While its client base expanded by 31% during the quarter, revenue tanked by 19%. Thanks to EBDAT margin compressing from 38% to 22%, EBDAT saw an even sharper fall of 54% year-on-year, and profit after tax (PAT) dropped from ₹293 crore to ₹115 crore. EBDAT stands for earnings before depreciation, amortization, and taxes.

As one of the top five digital brokers in India, Angel’s performance raises questions about the overall industry’s health. Are the latest quarter’s troubles unique to Angel, or do they signal industry-wide stress?

What drove the shrinking top line?

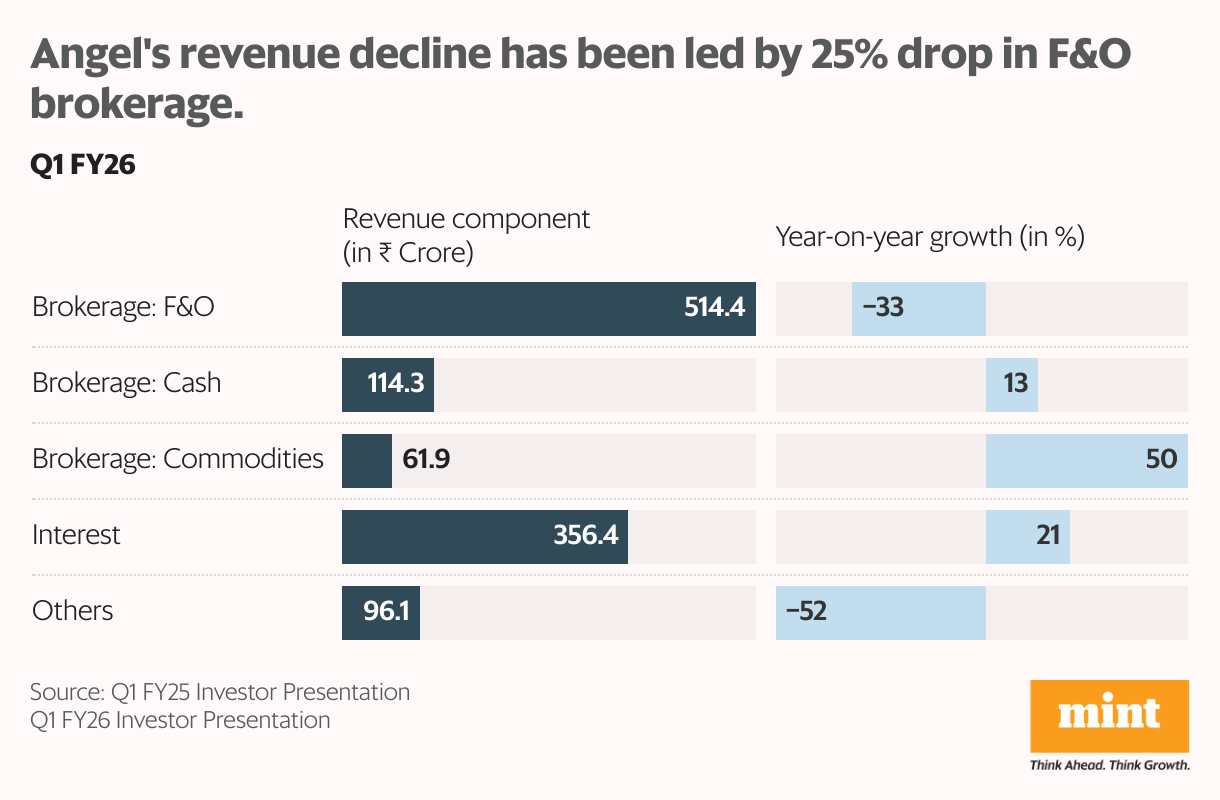

According to its investor presentation, Angel is engaged in broking, wealth management, asset management, mutual funds, credit, fixed deposits, and insurance. But a deeper look shows that more than 60% of its revenues come from brokerage, three-fourths of which are derived from the F&O segment.

Another 30% comes from interest income, which expanded by 21% over the same quarter of the last fiscal year. On the other hand, the largest component of its revenues—brokerage—declined by almost 25% from ₹917 crore in Q1FY25 to ₹691 crore in Q1FY26.

Within brokerage, cash and commodity brokerage have increased by 13% and 50% year-on-year. This is to say that once again, the largest component, F&O brokerage, is the culprit, having reported a 33% decline over Q1FY25. To drive the point home, consider this: F&O brokerage dropped by around ₹260 crore year-on-year, resulting in the ₹267 crore decline in overall revenues.

Has the regulator played a role?

