But the real story lies in how India plans to meet this demand. And it’s not by mining more, but by recycling smarter.

The scarcity of critical metals like copper, aluminum, and zinc is already pushing policymakers and manufacturers to rethink sourcing. Recycling is emerging as the silent engine powering this shift, backed by a government roadmap that mandates a minimum of 5% recycled content in new non-ferrous metal products by FY28, rising to 10% for aluminum, 20% for copper, and 25% for zinc by FY31.

This structural change is opening a large, long-term opportunity for organized recyclers. While names like Gravita India and Pondy Oxides & Chemicals have already found investor attention, another contender, Jain Resource Recycling, is quietly scaling up.

With the strongest revenue profiles in the sector, the company is carving its niche in India’s evolving green metals story. But what exactly does it do, and what makes its model stand out in this fast-emerging space?

What powers Jain Resource recycling?

Jain Resource Recycling operates as a vertically integrated non-ferrous metal recycling business, processing scrap materials procured both domestically and internationally.

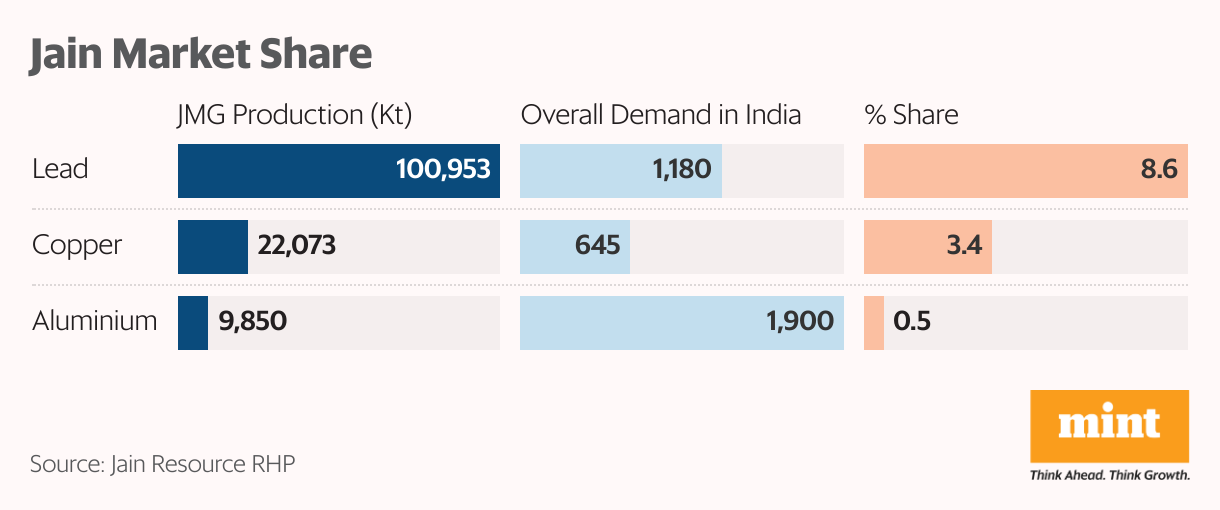

Its core business involves manufacturing non-ferrous metal products (lead, copper, and aluminium) by recycling non-ferrous metal scrap. It boasts a strong market position, commanding 8.6% market share in lead, 3.4% in copper, and 0.5% in aluminium.

Sourcing advantage exposes it to geographic risk

The company caters to various industries, including lead-acid batteries, electronics, pigments, and automotive. Jain has an extensive global sourcing network, procuring bulk raw materials directly from overseas scrapyards in over 120 countries through advance payments. This direct sourcing advantage ensures a steady supply, reduces dependence on intermediaries, and helps lower procurement costs.

