If this is confirmed, investors will be relieved. Even otherwise, the return of long-standing former managing director Rajeev Jain until March 2028 takes the edge off the bad news. Of course, he may have to pull back from his role as an advisor at Bajaj Finserv, but considering Bajaj Finance is the group’s primary business, this would be unlikely to hamper investor sentiment.

Moreover, the Q1FY26 earnings announced on Thursday inspired confidence in the business. The lending behemoth has been a consistent outperformer, having delivered a 43% compound annual growth rate (CAGR) since March 2012, against the broader industry’s modest 15%.

But is the stock finally running out of steam, or should investors hang on?

Behind the legacy

Bajaj Finance is India’s largest private non-banking financial company (NBFC). With 239,000 active distribution points across more than 4,000 locations, the lending arm of Bajaj Finserv has an almost unparalleled distribution might.

The company holds an 88.7% stake in Bajaj Housing Finance, and 100% in Bajaj Financial Securities, a broker. It has sister concerns across the industry, from vehicles to insurance, mutual funds and a digital marketplace. Thanks to the resulting cross-selling and up-selling opportunities (cross-selling constitutes 63% of the lender’s total customer franchise), it has managed to consistently deliver industry-beating numbers.

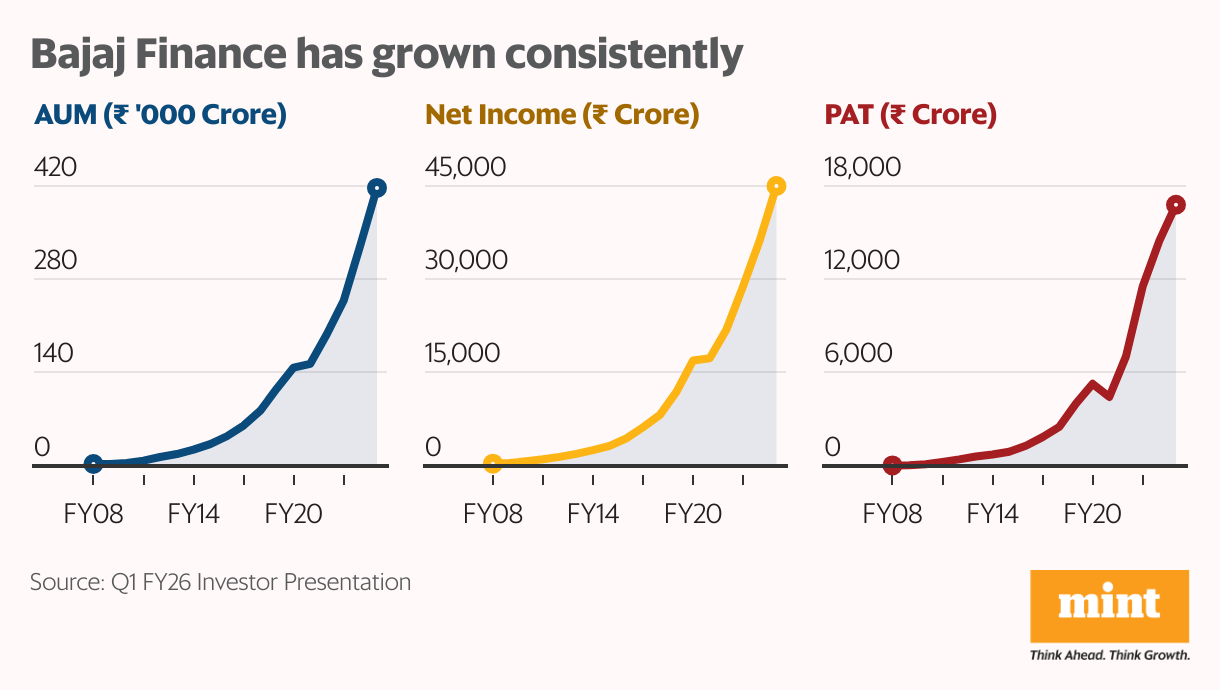

Its assets under management (AUM) was nearing ₹4.5 trillion as of June, having clocked a CAGR of 35% between FY08 and FY25. Provisioning coverage has expanded from 30% to 54% over the years, offering protection against sudden hits to the books. Meanwhile, cost efficiencies have improved, with opex-to-net-income moderating from 58% to 33%. Loan loss to assets under finance (AUF) has almost halved to 2.17%.

