While the broader market was unimpressed, the automobile sector has been spooked. Following years of outperformance with the sector’s five-year compound annual growth rate (CAGR) of 22% significantly ahead of the broader market’s 13%, the sector has slipped deep into the red over the last few days.

Will the EU trade deal mark an end to the auto sector’s rally, or is it just a hurdle until the sector finds its feet again? Let’s dive in.

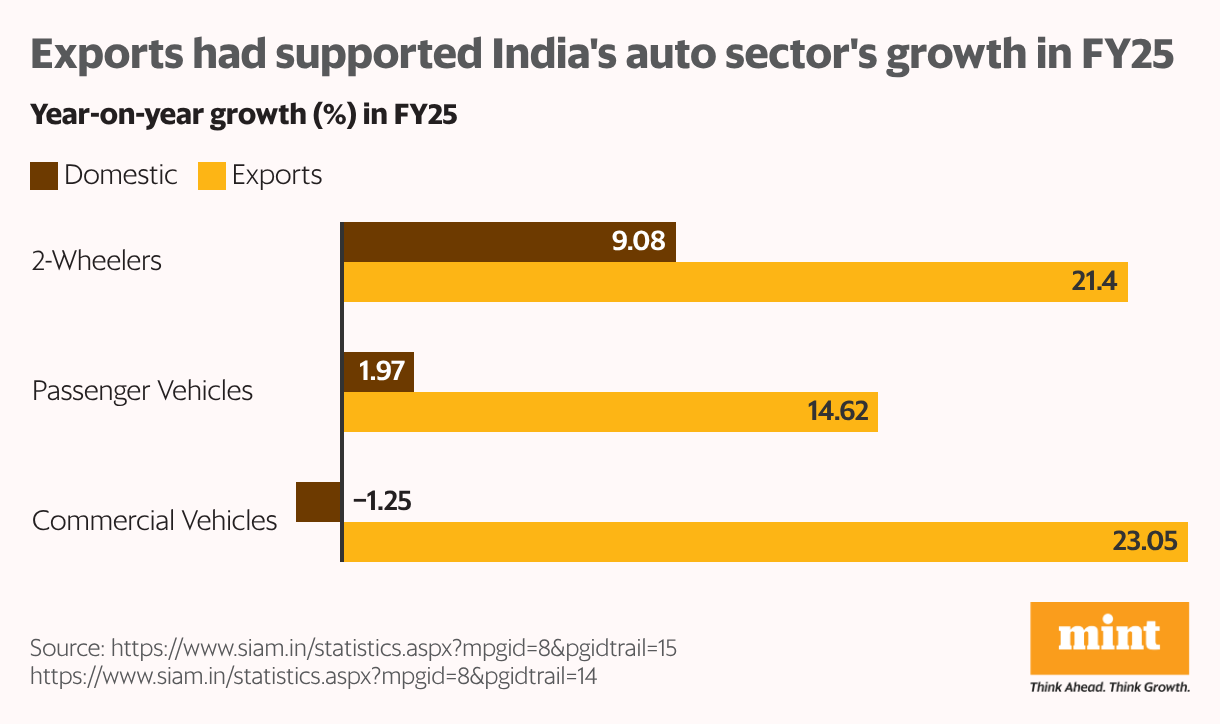

Can India’s auto exports get a fillip?

India’s auto sector has remained one of investors’ favourites, despite domestic demand remaining mellow until September 2025. Exports are to thank for this. With India’s auto exports clocking double-digit growth across segments, India’s automakers had managed to buck the domestic slowdown trend in FY25.

While local demand has picked up pace amid the GST 2.0-powered festival demand spike, exports continue to remain a key driver. Sure, Trump’s tariffs have had little effect on OEM (original equipment manufacturer) exports due to limited direct exports to the US. But auto-component exports could see a contraction. Some of the US-impact can be cushioned as the tariffs on India-made vehicle and component exports to the EU eventually go down from 10% to 0%, and 3-4.5% to 0%, respectively, under the trade deal. But there are caveats.

One, the EU is a small destination for India’s exports, making up 2% of passenger-vehicle exports and 1% of two-wheeler exports. While this leaves room for growth, execution will be key. Maruti Suzuki India Ltd is responsible for half of the passenger-vehicle exports to the EU, and stands as one of the key beneficiaries of the trade deal, particularly as it pushes the pedal on the export of its e-Vitara. Two, the EU’s demand is concentrated in premium motorcycles and electric vehicles (EVs), where India still needs to carve a niche for itself. Finally, green standards can play spoilsport in India’s exports to the EU.

