For years, performance remained subdued. But with the demerger, management looked to reset the growth path and outlined a strong expansion plan. The company’s goal is to transform each of its four flagship labels into ₹2,500-crore brands by FY30, by capitalising on India’s rising discretionary spending and evolving fashion aspirations.

The government’s decision to cut the Goods and Services Tax (GST) on apparel priced below ₹2,500 to 5% has given this ambition a fresh impetus. The question now is how well-placed the company is to deliver on its goal.

Business breakdown

ABLBL operates through two segments:

- Lifestyle brands, which includes its four flagship labels Louis Philippe, Van Heusen, Peter England, and Allen Solly along with the international brand Simon Carter.

- Youth brands and innerwear, which houses American Eagle, Van Heusen Innerwear, and Reebok.

Lifestyle brands show signs of recovery in Q1FY26

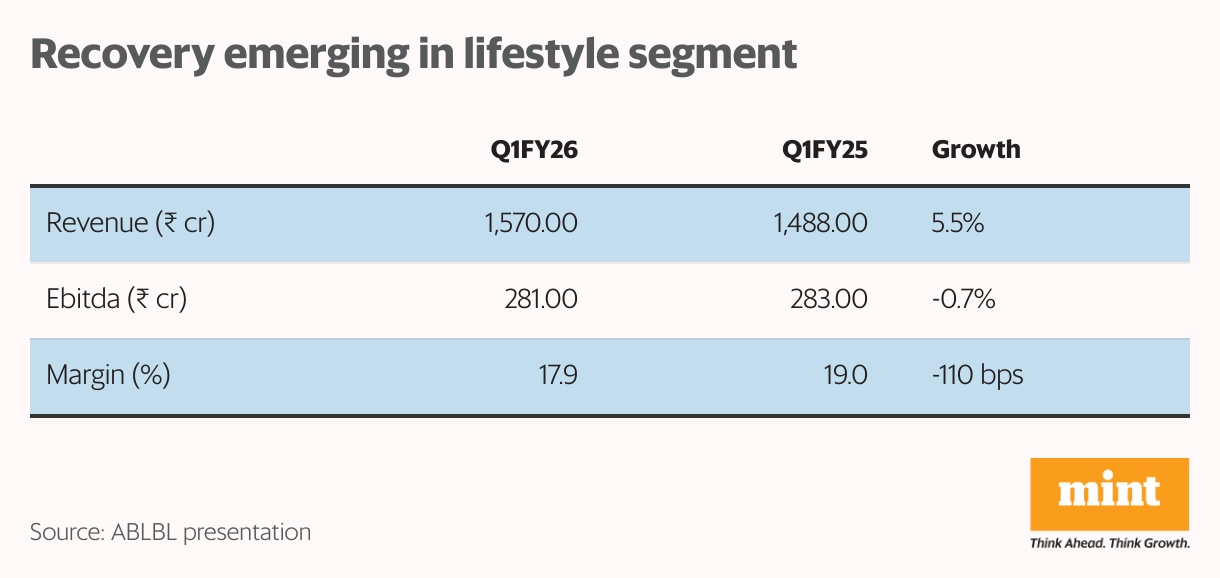

Lifestyle brands continue to dominate both revenue and profitability. In Q1FY26, segment revenue increased 5.5% year-on-year (yoy) to ₹1,570 crore, accounting for 84% of total revenue. The company reported 15% like-to-like (LTL) growth led by strong double-digit growth across all brands.

This marked the fourth consecutive quarter of robust LTL growth, after 9% in Q3 and 12% in Q4 of FY25. In terms of profitability, the lifestyle segment contributed 97% of total Ebitda. With its mature portfolio, it also sustained a healthy margin of 18%.