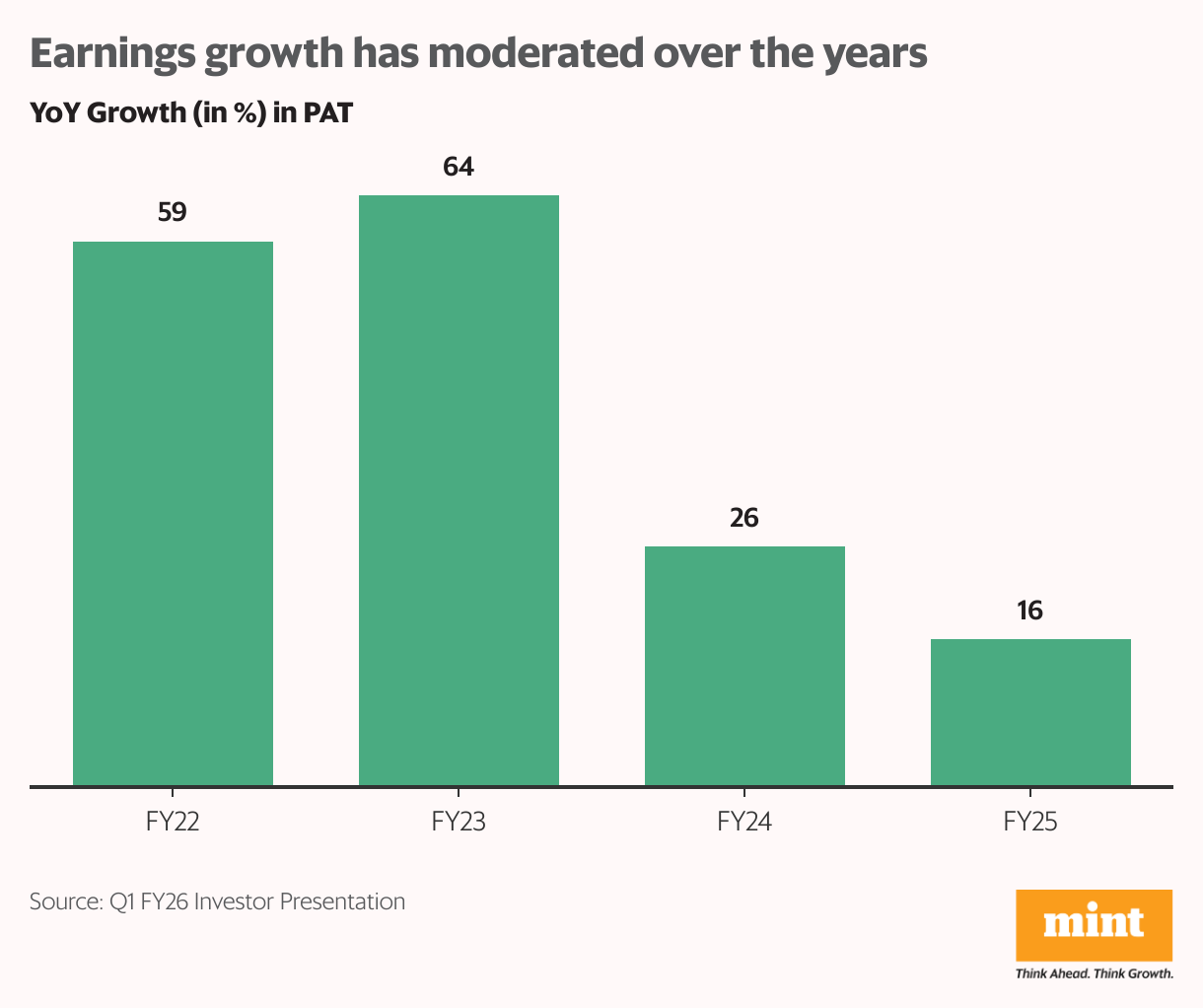

The result? Profit after tax grew at a 48% CAGR over this period, and the stock moved in tandem.