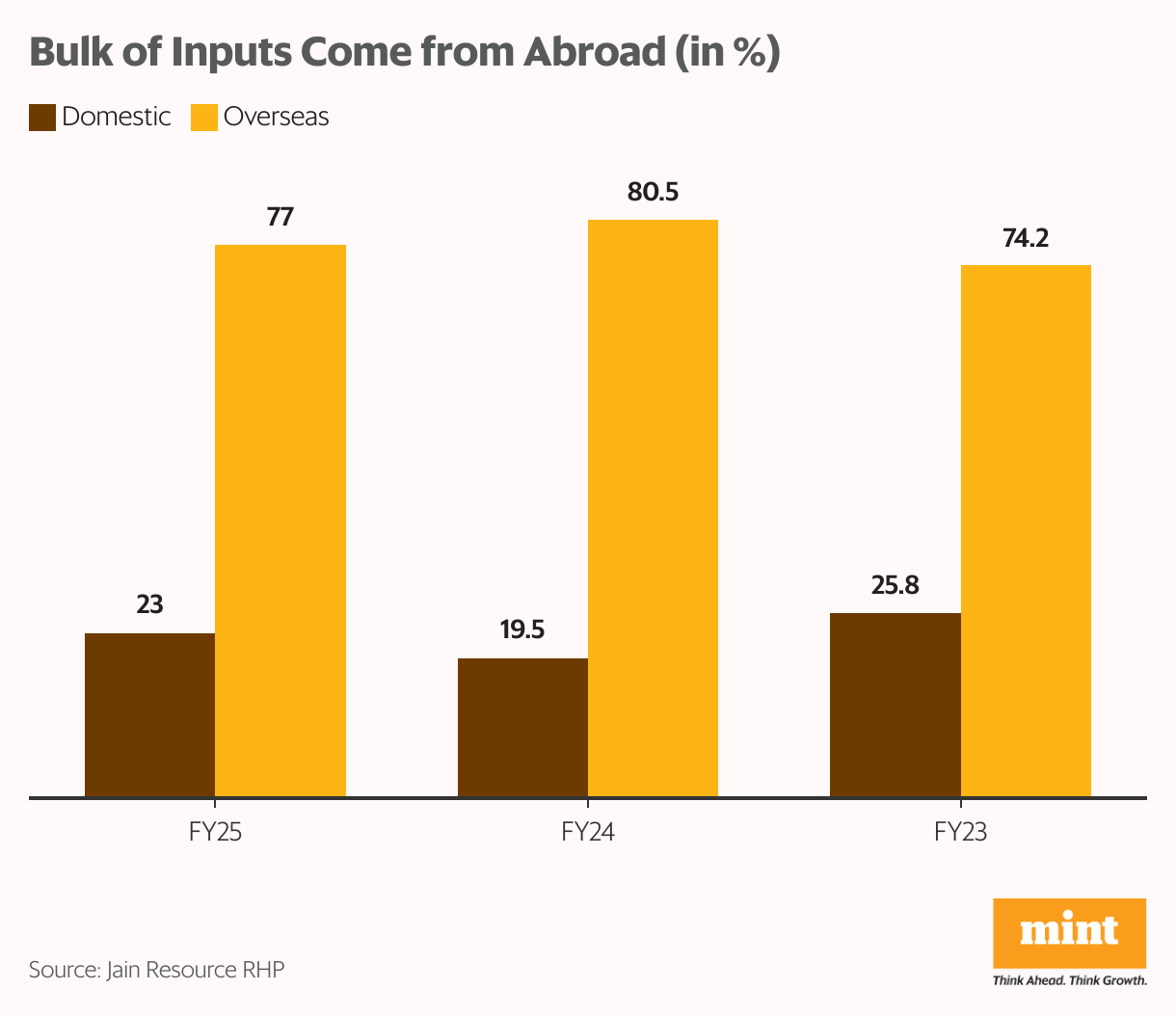

However, this dependence also exposes it to geographical risk. In FY25, Jain imported around 77% of its scraps from abroad and sourced the rest domestically. Such high import reliance makes it sensitive to geopolitical developments, logistics constraints, and regulatory shifts in key sourcing regions.