The flip side of the trade deal

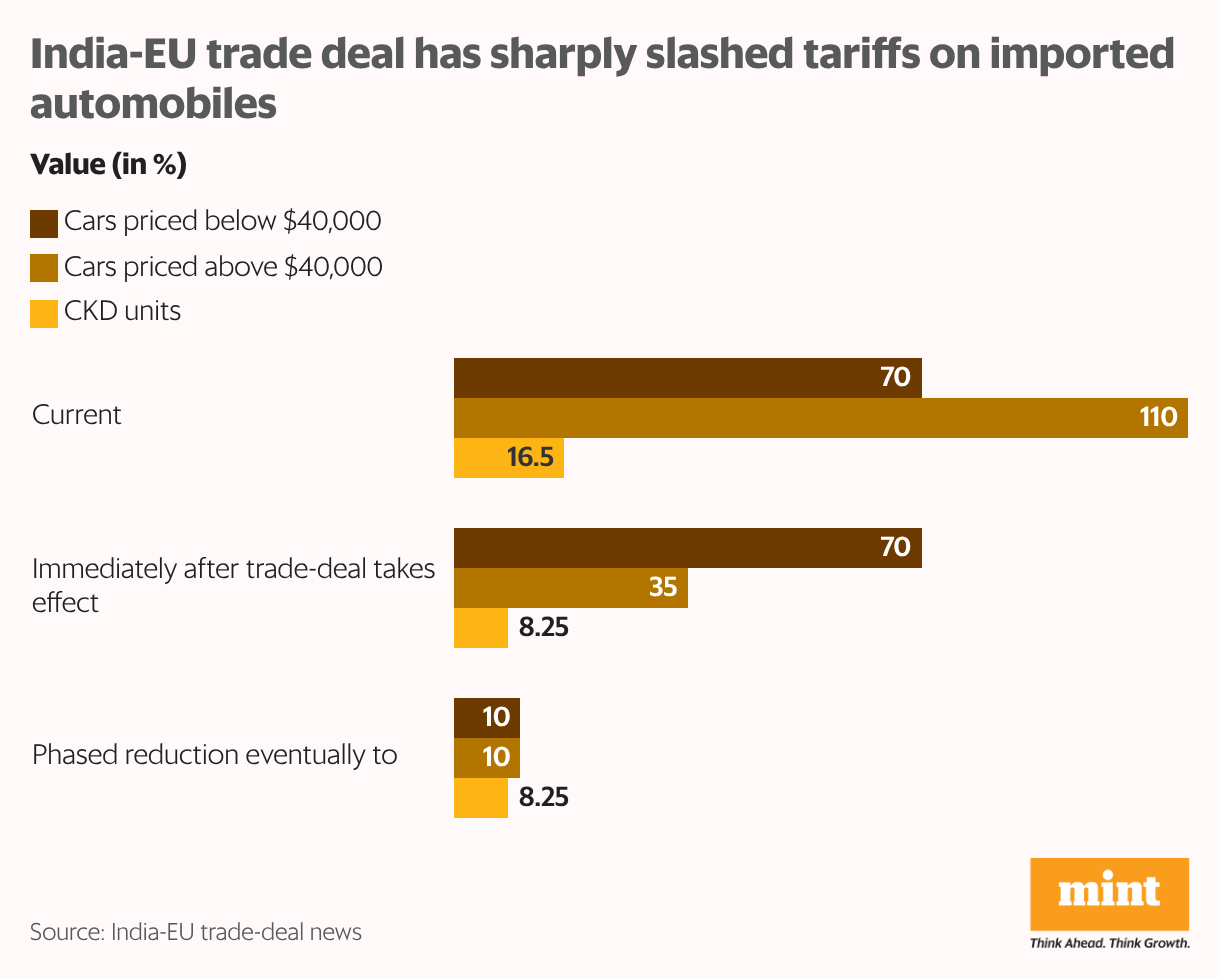

India’s automobile sector has so far been protected from import competition, thanks to tariffs as high as 110%. The trade deal with the EU puts an end to this, with duties on premium automobiles (priced above $40,000) slashed to 35% when the trade deal takes effect, and to 10% eventually. Tariffs on affordable cars will also be phased down to 10% in due course. This is to say that players like Maruti Suzuki in the affordable car segment will also be eventually subject to higher competition.

To be sure, EU carmakers such as Volkswagen, Mercedes-Benz, Renault, and BMW already sell in India. But they have been importing completely knocked down (CKD) units, which attract a much lower 16.5% tariff. By assembling them in India, instead of importing completely built units (CBUs), EU firms have been sidestepping the 100+% tariffs.

