In doing so, ICICI Group will break away from two of its peers, SBI Group and HDFC Group, each of which has three listed businesses. All three are behemoths with fingers in every financial services pie of size and significance, having driven and shaped the massive opening up of India’s financial sector after 1991. However, they have gone about this is different ways, with banking behemoth SBI delivering some surprises.

Mint takes a closer look at how all three giants are performing.

Taking stock

Stock returns over the long term are one of the indicators of their performance. For all three groups, only their banks have a long track record on the bourses. The other businesses, principally mutual funds and insurance, have all been listed in the past five years or so. And contrary to perception, they have not always beaten the market.

Over the past five years, only three of the nine businesses have outperformed the bellwether BSE Sensex: SBI, SBI Life Insurance, and ICICI Bank. Over 10 years and 15 years, all three banks topped the Sensex. But over 20 years and 25 years, HDFC Bank beat the Sensex, while ICICI Bank and SBI trailed it. All three banks are among the 12 stocks that have been part of the Sensex for 20 years or more. During this period, the Sensex has delivered a compounded annual return of 16.7%. But only two of the 12 stocks, HDFC Bank and Maruti Suzuki, have bettered that.

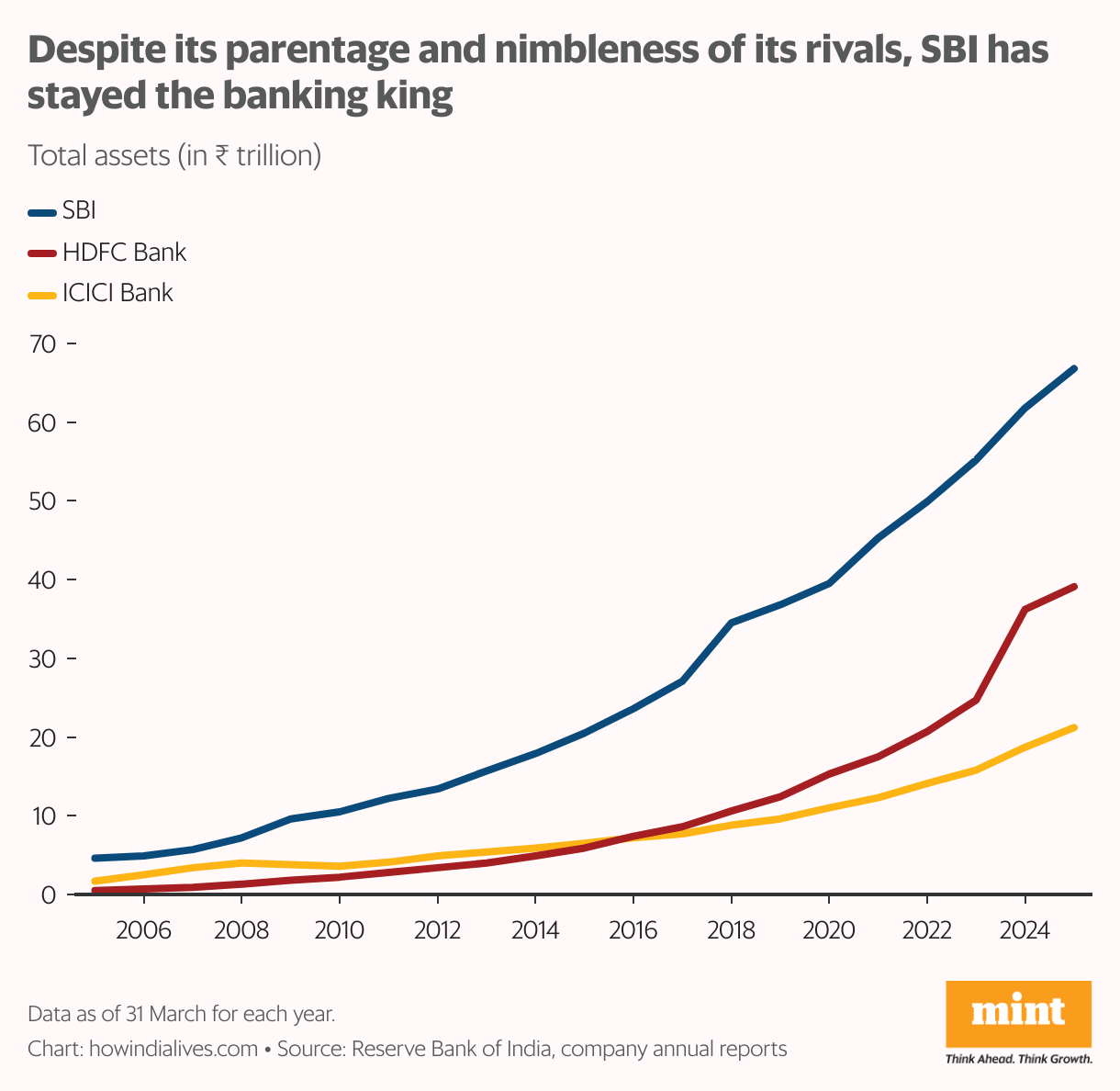

Banking: SBI retains its crown

Each of the three groups has different roots. SBI has a government connection, HDFC’s traces its origins to a housing finance company, and ICICI began as a financier for long-term projects. After the widespread economic reforms of 1991 threw open India’s financial sector, private groups gradually expanded their presence in growing sectors.

In banking, SBI’s status as India’s largest bank was under threat. That was as much a consequence of ICICI Bank’s aggressive expansion as it was of SBI trying to find its feet in the changing landscape.

ICICI Bank was incorporated only in 1994; SBI had been around since 1955. Yet, by 2007, ICICI Bank’s asset base was about 60% of SBI’s. That was the closest it would come, however, as ICICI tripped on bad loans and SBI started leveraging its size and network better. It’s only now, with HDFC Bank absorbing its parent HDFC, that a bank has bridged the assets gap with SBI.

