The offer-for-sale (OFS), priced between ₹540 and ₹570 per share, marks a key milestone for the company, which has demonstrated strong revenue growth, international expansion, and improving profitability over the past three years.

Having executed over 8,000 drug development projects for more than 675 clients across 44 countries, Anthem has built a solid position in the new chemical entity (NCE) and new biological entity (NBE) segments.

The company’s services cater to over 550 pharmaceutical and biotech clients, primarily in the US, Europe, and Japan. Its core CRDMO segment contributes 81.7% of total revenue, with the rest coming from speciality ingredients.

However, valuation concerns, higher inventory levels, and declining research and development (R&D) intensity may temper enthusiasm. The company’s strong growth trajectory is evident, but will investors look past these risks?

Anthem has posted a 32% compound annual growth rate (CAGR) in revenue between 2022-23 and 2024-25, outpacing peers such as Syngene International (7%), Divi’s Laboratories (10%), and Sai Life Sciences (18%).

“Our growth comes from end-to-end capabilities across the drug development lifecycle,” said Mohammed Gawir Baig, chief financial officer of Anthem Biosciences, in an interview with Mint on 10 July“We support clients from early research to commercial manufacturing.” “About 64% of revenue now comes from 10 commercialized molecules. This integration and long-term client partnerships provide a strong foundation for continued momentum,” he added.

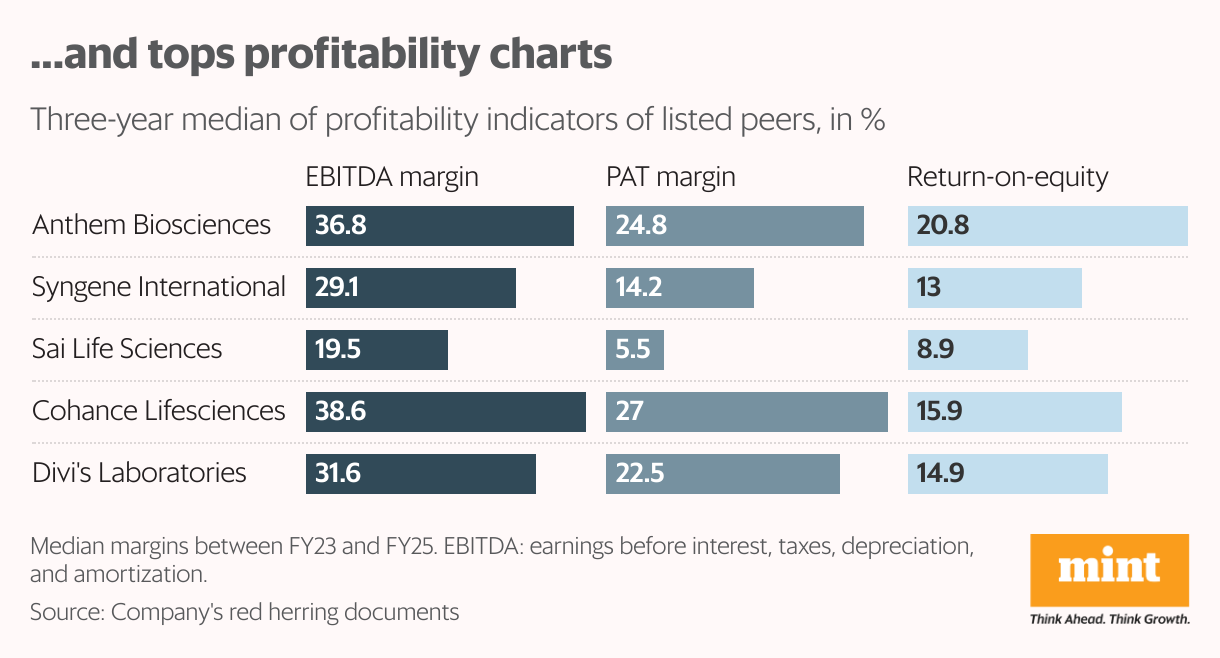

Anthem also stands out for its strong profitability and capital efficiency. It has posted a three-year median Ebitda margin of 36.8%, just below Cohance Lifesciences (38.6%) but ahead of Divi’s (31.6%), Syngene (29.1%), and Sai Life (19.5%). It has delivered a sector-leading median return on equity of 20.8% and a net profit margin of 24.8% in the last three years.

