One fine day, some investors land up at your doorstep and gush about the good things they are hearing about the market, the runway for growth, the buzz around your business, etc., and request you to sell a part stake in your company to them. You are free to name any price. After you manage to hide your smile, what will be the price that you quote them? More importantly, when you name that number, whose upside will you really be trying to maximize—yours or theirs?

This is a classic example of what economic theorists call ‘informational asymmetry,’ or a situation where one party (the seller in this case) knows far more than the buyer and therefore holds a decisive upper hand from the very start.

While most transactions contain some imbalance of information, nowhere is this gap wider than in initial public offering (IPO) investing. Which is why many astute investors refuse to come anywhere near such offerings.

Warren Buffett has famously stayed away from IPOs. The only time he personally participated in a new listing was when he purchased some shares of Ford Motor during its IPO way back in 1956. Berkshire Hathaway’s maiden IPO investment was in data storage firm Snowflake in 2020. Just two IPOs in an investing career spanning over 70 years!

Fellow market legend Peter Lynch, in his best-seller One Up on Wall Street, says shiny new IPOs have an almost hypnotic effect on investors, adding that three out of four IPOs he has bought turned out to be long-term disappointments.

That said, it’s worth remembering that excess of anything is harmful, including scepticism. Some startup stocks have created fabulous wealth for early believers, while storied bluechips have disappointed. And frankly, if you say no to every new opportunity, you might as well ask yourself what you’re doing in the equity markets in the first place. The field may be strewn with red flags, but an early entry into the next Infosys, Titan or TCS will be enough to wipe away years of misjudgements and wrong calls.

With Dalal Street seeing a surge in both new listings and investors who have burnt their fingers, this is perhaps the perfect moment to look for clues on what makes an IPO truly successful, how to look beyond grey market premiums and how to separate the signal from the noise.

True test

All IPOs are tricky, but startup IPOs sit at the very peak of the difficulty curve. These are young, fast-growing companies with untested business models and inadequate financial histories. Most are loss-making, which means we cannot use traditional metrics like price-to-earnings (P/E) ratios to evaluate them. To compound matters, the hype cycle around them is almost always in overdrive.

But that’s not to say it is all sizzle and no substance. Some startups are reshaping entire industries and forcing legacy heavyweights to shape up or ship out.

A prime example is Zomato (now Eternal), which has steamrolled past every critic and is trading at more than four times its issue price. From an IPO valuation of about ₹60,000 crore, it has ballooned into a ₹2.7 trillion giant, creating a staggering ₹2 trillion in investor wealth in just four-and-a-half years. For context, it took Infosys more than two decades to create equivalent shareholder wealth.

View Full Image

At the same time, several once-celebrated next-generation companies have turned out to be unmitigated public market disasters, languishing up to 50% below their IPO prices. Clearly, startup IPOs inhabit the extreme edges of the risk-reward spectrum.