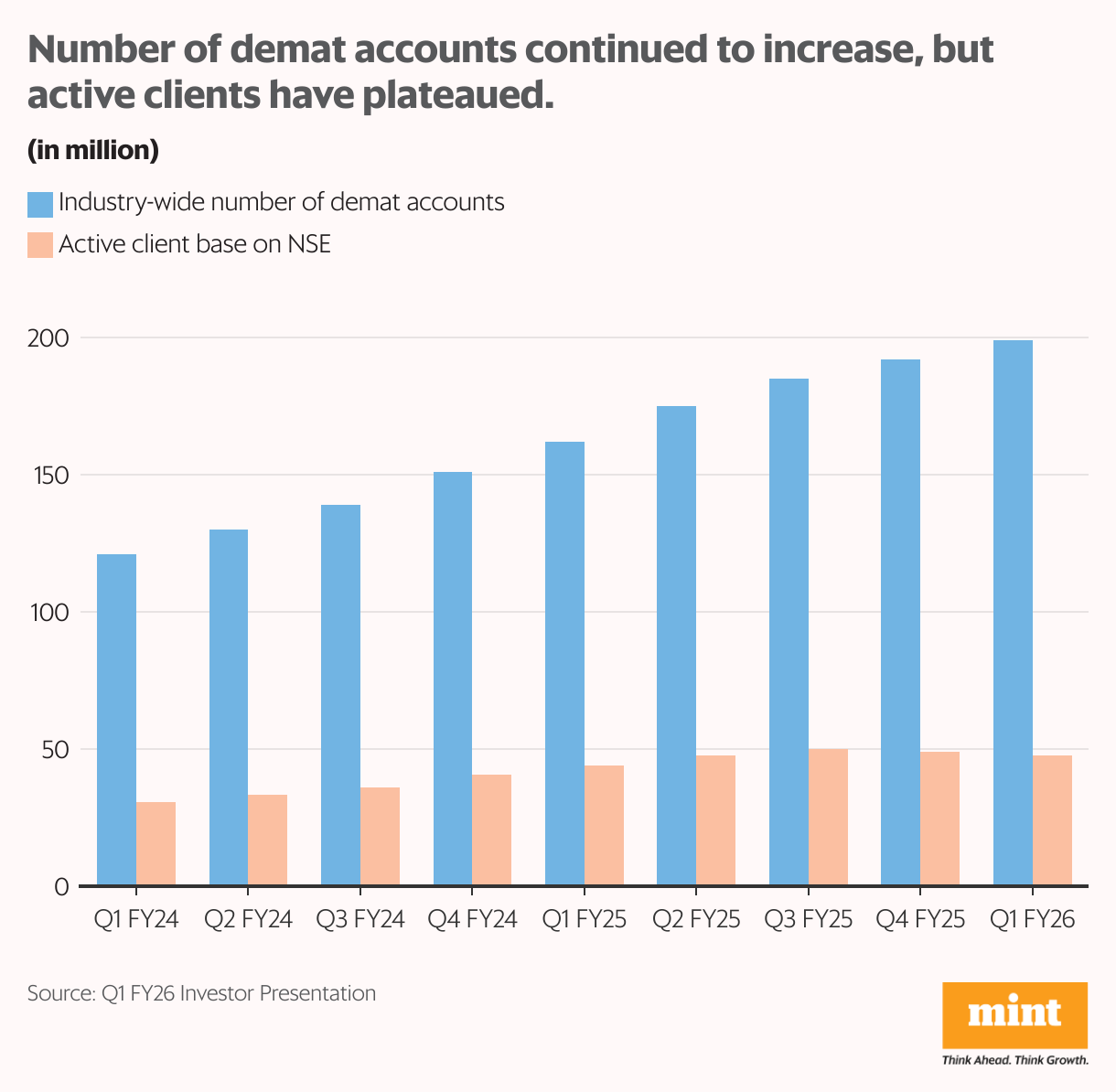

Following the pandemic, the number of demat accounts exploded from just about 40 million as of March 2020 to 190 million in FY25. A bulk of this increased participation came from index option trading. The seemingly unceasing appeal of derivative trading among retail investors has kept the Securities and Exchange Board of India (Sebi) on high alert. Since October 2024, the regulator has introduced several measures to curb speculative option trading.

It narrowed down on speculative expiry-day strategies as the home ground for most retail option traders. In response, it cut down the number of expiries from one every day to only one per exchange per week. It has also increased the option contract sizes and margin requirements to weed out smaller players. Upfront premium collection and intraday monitoring of position limits have also been mandated to track and control risk better.

Still, the number of demat accounts has continued to increase, almost touching 200 million in Q1FY26. But the number of active clients on the National Stock Exchange had peaked at around 50 million in December and has fallen to 48 million since then. It is important to note that Angel One has gained ground during the period, with its share of the retail equity turnover expanding from 18.9% in Q1FY25 to 19.6% in Q1FY26.