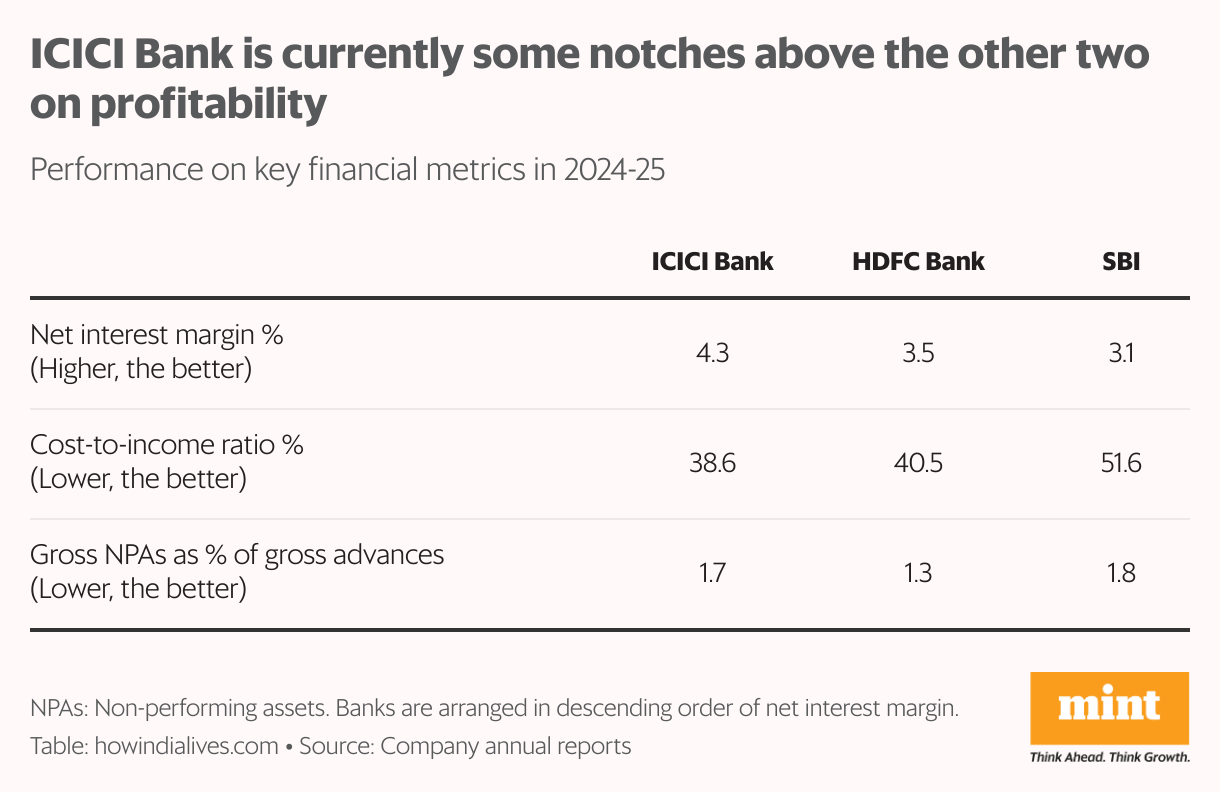

Banking: Private players’ profitability premium

The banking sector has seen consolidation, especially among government banks. While ICICI Bank and HDFC Bank have made small mergers and acquisitions, SBI made a significant move in 2017 by bringing six associate banks into its fold. Even without that, ICICI Bank and HDFC Bank have seen growth moderate as they focus on strengthening their balance sheets and preserving profitability.

A key measure of a bank’s profitability is the net interest margin (NIM)—the difference between the average interest it earns on its loans and the interest it pays on its deposits. The higher this spread, the more profitable a bank.

ICICI Bank’s NIM is a cut above HDFC Bank’s—which has seen this number fall following the merger with its parent—and more than a percentage point higher than SBI’s. Higher profitability is a big reason why HDFC Bank and ICICI Bank command richer valuations than SBI. They have a price-to-earnings ratio of 21 and 17, respectively, versus 11 for SBI. This premium is unlikely to disappear anytime soon.

