Its stock has surged 120% in a matter of months – from ₹509 on 2 May to around ₹1,113 at present, reflecting investor optimism around this plan.

At the heart of this optimism is Lumax’s next mid-term plan for FY26-31, dubbed the ‘20-20-20-20 NorthStar’ strategy. The four-part goal includes minimum 20% annual revenue growth, a 20% margin, a 20% return on capital employed (RoCE), and a revenue contribution of over 20% from clean mobility solutions.

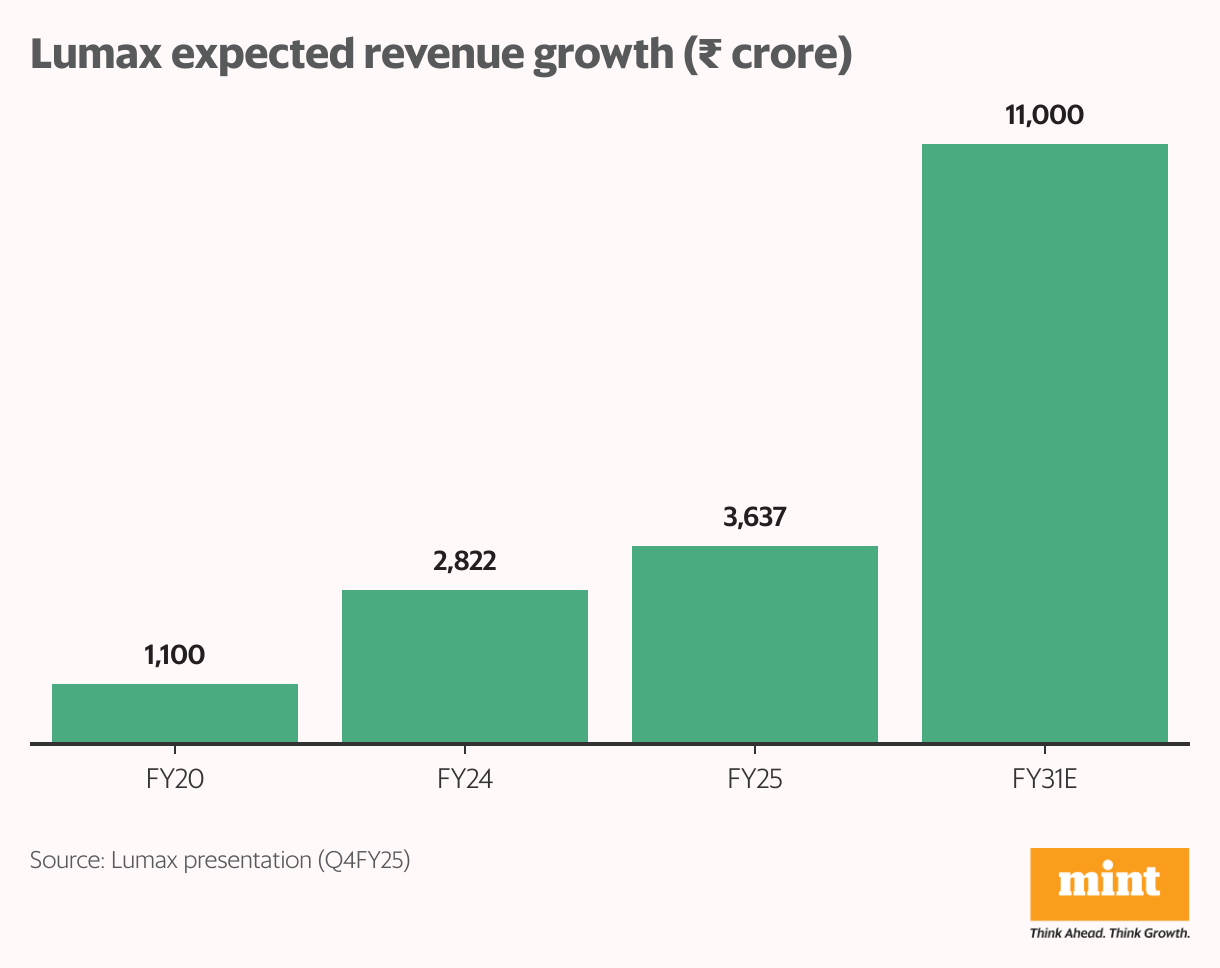

If achieved, Lumax’s revenue could triple to around ₹11,000 crore by FY31 from ₹3,637 crore in FY25.

Lumax aims to unlock growth across its portfolio through its ‘BRIDGE’ (bold roadmap integrating diverse growth engines) strategy, and make the shift from a traditional tier-1 supplier to a tier-0.5 systems integrator.

But how realistic is this target? And what’s driving this optimism?

Let’s dive in.

