The market-cap-based HHI for the National Stock Exchange (NSE) peaked at an 11-year high of 173 in March 2020, when pandemic uncertainty funnelled money into the most liquid large-caps. By October 2025, it had eased to 80, lowest level since March 2018, reflecting a broadening of ownership and liquidity.

What the HHI says—and why it matters

The HHI is calculated by squaring each entity’s market share and adding up the results. It ranges from near zero in a perfectly competitive market to 10,000 in a pure monopoly. In equity markets with thousands of tradable stocks, even small changes in HHI are meaningful: lower scores indicate dispersed liquidity, while higher ones signal clustering around a few influential names.

Regulatory thresholds place scores below 1,500 in the “competitive” zone, 1,500-2,500 in “moderate concentration,” and above 2,500 in “high concentration.” Absolute values in equities rarely approach these levels, but directionally, a decline signifies a healthier spread of activity.

A broadening market across segments

That trend is most visible in headline indices. The Nifty 50 remains the tightest cluster, with an HHI of 363, slightly higher than 354 a month earlier but well below its March 2009 peak of 476. The Nifty Next 50 stands at 252. Beyond the large-caps, concentration collapses: mid-cap, small-cap and micro-cap HHIs sit near multi-year lows at 77, 47 and 47, respectively.

This dispersion reflects a larger listed universe, the sustained outperformance of mid- and small-caps, and rising domestic participation through retail flows, systemic investment plans (SIPs) and passive assets under management (AUM).

Experts say the drop in concentration across indices signals a shift in how market leadership is forming.

“When large-cap HHIs remain elevated but mid-, small- and micro-caps sit in the 47-77 band, it shows that participation is no longer top-heavy,” said Charmi Shah, business head, Wealth1 – PMS & AIF Investments. “Such dispersion changes the behaviour of rallies. The market is less exposed to a correction in a handful of heavyweights, and leadership tends to rotate more frequently across sectors and sizes.”

Shah added that a lower-HHI environment widens the opportunity set for active managers but also brings higher dispersion in returns. “If earnings breadth stays intact, this phase could support more durable, broad-based uptrends rather than narrow, index-led moves.”

A metric of democratization

Turnover data underscores the shift. Equity cash-turnover HHI fell to 43.6 in October, down sharply from 51.8 a year earlier. Market-cap concentration eased from 79.3 to 78 over the same period.

Both metrics had soared during the pandemic. Turnover HHI hit 204.5 in July 2020 and market-cap HHI peaked at 196.7 in October 2020, when investors crowded into a narrow set of liquid names.

Since then, both have steadily normalized, mirroring the broadening of participation across the exchange.

“India’s market microstructure is undergoing a notable shift. The decline in turnover HHI from October 2024 to October 2025 suggests a broadening of liquidity, though it isn’t guaranteed to persist,” said Harshal Dasani, business head, INVasset PMS. “This phase is different because of sustained domestic demand—record SIP inflows in October 2025 and a demat base of over 210 million accounts—which is spreading capital more evenly across segments.”

