A Mint analysis of more than 4,000 BSE-listed firms shows that India’s markets, even after recent corrections, look closer to premium than cheap. The debate is no longer whether stocks are undervalued, but whether India’s growth trajectory justifies the premium investors continue to pay.

Bargains or premiums?

To grasp this shift, look back to the pandemic lows. On 23 March 2020, when the Sensex hit its Covid trough, fear reigned. Nearly two-thirds of companies traded below 10x earnings. Those bargains made up about 16% of the market’s capitalization, while close to half of all equity wealth sat in stocks priced at 10-25x earnings.

At the premium end, very few companies commanded hefty multiples: Barely 5% of firms traded above 60x earnings, together making up just 9% of total market value. The rest clustered in the 40-60x range, representing about 13% of the market. For investors with conviction, bargains abounded—though fear kept many from acting.

Also read | Endgame: Crores wiped out as investors flee gaming stocks—did they see it coming?

By 26 September 2024, when the Sensex touched record highs, the composition had flipped. A staggering 26% stocks were trading above 60x earnings, accounting for 36% of total market cap. Nearly 30% of the scrips were priced between 25x and 60x, commanding 38% of market wealth. By contrast, companies valued below 10x earnings had shrunk to a meagre 7% of total capitalization.

The rally didn’t last. By March 2025, the headline index had fallen 15% from its peak, as foreign outflows, US tariff moves, and geopolitical tensions hit sentiment. Even so, bargains didn’t return. The market has since recovered 10% from that low, but still trades more than 5% below its peak. Today, 22% of companies continue to trade above 60x earnings, accounting for 28% of market wealth, while 26% sit in the 25-60x range. Deep discounts remain rare.

This persistence raises an uncomfortable question: if valuations remain structurally high, how to navigate this?

Divided debate

“India has created seven new industries in the past eight years, many of which rewarded investors handsomely,” said Manish Bhandari, founder & CEO of Vallum Capital. “The real challenge is not whether markets are cheap or expensive overall, but identifying the right pockets of value—and that’s where true wealth gets built.”

Others argue that corrections in recent months have already begun stabilizing valuations. “With the recent market consolidation and broad-based correction across sectors, valuations are recalibrating,” said Ranju Rajan, head of managed accounts at Axis Securities. “This setup is constructive for bottom-up stock picking, especially in sectors where fundamentals remain intact and near-term headwinds are priced in.”

Also read | Retail investors’ verdict: Tariffs can’t trump a good bet

A third school of thought views the “undervaluation” narrative less in absolute terms and more as a relative opportunity.

Narinder Wadhwa, MD & CEO of SKI Capital, said, “Indian valuations today—Nifty 50 at 22x earnings and nearly a quarter of companies above 60x—are clearly elevated versus Covid lows and Asian peers. Yet India’s structural growth story—world-leading GDP growth, strong institutions, favourable demographics, and policy reforms—justifies a premium. The claim of being undervalued is less about ratios and more about the runway of growth and institutional stability.”

India’s premium problem

Compared with peers, India looks expensive. The Nifty 50 trades at 22x earnings, above most of Asia. South Korea’s Kospi and Taiwan’s Taiex sit in the mid-to-high teens, while China’s CSI 300 trades even lower. Indonesia is at 15.9x and Brazil at just 8.7x. By global standards, India looks more like a developed market than an emerging one.

“On the face of it, Indian markets don’t look cheap,” said Akshat Garg, AVP at Choice Wealth. “More than a hundred companies trade above 50x earnings, and the Nifty itself is at 20-22x, compared with 12-16x for most Asian peers. By traditional yardsticks, that sounds expensive.”

But Garg argued that India’s premium is not simply about sentiment.

“The domestic economy is growing at 6–7%, with expectations of double-digit corporate earnings in coming years. A young population, rising middle class, stronger bank balance sheets, and reforms like GST, IBC and PLI are expanding the formal economy in ways few peers can match. So while valuations look stretched on paper, the undervaluation narrative comes from the belief that India’s growth premium is still underappreciated. If earnings deliver, today’s multiples may not be expensive—they may simply be the ticket to the next decade of India’s growth story,” Garg added.

Mayank Mundhra, VP at Abans Financial Services, echoed that view: “Indian stocks, while trading at higher valuations compared to pre-Covid levels and Asian peers, are still seen as undervalued from a forward-looking perspective. Some softness in earnings is visible due to global headwinds, but confidence in the long-term growth story remains strong.”