Broad-based growth drives record FY25 performance

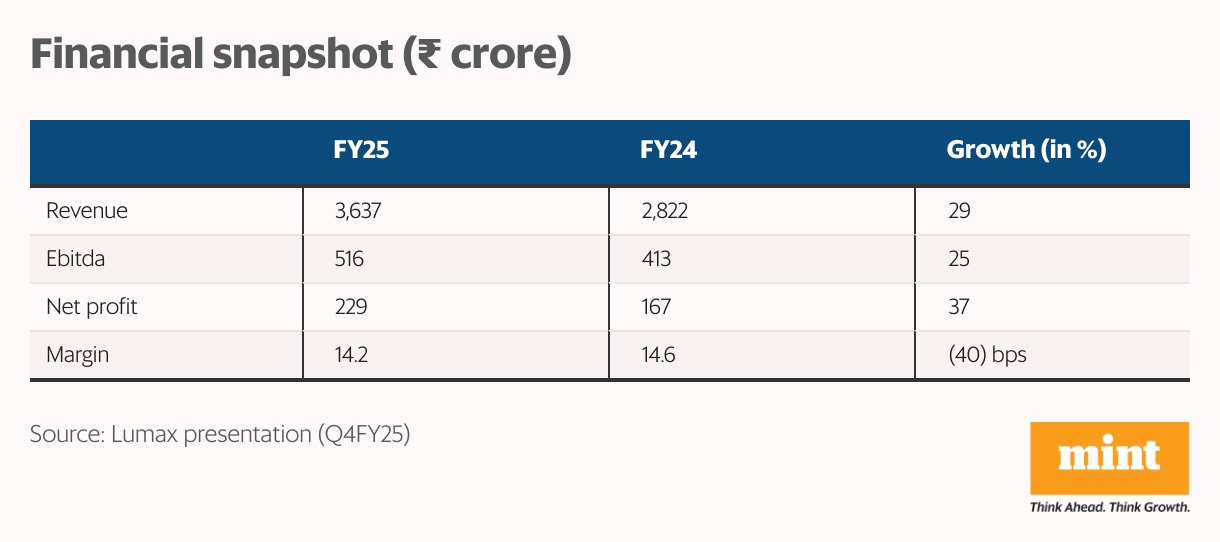

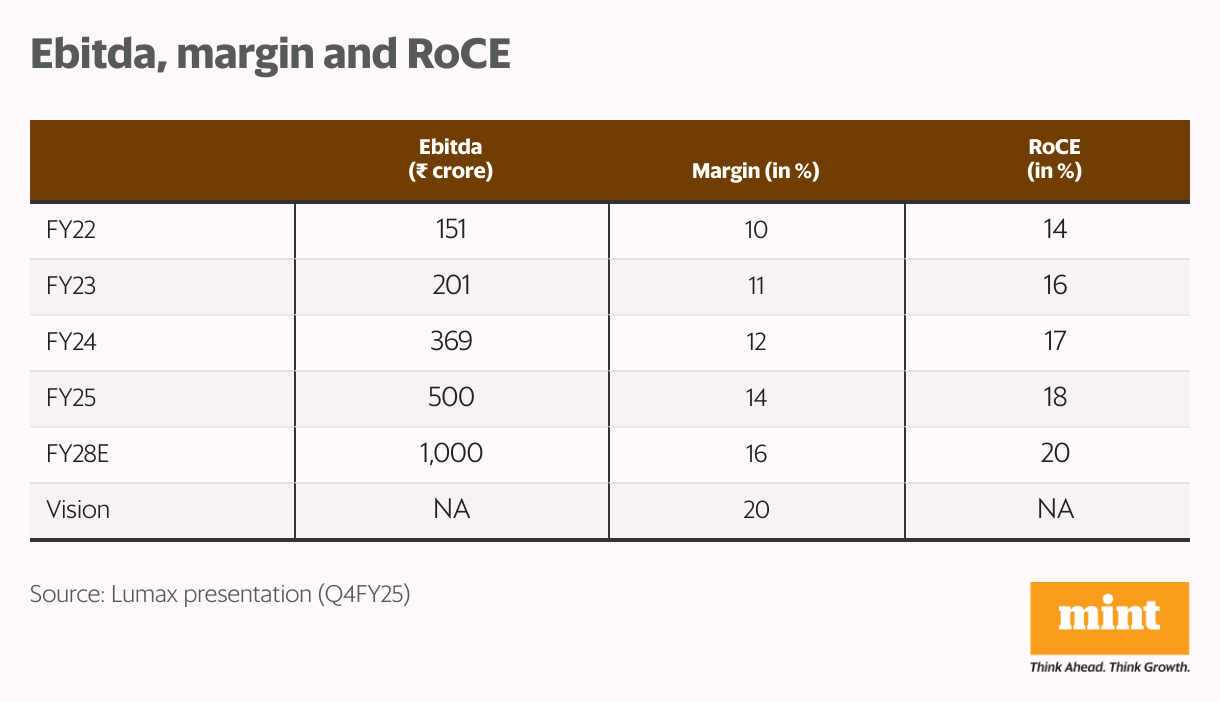

Lumax closed FY25 with its best-ever financial performance. Revenue rose 29% year-on-year to ₹3,637 crore while Ebitda grew 25% to ₹516 crore, crossing ₹500 crore for the first time. The Ebitda margin stood at 14.2% while net profit (before minority interest) also hit a record high, rising 37% to ₹229 crore.