FY26 started on a strong note

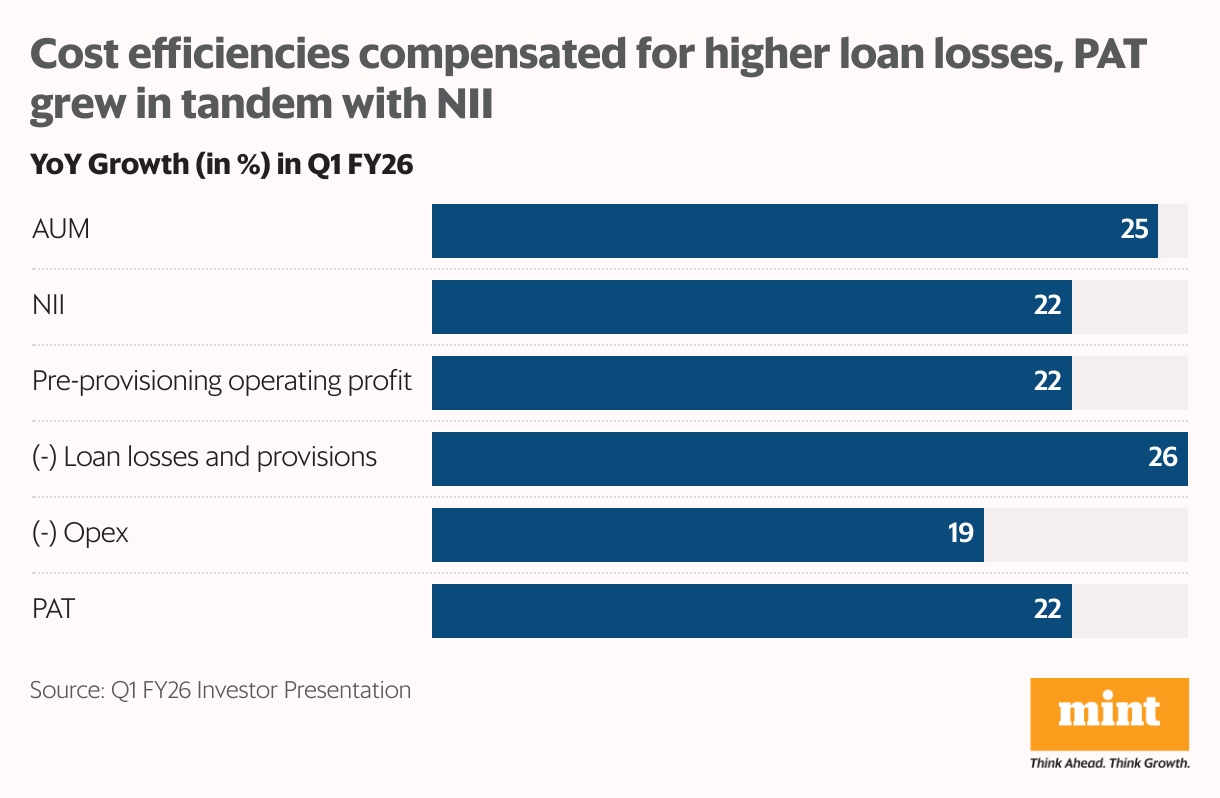

The company has kept up the momentum in FY26 as well. Building on its more than 100 million customers, the company registered 23% growth in new loan bookings. Its AUM expanded by 25% year-on-year to ₹4.4 trillion as of June 2025. Deposits also grew at a healthy 15% to ₹72,109 crore.

