Domestic capital inflows into private equity- and private credit-led Category II alternative investment funds slumped to a five-quarter low of 4% in the April-June quarter, the analysis shows. In contrast, Category III funds continued to draw steady inflows, outpacing both Category I and II funds for a fifth straight quarter.

Alternative investment funds collect funds from other investors to invest in companies or projects. Category I AIFs include venture capital and infrastructure funds, while private equity and debt funds fall under Category II AIFs. Category III AIFs such as hedge funds have a higher risk appetite with aggressive investment strategies such as using algorithms for automated high-frequency stock trading.

The Delhi High Court recently clarified that Cat III AIFs with clear disclosures of beneficiaries will only attract short-term and long-term capital gains taxes, and not an automatic maximum marginal rate of 40%.

With clearer tax rules and strong distribution incentives, wealth managers are likely to ramp up Category III AIF offerings this year, predict market experts.

Domestic inflows into Category III funds grew 66% year-on-year in the April-June first quarter, over twice the growth of Category II funds, show data from the Securities and Exchange Board of India.

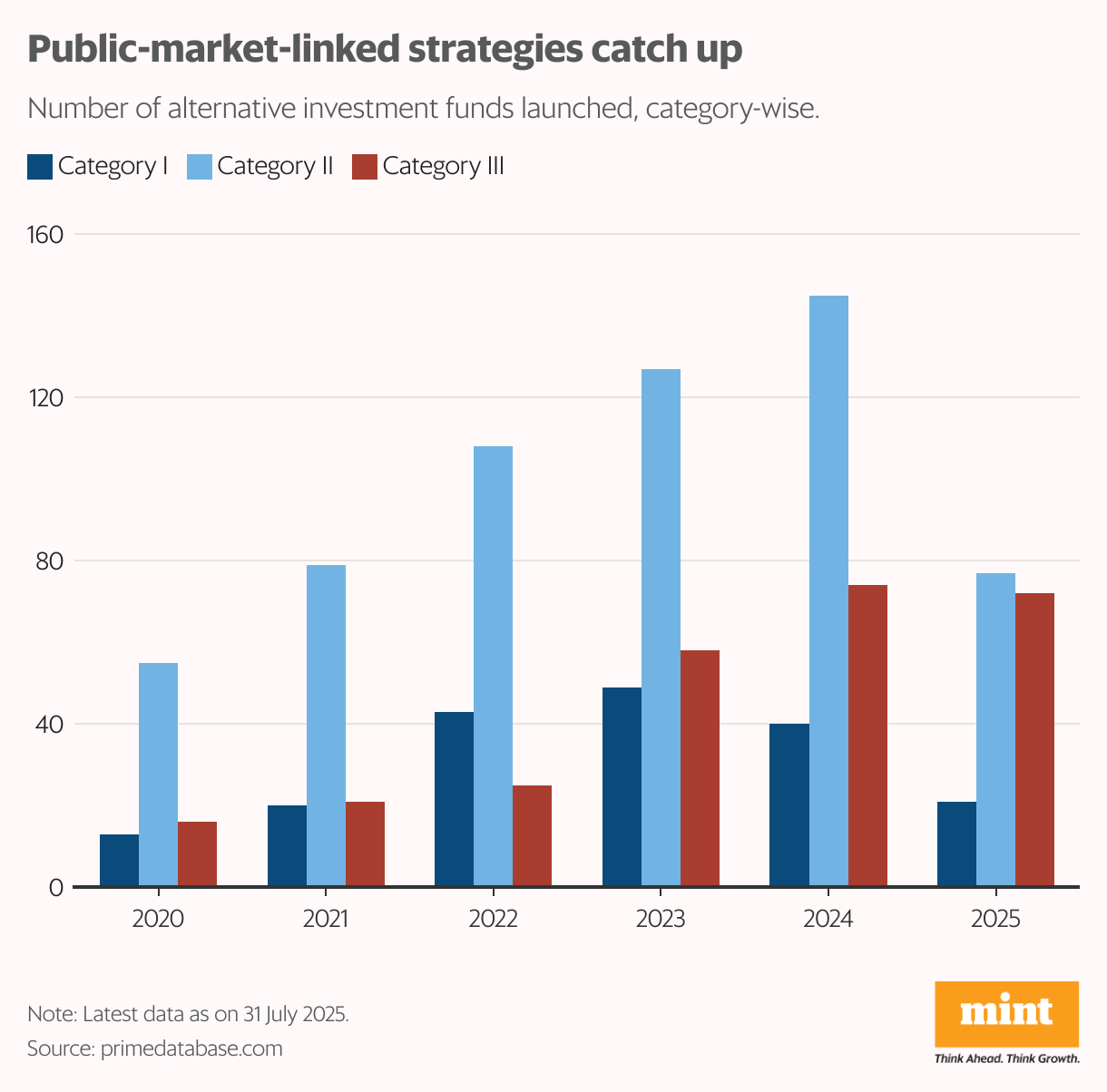

A separate analysis of PRIME Database’s AIF data shows that with 72 launches so far this year, Category III funds are on track to surpass last year’s 74.