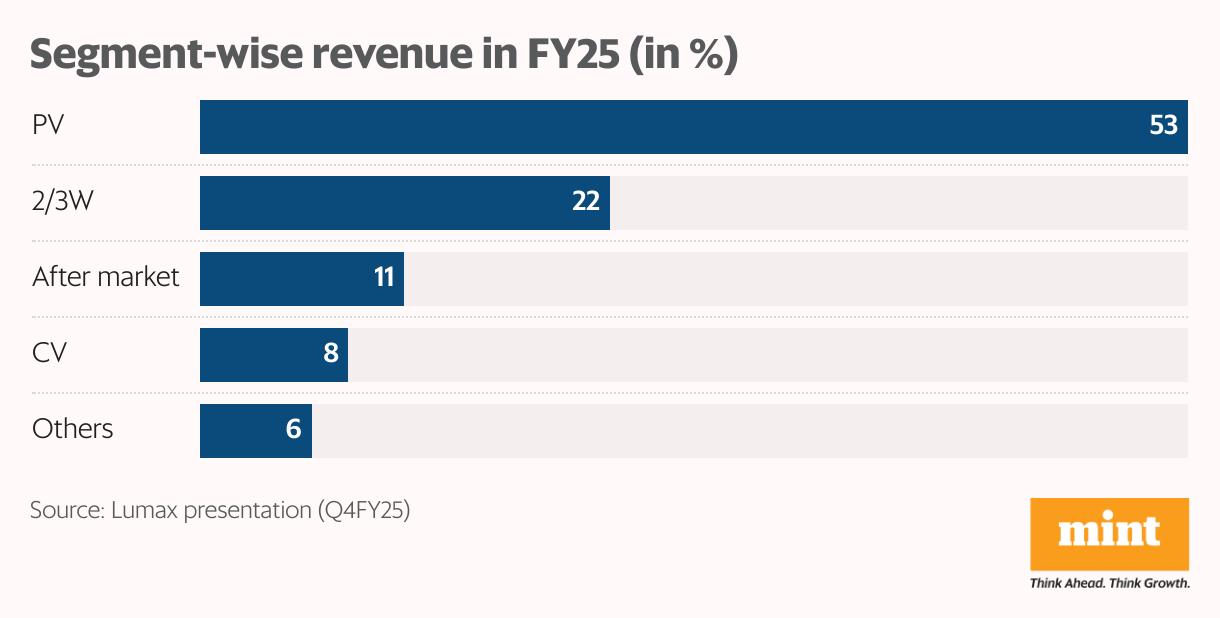

Growth was supported by both product diversification and alignment with industry demand trends. Passenger vehicles (PV) remained the largest segment, accounting for 53% of revenue, followed by two- and three-wheelers (22%), aftermarket (11%), and commercial vehicles (8%).