Amid monetary easing, despite a 20 basis points (bps) moderation in the cost of funds, net interest income (NII) grew at 22% to ₹10,227 crore, slower than AUM. Pre-provisioning operating profit matched this pace. While loan losses and provisions expanded at 26% year-on-year, operating expenses fell from 33.3% to 32.7% of net income.

As a result, PAT growth has kept up with growth in NII, up 22% to ₹4,765 crore. Bajaj Housing Finance saw PAT grow 21%, while the broking subsidiary reported bottom line growth of 37%.

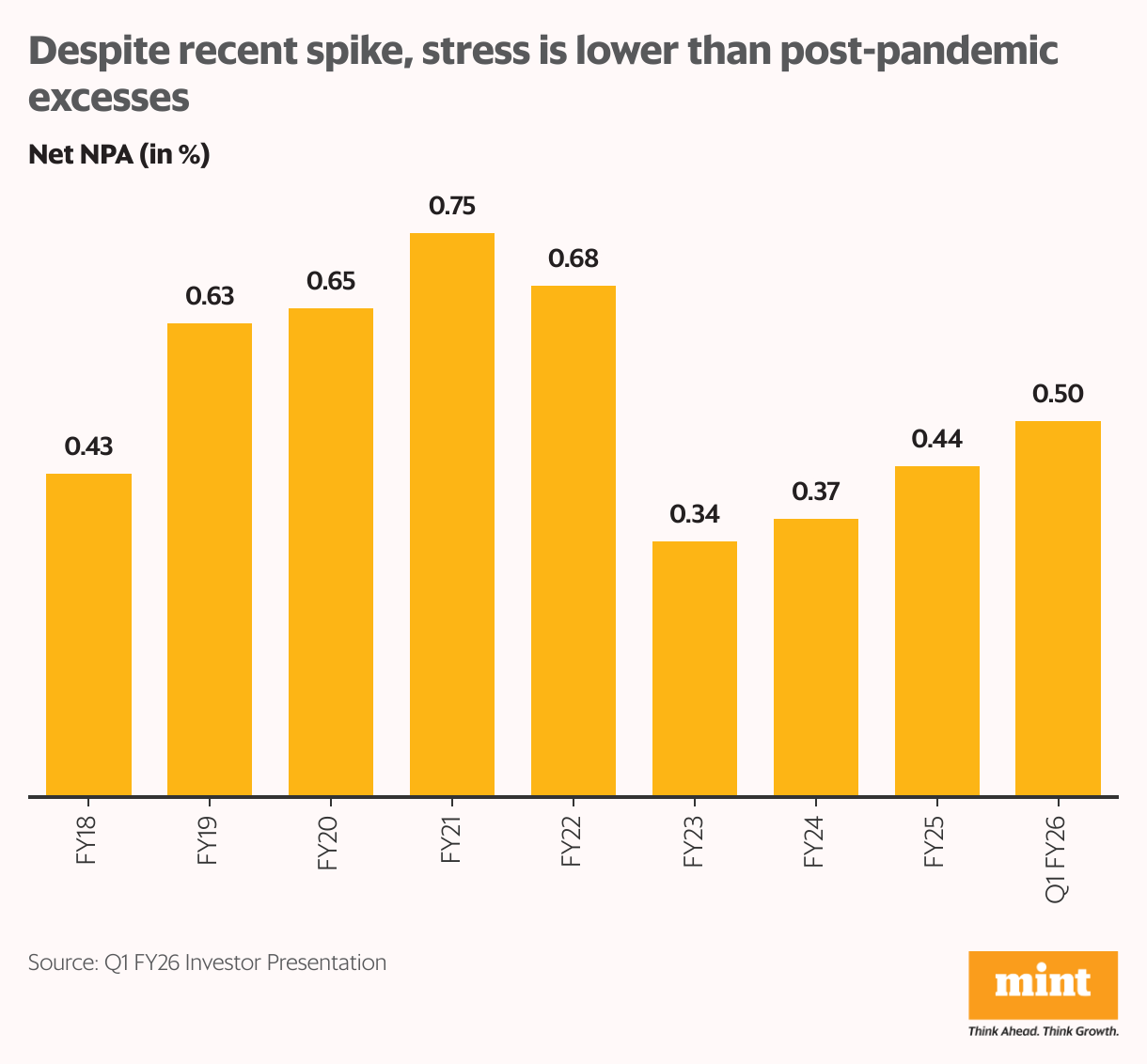

Stress is high, but hope lingers

Stress has picked up. Gross and net non-performing assets (NPAs) expanded to 1.03% and 0.5% in Q1 FY26 from 0.86% and 0.38%, respectively, a year ago. Specifically, two- and three-wheeler and MSME financing have seen significantly higher stress, with gross NPA at 6.4% and 1.8%. But the yearly trend shows an improvement from the post-pandemic excesses.

Moreover, thanks to its diversified asset mix, Bajaj Finance’s NPA levels are among the lowest in the industry. It has also been working on relieving some of the stress on its books. It has reduced its exposure to overleveraged borrowers and held back on lending to stressed segments.