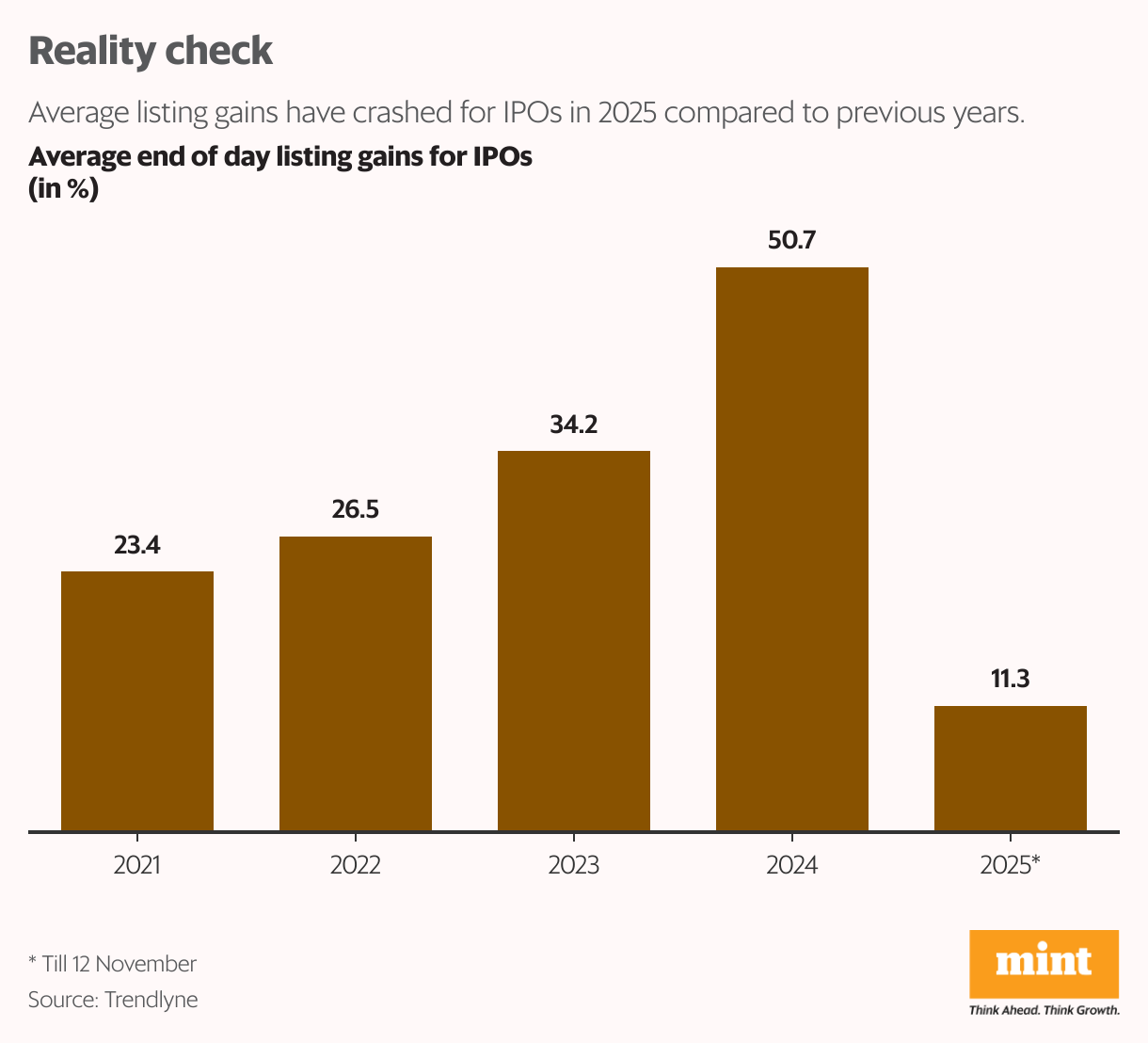

Consider the around dozen startups that have launched mainboard IPOs in 2025 so far. Half have already lost money for investors, including one counter that’s down 30% from the listing price. Two have made decent gains, while another two have delivered phenomenal returns.

The story isn’t very different for the startups that debuted last year. Five out of 10 have plunged as much as 50%, including names like Firstcry, Mobikwik and Ola Electric. Four have delivered respectable double-digit returns. And one standout stock has rocketed over 130%.

Is this wide dispersion just randomness at play? Or is there a method to this madness?

“A key factor is that many of these businesses arrived at the public markets with valuations shaped by private fundings, where aggressive capital raises often push valuations that may not always translate into corresponding fundamentals at the time of public listing,” Ravi Singh, chief research officer at Master Capital Services, a financial services outfit, told Mint.

Public markets are more demanding in terms of profitability and growth visibility, governance comfort and fair pricing. When these are missing, it often leads to weak listings and poor post-IPO performance.

“Moreover, many of these new-age business IPOs are more designed to offer lucrative exits to existing investors than to build new shareholders confidence, which the market ultimately tends to push back,” Singh added.

This strikes at the very heart of what separates investing from speculation. In their rush to grab the latest hot thing in the market, most investors forget the simplest truth in finance: even the finest company can bomb your portfolio if you pay the wrong price for it. What determines your returns is not how good a particular company is, but how much you’ve paid for it.