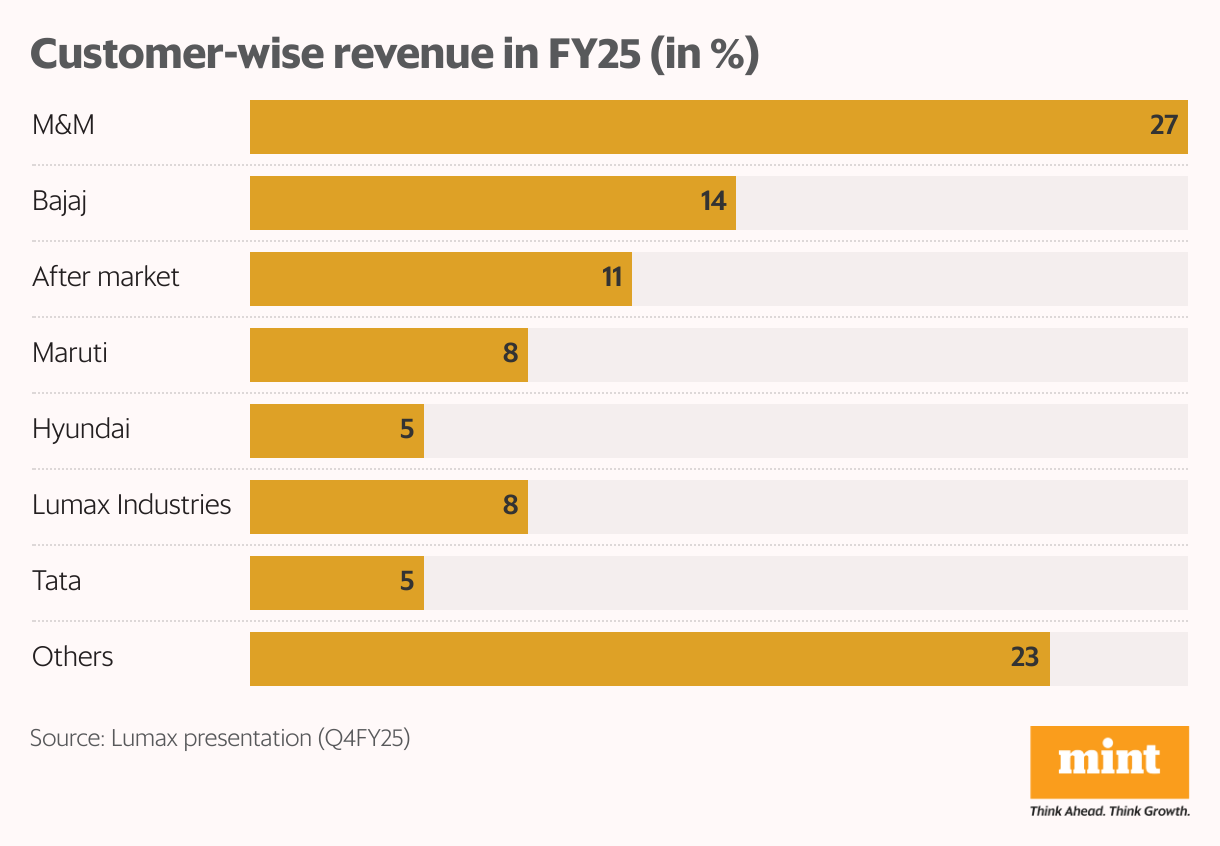

Customer concentration risk remains low, given Lumax’s well-diversified client base.M&M contributed 27% of revenue, followed byBajaj (14%),Maruti Suzuki andLumax Industries“>Lumax Industries (8% each), andHyundai-motor-india-share-price-nse-bse-s0005969″ data-vars-anchor-text=”Hyundai”>Hyundai andTata Motors“>Tata Motors (5% each). The aftermarket accounted for the rest.

The company has steadily increased its content per vehicle, reflecting deeper client integration. In PV, content per vehicle has grown fivefold over the past five years to ₹70,000-75,000. Over the same period, content per two-wheeler has increased nearly fourfold to ₹15,000-18,000. This growth has been supported by a broad product portfolio spanning both internal combustion engines and EV platforms.