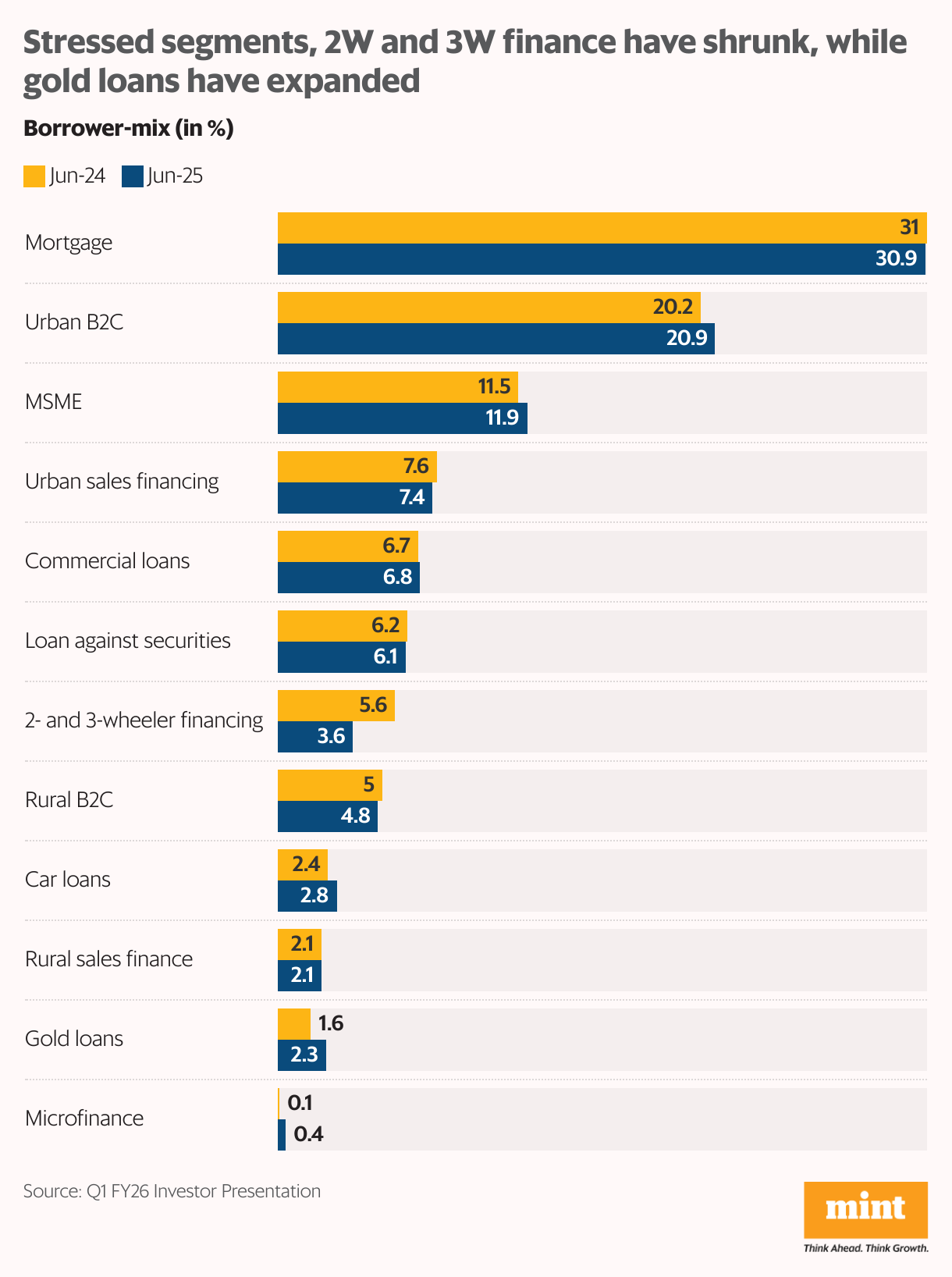

Two- and three-wheeler financing shrunk 53% and 56% year-on-year, respectively in Q1 FY26, reducing their share in the lending mix. Meanwhile, the lender has doubled down on gold loans and microfinance to pick up the slack in growth. It added 85 standalone gold loan branches and 4 microfinance branches in Q1, taking its total presence to 1,254 gold loan branches and 337 microfinance branches. In early vintages, barring MSME financing, stress in all segments has eased.

Regulatory winds blow both ways

The RBI recently allowed NBFCs to launch cards without banking partners. This blunted the edge for the likes of Bajaj Finance, which had established partnerships with RBL and DBS. On the other hand, bank credit as a source of funding has been reopened since the RBI reversed the risk weights on bank lending to NBFCs.