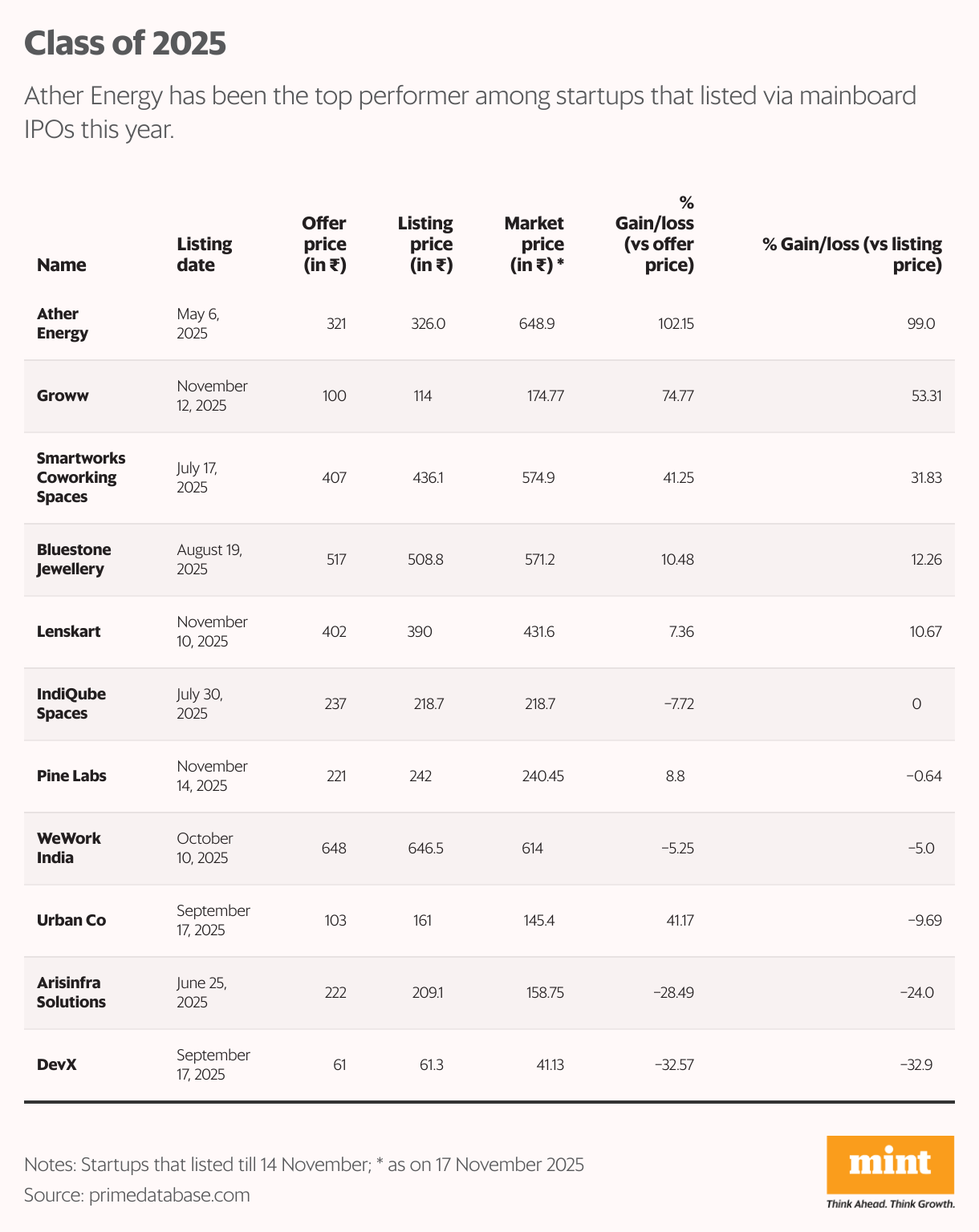

An egregious example of this has been Lenskart, among this year’s most anticipated (not to mention the most trolled) startup IPOs.