Core business segments continue to support momentum

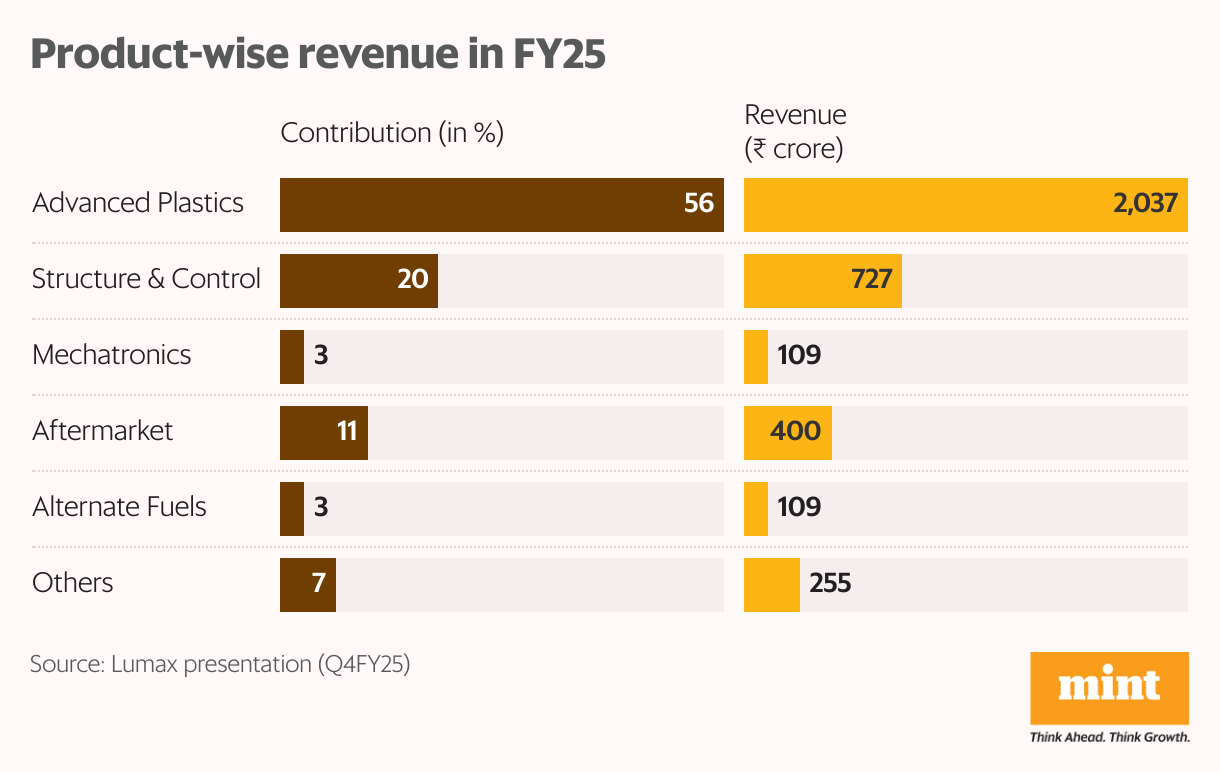

Lumax operates across five key verticals: advanced plastics, structures and control systems, aftermarket, mechatronics, and alternative fuels. The first three collectively account for 87% of overall revenues.

In FY25, advanced plastics revenue increased 27% to ₹2,037 crore, driven by the launch of premium vehicles and deeper client penetration. Structures and control systems rose modestly by 8% to ₹727 crore, driven by steady demand for gear shifters and seating frames.

The aftermarket business grew 5% to ₹403 crore, supported by improving demand and an expanding product portfolio. Mechatronics posted the sharpest rise, up 80% to ₹109 crore, riding on increased adoption of telematics and smart actuators.

With the acquisition of GreenFuel Energy in November 2024, Lumax entered the alternate fuel segment. The company added another ₹110 crore in just four months, implying an annual revenue run rate around ₹330 crore.

Clean mobility is at the core of the strategy

GreenFuel, in which Lumax has a 60% stake, is a market leader in CNG, hydrogen, and EV battery systems, complementing Lumax’s clean mobility ambitions. Notably, it has an asset-light business model with patented products, which helps it generate high margins.

GreenFuel’s margin stood at 22%, well above Lumax’s consolidated 14.2%, making it a margin-accretive asset. The acquisition is expected to contribute ₹300-350 crore to Lumax’s top line in FY26, which accounts for about 10% of FY25 revenue.

GreenFuel also offers potential beyond original equipment manufacturers (OEMs). Its aftermarket presence, technology partnerships, and access to emerging fuel segments can help grow its wallet share. Lumax plans to harness these capabilities to deepen its clean mobility footprint with existing clients.

Other subsidiaries are also being positioned as growth engines. Lumax Alps, Lumax Yokowo, and Lumax Ituran are expected to grow 30–40% annually. Of these, Lumax Alps is projected to grow from ₹50 crore to ₹500 crore over 4–5 years. This is expected to be driven by a 22-product rollout from Alps Alpine’s global portfolio, slated to be operational by FY29.

Lumax has also launched SHIFT (smart hub for innovation & future trends) to strengthen its digital edge with a dedicated software-defined vehicle vertical. Within this, it is working on advanced driver assistance systems, with a pilot batch rolled out to a major two-wheeler manufacturer.