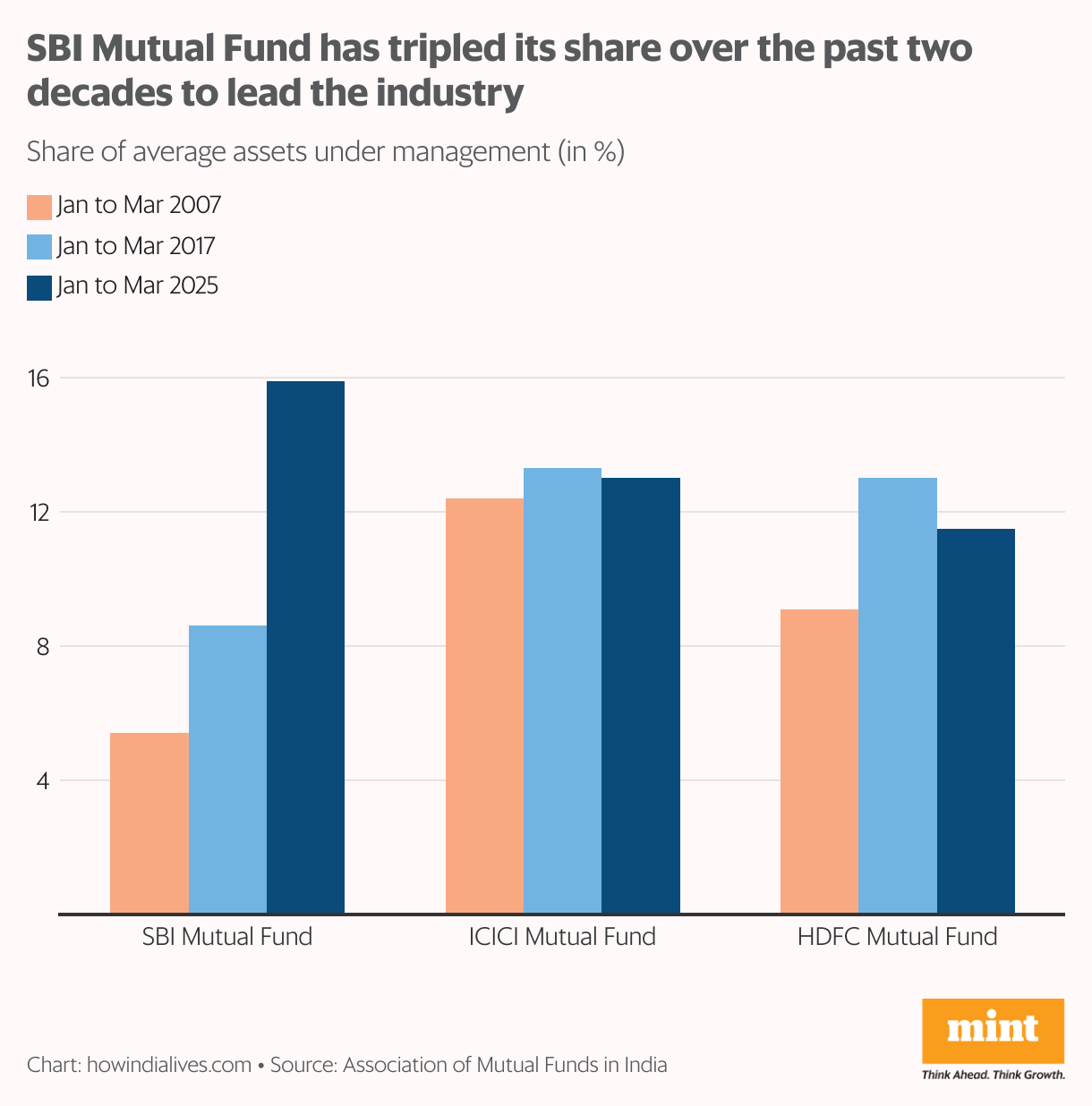

Mutual funds: HDFC a late bloomer

As in banking, these are the top three mutual fund houses in India, accounting for about 40% of the industry’s assets. However, their journeys started at different times. SBI Mutual Fund, one of the handful of mutual funds that existed before liberalisation, was born in 198. ICICI Mutual Fund came into existene in 1993, soon after the sector was opened to private players. HDFC Mutual Fund was a late entrant in 2000. Only in recent years have they come to dominate the market, and the big mover here is SBI Mutual Fund.

In March 2007, when the total size of India’s mutual fund industry was ₹3.5 trillion, SBI Mutual Fund was ranked number 7 by assets. By March 2017, the industry grew to about ₹18.2 trillion. ICICI Mutual Fund and HDFC Mutual Fund occupied the top two slots, while SBI Mutual Fund was at number 5. Since then, it has leapfrogged both to the top spot, riding on solid scheme performance, government connections, and the post-covid expansion in the sector.