Jain leads the market through plant network

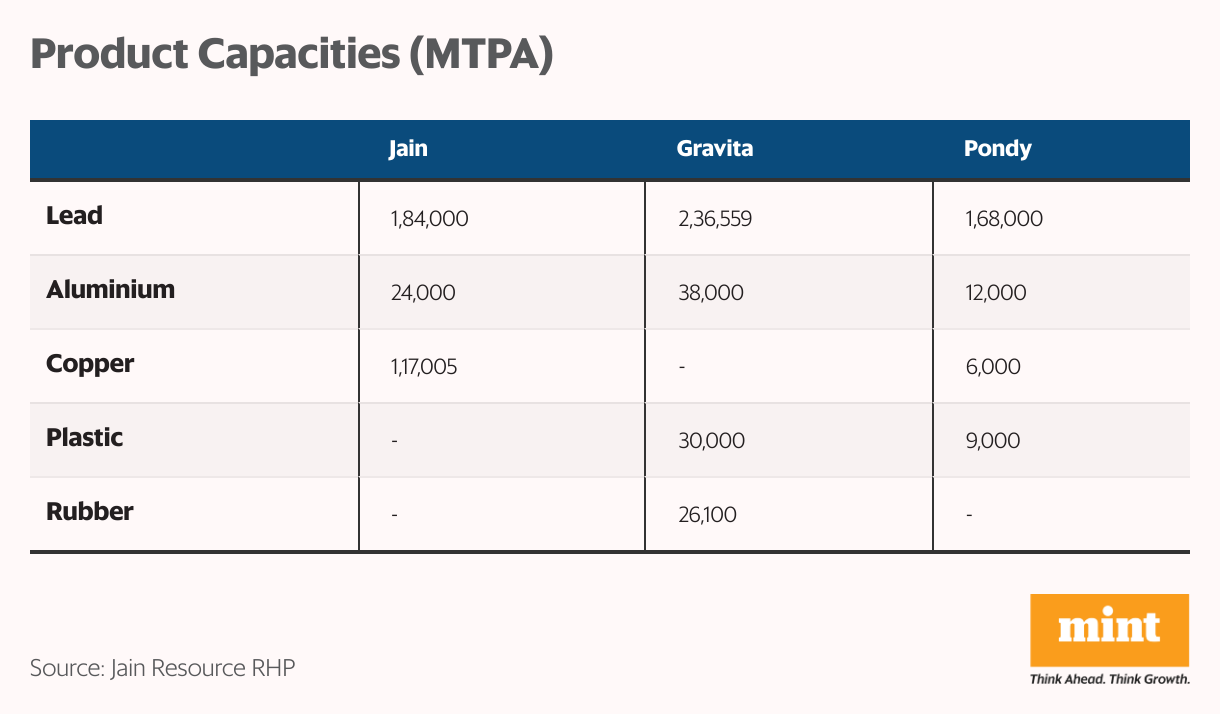

These imported and domestic scraps are then processed across four plants– three recycling facilities in Chennai and one Segregating Facility in Krishnagiri, Tamil Nadu. Notably, the company has the second-largest lead and aluminum recycling capacities in India after Gravita. In copper, however, Jain holds the leading position, followed by Pondy Oxides, as Gravita currently does not operate in this segment.

Jain is expanding into high-demand and high-margin copper cathode and wire rod manufacturing. To capitalize on higher lead demand, it has begun extracting tin to produce crude tin and lead tin ingots. Similarly, it has also started to manufacture PPVC granules and PVC granules from recycled plastic. These expansions are expected to increase profitability as they do not incur raw material costs. The company has also maintained healthy utilization levels of around 70%, reflecting steady demand.

In addition, all these recycling plants are strategically located within the SIPCOT Industrial Estate (Chennai), close to the Chennai, Ennore, and Katupalli ports. This proximity provides a logistical advantage for both imports and exports, particularly to China and Southeast Asia. Together, these plants form an integrated base, enabling the company to process multiple metal streams under one roof.

High customer stickiness drives growth

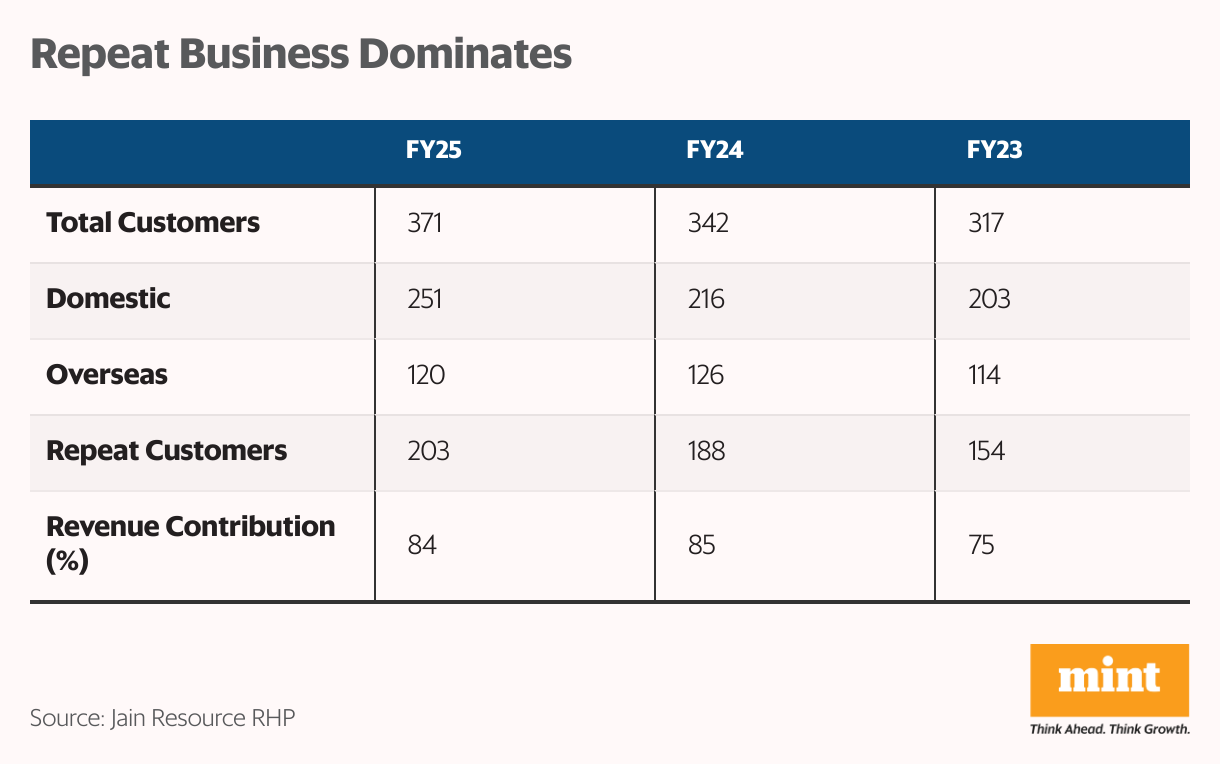

The company’s customer base spans 371 clients–251 domestic and 120 overseas. Jain also faces client concentration risk, especially from the top customer, which contributes 19% of revenue, and the top 10 (58.4%). However, the company’s strength lies in its high customer loyalty, which promotes repeat business.