On a fundamental level, investing in a company that posted revenue from operations of ₹6,652 crore and profit after tax of ₹297 crore in fiscal year 2025 (FY25), and which is the largest seller of prescription eyeglasses among organized retailers in India, makes perfect sense.

View Full Image

And yet, the devil, as always, lies in the pricing details. At the upper end of the IPO price band, the company was seeking a market valuation of about ₹70,000 crore, translating into a head spinning P/E ratio of around 235. This is more than double the earnings multiple commanded by retail majors like DMart, Trent and Titan. And the cherry on the cake was that out of the profit for FY25, more than half came from a one-time gain from an acquisition.

All this led to Ambit Capital initiating coverage on Lenskart with a ‘sell’ call—one of the very rare instances when a stock received a downgrade even before its market debut.

Consider another much-hyped listing: Urban Company, the most oversubscribed startup IPO of 2025, drawing an eye-popping 109x subscription.

Urban Company is, in many ways, the archetype of a breakout startup. It was one of the earliest movers in the organized home services space, and is effectively building the category nationwide. The firm has also extended into branded products, including water purifiers and electronic door locks. Its financials look healthy, with total revenue in FY25 of ₹1,260 crore and profit after tax of ₹240 crore. It also enjoys some genuine bragging rights, with no direct listed competitor to benchmark against.

The stock made a blockbuster debut, listing at over 55% premium to its issue price. However, the stock is down 10% since that day.

A 61x P/E at IPO was a mountain too high to summit, and an EV/Ebitda multiple north of 100 on FY27 projections pushes it firmly into the bubble territory.

EV refers to enterprise value. Ebitda is earnings before interest, taxes, depreciation and amortization.

Urban Company’s stock made a blockbuster debut, listing at over 55% premium to its issue price. However, the stock is down 10% since that day.

Ambition, it turns out, is great for every aspect of the business except the IPO price.

“The scale of fundraising and intensity of issuances this year underscore confidence in India’s capital markets,” Vivek Rajaraman, executive director and head, client advisory, Waterfield Advisors, told Mint. “The fact that companies are willing to list and investors are willing to subscribe—even at elevated valuations—suggests robust market depth and liquidity. This bodes well for equity market sentiment and may support broader market gains,” he added.

However, the high activity also warrants caution: elevated valuations increase the margin for short-term disappointment, Rajaraman further said.

Decoding debuts

While valuation remains the most important arbiter of IPO destinies, there are some other very crucial clues worthy of tracking.

A striking pattern among most underperforming startup IPOs this year has been heavy subscription, particularly by the most excitable segment in the market—retail investors.

Case in point is Urban Company, which saw the retail portion of its offering oversubscribed 41 times.

Close behind is co-working player DevX, subscribed 64 times overall and a staggering 165 times by retail investors. It was trading more than 30% below its issue price on 17 November, making it the worst performer among 2025 startup listings (see chart).

This showcases a remarkable moth-to-the-flame dynamic: in IPOs where retail investors emerged as the highest or second-highest subscribing category, the stock has mostly destroyed value or eked out only meagre gains. Retail enthusiasm has turned into a pretty reliable ‘negative indicator’. And 2025 is not an aberration.

Mobikwik, one of the most hyped listings of the previous year, saw 125 times overall subscription and 141 times by retail. It is now down 40% from its listing price. Unicommerce attracted an extraordinary 168 times subscription in August 2024, with retail at 131x, yet the stock has crashed 40% since.

Interestingly, experts say this trend is visible in the overall primary market as well.