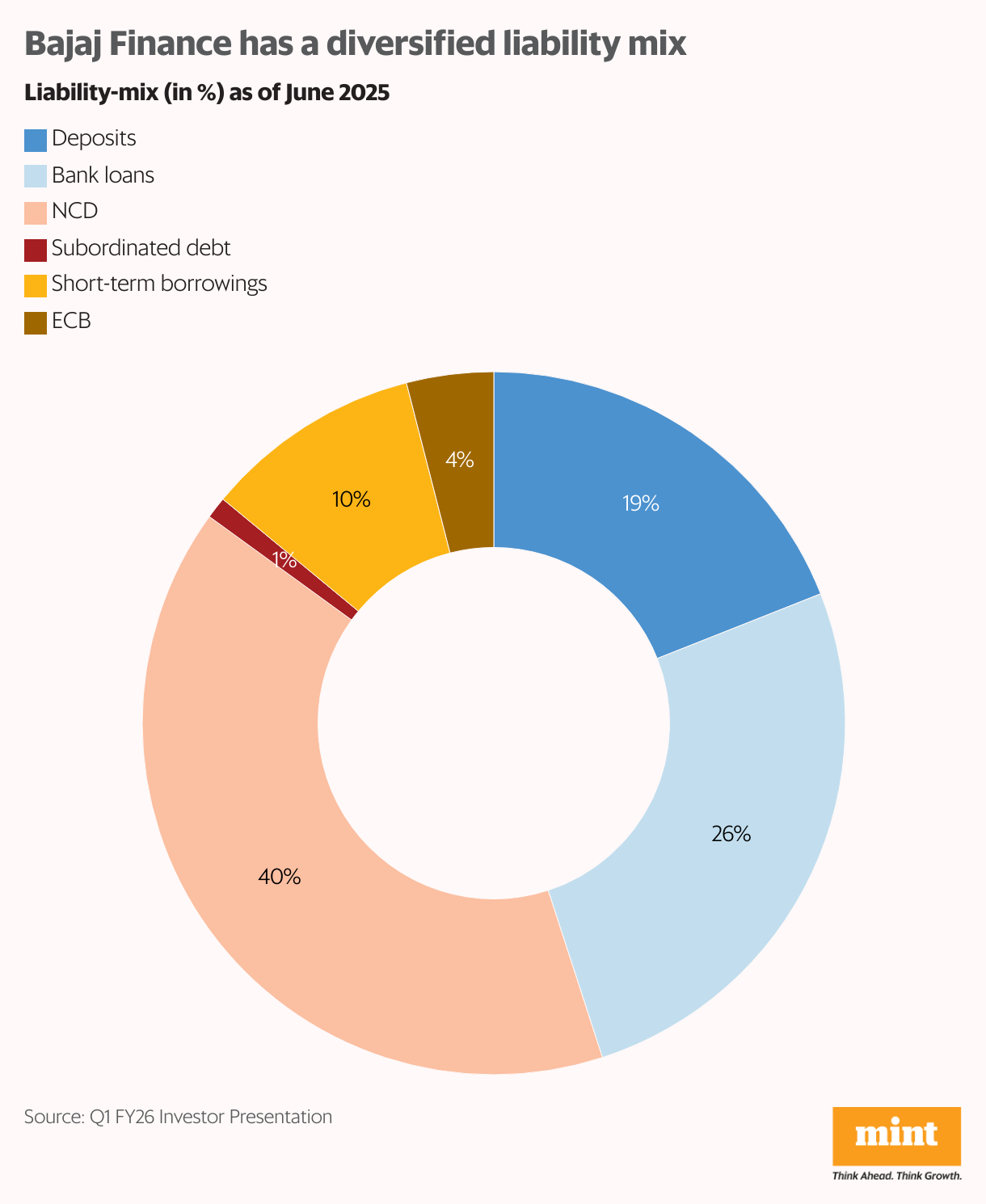

As for monetary easing, a bulk of Bajaj Finance’s lending mix is concentrated in floating-rate loans, which reprice in sync with monetary easing. This places the lender at a disadvantage compared topeers that focus on fixed-rate loans such as vehicle financing. That said, the NBFC has only 19% of its borrowing mix exposed to deposits, so it’s better placed than its banking peers, which depend primarily on sticky current account savings account (CASA) deposits.