While tariffs on premium CBUs will be slashed to 35%, those on CKDs will be halved to 8.25% (subject to a 75,000 annual quota). So, cars, which have assembly facilities in India, will turn more cost-effective. Meanwhile, the CBU tariff cuts will expand the range of luxury European cars which can now be sold in India. This will effectively expand the range of cars facing import competition.

Can the trade deal make the pie bigger?

European carmakers have been bullish on the Indian consumer. Germany-based Mercedes-Benz has already announced local assembly of its luxury SUV, Maybach GLS, making India the only market outside the US to produce the car. Volkswagen has started assembling its recently launched Tayron R-Line in its Maharashtra plant, and France’s Renault plans to manufacture its new Duster SUV in India.

Experts expect the steep tariff cuts to expand market access, thus encouraging deeper integration of European automakers into domestic ecosystems. The BMW chief, for instance, has talked about broadening its India portfolio with globally popular models.

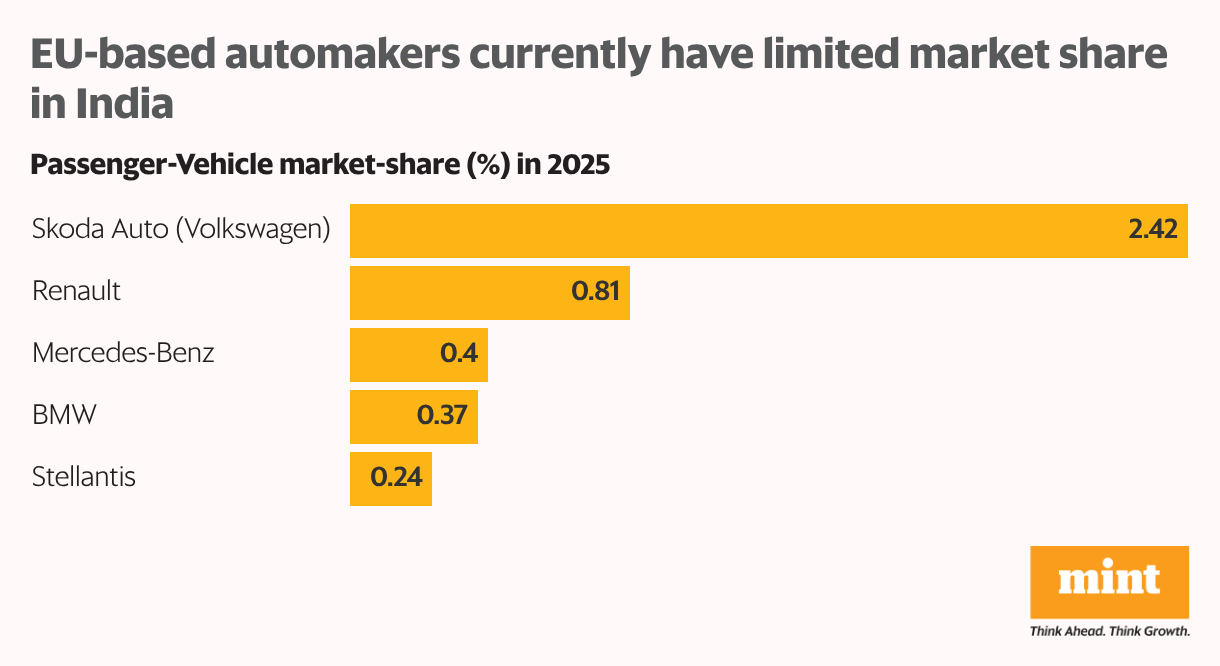

EU-based automakers together claimed less than 5% share of India’s passenger-vehicle market in 2025. While the EU trade deal sets the stage for market share expansion, it may not necessarily come at the cost of other players. Some experts suggest that as new luxury car models become available in India, the country’s luxury automobile market will expand. As the pie gets bigger, even with EU-based players potentially claiming a larger share, overall fortunes should also see an upturn.