Anthem’s future trajectory appears promising, analysts believe.

Sachin Jasuja, founding partner and head of equities at Centricity WealthTech, a wealth management platform, saw momentum ahead, citing a pipeline of 16 molecules in late-stage development and global factors like the Biosecure Act (a proposed US law to restrict federal ties with biotech firms linked to foreign adversaries, especially China) driving demand away from China. “Ongoing investments in capacity, especially through the new Unit-4 facility, will further strengthen Anthem’s manufacturing and development capabilities.”

However, he cautioned that global macro risks cannot be overlooked, given the high share of revenue derived from exports.

That’s not all. The CRDMO segment operates under significant oversight with players facing sectoral headwinds such as regulatory scrutiny from agencies like the US Food and Drug Administration and European Medicines Agency and the high capital cost of infrastructure and R&D. While these are structural hurdles for most players, Prashanth Tapse, senior vice president at Mehta Equities highlighted that Anthem has demonstrated the ability to scale rapidly while managing such risks effectively—a rare combination in this industry.

What else contributes to its unique standing in this challenging landscape?

Bhavik Joshi, research analyst at INVasset PMS, said Anthem’s strength lies in consistent, high-value delivery. “With a 1,200 KL reactor capacity and 16 late-stage projects, the company has both the visibility and the infrastructure to support its next phase of growth.”

Pricey bet?

At the upper band of ₹570 per share, Anthem seeks a post-issue valuation 70.6 times its 2024-25 earnings. While high on the surface, this is more reasonable when compared to its peers such as Sai Life Sciences (186x), Cohance (144x), and Divi’s (84x).

Experts readily offer reasons for the company’s elevated valuation.

“Anthem’s leadership in the CRDMO segment, combined with strong growth visibility and high-margin operations, supports a premium valuation,” said Tapse, who saw a potential 20-25% upside for long-term investors.

Joshi felt the issue is fairly priced, given its earnings trajectory and capital efficiency. However, he flagged that as a pure OFS, the IPO brings in no fresh capital and could restrict future flexibility.

On a rather optimistic note, Jasuja added: “Anthem stands as a profitable, growth-stage CRDMO backed by strong global demand, solid cash flows, and low leverage. Execution and client concentration risks exist, but the company’s structural strengths make it a compelling long-term story.”