The surge in Category III fund launches reflects growing client confidence that tech-driven stock selection can deliver better returns even in a slow equity market, said Srikanth Subramanian, chief executive and co-founder of Ionic Wealth, a wealth management platform.

Higher demand for a variety of liquid investments and clearer rules on Category III fund taxation have helped boost interest, he added.

Shifting winds

Category III funds, despite their appeal, were constrained by complex and unclear tax rules, while Category II funds, though illiquid, are popular because they don’t attract taxes, said Tushar Sachade, partner at Price Waterhouse and Co. Llp.

This is evident in the numbers. Category II funds attracted domestic inflows worth ₹2.17 trillion in the June quarter, while inflows into Category III funds were around ₹1.55 trillion, Sebi data show.

“There is ample appetite for Cat II funds,” Sachade said. “But lack of quality investment opportunities and tighter exit conditions may limit fundraising.”

Global market fluctuations and sector-specific challenges, including the recent ban on online gaming platforms involving real-money transactions, are putting pressure on deal valuations and affecting exit opportunities for mature private equity portfolios, according to Ionic Wealth’s Subramanian.

Limited price discovery and cautious market sentiment are making secondary PE-to-PE investment sales more challenging, causing many early-stage funds to accept lower valuations, he added. “Also, softer IPO sentiment earlier this year reduced liquidity and dampened exit activity for growth and late-stage funds.”

In such a scenario, fewer PE‑backed companies might list on public markets this year, said Pranav Haldea, managing director of PRIME Database Group. “… They might defer exits in search of stronger pricing.”

That said, India’s equity market is seeing a significant increase in IPO activity after a lull earlier this year. Experts, however, said investors might still hold back for a more opportune time to make their bets.

Price Waterhouse’s Sachade said investors often demand 5-7% additional returns over liquid alternatives while locking up capital in private markets.

“But in a tight market, generating that illiquidity premium becomes increasingly challenging, particularly in PE investments,” said Feroze Azeez, joint CEO of Anand Rathi Wealth. “This has mainly cooled appetite for Category II funds, pushing some… toward public allocations.”

Azeez anticipates a surge in Category III fund launches this year, as these are also typically easier to distribute among a broader investor base. While product launches are more performance-driven in the private market, supply often creates its own demand for new public-market products, he added.

Chasing fat purses

Unlike mutual funds, which are low-cost products and allow limited distributor earnings, portfolio management services (PMS) and AIF structures typically provide higher revenue opportunities for wealth managers through fat distribution commissions and management fees, Azeez said.

Over time, this difference in economics leads wealth managers to gradually tilt client portfolios toward PMS and AIF allocations, helping them maintain better return on assets, he added.

Centrum Broking in a recent report said AIF and PMS distribution yields for 360 ONE Wam Ltd, India’s largest wealth franchise, were 0.72-0.84% in the June quarter, higher than the 0.42-0.46% yields for mutual funds and 0.28-0.30% for advisory mandates.

Such AIF yields provide wealth houses with a steady stream of highly profitable annual recurring revenue, helping offset revenue cyclicality and rising operating costs.

360 ONE plans to roll out one alternative strategy product every quarter, with its AIF assets under management climbing 13% year-on-year in the first quarter, the firm’s management team said during the June-quarter earnings call.

“The rise in alternatives is not just a passing trend but a structural shift (in the wealth management industry),” Anshuman Maheshwary, chief operating officer at 360 ONE, told Mint. As wealth creation accelerates, flows into alternative assets will only grow stronger, he added.

Listed peers Nuvama Wealth Management Ltd and Anand Rathi Wealth Ltd also reported strong revenue and margin growth from AIF distribution in the first quarter, while Motilal Oswal Financial Services Ltd’s PMS and AIF net flows turned positive after last year’s outflows.

“Wealth houses which can steadily shift business mix toward annuity-like fee streams will benefit disproportionately going ahead,” said Alekh Yadav, head of investment products at Sanctum Wealth.

Large family offices, however, will continue diversifying across products and favour managers with proven track records, said Price Waterhouse’s Sachade.