The double-edged EV sword

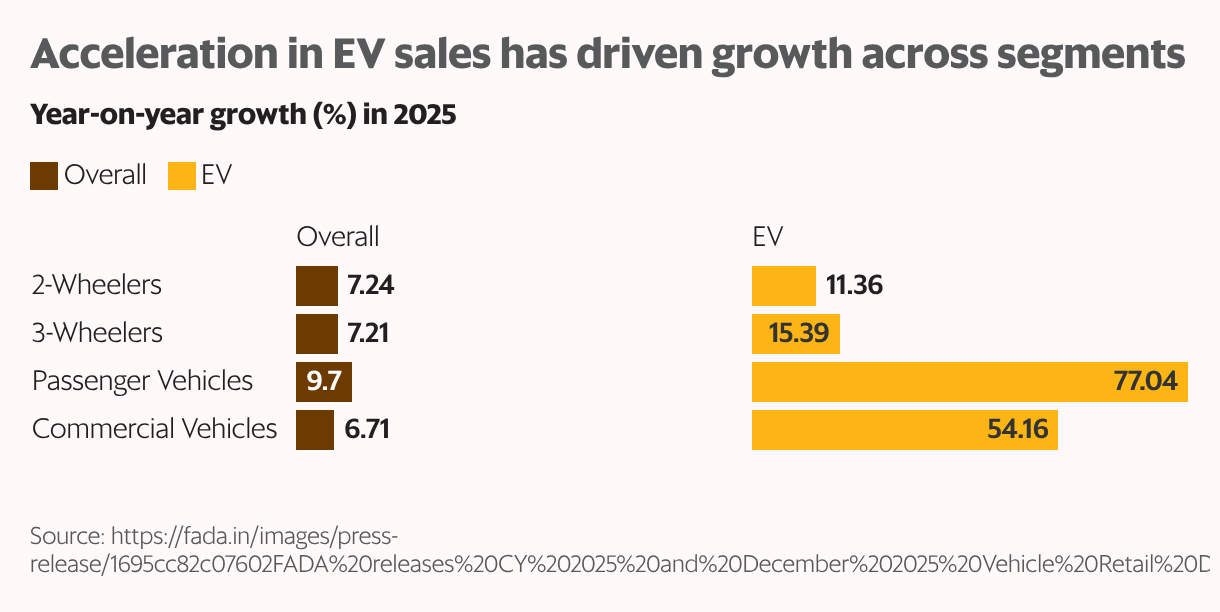

EVs have moved into the fast lane. As drivers’ range anxiety is managed by emerging charging stations and increasing charging density along highways, EVs are quickly becoming mainstream. In fact, the auto-sales growth in 2025 can be ascribed primarily to the growth in EVs. Across segments, EV sales have led overall sales, with the 54%, 77%, and 1,010% year-on-year growth in EV tractors, passenger vehicles, and commercial vehicles taking the cake.

Even as EVs are shaping up to become a structural driver of long-term growth, cracks are starting to appear. GST 2.0, which slashed the GST rate on affordable cars from 28% to 18%, effectively eroded EVs’ tax advantage because they continue to attract a5% GST. New lifecycle analysis (LCA) norms propose including the cost of mining critical minerals and recycling to assess climate impact across vehicle segments, and could further tilt the scales away from EVs. With EU EVs standing to benefit five years after the deal’s ratification, competition is set to intensify further.

China’s dominance in the EV supply chain has also kept the industry on edge. First, there was intense competition in China following the introduction of domestic EV incentives. Then, China’s curbs on exports of rare-earth magnets disrupted global production. The latest hit has come on the cost of production, due to the removal of China’s rebates on the export of EV raw materials. Such risks have forced policymakers to look at alternatives, including hybrids and flex-fuel vehicles, while also opening the floor for debate that green hydrogen vehicles, not EVs, are the end goal. Until a clear policy direction emerges, the pace of EV adoption could stumble.

Summing it up

Analysts estimate that a year before the EU trade deal can go into effect after due ratification. The duty cuts on premium cars will also be subject to an annual quota of 250,000 units, capping the impact on competition. Until the tariff cuts take effect, domestic auto sales could spike, subject to demand holding up.

The near-term domestic demand outlook is expected to be supported by GST 2.0-driven sentiment, “a packed calendar of festivals and the marriage season, and typical financial-year-end buying”, according to the Federation of Automobile Dealers Associations. Rural demand is expected to keep pace, supported by robust Rabi sowing, contained inflation, and lower interest rates. Any consumption incentives announced in the Union budget on 1 February can also drive up sales, even as price revisions announced by OEMs keep purchase urgency intact.

Long-term prospects remain promising, on the back of growing urbanization and expanding disposable incomes. While the EU trade deal can intensify competition at the premium end over the medium term, healthy competition bodes well for the industry’s long-term outlook. That said, supply-chain issues, an evolving regulatory environment, and an unforgiving valuation at 29x P/E can lead to short-term volatility.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser.

Disclosure: The author does not hold shares of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.