Red flags

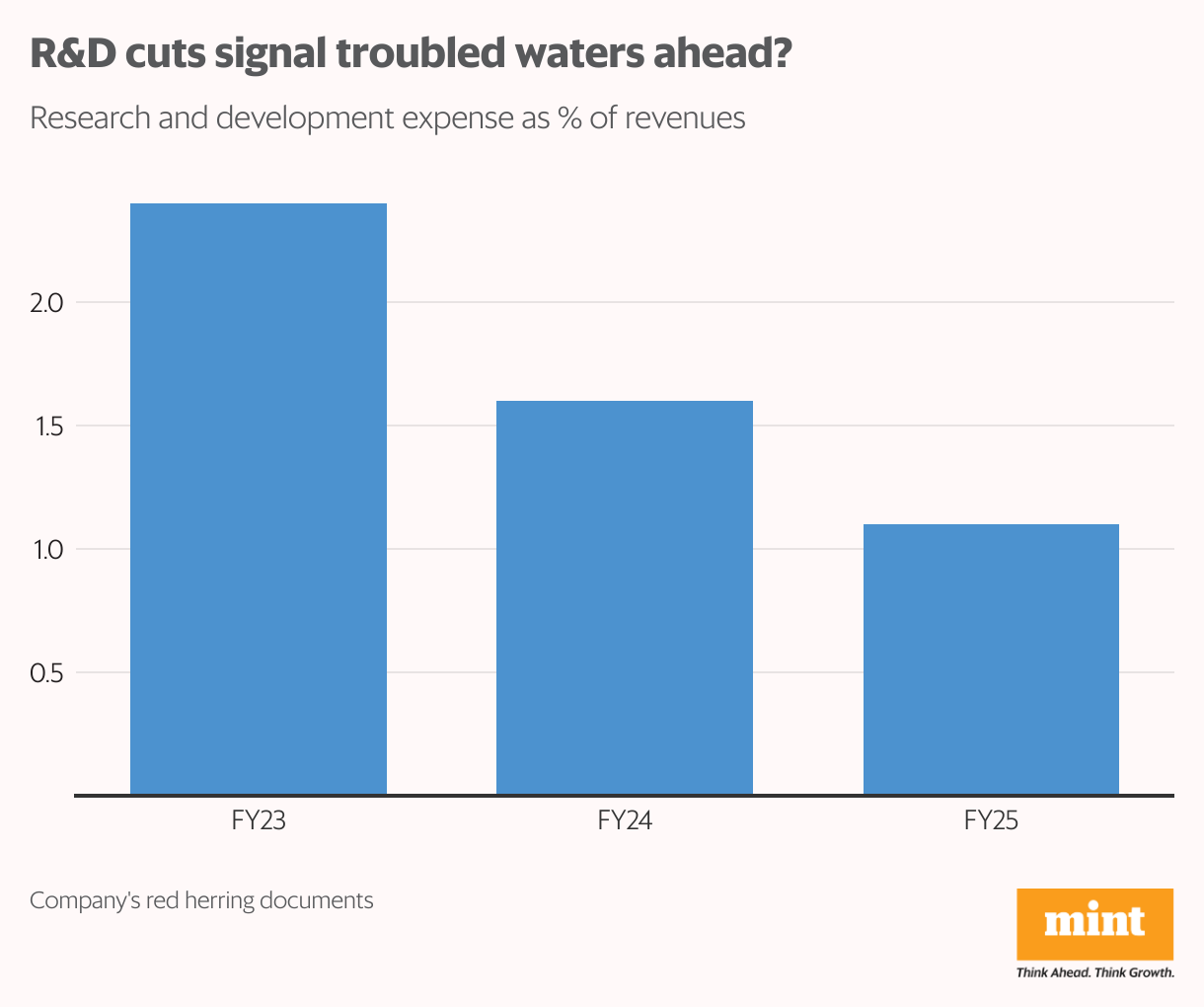

That said, its spending cut on innovation could raise some concerns. Anthem’s research and development expenses as a share of revenues dropped from 2.4% in 2022-23 to just 1.1% in 2024-25. While it might initially raise concerns about innovation, the company clarifies its unique R&D model.

“Most R&D is conducted on a contract basis for our customers. Much of our R&D is customer-paid and does not appear as an internal expense,” said Baig.

He noted that spending on internal innovation, primarily for the speciality fermentation business, remains steady at ₹20-25 crore annually, and the decline in ratio is due to revenue growth, not actual cuts.

Tapse interpreted the trend as a normalization. “R&D expenses may have dropped due to one-time research capacity ramp-ups and may reflect a normalized run-rate. More research may now be done as part of paid client projects.”

He believed this is not a strategic shift, adding, “Anthem’s continued commitment to innovation reinforces its positioning as a full-stack CRDMO.”

However, Joshi flagged potential risks. “The drop in Anthem’s R&D spend is noteworthy, especially in a science-intensive industry.”

He noted that Syngene and Aragen invest 5-7% in R&D. The decline could “signal a tilt toward commercialization over innovation”.

He warned that “as the market matures innovation—not just scale—will determine pricing power and global stickiness”.