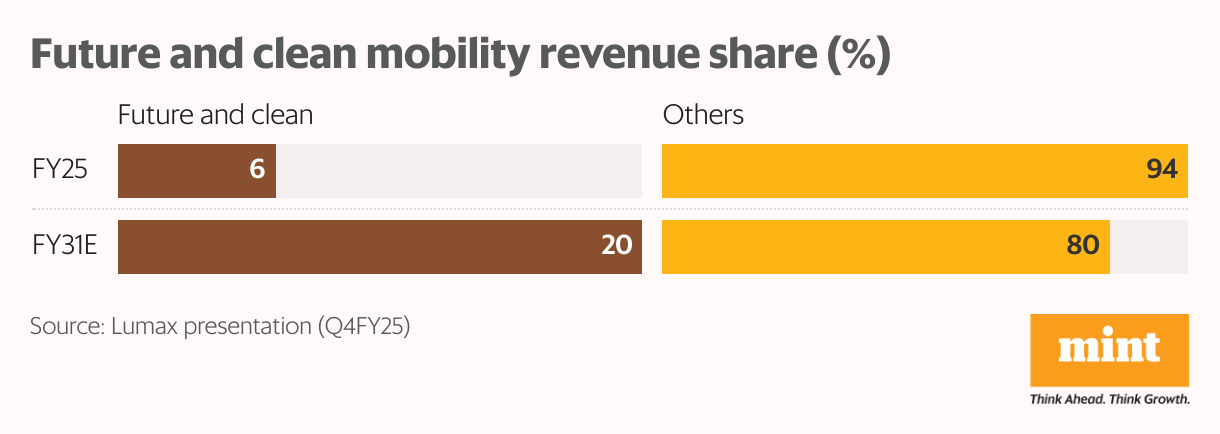

These initiatives aim to increase the share of clean and future mobility revenue from 6% in FY25 to over 20% by FY31. Around 40% of the ₹1,300 crore order book is already tied to the battery electric vehicle (BEV) platform.

IAC India emerges as a critical driver

In May 2025, Lumax acquired the remaining 25% stake in International Automotive Component Group (IAC), making it a wholly owned subsidiary. A merger may follow in due course.

IAC is a major supplier of interior and exterior components to auto companies and has played a key role in Mahindra’s premium EV launches, such as the BE6 and XUV9e. It enjoys a 90-95% wallet share for cockpits and door panels with Mahindra. However, it now aims to expand with Tata Motors and Maruti Suzuki as well.

In FY25, IAC’s revenue rose by 35-40% to around ₹1,200 crores, with an Ebitda margin of 17-17.5%. Management expects IAC revenue to grow at 10–15% annually over the next few years, driven by higher content per vehicle and new client additions.

Though it has sufficient capacity in place, it plans a brownfield expansion for the upcoming Mahindra models. These BEV models offer higher content per vehicle— ₹40,000 to ₹45,000—translating into greater revenue potential. Thus, the incremental volumes from these vehicles will be the key growth driver for IAC from FY26.

Lumax is also looking to grow its aftermarket segment, potentially upwards of 15% in FY26. Focusing on demand generation, spending resources on connecting with retail and mechanics at the last mile, and strong product development plans are expected to contribute to the growth.

It also plans new product launches, including electrical products for 2W in Q1FY26, and suspension and brake systems for 4W in Q3FY26. With these broad-based growth levers, including new product launches, software-driven solutions, and increasing share of clean mobility, it aims to triple its revenue to ₹11,000 crore by FY31.

This can be achieved, given that Lumax’s revenue has already tripled from ₹1,100 crore in FY20 to ₹3,637 crore in FY25.

Lumax expects to double its Ebitda from ₹516 crore in FY25 to ₹1,000 crore by FY28. This would come through operating leverage, a full-year contribution from acquisitions, growth in clean mobility, and scale-up in subsidiaries. If achieved, this could increase Ebitda margins by 100–200 basis points.

While the 20% margin is not set as a hard deadline for FY31, the company’s roadmap is aligned towards inching closer to that target. With higher profitability, its RoCE, currently at 18%, could reach close to 20% by FY28.

Management is also open to further acquisitions but is prioritizing margin-accretive, profitable targets. It has launched a special-purpose vehicle for future inorganic opportunities. But nothing is planned for FY26.

Growth priced in; now it’s about execution

After more than doubling in two months, the stock now trades at a price-to-earnings ratio of 43, well above its five-year median of 24. A significant portion of the growth story is priced in, making the risk-reward less compelling in the near term.

Now, execution is the key.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specializes in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.