Institutional portfolios begin to widen

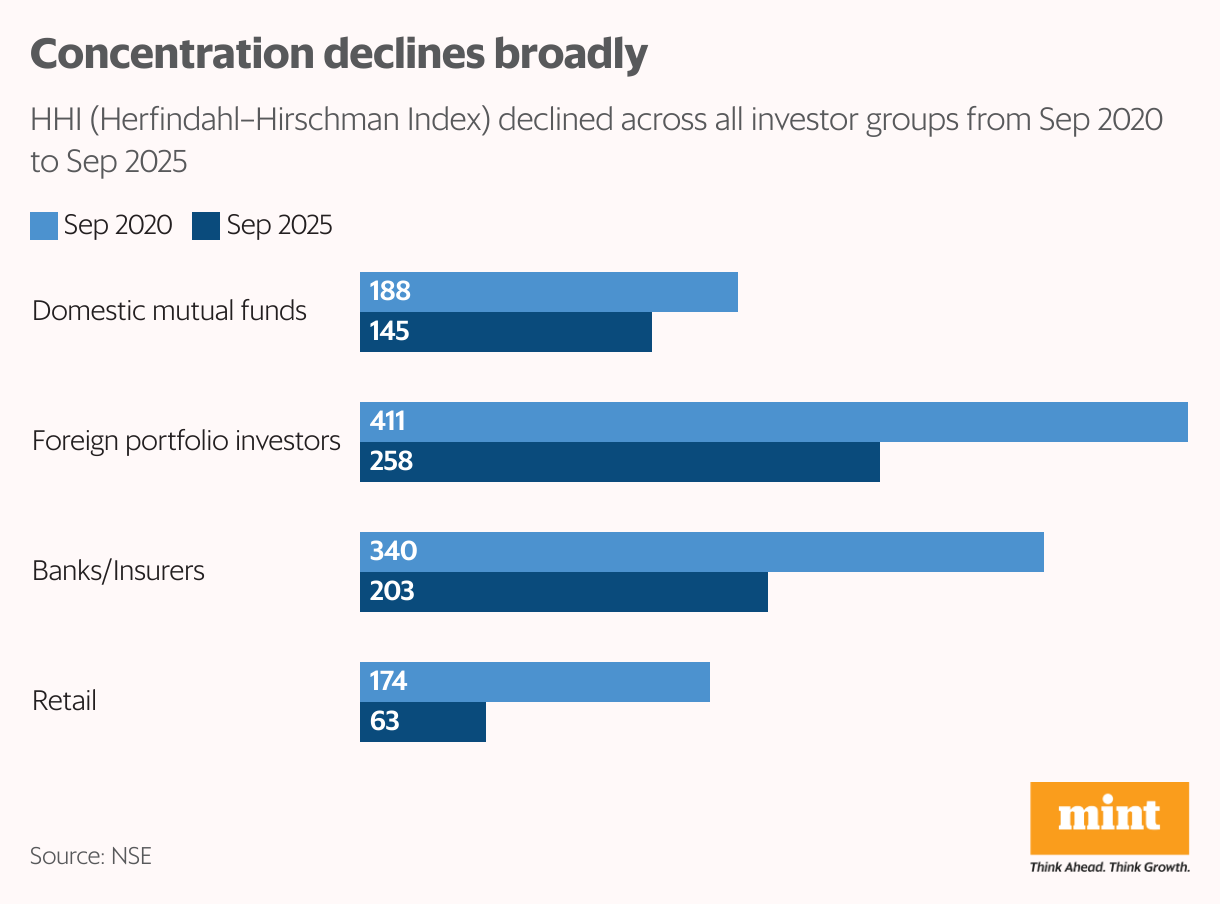

Institutional ownership patterns reinforce the broadening. In the September quarter, the HHI for institutional portfolios across NSE-listed companies fell to 186, its second straight quarterly decline. Banks, insurers and financial institutions showed the sharpest dispersion: their HHI slid to 203, a near 20-year low. Historically, this cohort concentrated heavily in liquid defensives, with HHIs of 340 in September 2020, 287 in 2015, 229 in 2010 and 199 in 2005.

Domestic mutual funds (MFs) followed a similar trajectory. Their HHI dropped to 145, well below 188 in September 2020 and far from the post-pandemic peak of 189 in December 2020. Record SIP flows and expanding passive AUM have pushed domestic MFs towards a wider stock universe, reducing concentration risk.

Across major sectors, too, concentration has eased between September 2020 and September 2025. Communication services HHI fell from 5,719 to 5,011; IT from 2,654 to 1,380; consumer staples from 1,229 to 1,114; financials from 1,054 to 1,002; and industrials from 660 to 529. Energy, historically a tightly held pocket, declined from 4,810 to 4,126. Materials alone saw a marginal rise from 343 to 388 but remained within a competitive range.

Domestic MFs, however, remain most concentrated in communication services and energy, reflecting the dominance of a few large constituents.

FPIs widen their footprint

Foreign portfolio investors, traditionally the most concentrated category, have also expanded their reach. The FPI HHI fell to 258 September 2025, sharply lower than the September 2020 peak of 411. The number of companies with FPI holdings has risen for five quarters in a row, reaching 2,046 in September 2025, up from around 1,300 four years ago.

Sectoral HHI declines confirm this trend. Concentration in consumer discretionary eased from 836 to 675, consumer staples from 1,358 to 945, industrials from 684 to 536, and IT from 2,580 to 1,832. Materials dropped sharply from 726 to 425.

Energy remains elevated despite moderating from 8,268 to 5,698 due to the limited number of large investable companies. Communication services saw a rise from 2,349 to 6,311, reflecting the dominance of a few big firms, but this remains an exception in an otherwise broadening landscape.

Retail investors: the broadest of all

Retail investors remain the most diversified. Their portfolio HHI dropped from 174 in September 2020 to 63 in September 2025, the lowest among all investor categories. Retail allocations are naturally spread across mid-, small- and micro-caps, unburdened by liquidity or mandate constraints.

Sectoral numbers capture this dispersion, Energy HHI fell sharply from 7,271 to 4,486, consumer staples from 1,333 to 900, IT from 1,700 to 606, industrials from 693 to 275 and materials from 690 to 265. Utilities saw a mild rise from 603 to 703 but remain well below institutional levels. Communication Services stands at 1,075, still higher than competitive thresholds but significantly lower than post-pandemic peaks.

“The easing of institutional concentration—particularly among DMFs—shows that India’s largest allocators are spreading their portfolios more widely,” said Dasani. “Retail investors get diversification through SIPs and low-cost funds, while FPIs continue to take concentrated bets in high-growth pockets like communication services.”