Corporate earnings have been largely muted owing to a slowdown in demand, which has weighed on investor sentiment. Global macroeconomic uncertainties, from renewed trade tensions to tariff-related jitters, have given them more reasons to be cautious.

But beneath the surface, a few stocks have staged powerful rallies fueled by strong earnings momentum, strategic expansion plans, and improving fundamentals.

What makes these stocks particularly interesting is that they haven’t just surged more than 30% so far this year but that they’re still trading around 20% below their 52-week highs. In other words, despite strong rallies, they may still have room to run up further.

If you’ve been sitting on the sidelines, looking for a big opportunity in this cautious market, here are three stocks that are worth a look.

#1 Narayana Hrudayalaya

Shares of the company are up 40% in 2025, yet 28% below their 52-week high of ₹2,372.

The stock has been on an upswing over the past few months for various reasons: growing capacities, diversifying into other fields, and improving operational efficiency.

Earlier in the year the company announced plans to add 1,535 beds by FY29, with a focus on strengthening its presence in existing locations: Bengaluru, Kolkata and Raipur.

It outlined a capex outlay of about ₹750 crore over the next three to four years, of which ₹300 crore will be used for routine maintenance and increasing capacity at existing facilities, while ₹450 crore will be earmarked for greenfield and brownfield expansions.

The company has also diversified into insurance services, aiming to improve healthcare access for the working class and poor. It has invested ₹1,000 crore in this vertical and plans to scale it up further depending on the initial outcomes. It is also eyeing aggressive growth in the primary healthcare segment, with plans to set up 50 clinics over the next year.

Narayana Hrudayalaya’s robust financials continue to underpin its expansion strategy. Over the past five years the company has delivered a steady 12% compound annual growth rate (CAGR) in revenue, driven by higher realisations, and an impressive 44% CAGR in net profit, reflecting its focus on operational efficiency and sustainable growth. Operating profit margins have followed suit, increasing steadily from 10.3% in 2019 to 23% in 2025.

This has resulted in healthy return ratios for the company. The three-year average return on equity (RoE) stands at 28.8% while the return on capital employed (RoCE) stands at 25.1%.

Despite this robust performance, shares of the company have declined 8.4% over the past month, following a minor dip in net profit for the June quarter. This has led to a slight valuation reset, with the stock now trading at a price-to-earnings ratio of 47.6, below its 10-year average of 50.2.

FIIs, however, increased their stake in the company from 9.66% in March to 10.46% in June after four consecutive quarters of decline. This rebound could indicate renewed confidence in the company, possibly driven by improved earnings visibility, expansion plans, or a more attractive valuation after the correction.