Of its total clients, 203 are repeat customers, a number that has steadily increased from 154 in FY23 and 188 in FY24. This loyalty also translates into consistent revenue visibility. Repeat customers contributed 81.4% of the average revenue during the last three years. This stickiness benefits Jain from economies of scale, competitive costs, and increased geographical reach.

Lead and copper drive the revenue mix.

Jain Resource’s product portfolio is composed of five main segments. The largest revenue driver is copper and copper ingots, which contributed 44.8% of FY25 revenue. It is a leading recycler of copper scrap, including wires, cables, and electronic waste, supplying both domestic and international markets.

Next comes Lead and Lead Alloy Ingots, produced by recycling used lead-acid batteries and various types of lead scrap. This segment accounted for 39.5% of revenue in FY25. Notably, Jain’s lead ingot is a registered brand on the London Metal Exchange (LME), providing it access to a global customer base and the benefit of LME reference pricing. The refined lead brand, “Jain 9998,” is also approved by the Multi-Commodity Exchange (MCX).

![[ Insert title here ] (Table)](https://datawrapper.dwcdn.net/S1yAB/full.png)

The third segment covers precious metals, specifically gold refining, which contributed 9.8% of revenue. However, this business was discontinued from 15 April 2025 due to low margins and volatility in the gold refining sector. The fourth segment is aluminum and aluminum alloys, accounting for 3.8% of revenue, produced by recycling aluminum scrap. The recycled aluminum is supplied to industries including automotive, construction, and packaging.

Finally, the company also engages in domestic and international trading, including high-seas trading of non-ferrous metals and other commodities such as nickel cathode, silicon metal, tin ingots, and zinc ingots on an opportunistic basis. This contributed 2.03% of FY25 revenue. This diversified product portfolio enables Jain to navigate different business cycles across end-use industries, reducing dependence on any single segment.

