product will make you tap?

It’s all calculated.

And here’s where Affle’s trying to stand out. While the world is going cookie-less and privacy rules are being tightened, Affle claims it uses contextual data. This is data from within apps, not from tracking you across the web.

That means it isn’t reliant on third-party cookies, which browsers and platforms like Apple and Google are phasing out.

Instead, it watches what you’re doing inside the app itself and uses that as its signal.

This could be the company’s moat. At a time when many ad-tech platforms are struggling to adapt, Affle’s model may have found a more sustainable path.

Recent rebranding and more

In April 2025, Affle renamed itself “Affle 3i Limited.” This wasn’t just a simple rebranding. It has outlined an ambitious roadmap for the next decade.

The company wants to grow annual consumer conversions tenfold, from 400 m to 4 bn, expand its reach to 10 bn devices, and deliver over 1 bn personalised ads for more than 1 m advertisers.

At the heart of this strategy is Opticks AI, Affle’s in-house tool. It can produce hyper-personalised, localised ads using just a logo, a product image. and a simple prompt.

It can tailor ads to geography, language, and user behaviour, making it feel native and not generic.

The company says it can already churn out over a billion such ads. And for now, it’s not charging for them. Instead, it sticks to its cost-per-converted-user model.

The edge is in its dataset. Years of data across apps and markets give Affle a unique advantage that helps it craft ads that gets clicks.

The company is bringing India’s small businesses online. Of the 60 m SMEs in the country, only a handful use digital advertising.

As connected TV adoption surges, especially in smaller towns, Affle wants to help local businesses launch geo-tagged, bite-sized ad campaigns.

It’s also aiming for scale without adding headcount. The company will augment its 650 employees with 100 AI agents trained on its own data. These agents will support everything from investor relations to campaign analysis. It’s not just about cutting costs. It’s about building an AI workforce into the core of its operations.

The company is backing this with intellectual property. It has filed 15 new AI patents, taking its total to 36. These include human-like AI agents, privacy-first targeting, fraud detection, and content generation. Affle wants to move up the value chain from being a data-driven ad player to an AI-led platform.

In a market dominated by the likes of Google and Meta, the company knows it can’t compete on scale. But it’s betting it can compete on depth—through personalisation, localisation, and contextual intelligence.