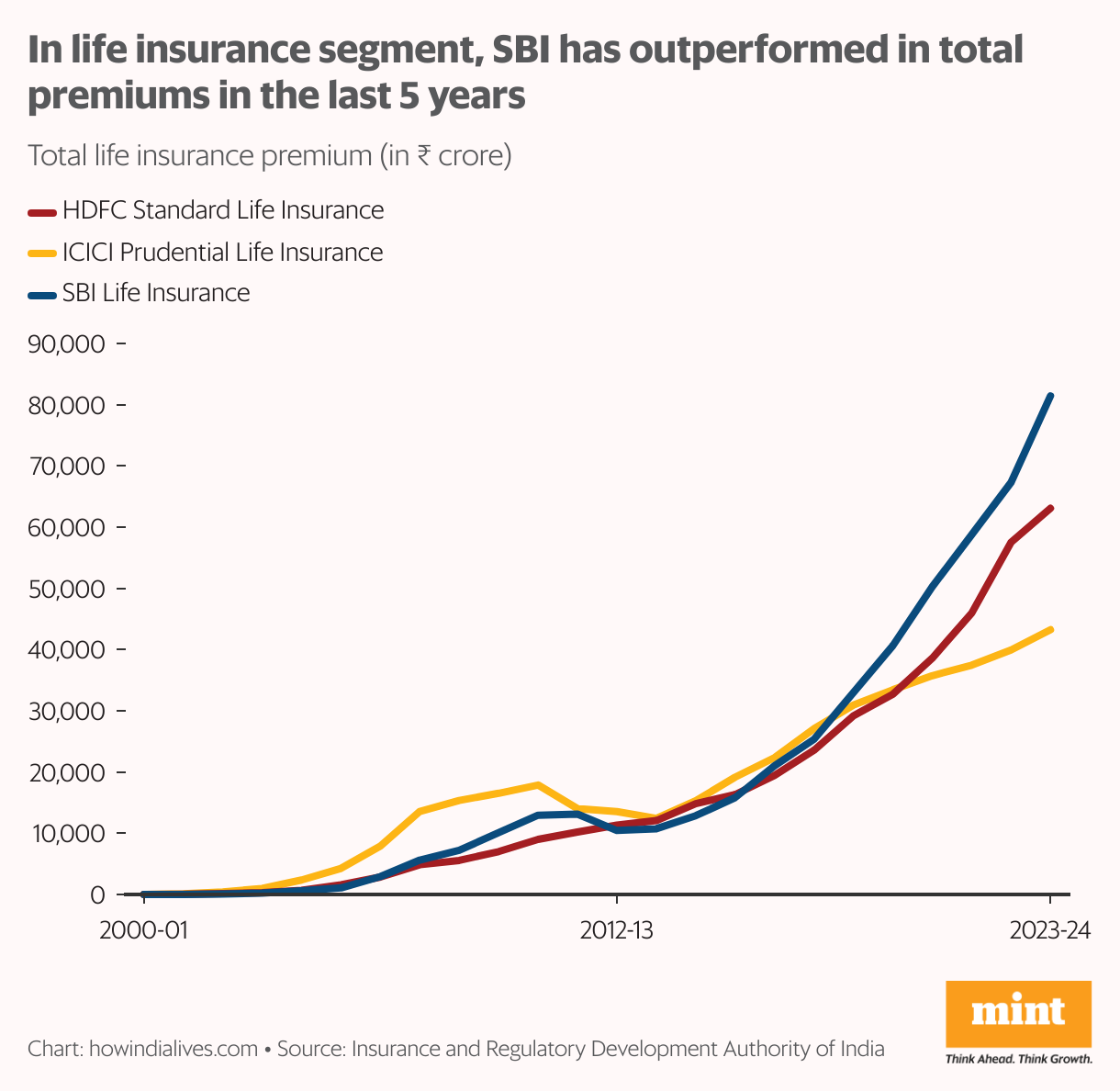

Insurance: SBI pulls ahead

Life insurance is one business where the entry of the three groups more or less coincided. The monopoly of Life Insurance Corporation (LIC) was lifted in December 1999, and all three groups entered the business over the next two years. As in banking, ICICI was the early mover, riding on investment-cum-insurance plans. A regulatory clampdown on such plans checked growth both for ICICI Prudential Life and SBI Life. In 2012-13, all three were nearly the same size. But in the past five years, SBI Life has broken away at the top.

Even in non-life insurance, SBI General has grown faster over this period than its two peers, albeit on a smaller base. Several of these non-banking businesses are yet to deliver the kind of market returns that solid businesses are known for. Their ability to do so in the coming years will depend on their continuing dominance.

www.howindialives.com is a database and search engine for public data.