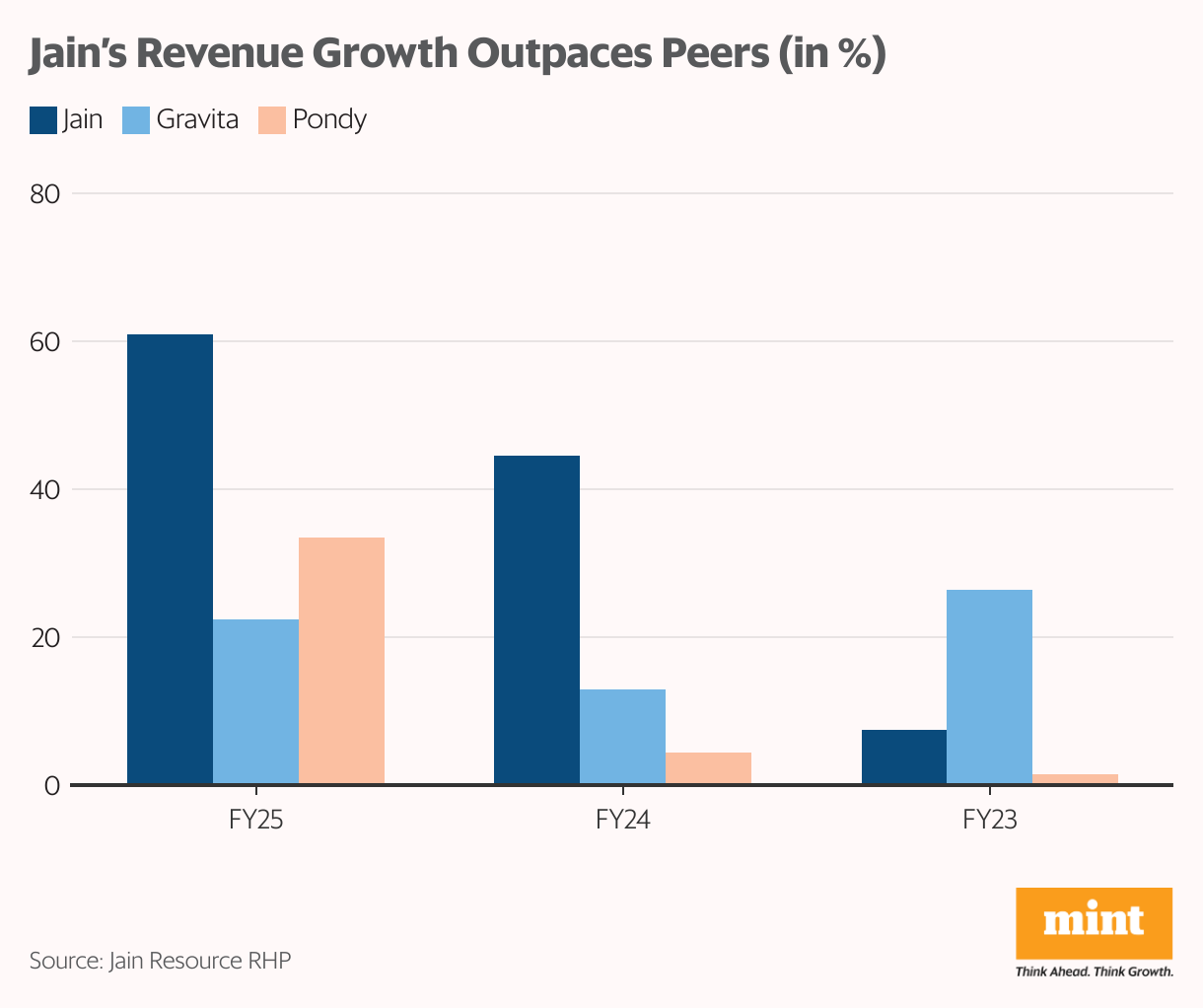

Outpacing peers, but what’s driving its growth?

Jain is the fastest-growing recycling company in its segment, with revenue more than doubling from ₹3,064 crore in FY23 to ₹7,126 crore in FY25. This growth significantly outpaces peers such as Gravita (up 38%) and Pondy Oxides (up 39%).