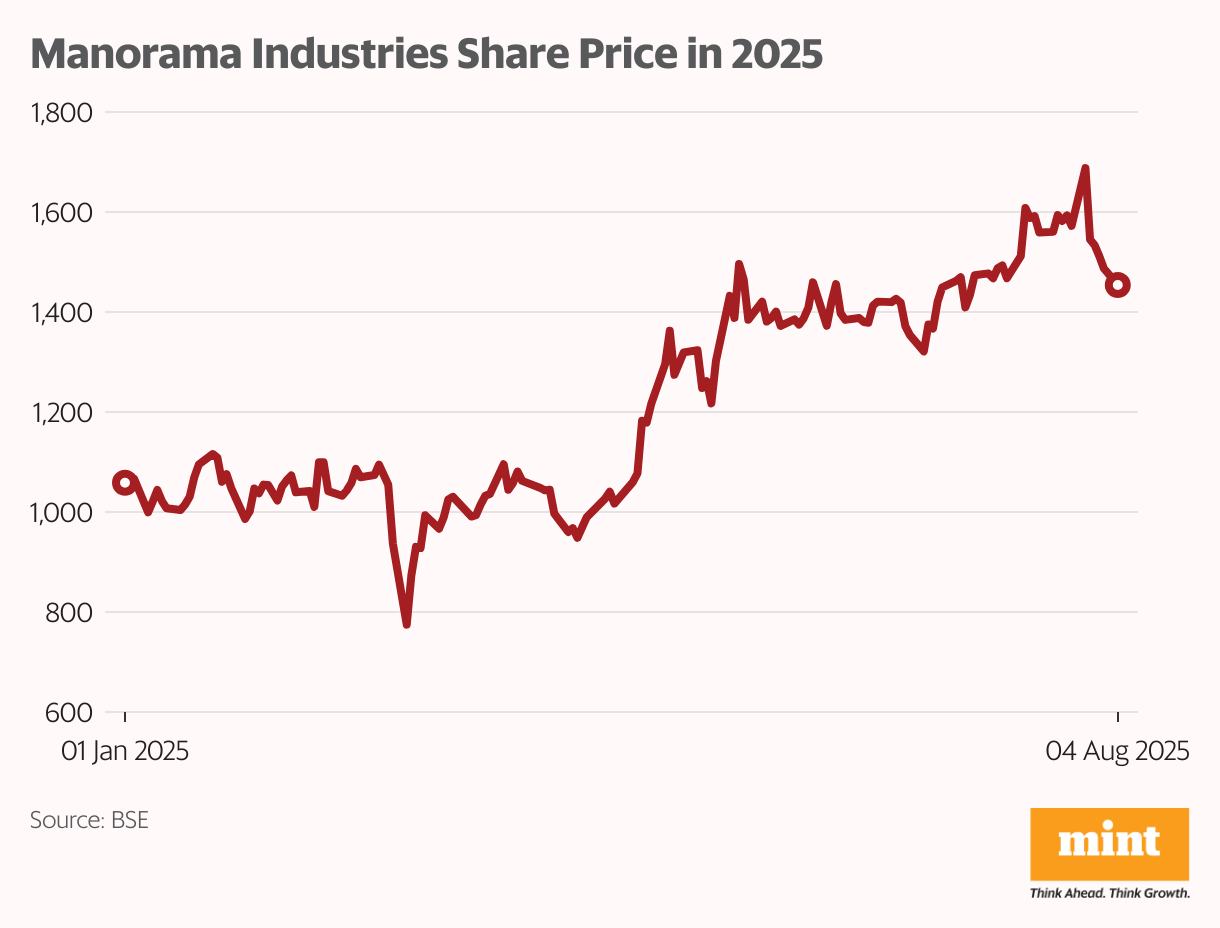

#2 Manorama Industries

Manorama Industries is one of India’s leading manufacturers of specialty fats and butters used in the chocolates, confectionery and cosmetics.

The stock is up 38% in 2025 on account of its strong financial performance over the past two quarters, yet 18% below its 52-week high. It has consistently generated returns over the past year, boasting a remarkable increase of 114%, significantly outpacing the Sensex’s 2.87% return.

Over the past four quarters the company consistently improved its financial metrics with higher capacity utilisation, improved product mix, and sustained export demand.

Revenue has grown steadily each quarter, from ₹133 crore in June 2024 to ₹195 crore in September 2024 and ₹290 crore in June 2025, likely driven by both volume gains and improved pricing power. Net profit grew from ₹14 crore in June 2024 to ₹51 crore by June 2025.

The company has also managed to expand its operating profit margin from 20% to 27%, indicating strong operating leverage and improved cost-efficiency as revenue scaled.

It aims for a top line of ₹1,050 crore in FY26, with 25-30% of the growth expected to come from higher volumes and another 5-10% from better price realisations. Revenue in FY25 stood at ₹771 crore.

A recent ramping up of capacity is also expected to contribute to this growth. In the September quarter of 2024 the company commercialised a new 25,000-tonne fractionation facility, taking total capacity to 40,000 tons per annum. With capacity utilisation projected at 75-80% in FY26, the company expects to achieve greater operating efficiencies and cost optimisation.

On the global front, Manorama has expanded its footprint through subsidiaries in West Africa, the UAE, and Brazil. The Latin American market, particularly Brazil, is seen as a major growth opportunity for its cocoa butter equivalent (CBE) and stearin products, with potential demand of 25,000-30,000 tonnes.