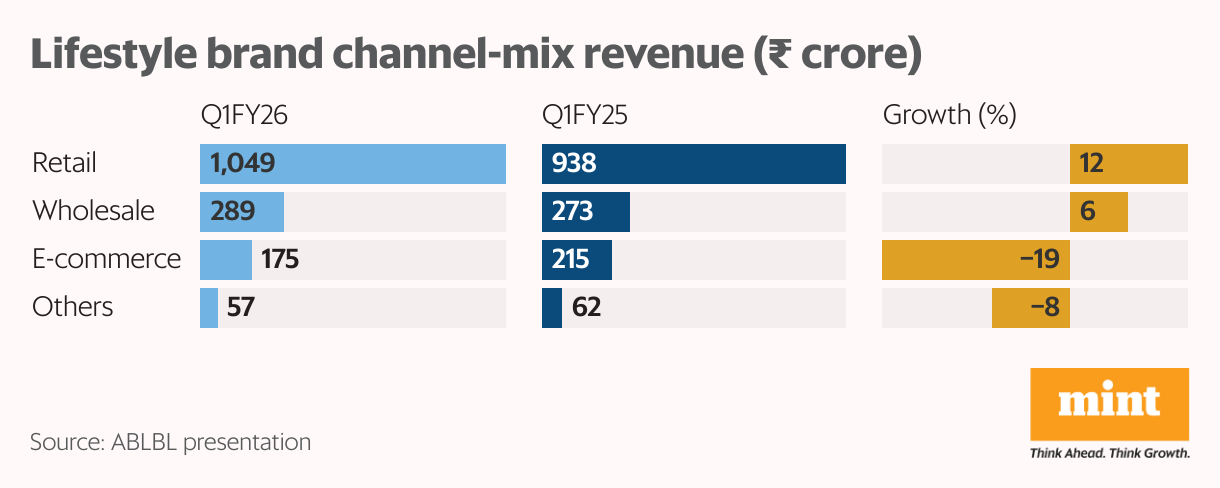

Within the channel mix revenue, retail sales grew 12% to ₹1,049 crore, reflecting a rebound in demand. Small towns in particular delivered double-digit growth in LTL. Wholesale rose 6% to ₹289 crore, while e-commerce declined 19% to ₹175 crore as it prioritised profitability and moved towards uniform pricing across channels.

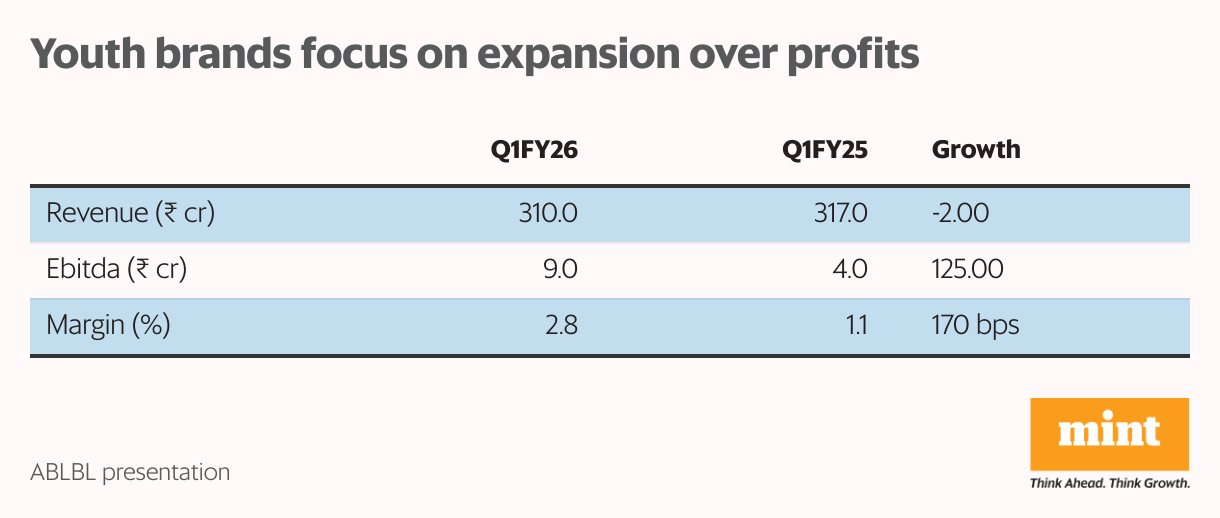

The youth brands and innerwear segment, meanwhile, reported 2% yoy decline in revenue to ₹310 crore owing to the closure of Forever21 stores. The segment accounted for 16% of revenue. Ebitda, however, more than doubled to ₹9 crore from ₹4 crore in Q1FY25 as Van Heusen Innerwear’s losses halved. As a result, margins expanded by 170 basis points (bps) to 2.8%.