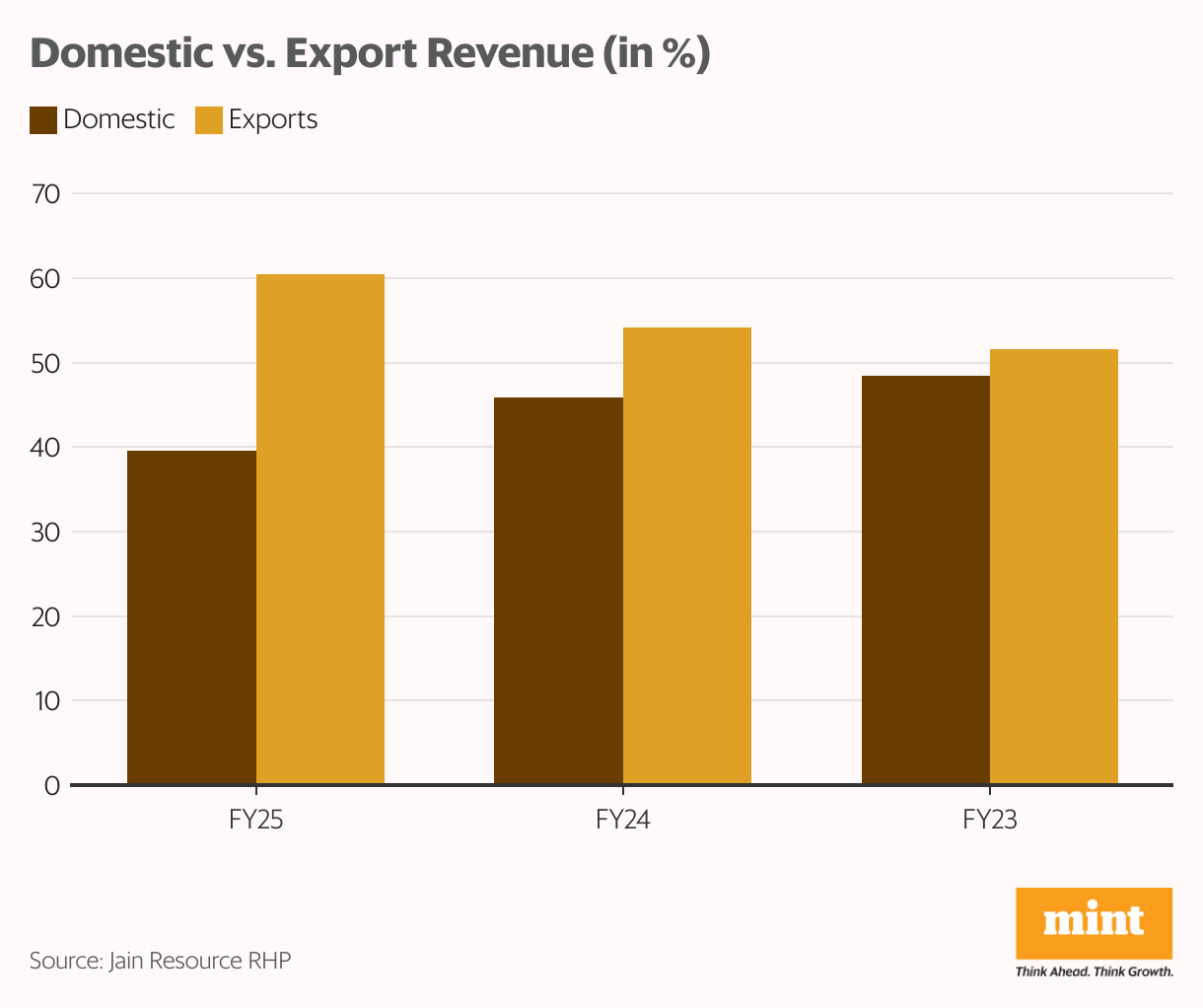

A key driver behind this expansion is the steady increase in fixed-asset turnover, which increased from 48 to 83 during this period. Growth is particularly fueled by higher sales of copper and copper ingots, as well as lead and lead alloy ingots. However, the company gets 60.4% of its revenue from exports and the balance from the domestic operations, which also exposes it to geopolitical and currency risks.

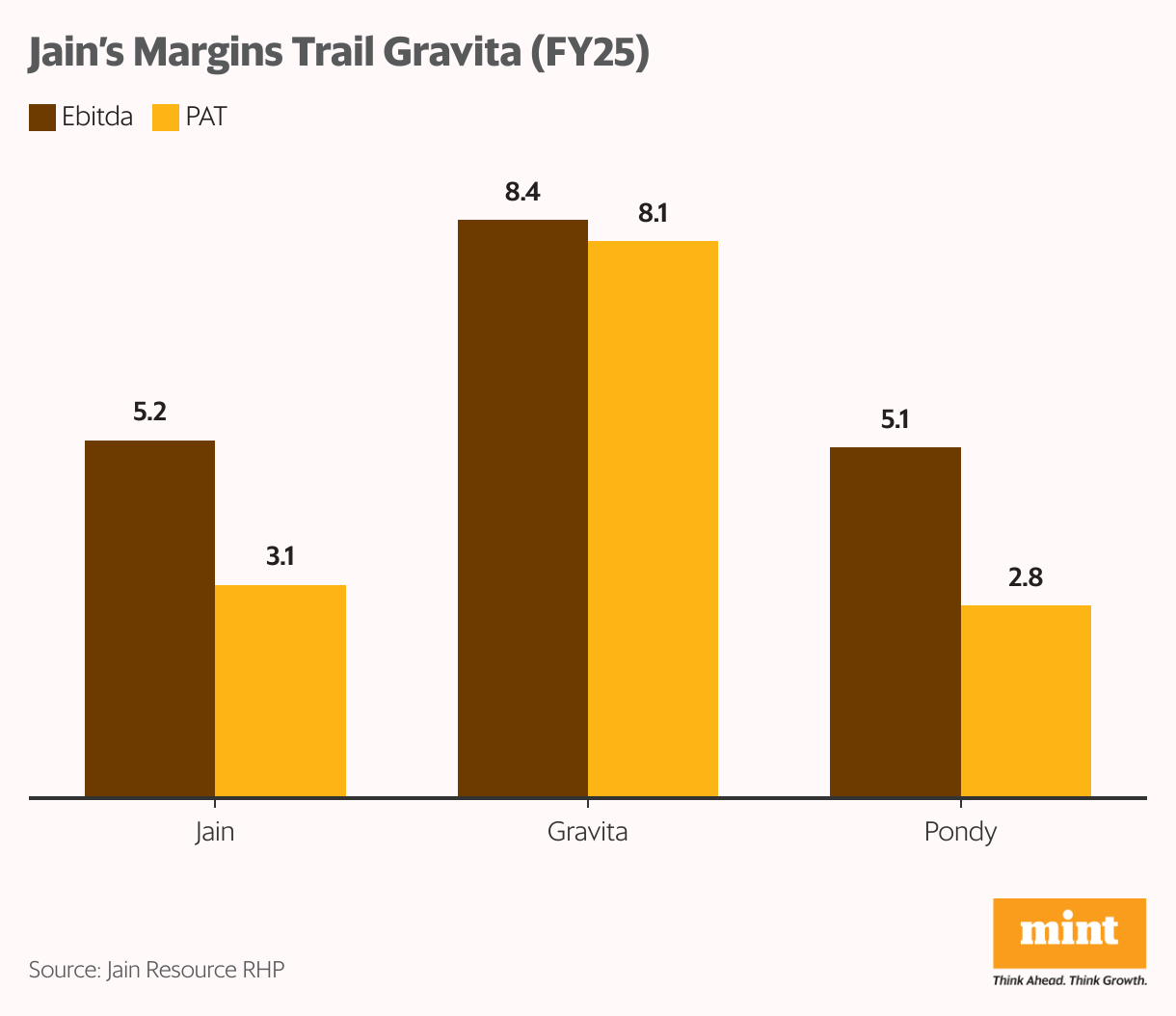

High revenue, but why is profit still behind Gravita?