But the overall drop in trading volume has overshadowed the gains in market share. According to Zerodha’s cofounder, brokers across the board have witnessed trading activity decline to the tune of 30% over the past one year.

He highlighted the shallow nature of retail participation in Indian equities, which leaves volumes particularly vulnerable to market conditions and regulatory interventions. At Angel One, order volume crashed by 26% on-year in Q1FY26. Zerodha suffered the first degrowth in its business since it was founded 15 years ago.

Why did Angel’s profits drop sharply?

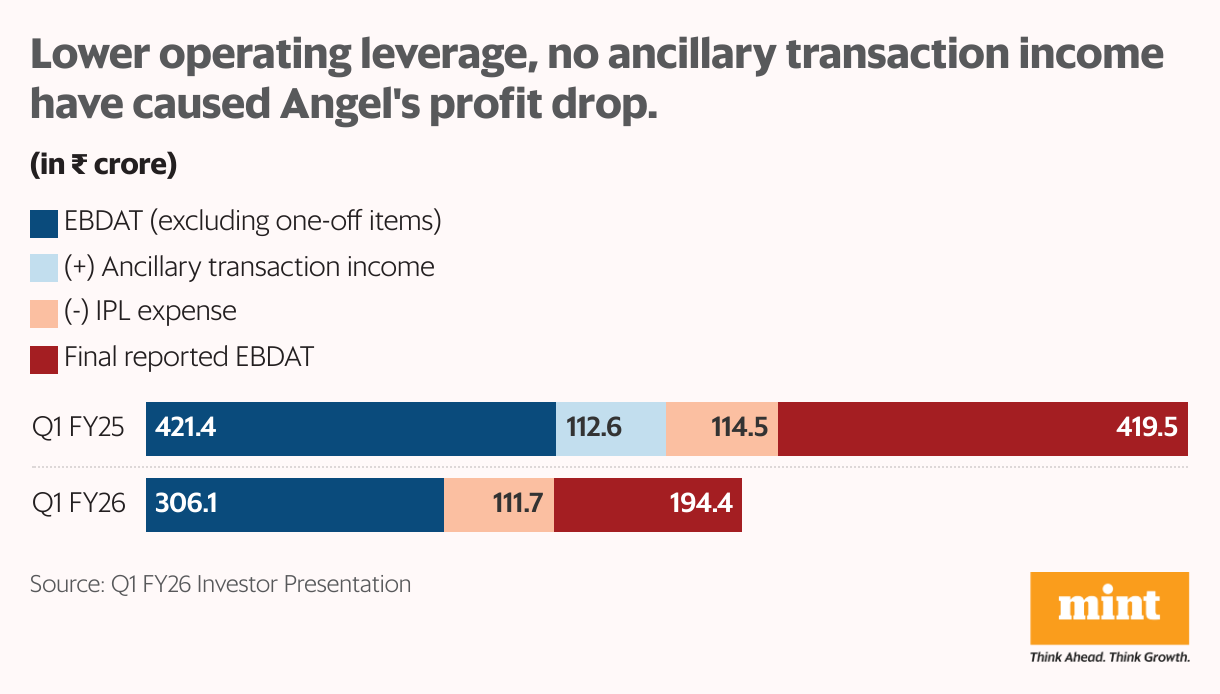

When revenues decline but sticky fixed costs like employee expenses persist, margins see some compression. This drop in operating leverage results in profits falling slightly more than revenues. Of the 16% points compression in Angel’s EBDAT margin from 38% to 22% over the past year, about 8% points can be explained by declining operating leverage. A rise in employee expenses may also have contributed.

The rest has come from one-off items, primarily due to regulatory impact. The company had reported ancillary transaction income worth ₹112 crore in Q1FY25, which is to blame for the higher base and consequent year-on-year decline. No such ancillary transaction income came to the margins’ rescue in Q1FY26, because of Sebi’s “true to label” regulation.

Exchanges used to charge brokers based on the turnover they brought to the table, with higher turnover being rewarded with lower charges. On Angel’s books, this discount in charges showed up as additional income, labelled as “ancillary transaction income”.

Sebi’s true-to-label regulation requires exchanges to charge brokers uniformly, irrespective of their turnover. Result? No more “expense-less” ancillary transaction income to boost Angel’s profitability.

This regulation impacts all large brokers, typically discount brokers like Angel One and Zerodha. Such brokers used to pass on the low exchange charges as brokerage discounts to end consumers, including retail investors. This would bring in more customers and drive up trading volumes, which would trigger the virtuous cycle leading to higher turnover and lower exchange charges. This business model is now at risk with the true-to-label regulation.