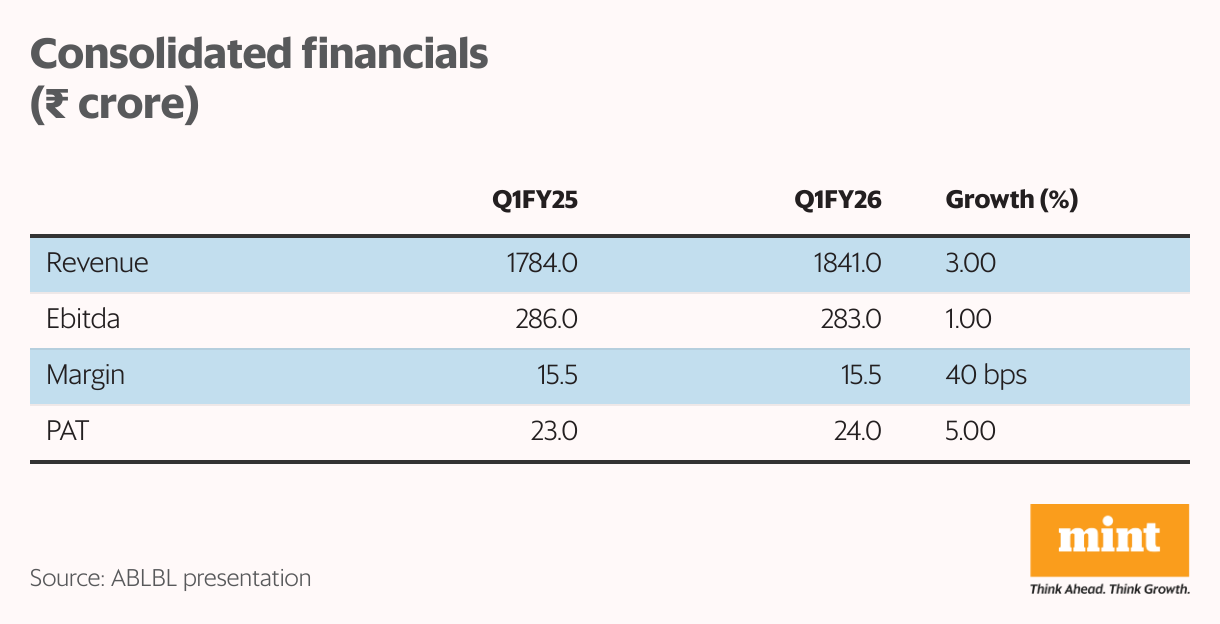

At the consolidated level, the company reported modest 3% revenue growth to ₹1,841 crore in Q1FY26. Growth lagged peers in the branded apparel space, despite a low base and seasonal boost from wedding-related footfalls. On the positive side, gross margins expanded by 375 bps to 62.6%, supported by a better channel mix, closure of unprofitable stores, and lower markdowns.

However, Ebitda margin fell 40 bps to 15.5% as the company increased advertising during the Indian Premier League. Profit after tax (PAT) rose 5% to ₹24 crore, aided by lower depreciation, higher other income, and a reduced tax rate. Management reiterated its target of doubling revenue over FY24-30, translating to a compound annual growth rate above 11%.

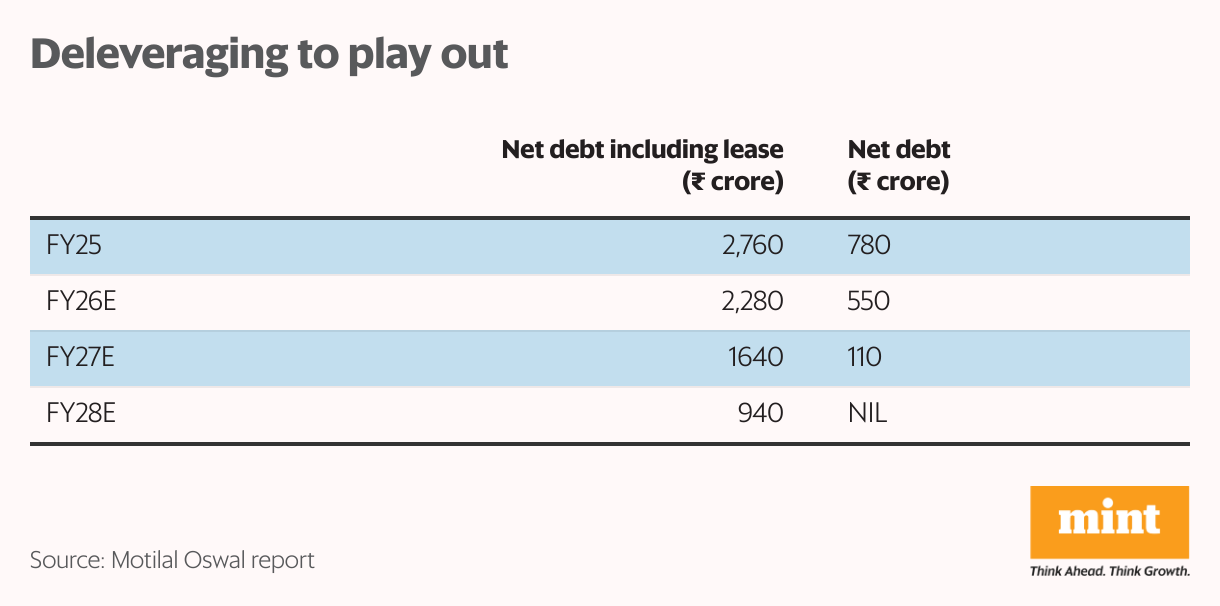

ABLBL is also working to strengthen its financial position. It aims to be net-debt-free (excluding leases) in the next two to three years by paying off ₹200-300 crore of debt every year. It paid ₹382 crore as finance charges in FY25 and this reduction in debt will also improve the bottom line.