However, this should not be a cause for concern, as Gravita and Pondy also derive 64.5% of their revenue from exports. On the profitability front, however, the picture is more mixed. Jain’s Ebitda margin stands at 5.2%, in line with Pondy Oxides (5.1%) but below Gravita (8.4%). PAT margin is also lower at 3.1%, trailing Gravita (8.1%) but ahead of Pondy (2.8%).

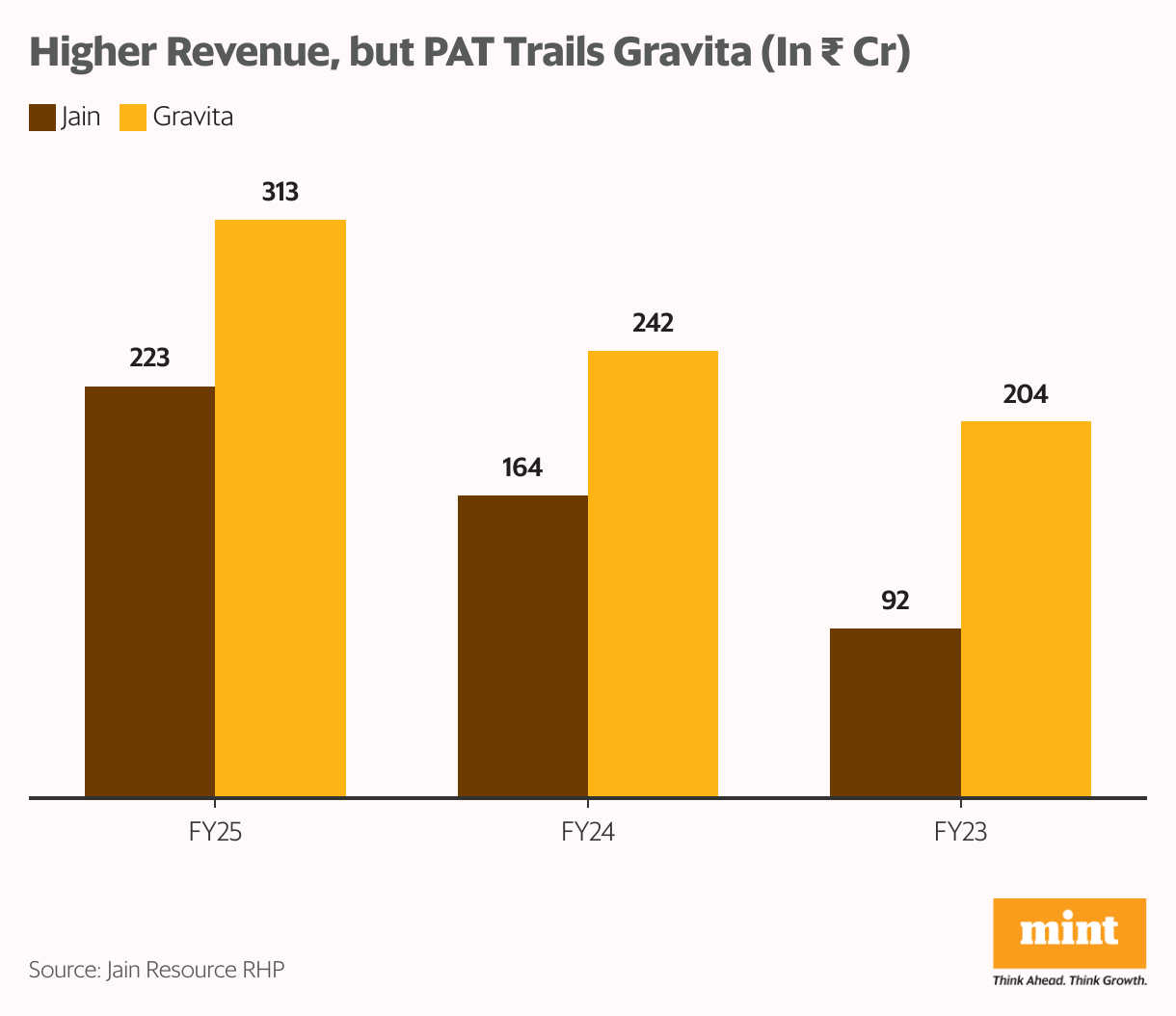

That is why, despite nearly double the revenue of Gravita ( ₹3,869 crore), Jain’s PAT of ₹223 crore (up 142% since FY23) remains below Gravita’s ₹313 crore. However, Management is focused on improving margins through debt reduction and cost control, while expansion into higher-margin segments could further support profitability. Its financial leverage is strong with a net debt-to-equity ratio of 0.92.