Capital shift

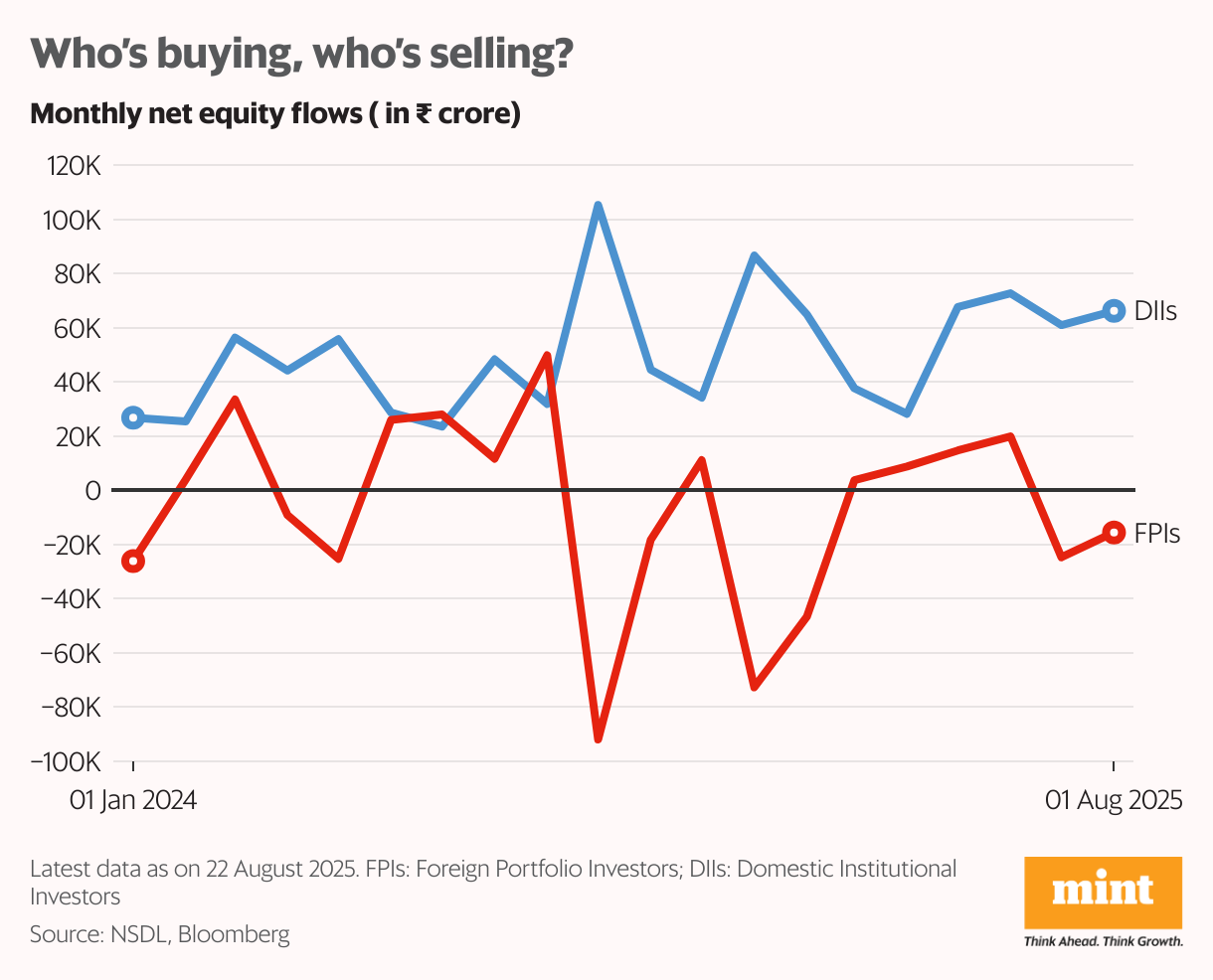

What sustains this elevated structure is not just growth expectations but also the shifting balance of capital flows. So far in calendar year 2025, foreign portfolio investors (FPIs) have sold equities worth ₹1.13 trillion. Domestic institutions (DIIs), however, have absorbed the selling, buying a massive ₹4.74 trillion. The gap is stark in monthly flows. In August alone, FIIs sold ₹15,547 crore, while DIIs bought ₹66,183 crore.

This is in sharp contrast to September 2024, when the Sensex hit record highs and both FPIs and DIIs were net buyers— ₹49,792 crore and ₹31,860 crore respectively. Since then, domestic inflows have become the market’s stabilizing force, propping up valuations despite foreign exits.

“Despite continued foreign outflows, strong domestic inflows have kept markets resilient,” said Mundhra.

Axis’s Rajan also sees opportunity in the current setup: “The consolidation around Nifty 25,000 has potential to surprise positively in the long term—once earnings gain momentum and global flows stabilize. For disciplined investors, this is a window to reposition portfolios towards selective structural winners with strong balance sheets.”