With profitability improving, management aims to generate strong free cash flow by FY30, paving the way for dividend payouts. The company’s return ratios are also expected to rise meaningfully.

Lifestyle brands: core growth driver

This growth will be led by lifestyle brands, where management expects low double-digit growth. This expansion is expected to be driven by a growing store network and sustained LTL momentum. As of Q1FY26, ABLBL had over 3,230 stores covering 4.6 million sq ft of retail area, of which more than 2,800 belonged to its four flagship brands.

Small-town expansion remains central to the company plans. It currently has 569 stores in small towns and plans to increase this more than 1,000 in the coming years. It plans to open 250 stores a year and has a target of 4,500 stores by FY30. The average store size will also be increased from 1,400 sq ft to 2,000 sq ft for a more premium experience as the company is not only looking to expand its footprint but to make its stores more productive as well.

ABLBL has aggressive expansion plans

View Full Image

Currently, 70% of the company’s stores operate under the asset-light franchise-owned model, and it plans to maintain the same mix going forward. With a faster retail expansion, management expects the share of retail in the overall business mix to be about 70% by FY30, from 62% in FY25. This is also expected to improve the Ebitda margin by 300 bps to over 18%.

In FY24, Louis Philippe and Van Heusen reported revenues of around ₹2,000 crore each, Allen Solly ₹1,400 crore, and Peter England ₹1,250 crore. Louis Philippe has already surpassed 1,000 stores. The goal is to turn at least three of these into ₹2,500-crore brands with more than 1,000 stores each by FY30. Brand-wise numbers for FY25 are not available.

Focus on growing core premium brands

View Full Image

Scaling youth brands and innerwear

Management aims to grow the youth brands and innerwear segment at 15-25% a year by expanding Reebok, American Eagle and Van Heusen innerwear over the next two to three years.

After acquiring the distribution rights for Reebok across India, Bangladesh, Bhutan, the Maldives, Nepal, and Sri Lanka in October 2022, the company is gradually ramping up the business. Reebok was struggling, but ABLBL’s investment has begun to yield results. This is evident in its FY24 revenue of ₹450 crore, which was almost flat from FY20 ₹430 crore.

Since ABLBL’s acquisition, Reebok has grown about 2.5-fold to nearly ₹500 crore with a doubling of its retail footprint and a clean-up of old inventory. The brand is expected to deliver over 20% annual growth in the long term, and double its revenue in the next three to four years.

Meanwhile, Van Heusen Innerwear reported revenue of around ₹500 crore in FY25 and is targeting ₹1,000-2,000 crore by FY30. Losses have already halved, with management indicating that revenue of ₹700-800 crore is needed to achieve single-digit profitability. The business is expected to break even by FY27.

Innerwear demand is showing signs of recovery, and the company anticipates a steady rebound in growth. It also plans to make American Eagle one of the top three denim brands in India with a revenue target of ₹500-1,000 crore by FY30.

What lies ahead?

ABLBL has re-entered the market with a clean slate after years of muted performance under its parent firm. The demerger allows management to sharpen its focus, while the company’s wide retail footprint and strong brand recall leave it well-placed to capture rising discretionary demand. Lifestyle brands will remain the core growth engine, but the scaling up of Reebok, American Eagle and Van Heusen innerwear could provide additional levers over the medium term.

Balance-sheet strengthening, margin expansion, and the goal of creating several multimillion-dollar brands add optimism to the long-term narrative. From a valuation standpoint, ABLBL trades at a price-to-sales multiple of 2.2, a premium to Raymond Lifestyle (1.2) and Arvind Fashion (1.5), but a discount to smaller peers Kiran Clothing (3) and Cantabil (2.8).

While others have seen valuations compress, ABLBL’s positioning remains relatively strong. With policy tailwinds such as GST cuts on mass apparel and income tax relief expected to boost discretionary spending, any meaningful revival in demand could drive the stock up.

For more such analysis, read Profit Pulse.

Madhvendra has over seven years of experience in equity markets and writes detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.