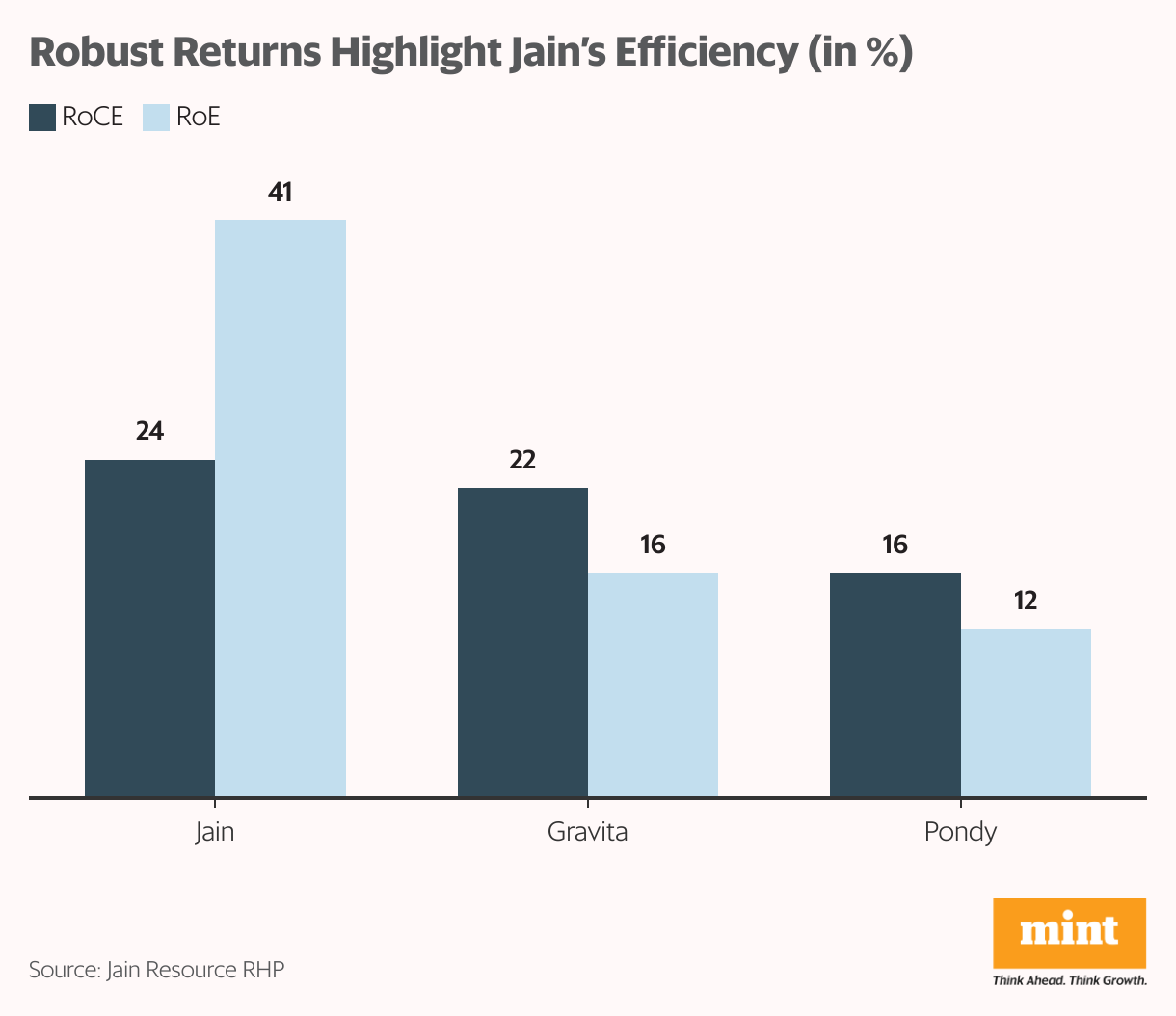

Despite lower margins, Jain leads in returns. Operating leverage has driven its Return on Capital Employed up to 24% from 12% in FY23. Return on Equity has moderated to 41% from 60%, but remains robust. These levels are also substantially higher than Gravita (16%, 22%) and Pondy Oxides (16%, 12%), highlighting efficient capital utilization.

Valuation leaves little room for missteps.

At a share price of ₹328, Jain trades at a price-to-earnings multiple of 54x, comparable to Pondy Oxides (53x) but at a premium to Gravita (35x). While the company is well-positioned to benefit from structural growth trends in the recycling industry, valuation leaves little room for error. Any slowdown in revenue or margin growth could lead to a sharp derating.

Risks also remain, as Jain operates in a cyclical commodity business with volatile prices. The company partially mitigates this through hedging its raw material purchases, helping cushion against market fluctuations.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.