The US Federal Reserve cut the key interest rate on Wednesday—a first in this calendar year. After the latest 25-basis-point reduction, more easing may be in the offing by the US Fed. Given persistent weakness in the US dollar, easing monetary policy could lead to reallocation of foreign funds towards other assets such as emerging market (EM) and Asian equities.

Usually, a weaker dollar and a more accommodating US monetary policy tend to boost EM equities and currencies, especially those with strong growth potential. But this time, the impact of trade tariffs on various Asian economies would be a critical variable for foreign investors while rejigging portfolios. This means fund inflows to EMs, if any, may be selective.

“Technology-heavy markets such as Taiwan and Korea will likely see continued interest as the AI-driven capex boom is set to continue into 2026. Markets whose economies are heavily geared to Chinese demand may continue to lag, with an example being Thailand, where the tourism sector in recent years has focused on Mainland Chinese tourism flows. The same can be said for the Philippines, to a lesser extent,” Stefan Hofer, chief investment strategist APAC at LGT Private Bank, told Mint. In China itself, preference is for the large technology names, in part because they are not directly impacted by punitive US import tariffs, he added.

Most Asian equity markets, including India, have seen steep outflows so far in 2025 (See chart). In India, domestic institutional investor flows have been resilient, but they may not be enough. “While domestic flows put a floor on markets, keeping them from correcting too much, it is FII inflows that are needed for markets to rise sharply,” said HSBC Global Investment Research’s 17 September report.

India’s domestic growth slowed while valuations were still elevated, leading to the relative underperformance of Indian stocks. In 2025 so far, the MSCI India index is up 6% compared to over 20% returns each for the MSCI Asia Ex-Japan and MSCI Emerging Markets indices. Even so, at one-year forward price-to-earnings, MSCI India is trading at 20x, a premium to Asian peers, showed Bloomberg data.

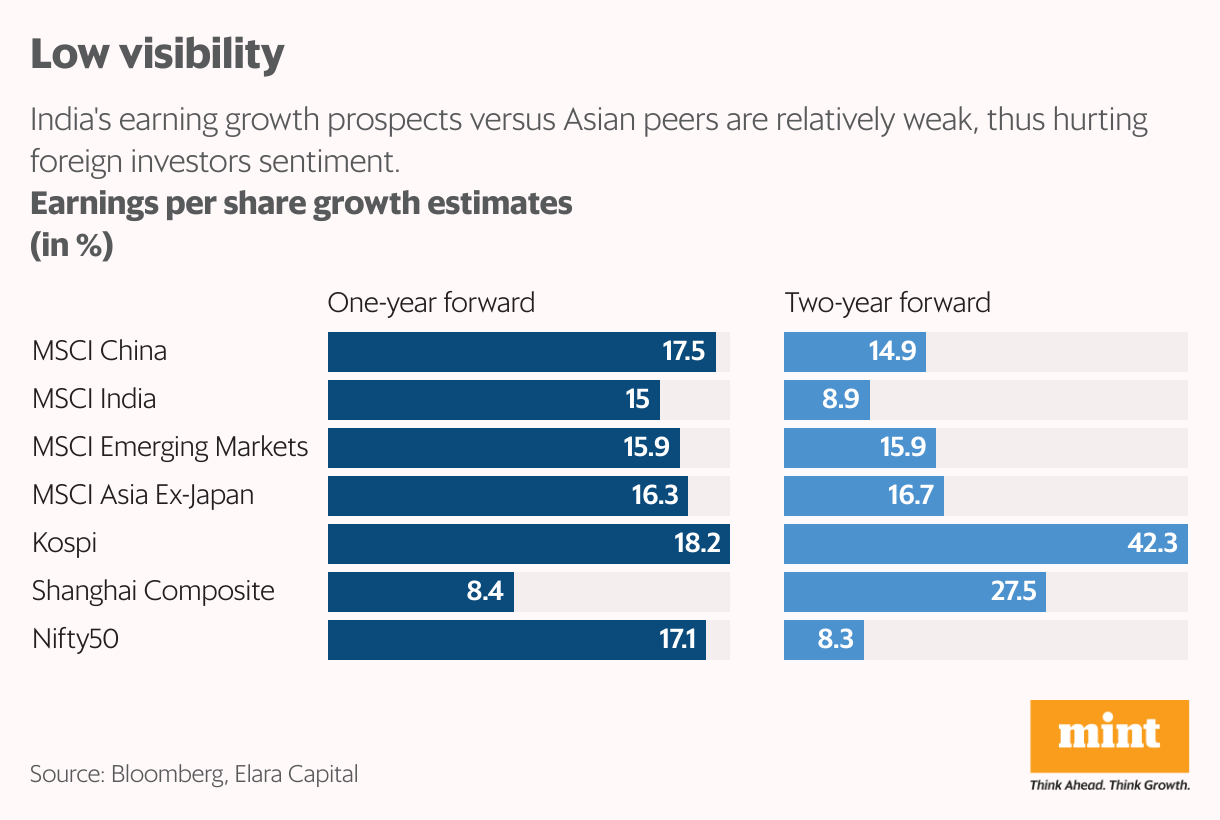

Plus, India Inc’s earnings growth prospects are unexciting. Despite the recent market correction, the earnings outlook for India remains a bit challenging vis-à-vis its counterparts. “Compared to peers KOSPI (42.3%), Shanghai Composite (27.5%) and broader emerging markets (~16%), Nifty 50’s 8.3% CY26 earnings per share growth estimate remains low,” said Garima Kapoor, economist & EVP Elara Capital. “Lower earnings visibility versus peers is a deterrence for FIIs to return in Indian equities even though a benign US Dollar is a positive,” she added.

Meanwhile, widely held expectations are that the rationalization of the goods and services tax, along with income tax cuts, may increase disposable incomes and revive consumption. This should eventually augur well for corporate earnings growth. Also, with retail inflation at comfortable levels, the clamour for more easing by the Reserve Bank of India, which meets in October, is getting louder. This should also aid demand in interest-rate-sensitive sectors.

“Tax cuts can help boost consumption over the near term, but investment and wage growth will have to pick up for a more sustained revival in consumption,” added the HSBC report. Moreover, among the other concerns, private capex is muted. Against this backdrop, investors must also note that the supply of equities is at a record high and new stock issuances can exceed domestic demand, leading to equity oversupply.