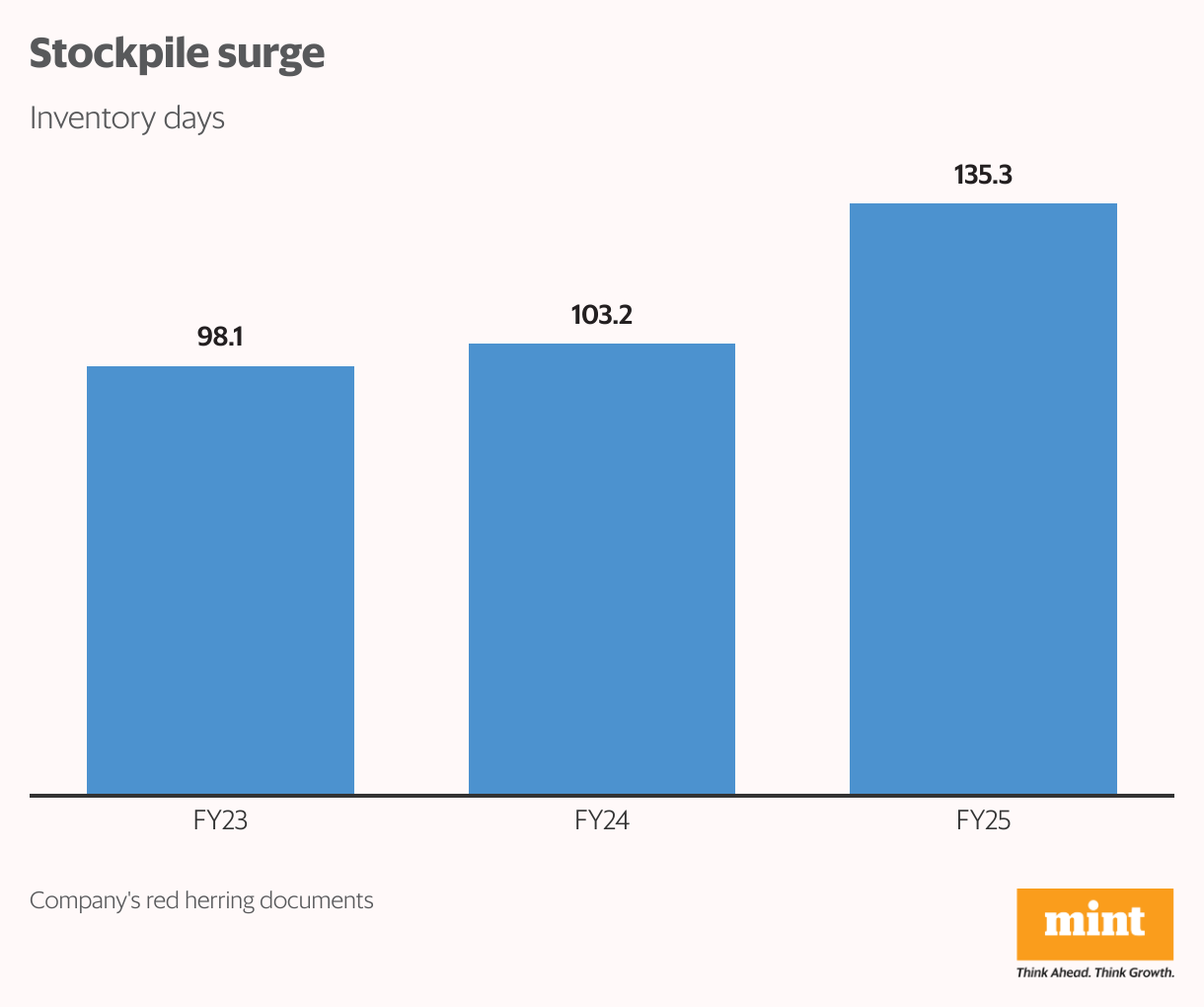

Higher inventory levels

Another area of concern: inventory days have risen from 98 in 2022-23 to 135 in 2024-25. But according to Baig, this reflects strategic stockpiling. “These molecules have long patent cycles, and we maintain buffer stocks as per client agreements to avoid supply disruptions.”

Analysts largely agree that the buildup stems from structural shifts, such as deeper engagement in fermentation and high-potency APIs. Still, risks remain.

“If inventory days remain elevated even post capacity ramp-up, it may point to demand mismatches or delays in commercialization. That could tighten cash flows and impact return ratios,” said Joshi.

Jasuja explained, “The company holds raw material stock in anticipation of the demand over the coming six months, to prevent shortage of stock. Also, with the expected increase in commercialized modules, the company increased its inventory and hence raised the inventory days.”

Sector outlook

The global CRDMO market is projected to grow from $136 billion in 2019 to $330 billion by 2029, driven by small molecules ($244 billion) and large molecules ($86 billion). Anthem, with its 1,200 KL reactor capacity and biologics capabilities, is well-positioned to benefit.

“India’s CRDMO sector is poised to witness accelerated momentum over the next five years, supported by structural tailwinds and global realignments in pharma outsourcing. A key catalyst driving this shift is the growing trust in India’s scientific talent, regulatory maturity, and cost-effective infrastructure, which has made the country a preferred global partner across the drug development value chain,” said Tapse.