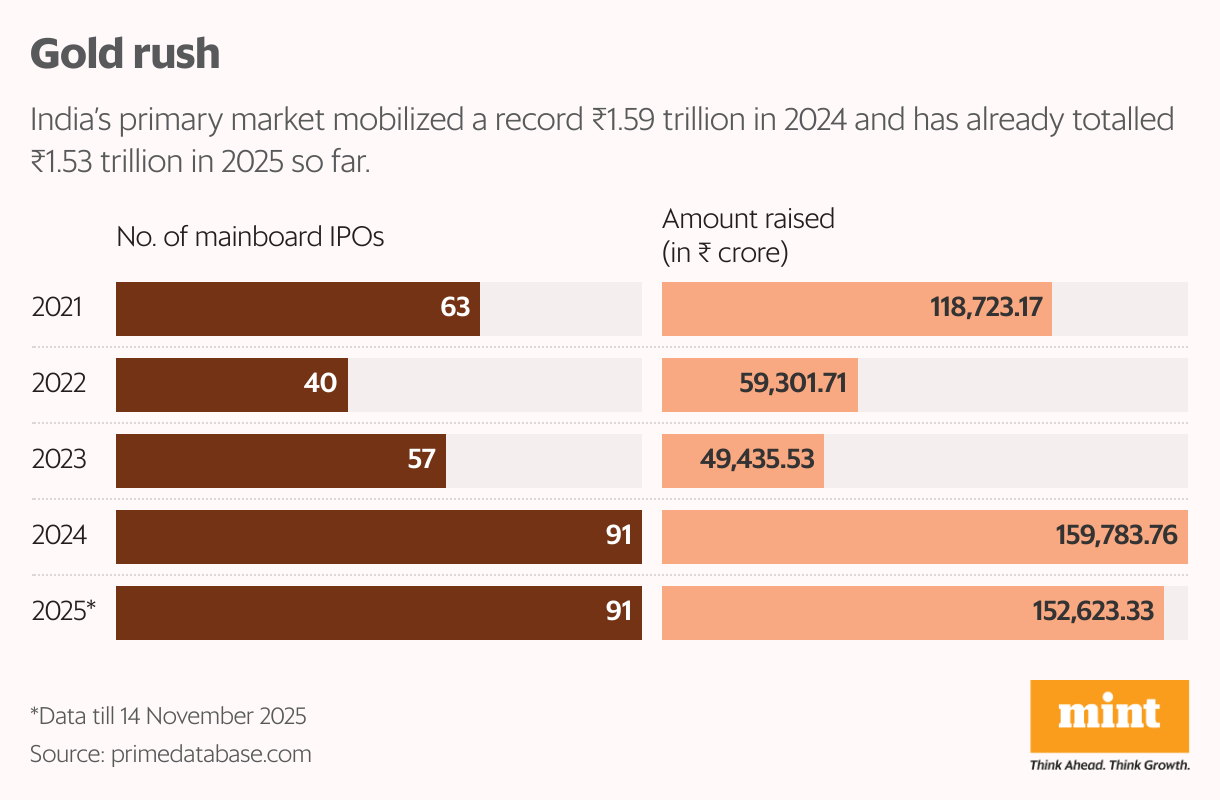

Akhilesh Prakhya, investment manager at SKG Investment & Advisory, said that out of the 189 mainboard IPOs in 2024 and 2025, 79 IPOs are currently trading below their issue price, and 39 companies have corrected more than 20% from their issue price.

“Of these 39 steep decliners, 19 companies had received subscriptions of over 25 times, meaning 48.72% of the sharply underperforming IPOs were actually among the most aggressively subscribed during the offer period,” he said.

This pattern extends to the most-sought-after issues as well. Among the 35 IPOs that attracted more than 100x subscription, typically dominated by high-net-worth individuals and institutional bids, a significant 18 companies (51.43%) are currently delivering returns of less than 15% .

This indicates that even exceptionally strong demand in the book-building process has not been a reliable predictor of sustained value creation.

“The data suggests that subscription intensity often viewed as a proxy for investor conviction has repeatedly failed to translate into long term performance. Instead, a substantial proportion of highly subscribed IPOs have delivered muted or negative returns, highlighting the widening gap between offer period enthusiasm and market reality,” Prakhya added.

In contrast, a far more dependable indicator of a company’s internal strength has been employee subscription.

One of the top-performing startup listings in recent times has been freight platform Black Buck, which has vaulted over 130% since its IPO in Nov 2024. Its ₹1,115-crore issue drew only modest interest, with overall subscription at 1.87 times and the non-institutional investors quota barely a quarter filled. But the employee tranche was subscribed nearly 10 times, a telling vote of confidence from a company’s real ‘insiders.’