Medium-term outlook appears hazy

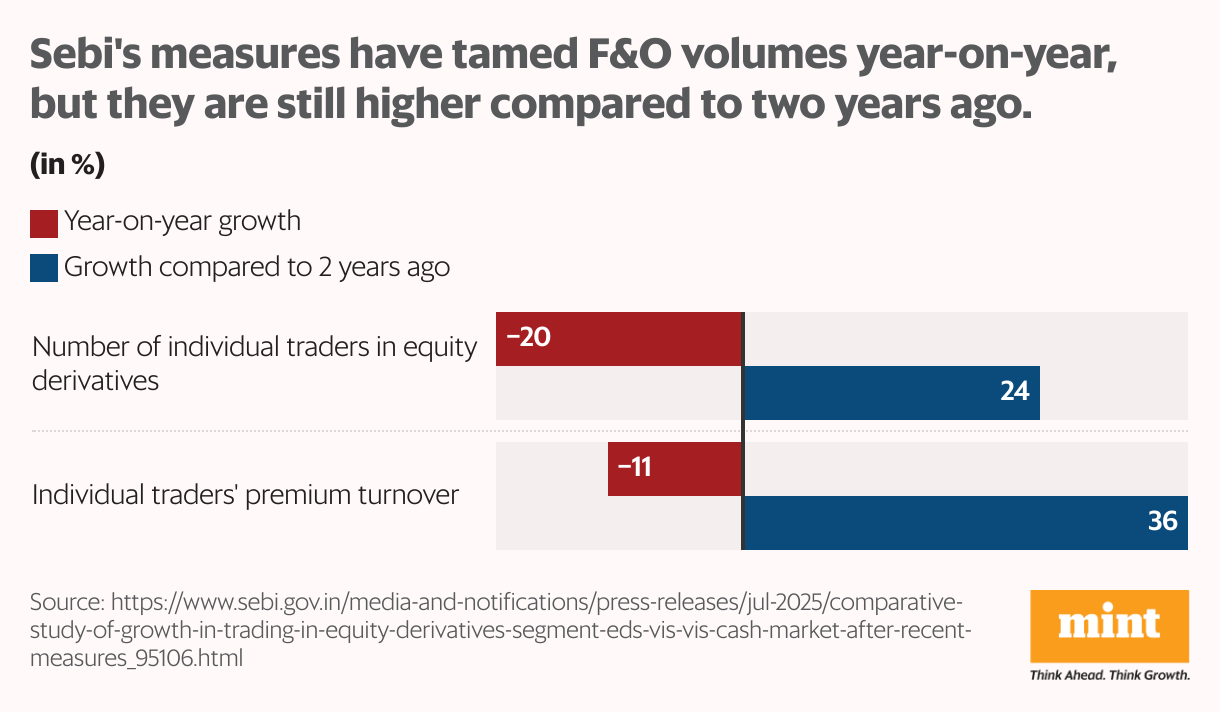

According to reports, derivatives volumes in India stand at more than 400 times the volumes in cash markets. This is the highest in the world, and Jane Street’s alleged scandal exposes the lacuna that arises as a result.

Furthermore, Sebi’s regulations have curbed volumes over the last year, but they are still high compared to two years ago. This is to say that Sebi is not done yet. More regulatory intervention is in the works, and could affect trading volumes and brokers’ prospects further.

This could be exacerbated by the second-order effect of Sebi’s true-to-label regulations. If the discount broking business model goes for a toss, it will have to be seen whether client acquisition keeps up with historical trends. Angel One’s gross client acquisition has dropped to 550,000 in June 2025, a 40% decline over the same month last year.

The company has been spending more than ₹100 crore per quarter on the Indian Premier League (IPL) spends, trying to make up for lost traction. This trend in the largest listed broker could be extrapolated across the industry. While the reportedly conservative players like Zerodha may cut back to an extent, marketing expenses are likely to go up for discount brokers going forward, leading to further compression of margins. Entry of deep-pocketed players in the industry could make matters worse for the incumbents.

That said, the diversification efforts are likely to soften the blow. At Angel One, several new businesses have taken flight. Loan distribution has already witnessed robust traction during the quarter, and the prospects appear promising for the distribution of FDs, wealth management, and AMC. These currently contribute only about 3% to the business revenues, but hold potential for growth. Increasing adoption of AI at nimble brokers which pride themselves on their fintech platforms, could also prove to be gamechangers.

Keeping in mind the regulatory uncertainty and cautious market sentiment, which counteract the promise of diversification, brokerages have pegged Angel One’s target price at ₹2,700 apiece. This is at par with current levels.

For more such analysis, read Profit Pulse.

Ananya Roy is the founder of Credibull Capital, a Sebi-registered investment adviser.

Disclosure: The author holds shares of some of the companies discussed. The views expressed are for informational purposes only and should not be considered investment advice. Readers are encouraged to conduct their own research and consult a financial professional before making any investment decisions.