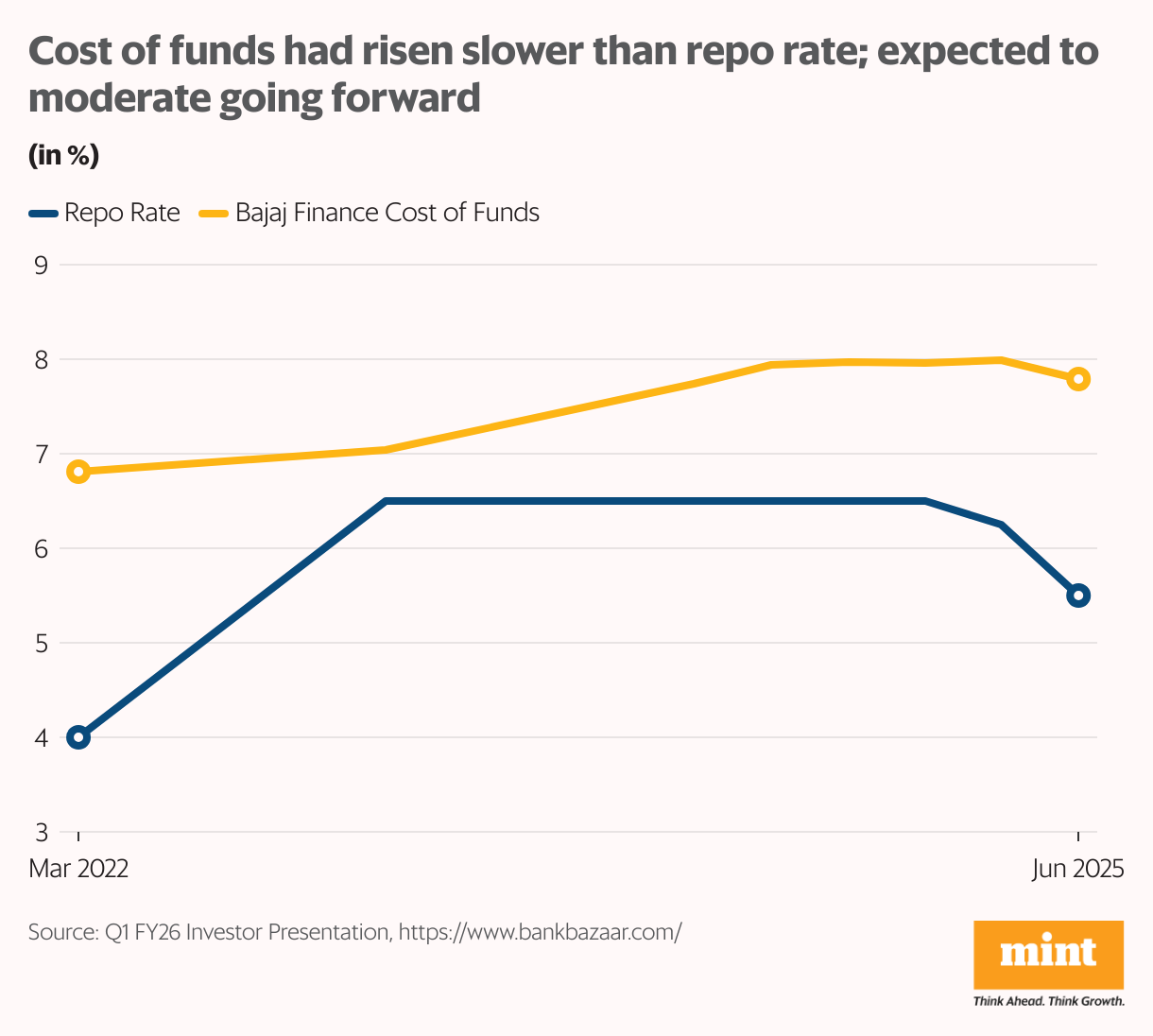

With its diversified liability mix, the lender saw its cost of funds rise from 6.8% to 8%, while the repo rate grew faster from 4% to 6.5%, between May 2022 and December 2024. As monetary easing began in 2025, Bajaj Finance’s cost of funds moderated to 7.79% by June. This is expected to trend lower at 7.60-7.65% for the full fiscal year.

Competition risk looms

The shifting of reins back to Rajeev Jain isn’t likely to threaten the lender’s prospects, considering it has around three years to firm up a succession plan. But competition poses significant risk. Fintech firms in particular have been gaining ground in personal loans. The entry of new players such as Jio Financial could make matters worse.

For Bajaj Finance, tech could prove to be a deterrent. Only 70% of its customers use its app, compared to 95% for peers. The RBI’s temporary embargo on its digital lending in FY24 exposed process gaps in the lender’s bid to accelerate digitisation. Of course, things have improved since then. The company has ddressed the regulator’s concerns and has formed a strategic partnership with Bharti Airtel to allow its customers to transact through the Airtel Thanks app.

To diversify its asset-mix amid growing competition, the lender has entered new segments including microfinance and vehicle finance. Considering their low-yielding and cyclical nature, they could weigh on its near-term margins. As the lender holds back on loans to stressed segments, revenue growth could be affected as well.

Bajaj Finance aims to add 1.4 to 1.6 crore customers this fiscal year, and clock 25-27% annual growth in its AUM over the long term. Management has guided for 23-24% growth in profits and a return on equity (ROE) of 19-21%, while keeping gross and net NPA in check at 1.2-1.4% and 0.4-0.5%, respectively. While the lender’s entry into EV financing has long-term potential, competition could play spoilsport.

Finally, the stock’s rich valuation at 33 times earnings leaves little room for any misses on growth. Brokers have pegged the target price at ₹1,000, reflecting an upside of less than 10% from the current price.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder ofCredibull Capital, a Sebi-registered investment adviser. X: @ananyaroycfa

Disclosure: The author holds shares of some of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.