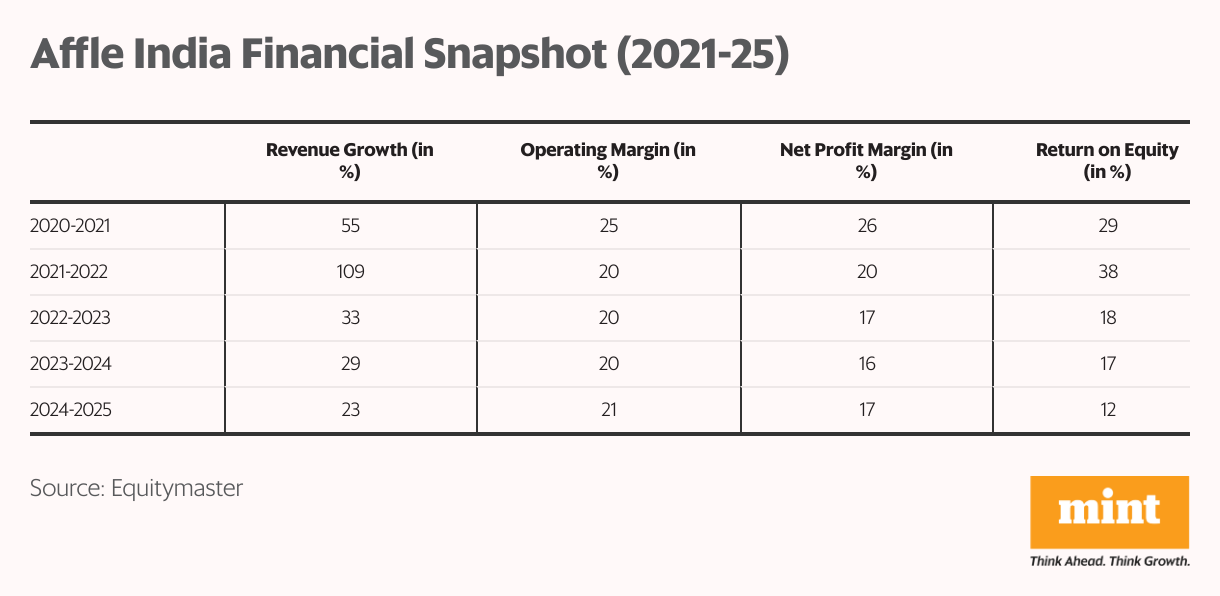

Financial performance

For all the AI talk, is the business delivering? In the past five years revenue has increased as compound annual growth rate (CAGR) of 49%.

Net profit jumped from ₹103 crore in FY21 to ₹382 crore in FY25, clocking a CAGR around 40%.

Margins are holding strong. The company recorded a 21.3% Ebitra margin and 16.2% net margin in FY25. Cash flow from operations was ₹426 crore in FY25, up 62% year-on-year.

The average return on capital employed is 23.6% and return on equity is 22% over the past five years. While not close to tech stocks that generate high returns, these are relatively healthy numbers for a tech company that’s still scaling.

Affle closed Q4 FY25 on a steady note, with revenue up 19% year-on-year and Ebitda growth of 37% driven by better operating efficiency. Margins expanded to 22.2%, reflecting improved cost control and stronger monetisation. Profit growth stood at 18%.

What stood out, though, was the rising share of conversions from developed markets, pointing to a more global, diversified growth path taking shape.

Diversified growth

Affle’s growth isn’t coming only from India. Developed markets now make up 29% of revenue, and they’re growing faster, up 27% year-on-year in Q4FY25, compared to 16% growth in India and other emerging markets.

This isn’t surprising. Developed markets tend to have higher digital ad spends per user. Its clients include Samsung, Swiggy, Tata Neu, Byju’s, Apollo, McDonald’s. And most of the money still comes from CPCU.

In FY25, Affle recorded 392 million conversions at an average CPCU of ₹57.5. That brought in ₹2,260 crore of revenue.

The CPCU model can scale well. As long as ad budgets grow and mobile engagement continues, Affle can expand without needing massive capex. This gives the business a level of predictability and visibility. As long as engagement and conversion ratios stay healthy, the business model remains resilient.

What could go wrong?

Let’s be frank. This is not a risk-free business. Privacy rules are being tightened globally. If countries tighten data laws further, Affle’s job becomes harder. Even contextual data could come under scrutiny, especially if laws evolve faster than tech.

Then there’s competitive pressure. Affle is a tiny fish in an ocean filled the likes of Google and Meta. If they decide to focus on Affle’s turf, things could get uncomfortable. And newer AI-first ad-tech platforms are coming up globally.

Also, the company has grown in part by buying smaller companies and integrating them. If any of those deals go wrong, it could hurt margins or slow growth.

Then there’s the AI risk.

While AI is central to Affle’s growth story, it also brings new challenges. If adoption moves quickly beyond mobile, or if newer platforms start delivering better conversions at lower cost, Affle’s moat could come under pressure.

If the AI tools that power its growth could become widely available, it could lose its edge of differentiation.

For now, the company believes these shifts will take time. And it’s already preparing for a world where authenticated AI agents, not just humans, drive purchasing decisions.

Valuation

Affle is valued at ₹27,900 crore today, or 73 times trailing earnings. This is a premium to its five-year median PE of 67. At its peak valuation, the stock was trading at a PE of 162 in June 2021.

Investors need to ask whether the current valuation already prices in too much AI upside. If growth slows or margins compress, there may not be enough room for disappointment.

Conclusion

Affle is trying to make ads smarter, more targeted and less wasteful. It’s built a good business, stayed profitable, and has kept innovating so far. Now it’s betting on AI not just to protect its turf, but to expand it. If things go well, Affle could become India’s quiet AI success story. Not by reinventing the wheel but by making sure every ad rolls out smarter than the last.

However, it’s always important for investors to carefully analyse a company’s fundamentals, including its financial performance, corporate governance, and growth strategies before considering an investment.

Happy investing!

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such.

This article is syndicated from Equitymaster.com