The company remains focused on retaining existing customers while steadily adding new ones without compromising on margins or return on capital.

Over the past five years revenue has grown at a CAGR of 33% while net profit has grown at 37%. Profitability metrics have remained healthy and stable, with a five-year average operating profit margin of 17.6% and an average net profit margin of 9.6%, reflecting strong cost control and consistent earnings quality. Return ratios have also held up well, with an RoE of 28% and an RoCE of 23%.

While the stock has delivered strong returns over the past year, it has slipped 1% over the last month amid broader market volatility and trades 17% below its 52-week high.

It has a PE ratio of 58.1, marginally below its 10-year average PE of 59.1, suggesting it may not be overheated despite the sharp run-up.

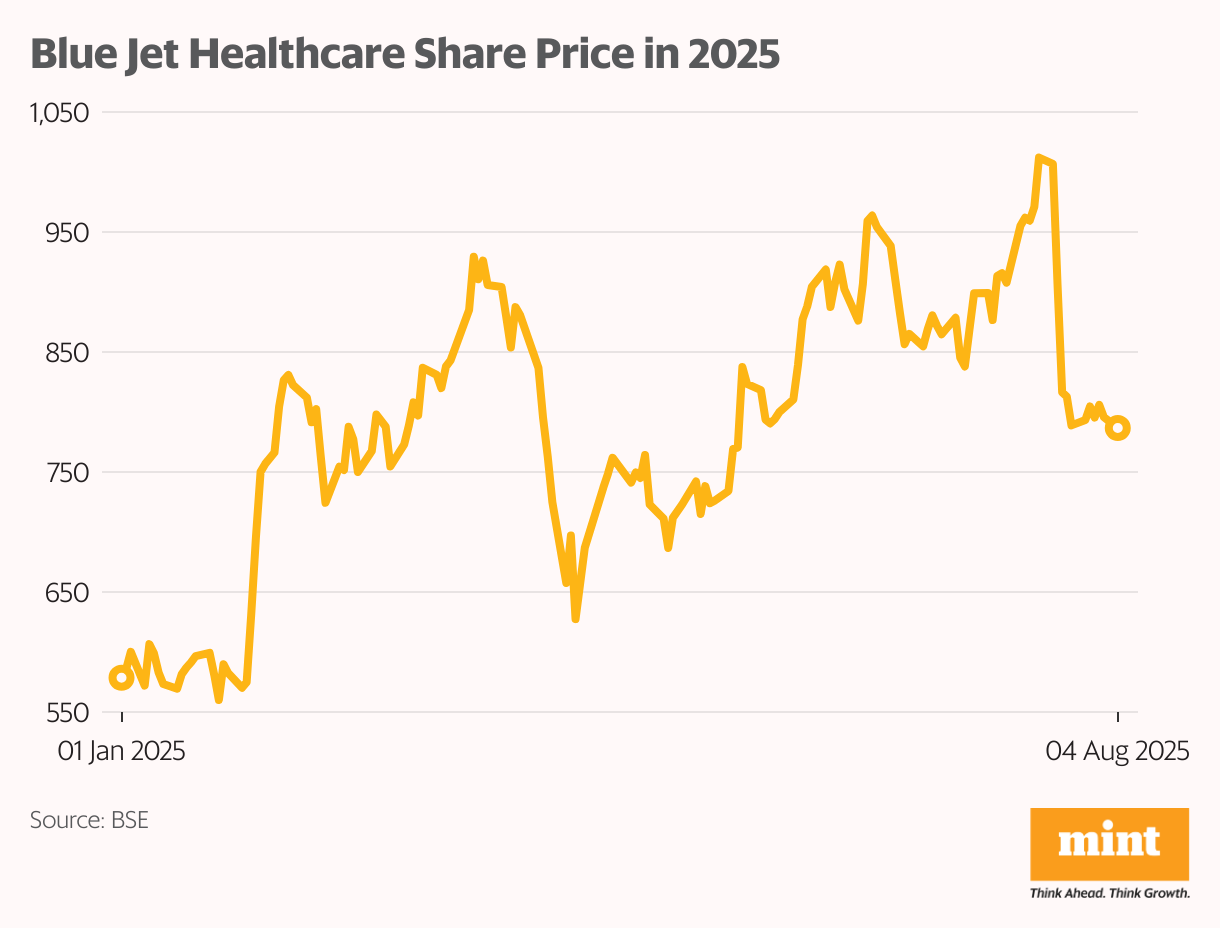

#3 Blue Jet Healthcare

Blue Jet Healthcare is a pharmaceutical and healthcare ingredient and intermediate company. It is the first manufacturer of saccharin and its salts (artificial sweeteners) in India.

Blue Jet Healthcare’s shares have climbed 36% in 2025, driven by improving growth prospects and renewed investor interest, but are currently 23.5% below their 52-week high. The stock is also up more than 100% since its listing in November 2023.

While financial performance was subdued between FY20 and FY24, mainly owing to a lack of new product launches, the company saw a sharp turnaround in FY25, when revenue rose 45% to ₹1,030 crore from ₹712 crore in FY24, supported by strong demand across key segments. Net profit jumped 86% to ₹305 crore from ₹164 crore in the previous year, reflecting higher operating leverage.

The company has also demonstrated strong capital efficiency, delivering an average RoE of 27% over the past three years. Its balance sheet remains conservative, with a debt-to-equity ratio of just 0.02.

The stock has come under pressure recently, falling over 12% in the past month after the company reported a sharp sequential decline in profit and margins for the June 2025 quarter.

Nevertheless, the company’s performance remained strong on a year-on-year basis: revenue surged 118%, while net profit grew 141.3%, led by a strong ramp-up in pharmaceutical ingredients and active pharmaceutical ingredients.

Management remains confident in its growth strategy, driven by capacity expansion, enhanced R&D capabilities, and a robust pipeline of high-value products.