Similar has been the case with the best-performing startup IPO of 2025, Ather Energy, which has surged 100% in just six months. Its IPO barely crawled over the finish line at 1.5 times subscription. The non-institutional investors portion remained undersubscribed, and retail bid for only 1.8 times the portion reserved for it, despite the red-hot electric vehicle theme. But once again, employees showed unshakeable confidence, subscribing their allotment 5.4 times.

In many aspects, Ather has been the standout startup IPO of this year. From roughly 12% market share at the time of its IPO, Ather has expanded its share to 17.4% in Q2 FY26, becoming the second-biggest electric two-wheeler player, behind TVS Motor, Mint had earlier reported.

This trajectory sharply contrasts with Ola Electric, which once commanded more than half of India’s electric two-wheeler market, but has now slipped to the fourth spot amid persistent service issues.

Most crucially, Ather left something on the table for retail investors at the time of its IPO. At an enterprise value of ₹12,300 crore, the IPO was effectively asking for a 5.6x revenue multiple on projected FY25 numbers. That was richer than Bajaj Auto’s 4x and TVS’s 3.5x multiples, but still far from the eye-watering 10x EV-to-sales multiple for Lenskart.

“Ather’s strong market performance is widely the result of improving business fundamentals and sensible IPO pricing,” Master Capital Services’ Singh said.

Ather’s strong market performance is the result of improving business fundamentals and sensible IPO pricing. — Ravi Singh

The valuation arc, however, is now unwinding at another IPO success story of 2025—Groww.

The IPO ticked all the right boxes. Groww came to the primary market as India’s largest broker as well as the largest retail investment platform with 12.6 million active National Stock Exchange clients, as of 30 June. It is also one of the foremost platforms for mutual funds distribution. A consolidated topline of ₹4,061 crore and profit of ₹1,824 crore for FY25 underlines its solid financial health.

The stock listed with a 12% premium on 12 November, and soared more than 90% from the IPO price in the next four sessions. This gave it a market cap of ₹1 trillion, pushing its P/E ratio beyond 50, while its peers like Motilal Oswal, Nuvama Wealth and Angel One were trading at roughly half that multiple.

Now only two scenarios are possible in this case. Either the entire sector re-rates, or Groww’s shareholders learn a very painful lesson in mean reversion. No prizes for guessing which way it went. The stock tanked over 15% in the next two days.

Mindset change

So how should one navigate the minefield of IPO investing where even fundamentally strong businesses can get hammered?

Experts say the first thing serious investors should do is to get out of the mindset of chasing listing day gains based on the grey market premium.

“Retail investors should not blindly follow the grey market premium as it can be misleading and does not necessarily indicate strong fundamentals and valuations. What matters far more is clarity on the business’s defined competitive edge, revenue traction, along with sustainable economic metrics which will lead the path to profitability, rather than just rapid top-line growth. Needless to say, IPO valuation remains a key filter,” Master Capital Services’ Singh said.

Not just that, it is important to realise that investing in startup IPOs requires far more careful scrutiny than traditional businesses.

“Given strong issuance momentum, investors should consider selective participation in high-quality IPOs (with solid business models, growth visibility, sensible pricing) rather than broadly chasing every issue. IPOs can serve as tactical/strategic add-ons but should not dominate core holdings, which rely on the broader market/regime,” Waterfield Advisors’ Rajaraman added.

In other words, if execution, management quality and sensible valuations are what make an IPO successful, then patience, discipline and the ability to look beyond the noise are the building blocks of a successful investor.

Key Takeaways

- All IPOs are tricky, but startup IPOs sit at the very peak of the difficulty curve.

- These are young companies with untested business models and inadequate financial history.

- High P/E ratios and overvalued listings, driven by private funding rounds, increase public market risk.

- Informational asymmetry lets sellers maximize their upside in private deals; this gap is widest in IPOs.

- Even strong firms fail if the launch price leaves investors nothing to gain.

- A striking pattern among most underperforming startup IPOs this year has been heavy subscription, particularly by retail investors.

- Experts say serious investors should not chase listing day gains based on the grey market premium.