Blue Jet plans to add 1,000 kiloliters of capacity over the next 2-3 years through a newly acquired land parcel to be developed in three phases. This will support a range of products including APIs, with a focus on the API for bempedoic acid, as well as capacity additions for contrast media intermediates (CMI) and high-intensity sweeteners.

The company is also deepening its R&D focus, allocating ₹40 crore to strengthening capabilities in amino acid derivatives and late-stage intermediates. It has built a robust pipeline of 20 high-interest opportunities, with around 30% (six candidates) already in the late phase 3 or commercial stage.

Brokerage firm Motilal Oswal has a ‘buy’ rating on the stock with a target price of ₹1,100. The brokerage expects pharma intermediates and APIs to continue their robust growth momentum in FY26, supported by strong customer demand visibility and additional product launches.

The stock appears attractively priced, currently trading at a PE of 38.1, below its historical average of 48.7.

FIIs and DIIs have both reduced their stakes in the company, albeit marginally, from 2.28% to 1.97% and 1.33% to 0.95% over the past quarter.

Even standout performers require research

While the broader market has been relatively muted in 2025, these three stocks stand out for their strong financial performance, strategic growth initiatives, and improving investor sentiment.

They’ve delivered solid returns despite broader volatility and still trade well below their 52-week highs, which makes them compelling stocks to watch.

However, it’s important to temper optimism with a dose of caution. Stocks that have corrected from their peaks may offer value, but can also remain under pressure if the company stumbled on execution or if market sentiment deteriorates further.

As always, investors should do their own due diligence, align investments with their risk tolerance and financial goals, and avoid chasing momentum blindly. Past performance is not always indicative of future outcomes, and in a market such as this, prudent stock selection and patience often make the real difference.

Ayesha Shetty is a research analyst registered with the Securities and Exchange Board of India. She is a certified financial risk manager (FRM) and is working toward her chartered financial analyst (CFA) designation.

Disclosure: The author does not hold shares in any of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers should conduct their own research and consult a financial professional before making investment decisions.